Quick Navigation

Report Overview

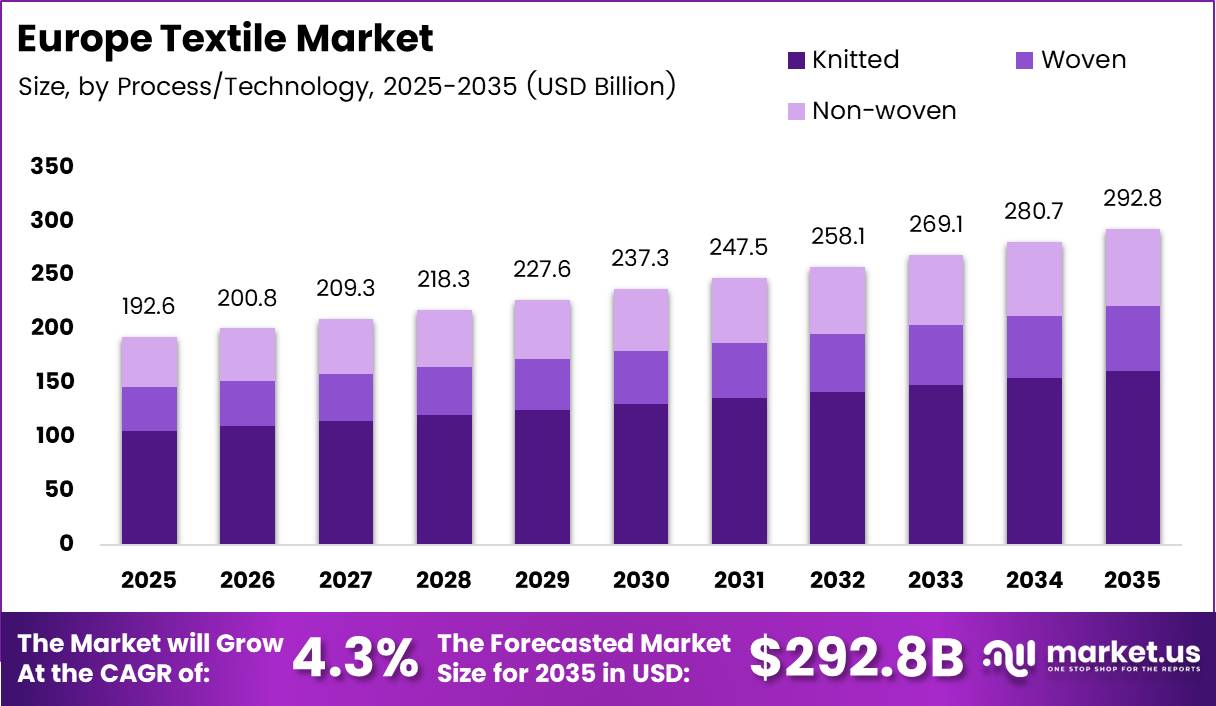

Europe Textile Market size is expected to be worth around USD 292.8 Billion by 2035 from USD 192.6 Billion in 2025, growing at a CAGR of 4.3% during the forecast period 2026 to 2035.

Europe’s textile industry occupies a structurally distinct position in global manufacturing. The region does not compete on volume with Asian producers. Instead, it holds pricing power through technical expertise, premium brand equity, and deep integration between fashion clusters and industrial textile networks. This dual-track model separates European producers from commodity-focused competition.

Technical textiles represent the highest-growth application layer within the European market. Automotive lightweighting, construction membranes, and medical-grade nonwovens all draw on Europe’s advanced fiber engineering capabilities. These segments carry higher margins than fashion textiles and are less exposed to price competition from low-cost imports. This structural mix makes Europe’s textile economy more resilient than headline figures suggest.

Sustainability policy is reshaping capital allocation across the industry. The EU’s Extended Producer Responsibility framework, incoming mandatory recycled content thresholds, and green public procurement rules are forcing manufacturers to invest in circular production infrastructure ahead of regulatory deadlines. Compliance timelines now function as a de facto market-entry barrier for producers without circularity infrastructure in place.

Public investment is accelerating the transition. In March 2025, the European Commission launched the Textiles of the Future partnership, committing €60 million for collaborative research and development in sustainable and high-performance textile technologies. This signals that institutional capital is now aligned with industrial transformation, not just research.

