Global Enterprise WLAN Market Size, Share and Analysis Report By Component (Hardware, Software, Services), By Deployment Mode (On-premises, Cloud-managed), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SME), By End-user Vertical (Banking, Financial Services and Insurance, Healthcare, Retail, IT and Telecommunications, Manufacturing, Education, Hospitality, Other Verticals), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178350

- Number of Pages: 370

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Insights Summary

- Drivers Impact Analysis

- Restraint Impact Analysis

- Investor Type Impact Matrix

- By Component

- By Deployment Mode

- By Organization Size

- By End-user Vertical

- Regional Overview

- Increasing Adoption Technologies

- Investment Opportunities

- Emerging Trend Analysis

- Key Market Segments

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

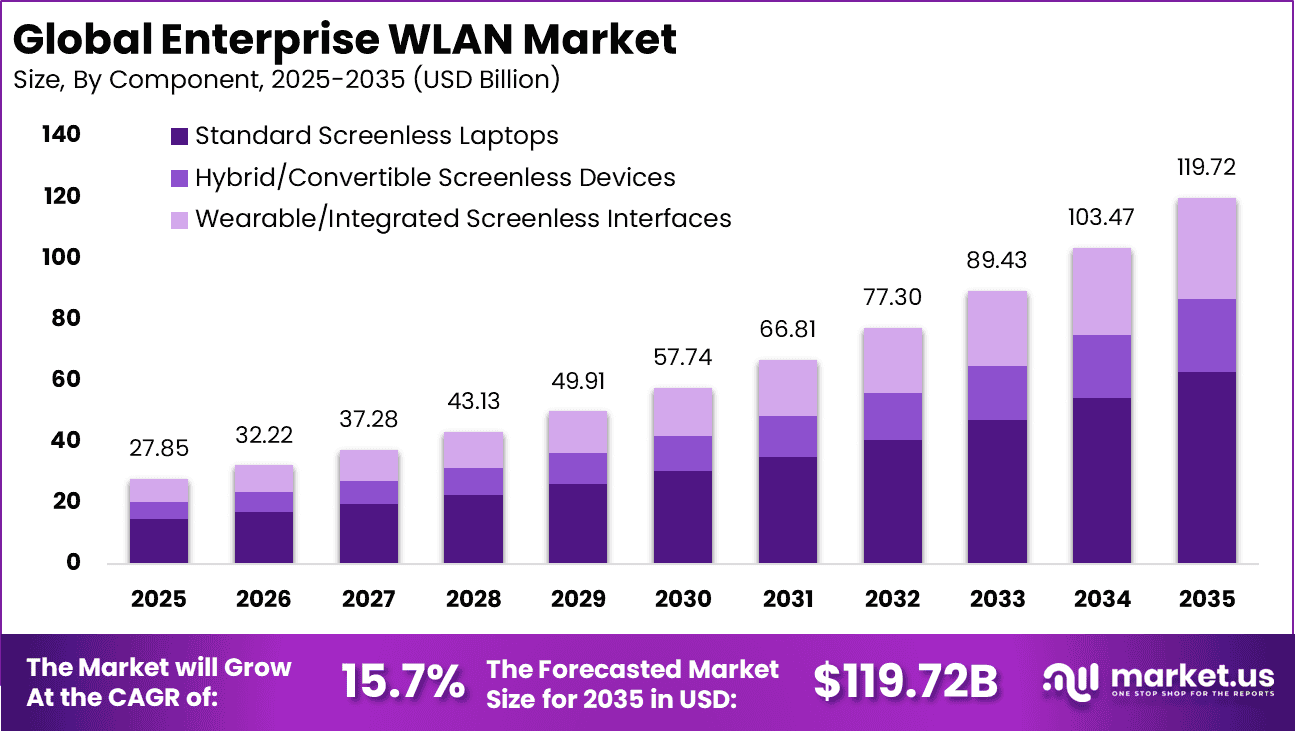

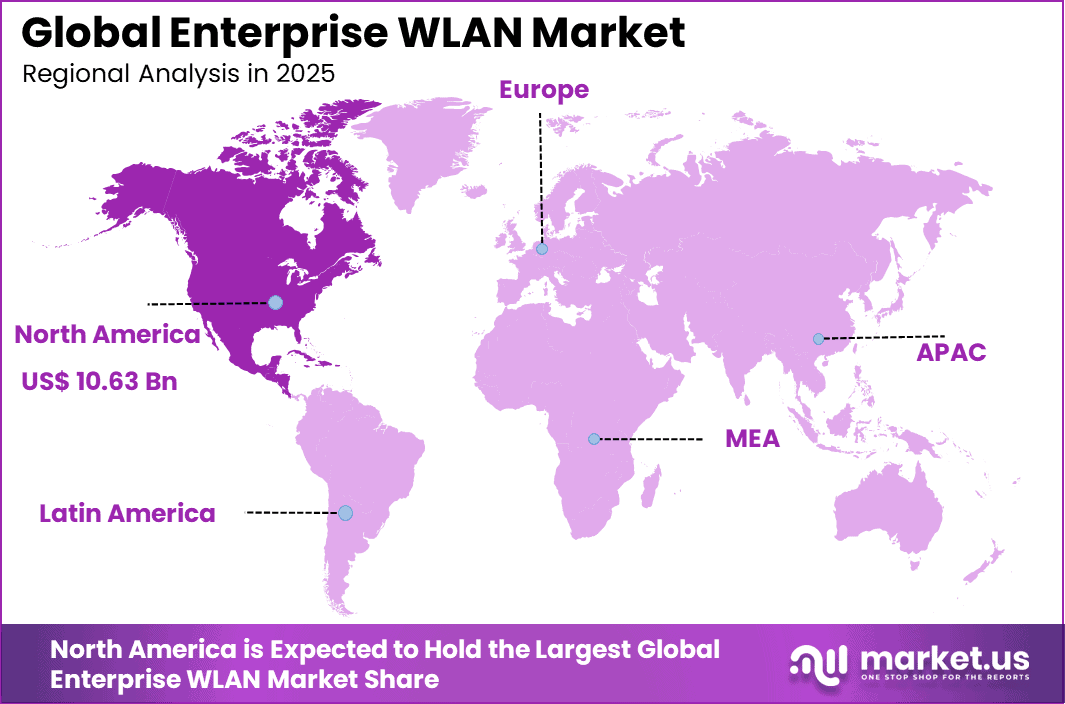

The Global Enterprise WLAN Market size is expected to be worth around USD 119.72 billion by 2035, from USD 27.85 billion in 2025, growing at a CAGR of 15.7% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.2% share, holding USD 10.63 billion in revenue.

The Enterprise WLAN Market refers to wireless local area network solutions designed to support connectivity within business environments. These solutions include access points, controllers, software management tools, and security features that enable reliable and secure wireless communication for employees and connected devices. Enterprise WLAN technology ensures high performance connectivity across office spaces, campuses, and large facilities.