According to the EEA, EU citizens consumed 19 kg of clothing, footwear, and household textiles per person in 2022, up from 17 kg in 2019. This 11.8% increase in per-capita consumption over three years confirms that European end-market demand is expanding, not contracting. For manufacturers, this means top-line volume growth sits alongside the structural cost pressure of compliance investment.

According to the EEA, 73% of discarded textiles and shoes in the EU-27 in 2022 were incinerated or landfilled, with less than 30% going to reuse or recycling. This disposal pattern creates a precise commercial opportunity. Producers who build fiber recovery and closed-loop manufacturing capabilities now will capture both regulatory goodwill and the material cost savings that circular inputs provide at scale.

Key Takeaways

- The Europe Textile Market was valued at USD 192.6 Billion in 2025.

- The market is forecast to reach USD 292.8 Billion by 2035.

- The market grows at a CAGR of 4.3% from 2026 to 2035.

- By Raw Material, Natural Fibers dominate, led by Cotton with a 56.1% share in 2025.

- By Process/Technology, Knitted holds the leading position with a 54.3% share in 2025.

- Within Synthetic Fibers, Rayon/Viscose holds a 49.8% share among synthetic sub-segments.

- EU per-capita textile consumption reached 19 kg per person in 2022, up from 17 kg in 2019.

- 73% of discarded EU textiles were incinerated or landfilled in 2022, per the EEA.

- Less than 1% of all textiles worldwide are recycled into new textile products, per EEA.

- Between 60% and 70% of textiles placed on the European market are made of plastic fibres.

Raw Material Analysis

Cotton dominates with 56.1% due to broad apparel and home textile demand.

In 2025, Cotton held a dominant market position in the By Raw Material segment of the Europe Textile Market, with a 56.1% share. According to EEA data, cotton anchors European apparel and household textile production across both fast fashion and premium segments. Its versatility across weaving, knitting, and blended fabric systems makes it the default fiber choice for most mid-to-high volume manufacturers.

Wool serves Europe’s premium knitwear and technical insulation sectors. Italian, British, and German manufacturers use wool for luxury garments and high-performance outdoor textiles where synthetic alternatives cannot replicate the thermal or tactile properties. Wool’s premium positioning insulates these producers from price-driven competition at the mid-market level.

Silk operates within a narrow but high-value niche across European luxury fashion clusters. French and Italian fashion houses incorporate silk into seasonal collections where exclusivity and material heritage command significant price premiums. Volume is structurally limited, but margin contribution per unit is among the highest in the natural fiber category.

Polyester dominates synthetic fiber consumption across European industrial and fast-fashion applications. Its cost efficiency, dimensional stability, and compatibility with high-speed automated production systems make it the default synthetic input for mid-market apparel and technical textile manufacturers operating at scale.

Nylon serves specialty applications in activewear, automotive textiles, and protective workwear where tensile strength and abrasion resistance are non-negotiable requirements. European manufacturers producing performance sportswear and safety-grade fabrics maintain consistent nylon demand independent of broader fashion cycles.

Rayon/Viscose holds a 49.8% share within the synthetic fiber sub-segment. This reflects widespread adoption across mid-market fashion, lingerie, and lining fabrics where a soft drape and breathability are required at accessible price points. However, water-intensive production and chemical processing requirements are drawing regulatory scrutiny under EU sustainability frameworks.

Acrylic fills the lower-cost knitwear and upholstery segment across European markets. It competes directly with wool in price-sensitive categories while offering superior color retention and machine-washability. However, acrylic’s microplastic shedding profile creates growing compliance exposure under proposed EU microplastics regulations.

Polypropylene serves geotextile, agricultural fabric, and nonwoven hygiene product applications across European industrial and consumer markets. Its chemical inertness and low density make it the preferred fiber for technical applications where moisture resistance and structural durability outweigh aesthetic requirements.

Recycled Fibers represent the fastest-growing input category as EU Extended Producer Responsibility mandates and brand sustainability commitments push manufacturers to integrate post-consumer and post-industrial fiber streams. Investment in recycled fiber sorting and processing infrastructure is accelerating ahead of incoming mandatory recycled content thresholds across European markets.

Process/Technology Analysis

Knitted dominates with 54.3% due to versatility across apparel and active categories.

In 2025, Knitted held a dominant market position in the By Process/Technology segment of the Europe Textile Market, with a 54.3% share. Knitted fabric construction supports the full spectrum from high-stretch activewear to structured outerwear, giving manufacturers flexibility to serve multiple end markets from a single production platform. This broad application range underpins its majority position across European textile output.

Woven fabric production remains central to European luxury fashion, workwear, and technical textile manufacturing. Woven structures deliver the dimensional stability and surface definition required for tailored garments, protective textiles, and high-end home furnishing fabrics. Italian and French mills with heritage weaving expertise command price premiums that low-cost Asian competitors cannot easily replicate.

Non-woven fabrics serve industrial, medical, and hygiene product markets where bonded fiber structures outperform conventional weaving and knitting in terms of cost, sterility, and production speed. The European medical and hygiene nonwoven segment expanded structurally after the pandemic and has not fully contracted, sustaining above-average demand for nonwoven production capacity.

Spunlaid (Spunbond/Melt-blown) technologies produce continuous filament nonwovens used in medical protective clothing, filtration media, and geotextile applications. Melt-blown capacity in particular became a strategic asset during the COVID-19 pandemic and European manufacturers have retained and expanded this capability given its dual-use value across healthcare and industrial filtration.

Dry-laid Hydro-entangled processes produce high-strength, softness-optimized nonwovens used in premium wipes, filtration layers, and medical dressings. European nonwoven producers serving pharmaceutical and medical device OEMs use hydroentanglement to meet sterility and fiber purity specifications that commodity nonwoven imports cannot consistently achieve.

Wet-Laid nonwoven production serves specialty paper-textile hybrid applications including filtration, battery separators, and acoustic insulation panels for automotive interiors. The segment is technically concentrated, with a small number of European specialty manufacturers holding proprietary process expertise and long-term supply agreements with industrial end-users.

Needle-punched nonwovens are the workhorse of European geotextile, carpet backing, and automotive felt manufacturing. High production throughput and compatibility with recycled fiber inputs make needle-punching the preferred nonwoven process for cost-sensitive industrial applications where fiber purity requirements are lower than in medical or filtration end markets.

3-D Weaving & Spacer Fabrics represent the technical frontier of European textile manufacturing. Aerospace composite preforms, orthopedic support structures, and advanced protective gear use three-dimensional fabric architectures that flat-weaving cannot produce. European research institutes and specialist manufacturers hold significant IP in this segment, creating defensible positions against volume-focused Asian competition.

Application Analysis

Fashion & Apparel anchors European textile demand and serves as the primary commercial driver across the value chain from fiber to finished garment. Europe’s concentration of luxury fashion brands, mid-market fast fashion infrastructure, and premium sportswear manufacturers sustains consistent volume demand. However, margin pressure at the mid-market level is intensifying as nearshoring cost advantages erode against Asian export pricing.

Industrial/Technical Textiles represent the highest-margin application segment within the European market. Automotive composite fabrics, construction geotextiles, filtration media, and protective workwear all rely on technically specified fiber structures that standard apparel production cannot supply. European manufacturers in this segment operate with long-term OEM supply contracts, creating revenue visibility that fashion-oriented producers do not have.

Household & Home Textiles cover bedding, curtains, upholstery fabrics, and floor coverings where European consumers demonstrate consistent willingness to pay for quality and origin certification. German, Italian, and Portuguese home textile manufacturers compete on design, durability, and sustainability credentials rather than price, allowing them to hold margin against lower-cost import alternatives.

Medical & Healthcare Textiles serve surgical drapes, wound dressings, compression garments, and implantable fiber structures where regulatory approval and clinical performance data create high switching costs for hospital and healthcare procurement. European manufacturers supplying CE-marked medical textile products benefit from regulatory moats that effectively exclude unqualified competitors from entering this segment.

Automotive & Transport Textiles include seat fabrics, headliners, carpet systems, acoustic insulation layers, and structural composite preforms embedded in vehicle bodies. European automotive OEMs sourcing from regional textile suppliers benefit from just-in-time delivery logistics and quality traceability requirements that favor domestic supply chain integration over long-haul import sourcing.