This market has grown steadily due to rising demand for seamless wireless connectivity and enhanced user experiences. Organizations require robust WLAN platforms to support business operations, cloud access, and real time communication tools. The shift to hybrid work models and mobile device proliferation has further driven the adoption of enterprise grade WLAN solutions. Reliable wireless networks are seen as essential to maintain productivity and support digital transformation initiatives.

One key driving factor for the Enterprise WLAN Market is the increasing need for high speed, uninterrupted connectivity within corporate environments. With the growth in bandwidth intensive applications such as video conferencing, cloud services, and virtual collaboration tools, traditional wired infrastructures are no longer sufficient. WLAN solutions provide scalable wireless access to meet these evolving needs. This has pushed organizations to upgrade existing network infrastructure to support performance requirements.

Demand for enterprise WLAN solutions is evident across sectors such as education, healthcare, corporate offices, hospitality, and retail. Institutions with large campuses require widespread wireless coverage to support diverse users and devices. In healthcare, WLAN is critical for accessing patient records, mobile diagnostic tools, and real time communication. Retail environments leverage WLAN for point of sale systems, inventory management, and customer engagement through connected services.

For instance, in May 2025, Extreme Networks launched ExtremeCloud Universal Zero Trust Network Access and Extreme Platform ONE, merging networking and security into a unified AI-powered control plane for enterprise WLAN deployments.

Key Takeaway

- In 2025, the Hardware segment led the Global Enterprise WLAN Market with a 52.6% share, reflecting sustained demand for access points, controllers, and advanced networking equipment.

- The On-premises deployment model accounted for 64.7% of the market, as enterprises prioritized network control, security management, and regulatory compliance within internal infrastructures.

- Large Enterprises represented 72.8% of total market share, supported by extensive campus networks, high device density, and large-scale digital transformation initiatives.

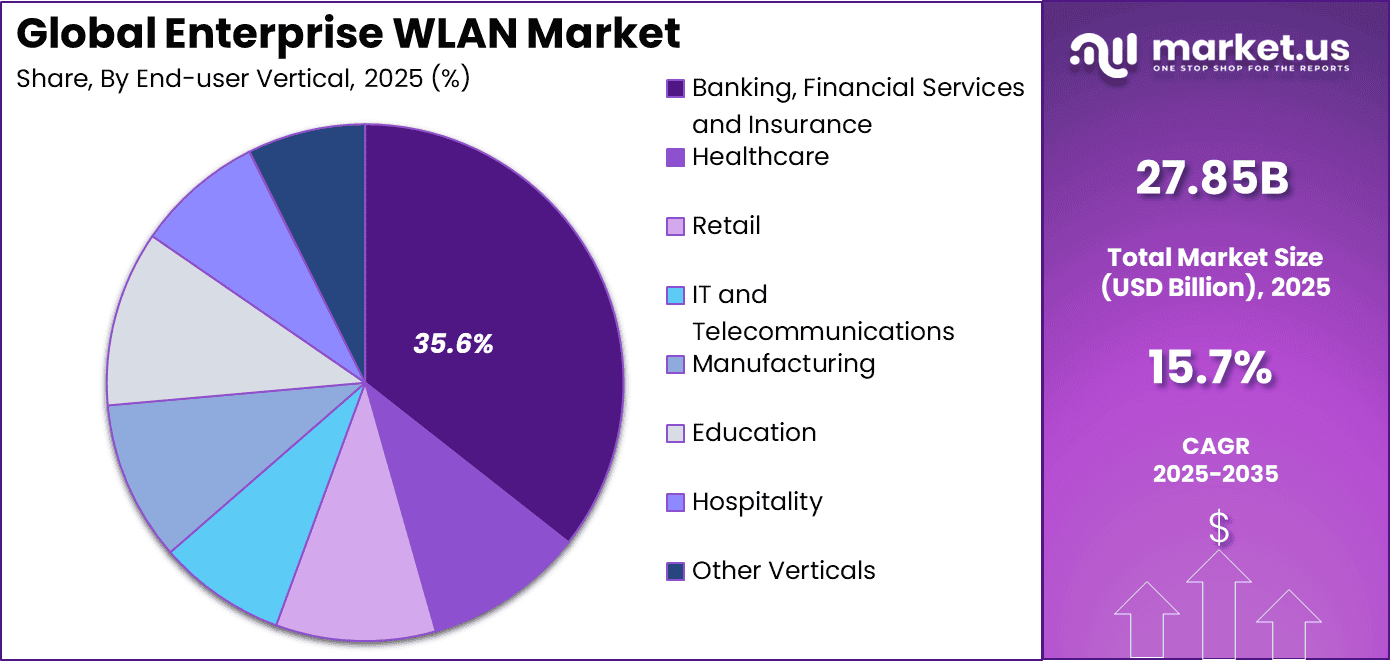

- The Banking, Financial Services, and Insurance sector captured 35.6%, driven by strict security requirements, secure wireless access for branch operations, and growing digital banking services.

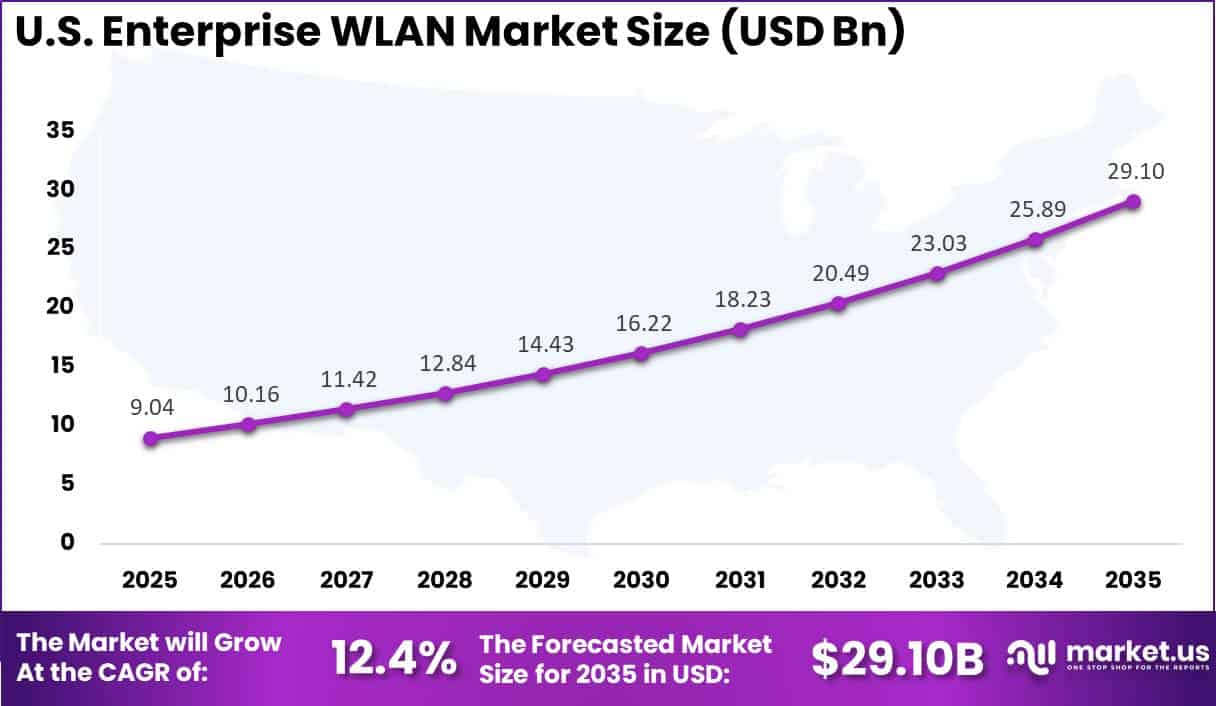

- The U.S. Enterprise WLAN Market was valued at USD 9.04 billion in 2025, expanding at a CAGR of 12.4%, supported by modernization of enterprise networks and rising Wi-Fi 6 and Wi-Fi 7 adoption.

- North America maintained a leading position with over 38.2% of the global market share in 2025, backed by advanced IT infrastructure, high enterprise IT spending, and early adoption of next-generation wireless technologies.

Key Insights Summary

- Enterprise WLAN standards are transitioning from Wi-Fi 6E to Wi-Fi 7 (802.11be), as major vendors expand full-scale enterprise portfolios.

- Wi-Fi 7 accounted for approximately 11.8% of dependent access point revenues by Q1 2025. Shipments are projected to reach 66.5 million units in 2025 and increase to nearly 117.9 million units in 2026, indicating rapid commercialization.

- Wi-Fi 6E represented 31.9% of dependent access point revenues in early 2025. Growth is expected to moderate as Wi-Fi 7 shipments begin to surpass 6E by mid-2025.

- Wi-Fi 6 and 6E combined continue to hold 52.3% of active user samples, while legacy standards such as Wi-Fi 5 (33%) and Wi-Fi 4 (13%) are gradually declining.

- In enterprises where the 6 GHz spectrum is enabled, client adoption ranges between 20% and 50%, reflecting progressive migration to higher-capacity bands.

- Currently, 5% to 10% of enterprise devices are Wi-Fi 7 capable. This base is expected to expand significantly, supported by more than 1,200 compatible device models, including AI-enabled PCs and premium smartphones.

- Cloud-managed WLAN continues to expand at a 17.66% CAGR, supported by growing enterprise reliance on cloud workloads.

- By 2025, approximately 60% of organizations are expected to run more than half of their workloads in the cloud, increasing demand for high-performance wireless infrastructure.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Increasing enterprise mobility and hybrid work adoption +3.9% North America, Europe Short to medium term Rapid deployment of Wi-Fi 6 and Wi-Fi 7 infrastructure +3.5% North America, Asia Pacific Medium term Growing IoT device density across campuses and facilities +3.1% Global Medium term Rising demand for high-speed, low-latency connectivity +2.8% Global Medium term Expansion of digital transformation across industries +2.4% Asia Pacific, North America Medium to long term Restraint Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High infrastructure upgrade and deployment costs -3.0% Emerging Markets Short to medium term Network security vulnerabilities and cyber risks -2.6% Global Medium term Complexity in managing dense wireless environments -2.3% North America, Europe Medium term Limited IT budgets in small enterprises -2.0% Asia Pacific, Latin America Medium term Interference and spectrum congestion challenges -1.7% Urban regions globally Medium to long term Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Enterprise networking equipment vendors Very High Medium North America, Asia Pacific Infrastructure refresh cycle opportunity Managed network service providers High Medium Global Recurring service contracts Semiconductor and chipset manufacturers High Medium Asia Pacific Wi-Fi 6 and 7 enablement Private equity firms Medium Medium North America, Europe Consolidation of networking vendors Venture capital investors Medium High North America Innovation in AI-driven network management By Component

Hardware accounts for 52.6% of the enterprise WLAN market, reflecting the foundational role of access points, controllers, and networking devices in wireless infrastructure. Enterprises continue to invest in high-performance wireless equipment to support growing data traffic and connected devices. The expansion of mobile workforces and cloud-based applications has increased demand for reliable and high-speed connectivity.

Modern hardware solutions are designed to support higher bandwidth and improved signal coverage. This sustained infrastructure demand supports hardware’s leading position in the market. Advanced hardware deployments also enable enhanced network security and traffic management. Features such as integrated firewalls, network segmentation, and device authentication strengthen enterprise security frameworks.

Upgrades to next-generation wireless standards further improve performance and reduce latency. Organizations prioritize hardware modernization to ensure stable connectivity across offices, campuses, and branch networks. These technical requirements explain the strong share held by hardware components.

For Instance, in December 2025, Cisco launched new Wi-Fi 7 access points and an updated wireless controller at its Partner Summit, boosting hardware performance for high-density enterprise networks. These devices offer higher throughput and efficiency, helping businesses handle AI workloads and edge computing demands. This move strengthens Cisco’s hardware dominance as companies upgrade for faster, reliable connectivity.

By Deployment Mode

On-premises deployment represents 64.7% of the enterprise WLAN market. Many organizations prefer on-premises infrastructure to maintain direct control over network configuration, data traffic, and security policies. This approach is particularly relevant for industries with strict compliance requirements. On-premises WLAN systems allow enterprises to manage performance and security within their own facilities.

The need for low-latency and uninterrupted connectivity also supports this deployment model. Enterprises often deploy centralized network controllers to manage multiple access points across locations. This ensures consistent policy enforcement and network visibility.

On-premises setups also allow customization based on operational requirements. Organizations with large campuses or high-security environments continue to prioritize in-house network management. The strong emphasis on control and compliance sustains demand for on-premises WLAN solutions.

For instance, in December 2025, HPE rolled out Aruba Central On-Premises 3.0, blending AI ops and automation for secure, local management without cloud reliance. It provides proactive alerts and client insights in a redesigned interface, ideal for enterprises needing control in regulated environments. This supports on-premises growth amid hybrid setups.

By Organization Size

Large enterprises account for 72.8% of the enterprise WLAN market. These organizations operate across multiple sites and require scalable wireless networks to support thousands of users. Reliable connectivity is essential for collaboration tools, cloud applications, and digital workflows. Enterprise-scale WLAN systems ensure consistent performance and centralized management.

High device density environments further increase infrastructure requirements. Large enterprises also prioritize advanced security and network monitoring capabilities. WLAN platforms integrate analytics tools to track usage patterns and optimize bandwidth allocation.

Centralized management simplifies troubleshooting and maintenance across regional offices. Investments in network modernization align with broader digital transformation strategies. The operational complexity of large organizations explains their dominant share in this segment.

For Instance, in October 2025, Cisco earned Leader status in IDC MarketScape for Enterprise WLAN, highlighting its options for large-scale deployments across campuses. Features like Meraki and Catalyst platforms unify management for multi-site operations, aiding big firms in scaling secure networks. This recognition underscores the appeal to Fortune-level buyers.

By End-user Vertical

The Banking, Financial Services and Insurance sector represents 35.6% of the enterprise WLAN market. Financial institutions require secure and stable wireless connectivity to support digital banking operations and internal workflows. WLAN infrastructure enables seamless communication across branches, headquarters, and customer service centers.

High network reliability is essential to process transactions and maintain data integrity. Security remains a primary consideration in this vertical. Banks and financial institutions implement strong encryption and access control mechanisms within WLAN environments.

Secure wireless networks support mobile banking operations and customer engagement services. Real-time monitoring reduces the risk of unauthorized access and service disruptions. Compliance with regulatory standards further drives investment in advanced WLAN solutions. The sector’s reliance on secure digital infrastructure supports its leading share.

For Instance, in May 2025, at Huawei’s Intelligent Finance Summit, it unveiled the upgraded Xinghe Intelligent Financial Network with AI-powered devices for banking resilience. Integrated with NetMaster, it tackles scale, regulations, and security, enabling automation and a secure WLAN for branches. This bolsters BFSI’s lead in wireless adoption.

Regional Overview

North America accounts for 38.2% of the global enterprise WLAN market. The region benefits from advanced IT infrastructure and widespread adoption of wireless technologies. Enterprises continue to modernize networks to support hybrid work models and high data usage. Investment in digital transformation initiatives strengthens demand for reliable WLAN systems.

For instance, in December 2025, Cisco unveiled Wi-Fi 7 hardware and unified management at the San Diego Partner Summit, targeting US enterprises. New APs and controllers aid AI infrastructure, with WWT winning US awards for deployments boosting North American leadership.

The United States leads regional growth with a market value of USD 9.04 Bn and a CAGR of 12.4%. Businesses across finance, healthcare, retail, and technology sectors are expanding wireless network capacity. Upgrades to high-speed wireless standards are accelerating across corporate campuses. Strong enterprise IT spending continues to support steady market expansion. North America remains a key contributor to global enterprise WLAN development.

Increasing Adoption Technologies

Cloud managed WLAN platforms are increasingly adopted due to their centralized management, scalability, and remote configuration capabilities. These platforms allow IT teams to monitor performance, apply policies, and troubleshoot issues from a unified interface. Integration with artificial intelligence powered analytics helps in optimizing network performance and predicting potential connectivity issues. Such automation improves user experience and reduces manual intervention for routine network tasks.

Wi Fi 6 and Wi Fi 6E technologies are being deployed widely to support higher data rates, increased device capacity, and reduced latency in dense environments. These advancements provide enhanced throughput and improved spectral efficiency compared to earlier standards. WLAN solutions are also incorporating advanced security protocols and encryption mechanisms to safeguard network traffic.

Investment Opportunities

Investment opportunities in the Enterprise WLAN Market are present in technology development, service offerings, and network analytics capabilities. Vendors are innovating in cloud based management platforms, intelligent network optimization tools, and enhanced security modules. There is growing interest in solutions that integrate advanced analytics and machine learning to anticipate network demands and automate performance adjustments.

Managed WLAN services represent an area for investment as organizations seek expertise in deployment, monitoring, and troubleshooting. Service providers offering subscription based models can attract businesses looking to reduce internal IT burden. Furthermore, investment in training and certification programs for WLAN implementation and security can support broader adoption.

Emerging Trend Analysis

A key emerging trend in the Enterprise WLAN market is the accelerated deployment of Wi-Fi 6E and the preparatory adoption of Wi-Fi 7 standards across enterprise environments to support higher bandwidth and reduced latency requirements. Enterprises are increasingly upgrading their WLAN infrastructure to accommodate the growing number of connected devices, including IoT endpoints and high-resolution video conferencing systems, which demand robust and consistent wireless performance.

This transition is being driven by the need to provide seamless user experiences in hybrid work settings and digital campus environments where performance degradation can directly affect productivity. The integration of cloud-based management and AI-enabled network analytics is also contributing to smarter WLAN operations, enabling predictive maintenance and automated troubleshooting that improve network reliability and scalability.

Furthermore, the trend toward zero-trust security frameworks is influencing WLAN solution offerings, as enterprises seek to embed advanced access control and device posture validation into wireless networks. This trend reflects broader security imperatives within enterprise networking to mitigate unauthorized access and protect sensitive data traversing WLAN environments.

Key Market Segments

By Component

- Hardware

- Access Points

- WLAN Controllers

- Wireless Hotspot Gateways

- Others

- Software

- WLAN Security

- WLAN Management

- WLAN Analytics

- Other Software

- Services

- Professional Services

- Managed Services

By Deployment Mode

- On-premises

- Cloud-managed

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SME)

By End-user Vertical

- Banking, Financial Services, and Insurance

- Healthcare

- Retail

- IT and Telecommunications

- Manufacturing

- Education

- Hospitality

- Other Verticals

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Established networking leaders such as Cisco Systems, Hewlett Packard Enterprise, Huawei Technologies, Juniper Networks, and Extreme Networks dominate the enterprise WLAN market. Their portfolios include access points, controllers, and AI-driven network management platforms. These vendors emphasize cloud-managed WLAN, zero-touch provisioning, and advanced security controls.

Network infrastructure and secure connectivity providers such as CommScope, Arista Networks, Fortinet, and Dell Technologies strengthen WLAN deployment in campus and branch environments. Alcatel-Lucent Enterprise and Zebra Technologies support vertical-specific solutions. Adoption is supported by Wi-Fi 6 and Wi-Fi 7 upgrades and rising IoT integration.

Cost-effective and regional vendors such as Ubiquiti Inc., TP-Link Technologies, Ruijie Networks, Cambium Networks, EnGenius Networks, and Netgear address SME and education sectors. These players focus on affordability and simplified management. Other vendors enhance competitive intensity, supporting continued growth of enterprise WLAN deployments globally.

Top Key Players in the Market

- Cisco Systems

- Hewlett Packard Enterprise

- Aruba

- Huawei Technologies

- Juniper Networks (Mist)

- Extreme Networks

- CommScope – Ruckus

- Dell Technologies

- Fortinet

- Ubiquiti Inc.

- Arista Networks

- Cambium Networks

- Zebra Technologies

- Netgear

- TP-Link Technologies

- Arista Networks

- Ruijie Networks

- Alcatel-Lucent Enterprise

- Huawei Technologies

- EnGenius Networks

- Cambium Networks

- Others

Recent Developments

- In October 2025, Huawei Technologies expanded Wi-Fi 7 deployments in Asia-Pacific despite challenges, maintaining a top-3 global share with integrated 5G/WLAN solutions. Their enterprise APs emphasized energy efficiency and dense IoT support, capturing growth in emerging markets.

Report Scope

Report Features Description Market Value (2025) USD 27.85 Bn Forecast Revenue (2035) USD 119.7 Bn CAGR(2026-2035) 15.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware, Software, Services), By Deployment Mode (On-premises, Cloud-managed), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SME), By End-user Vertical (Banking, Financial Services and Insurance, Healthcare, Retail, IT and Telecommunications, Manufacturing, Education, Hospitality, Other Verticals) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Cisco Systems, Hewlett Packard Enterprise, Aruba, Huawei Technologies, Juniper Networks (Mist), Extreme Networks, CommScope – Ruckus, Dell Technologies, Fortinet, Ubiquiti Inc., Arista Networks, Cambium Networks, Zebra Technologies, Netgear, TP-Link Technologies, Arista Networks, Ruijie Networks, Alcatel-Lucent Enterprise, Huawei Technologies, EnGenius Networks, Cambium Networks, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Cisco Systems

- Hewlett Packard Enterprise

- Aruba

- Huawei Technologies

- Juniper Networks (Mist)

- Extreme Networks

- CommScope - Ruckus

- Dell Technologies

- Fortinet

- Ubiquiti Inc.

- Arista Networks

- Cambium Networks

- Zebra Technologies

- Netgear

- TP-Link Technologies

- Arista Networks

- Ruijie Networks

- Alcatel-Lucent Enterprise

- Huawei Technologies

- EnGenius Networks

- Cambium Networks

- Others

Our Clients

- 178350

- Feb. 2026