Key Market Segments

By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

By Process/Technology

- Knitted

- Woven

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Premium Manufacturing Clusters and Technical Textile Expansion Drive Sustained Revenue Growth

Europe’s textile industry rests on geographically concentrated manufacturing clusters where fashion design, fiber engineering, and production expertise co-locate. Italian, French, and German clusters deliver products that command global price premiums. This cluster structure creates compounding advantages: skilled labor, supplier proximity, and shared infrastructure that individual manufacturers cannot replicate independently.

Technical textile applications in automotive, healthcare, and construction are widening the industry’s addressable market beyond traditional apparel. These applications require certified performance specifications and long-term OEM supply relationships. European manufacturers with established technical capabilities capture this demand at margins significantly above the apparel segment average.

In February 2026, Swiss spinning technology manufacturer Rieter successfully completed the acquisition of the Barmag Division from OC Oerlikon. This consolidation of precision spinning and filament winding technologies into a single European equipment group signals that producers are investing in vertical integration ahead of the next manufacturing cycle. According to the EEA, the share of separately collected EU-27 textile waste sent to incineration or landfill fell from 30% in 2010 to 26% in 2022. This 4-percentage-point reduction over 12 years confirms that circular infrastructure is building. Producers positioned within that recovery network gain material cost advantages as recovered fiber volumes scale.

Restraints

High Production Costs and Closed-Loop Recycling Gaps Compress Manufacturer Margins

European textile manufacturers face structural cost disadvantages against Asian competitors. Labor costs in Germany, France, and Italy are multiples of those in Bangladesh, Vietnam, and China. Energy costs amplified by the post-2022 energy price shock have added further pressure to dyeing, finishing, and spinning operations that run continuous high-temperature processes.

Stringent EU environmental compliance requirements add operational expenditure that Asian competitors do not carry. REACH chemical restrictions, wastewater discharge standards, and incoming mandatory sustainability reporting under the Corporate Sustainability Reporting Directive increase compliance overhead across the production chain. Smaller European mills face disproportionate cost burdens relative to large integrated producers who can spread compliance investment across higher output volumes.

According to the EEA, less than 1% of all textiles worldwide are recycled into new textile products. This near-total absence of closed-loop fiber recycling means manufacturers cannot offset raw material cost inflation with recovered fiber inputs at commercial scale. Until textile-to-textile recycling reaches viable industrial throughput, European producers remain exposed to virgin fiber price volatility while simultaneously absorbing compliance costs that competitors in unregulated markets do not face.

Growth Factors

Bio-Based Fiber Investment and Smart Textile Applications Open New Revenue Streams

Bio-based and recycled fiber production is transitioning from niche to mainstream as EU policy mandates and brand sustainability commitments create guaranteed offtake demand. Manufacturers who build fiber recovery and bio-based conversion infrastructure now are positioning ahead of mandatory recycled content thresholds that will create structural demand pull within the next regulatory cycle.

Smart textile applications in healthcare monitoring, military wearables, and occupational safety are creating product categories where European manufacturers compete on IP and performance rather than price. These categories carry significantly higher unit values than commodity apparel and create recurring revenue streams through sensor replacement, software integration, and service contracts that pure fabric manufacturers cannot access.

In June 2024, Lenzing partnered with Exponent Envirotech to launch ECOHUES, a waterless dyeing technology that significantly reduces dye and water consumption. This development signals that process innovation is directly targeting the highest environmental cost centers in textile production. According to an EEA-referenced briefing, between 4% and 9% of all textile products placed on the European market are destroyed without ever being used, with processing and destruction responsible for up to 5.6 million tonnes of CO₂-equivalent emissions. Eliminating pre-consumer waste alone would materially reduce both emissions liability and the input costs embedded in destroyed inventory.

Emerging Trends

Circular Manufacturing and Digital Production Systems Are Redefining European Textile Competitiveness

Circular textile manufacturing is moving from sustainability positioning to operational necessity as EU fiber recovery mandates take effect. Brands and manufacturers building fiber collection, sorting, and reprocessing infrastructure now will control the recovered material supply that compliance-driven competitors must source. First-movers in fiber recovery gain both cost and regulatory advantages as circular input volumes scale.

Digital printing and automated textile production systems are accelerating across European mills, reducing setup times, shortening minimum order quantities, and enabling on-demand production that reduces inventory waste. These capabilities directly address the cost structure that makes European manufacturing less competitive on volume. Automation allows European producers to compete on flexibility and speed-to-market rather than pure unit cost.

According to the EEA, between 60% and 70% of textiles placed on the European market are made of plastic fibres, primarily polyester. This majority share for fossil-based materials creates direct exposure to incoming EU microplastics and single-use plastics regulation. Manufacturers shifting toward bio-based and recycled synthetic alternatives are not only managing regulatory risk but are pre-positioning for a market where plastic-fiber textiles will face increasing trade and procurement restrictions.

Key Company Insights

Lenzing AG holds a structurally differentiated position in the European textile market through its TENCEL and ECOVERO branded fiber lines, which command premium pricing on sustainability certification. Lenzing’s vertical integration from pulp processing to finished fiber gives it direct control over the raw material quality and traceability claims that European fashion brands increasingly require as contractual supply conditions. Its partnership on ECOHUES waterless dyeing further extends this advantage into process innovation.

Worn Again Technologies is positioned at the highest-value intersection of European textile policy and material science. Its chemical recycling technology converts blended fiber textiles into virgin-equivalent polyester and cellulosic outputs, directly addressing the less than 1% global textile-to-textile recycling rate. First-mover IP in chemical recycling gives the company leverage in negotiations with major European brands facing mandatory recycled content obligations under incoming EU regulation.

Klopman International operates as a specialist supplier of high-performance workwear and protective fabrics to European industrial, defense, and public service procurement channels. Its focus on certified protective textiles creates revenue stability through long-term public and institutional supply contracts. This procurement structure insulates Klopman from the fashion cycle volatility that affects apparel-oriented manufacturers and reduces its sensitivity to consumer sentiment shifts.

Albini Group represents the premium fine shirting and luxury woven fabric segment where Italian manufacturing heritage translates directly into sustainable price premiums. The group’s customer base includes European and global luxury fashion houses with multi-season supply commitments. This long-term brand relationship model generates revenue predictability that commodity fabric manufacturers cannot replicate. In January 2024, BASF and Inditex introduced Loopamid, the first circular nylon 6 made entirely from textile waste, signaling that chemical company and brand partnerships are now producing commercially viable circular inputs that specialty fabric producers like Albini must integrate to maintain luxury ESG positioning.

Key Players

- Lenzing AG

- Worn Again Technologies

- Klopman International

- Albini Group

- Schoeller Textil AG

- Borges International Group

- Marzotto Group

- Gebrüder Otto

- ITV Denkendorf Produktservice GmbH

Recent Developments

- August 2025 – Albany International Corp. finalized the €132 million acquisition of Germany-based Heimbach Group, a major supplier of high-tech paper machine clothing and technical textiles, strengthening Albany’s European technical textile footprint.

- August 2025 – Authentic Brands Group acquired a 51% stake in the intellectual property of Guess Inc. as part of a strategic $1.4 billion transaction, expanding its European fashion brand licensing portfolio.

- October 2024 – Zara parent company Inditex allocated €50 million to a specialized fund targeting textile innovation and environmental impact reduction, reinforcing its commitment to circular supply chain development in European sourcing networks.

- October 2025 – Sages, a British startup developing biobased textile dyes derived from food waste, secured £190,000 in seed financing from the British Design Fund, validating early commercial interest in non-petrochemical dye alternatives.

- October 2024 – Reju opened Regeneration Hub Zero in Frankfurt, establishing its first commercial-scale textile-to-textile recycling plant in Germany, marking a milestone in European closed-loop fiber recovery infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 192.6 Billion |

| Forecast Revenue (2035) | USD 292.8 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Natural Fibers: Cotton, Wool, Silk; Synthetic Fibers: Polyester, Nylon, Rayon/Viscose, Acrylic, Polypropylene, Recycled Fibers, Others), By Process/Technology (Knitted, Woven, Non-woven: Spunlaid, Dry-laid Hydro-entangled, Wet-Laid, Needle-punched, 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Lenzing AG, Worn Again Technologies, Klopman International, Albini Group, Schoeller Textil AG, Borges International Group, Marzotto Group, Gebrüder Otto, ITV Denkendorf Produktservice GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |