Global ENT endoscopy Market By Product Type (Hearing screening devices, Flexible Endoscopes and Rigid Endoscopes), By Applications (ENT clinics, Ambulatory settings and Hospitals), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179002

- Number of Pages: 302

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

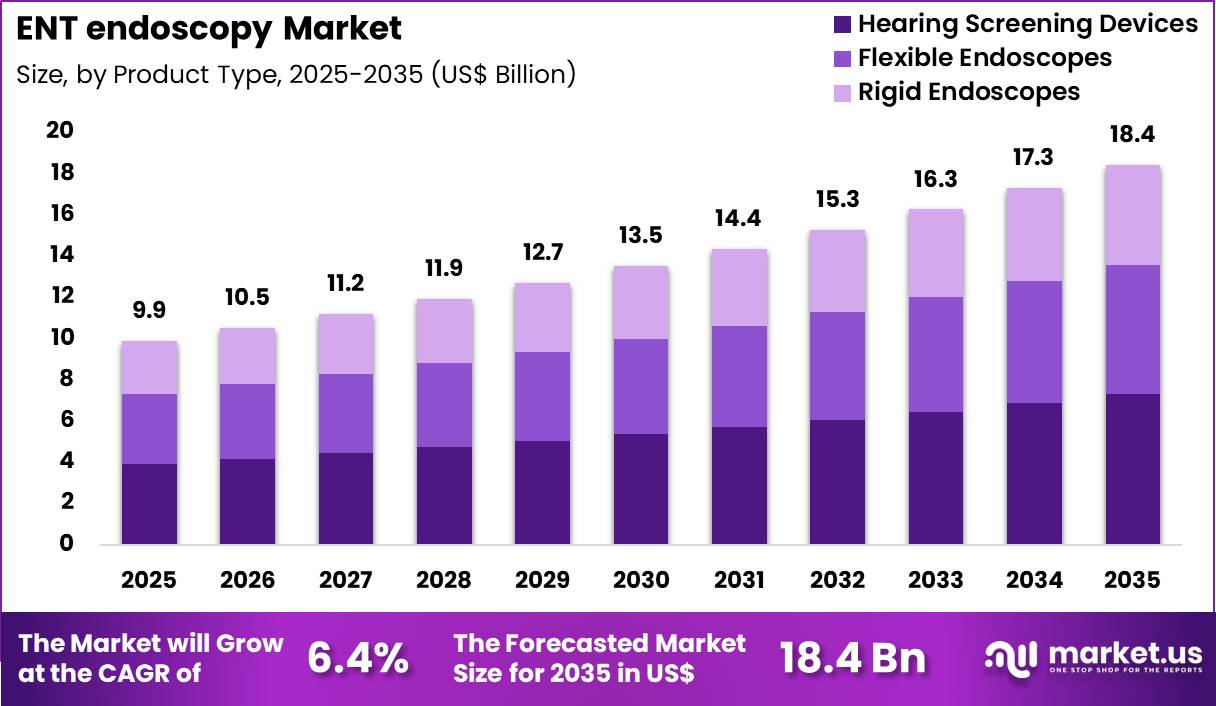

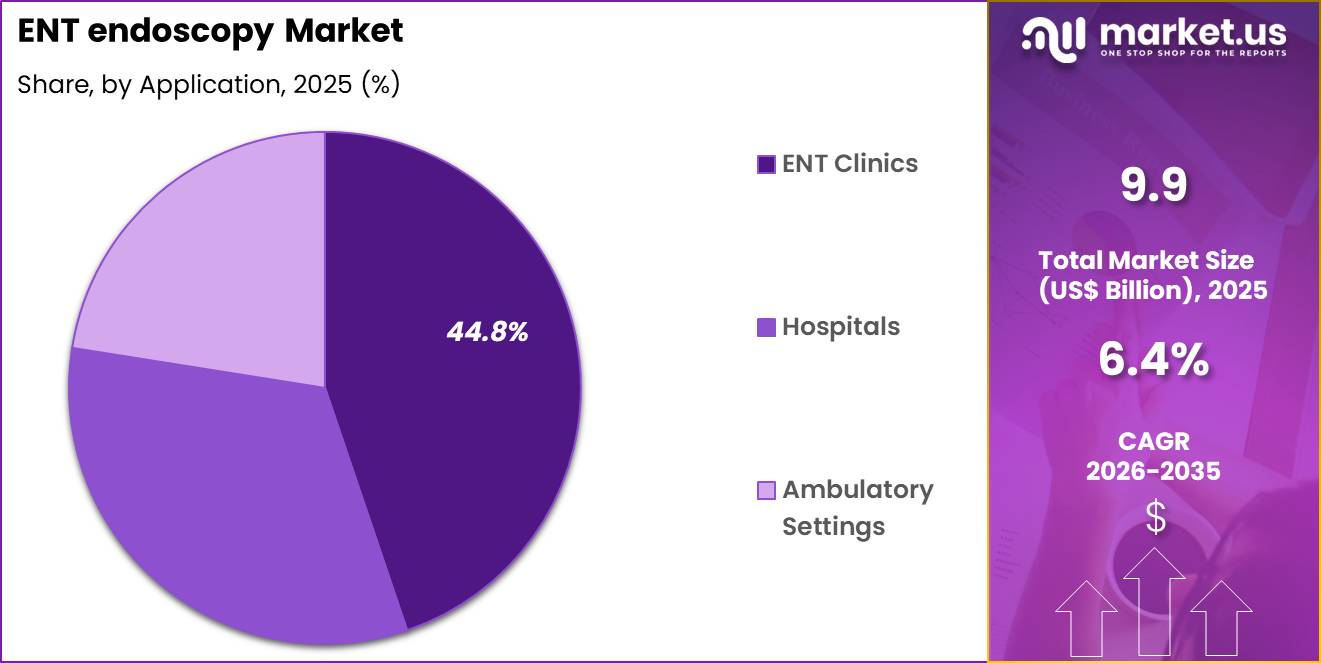

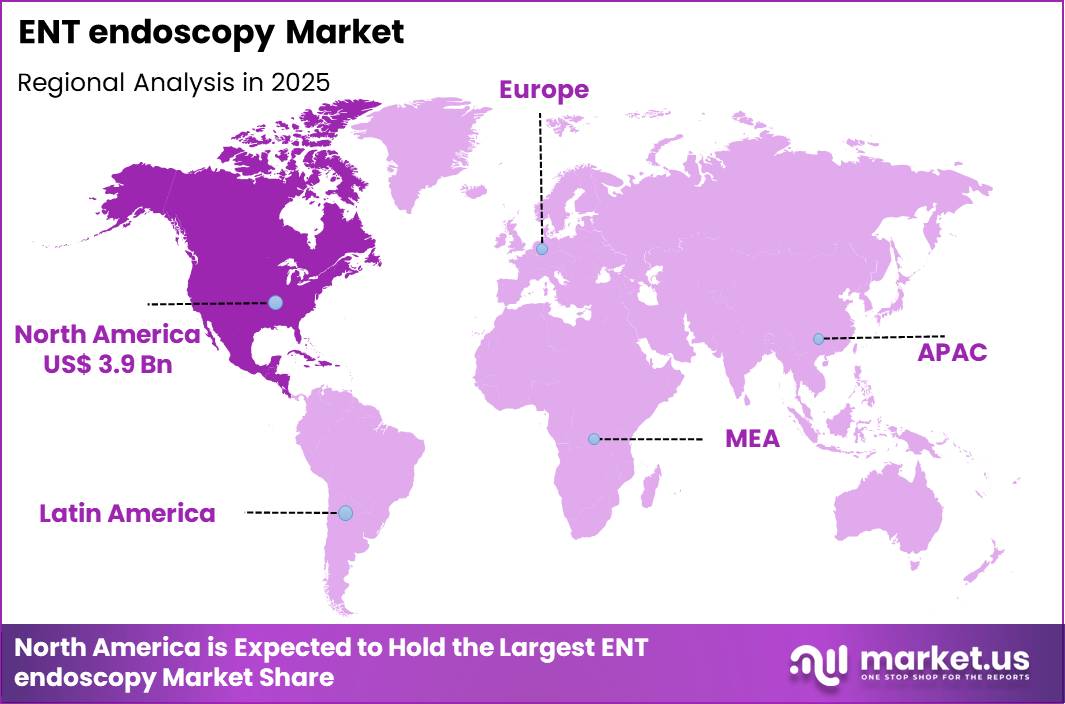

The Global ENT endoscopy Market size is expected to be worth around US$ 18.4 Billion by 2035 from US$ 9.9 Billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.5% share with a revenue of US$ 3.9 Billion.

Increasing demand for minimally invasive diagnostic and therapeutic procedures propels the ENT endoscopy market as otolaryngologists require advanced visualization tools to address a wide range of ear, nose, and throat conditions with greater precision and patient comfort.

Clinicians increasingly perform nasal endoscopy to evaluate chronic rhinosinusitis, identifying mucosal inflammation, polyps, and anatomical obstructions that guide medical or surgical management. These systems support laryngeal examinations in voice disorder clinics, allowing detailed assessment of vocal cord nodules, polyps, and paralysis during phonation to inform phonosurgery or injection laryngoplasty decisions.

ENT specialists utilize rigid and flexible endoscopes for middle ear exploration in chronic otitis media cases, detecting cholesteatoma extension and ossicular chain erosion to plan tympanomastoidectomy approaches. Pediatric otolaryngologists apply endoscopy to diagnose and manage airway pathologies, such as laryngomalacia and subglottic stenosis, enabling precise laser resection or balloon dilation under direct visualization.

Sinonasal surgeons employ high-definition video endoscopy during functional endoscopic sinus surgery, improving clearance of diseased tissue while preserving mucosal function in patients with recurrent sinusitis.

Manufacturers pursue opportunities to integrate 4K and 3D imaging technologies that enhance depth perception and tissue differentiation, expanding applications in complex skull base and transnasal pituitary surgeries. Developers advance narrow-band imaging and fluorescence-enhanced endoscopes that improve detection of subtle mucosal changes, broadening utility in early cancer surveillance of the larynx and pharynx.

These innovations facilitate integration with navigation systems for image-guided procedures in revision sinus surgery and orbital decompression. Opportunities emerge in disposable, single-use endoscopes that reduce cross-contamination risks in high-volume outpatient settings.

Companies invest in ergonomic, wireless designs with augmented reality overlays to support training and intraoperative decision-making. Recent trends emphasize compact, high-resolution systems with improved maneuverability and AI-assisted lesion detection, positioning the market for growth in precision ENT care focused on diagnostic accuracy, procedural safety, and patient-centered outcomes.

Key Takeaways

- In 2025, the market generated a revenue of US$ 9.9 Billion, with a CAGR of 6.4%, and is expected to reach US$ 18.4 Billion by the year 2035.

- The product type segment is divided into hearing screening devices, flexible endoscopes and rigid endoscopes, with hearing screening devices taking the lead with a market share of 39.6%.

- Considering applications, the market is divided into ENT clinics, ambulatory settings and hospitals. Among these, ENT clinics held a significant share of 44.8%.

- North America led the market by securing a market share of 39.5%.

Product Type Analysis

Hearing screening devices accounted for 39.6% of growth within product type and led the ENT endoscopy market due to increasing emphasis on early detection of hearing impairment. Governments and healthcare organizations promote newborn and pediatric hearing screening programs, which significantly raise device utilization.

Rising awareness of age-related hearing loss further expands routine diagnostic evaluations. ENT specialists prioritize screening equipment that delivers quick and accurate auditory assessments in outpatient settings.

Growth strengthens as portable and automated screening systems improve workflow efficiency. Technological advancements enhance signal processing and reduce testing time, which supports higher patient throughput.

Expansion of school-based and community-based hearing programs further increases demand. Integration with electronic medical records improves follow-up tracking and referral management. The segment is expected to remain dominant as preventive hearing care and early intervention strategies continue to gain momentum globally.

Application Analysis

ENT clinics generated 44.8% of growth within application and emerged as the leading segment due to specialized focus on ear, nose, and throat diagnostics. These clinics handle high patient volumes for hearing disorders, sinus evaluations, and laryngeal examinations. Dedicated ENT facilities invest in advanced endoscopic and screening equipment to enhance diagnostic precision. Concentration of specialist expertise strengthens consistent device utilization.

Growth accelerates as outpatient care expands and patients prefer specialized clinics for faster consultation. ENT clinics adopt flexible and compact equipment to optimize limited clinical space. Increasing prevalence of chronic sinusitis, allergies, and hearing disorders supports sustained demand.

Expansion of private specialty practices further boosts equipment procurement. The segment is projected to maintain leadership as specialized ENT services continue to grow within ambulatory healthcare frameworks.

Key Market Segments

By Product Type

- Hearing screening devices

- Flexible Endoscopes

- Rigid Endoscopes

By Applications

- ENT clinics

- Ambulatory settings

- Hospitals

Drivers

Rising incidence of chronic sinusitis and related conditions is driving the market.

The growing number of patients diagnosed with chronic sinusitis and other sinonasal disorders has substantially increased the utilization of ENT endoscopy for diagnostic and therapeutic purposes. Greater awareness among primary care physicians has led to more referrals for endoscopic evaluation of persistent nasal symptoms.

Otolaryngologists are performing higher volumes of office-based procedures using rigid and flexible endoscopes. The association between environmental factors and sinonasal inflammation further amplifies procedural demand. Public health campaigns promoting timely ENT evaluation support broader adoption of endoscopic techniques.

ENT endoscopy provides direct visualization of nasal passages and sinuses, enabling targeted interventions. National health data indicate consistent increases in sinus-related outpatient visits. Leading manufacturers continue to improve endoscope ergonomics and image quality to meet clinical needs.

This driver encourages development of specialized instruments for sinonasal surgery. Chronic rhinosinusitis affects approximately 12% of adults in the United States, contributing to frequent ENT consultations.

Restraints

Limited reimbursement for office-based ENT procedures is restraining the market.

Inconsistent or inadequate reimbursement policies for endoscopic procedures performed in outpatient settings create financial disincentives for physicians. Many payers apply restrictive criteria or lower payment rates for endoscopic sinus examinations compared to hospital-based procedures.

Otolaryngology practices face challenges justifying capital investments in advanced endoscopes when revenue recovery remains uncertain. Regulatory bodies often delay updates to reimbursement schedules for emerging endoscopic techniques. This restraint particularly affects independent ENT clinics and smaller group practices with limited financial flexibility. Physicians may continue using conventional tools to avoid potential revenue shortfalls.

Economic pressures from rising practice overheads further complicate budget planning for equipment upgrades. Advocacy efforts to expand coverage have achieved only partial success. Despite clear clinical advantages, reimbursement limitations slow the replacement cycle of older endoscopic systems. Insufficient reimbursement for office-based endoscopic procedures remains a key market restraint.

Opportunities

Increasing adoption of office-based sinus procedures is creating growth opportunities.

The expanding shift toward office-based sinus surgery and endoscopic interventions presents significant potential for ENT endoscopy systems in non-hospital settings. Governmental policies supporting ambulatory care reimbursement encourage the performance of sinus procedures outside operating rooms. Patients increasingly prefer convenient, lower-cost office treatments over hospital-based surgery.

Partnerships between ENT specialists and device manufacturers facilitate customized endoscopic solutions for outpatient environments. The large volume of chronic sinusitis cases in community settings magnifies demand for efficient endoscopic tools. Educational programs for otolaryngologists promote standardized techniques in office-based endoscopy.

This opportunity allows manufacturers to develop compact, high-resolution systems optimized for clinic use. Leading companies are expanding product lines with features tailored for ambulatory workflows. Overall, office-based growth aligns with efforts to reduce healthcare costs and improve patient access. The proportion of sinus procedures performed in office settings increased notably between 2022 and 2024.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the ENT endoscopy market through hospital capital planning, outpatient procedure volumes, and reimbursement visibility. Inflation increases costs for optical lenses, light sources, camera systems, and sterilization inputs, which raises acquisition and maintenance expenses.

Higher interest rates make financing new visualization towers and integrated systems more expensive, which slows upgrade decisions in smaller clinics. Geopolitical tensions affect global sourcing of precision optics, fiber components, and electronic modules, creating delivery delays and procurement uncertainty.

Current US tariffs on imported imaging equipment and subcomponents increase landed costs and compress supplier margins. These pressures can delay purchasing cycles and limit expansion in cost constrained facilities.

At the same time, providers strengthen domestic supplier partnerships and focus on durable, service backed systems to manage risk. Rising demand for minimally invasive sinus and airway procedures continues to support stable and confident long term growth.

Latest Trends

Introduction of single-use flexible endoscopes is a recent trend in the market.

In 2024, manufacturers introduced disposable flexible endoscopes specifically designed for ENT applications to address infection control concerns in outpatient settings. These single-use devices eliminate reprocessing requirements and reduce cross-contamination risks. Clinical evaluations confirmed comparable image quality to reusable models with added safety benefits.

The trend emphasizes cost-effectiveness for high-volume office procedures. Ambu launched the aScope 4 RhinoLaryngo single-use flexible endoscope in 2024, targeting routine ENT examinations. This development responds to heightened focus on infection prevention post-pandemic. Regulatory clearances in 2024 for single-use ENT endoscopes have accelerated clinical integration.

Industry collaborations optimize materials for flexibility and durability in disposable designs. These innovations aim to streamline workflows while prioritizing patient safety in otolaryngology practices. The introduction of single-use flexible endoscopes represents a key trend in ENT endoscopy.

Regional Analysis

North America is leading the ENT endoscopy Market

North America captured a 39.5% share of the ENT endoscopy market in 2024, reflecting strong procedural volumes across hospital-based and office-based otolaryngology practices. Physicians increasingly relied on high-resolution video scopes to evaluate nasal obstruction, chronic rhinosinusitis, vocal cord abnormalities, and upper airway disorders with greater clarity.

The continued shift toward minimally invasive sinus surgery and in-clinic diagnostic visualization supported equipment upgrades and recurring consumable use. Expansion of ambulatory surgical centers enabled faster patient throughput and encouraged investment in compact imaging systems. Greater emphasis on early detection of head and neck conditions further strengthened routine examinations.

Digital image capture and integration with electronic records improved documentation and interdisciplinary collaboration. A concrete indicator of underlying demand comes from the Centers for Disease Control and Prevention, which reported that sinusitis leads to millions of healthcare visits annually in the United States, highlighting sustained need for advanced nasal and airway visualization tools.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The ENT endoscopy market in Asia Pacific is expected to advance steadily during the forecast period as specialty care networks broaden and diagnostic awareness rises. Rapid urbanization and environmental exposure increase cases of allergic rhinitis and airway inflammation, prompting more frequent ENT consultations.

Hospitals strengthen minimally invasive surgical programs, encouraging adoption of modern endoscopic platforms. Private healthcare providers expand outpatient otolaryngology services to meet growing middle-class demand.

Medical institutions incorporate advanced visualization training into residency programs, accelerating clinician familiarity with updated systems. Technology vendors expand regional distribution and service support to capture emerging demand.

A verifiable signal of respiratory health burden appears in 2023 data from the World Health Organization, which continues to report substantial global prevalence of chronic respiratory conditions, reinforcing long-term procedural growth across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the ENT endoscopy market grow by advancing optics clarity, miniaturized instrument designs, and integrated visualization platforms that support precise evaluation and treatment of ear, nose, and throat conditions.

They also strengthen customer value by bundling high-resolution imaging with procedural workflow software and clinician training programs that improve adoption and procedural confidence across specialty practices and hospital ENT units.

Firms pursue strategic alliances with otolaryngology associations and healthcare networks to embed their technologies into clinical protocols and expand recurring clinical demand. Geographic expansion into Europe, North America, and high-growth Asia Pacific diversifies revenue streams and captures rising investments in minimally invasive diagnostics and therapeutic procedures.

Karl Storz SE & Co. KG exemplifies a global medical device leader with a broad portfolio of endoscopic imaging systems, precision instruments, and comprehensive support services that align with evolving surgeon requirements.

The company advances its competitive agenda through disciplined investment in product innovation, targeted collaborations across clinical communities, and a customer-centric commercialization strategy that translates technological enhancements into measurable clinical impact.

Top Key Players

- Olympus Corporation

- Karl Storz

- Stryker

- Richard Wolf

- Medtronic

- Smith & Nephew

- HOYA Corporation

- ConMed

- Pentax Medical

- ATMOS MedizinTechnik

Recent Developments

- In 2025, Smith & Nephew reported third-quarter revenue of US$ 57 million from its ENT division for the period ended September 27. The company indicated that the business returned to more stable growth following earlier softness in certain emerging markets. Performance was supported by demand within its tonsil and adenoid product line, particularly the Halo One system used in coblation intracapsular tonsillectomy, which has continued to see increasing utilization in the US due to its association with reduced postoperative discomfort and faster recovery.

- In 2026, Stryker disclosed that its MedSurg and Neurotechnology segment generated US$ 15.6 billion in fiscal year 2025 net sales. The division, which includes ENT navigation platforms and endoscopic surgical instruments, recorded a 17.5% rise in fourth-quarter net sales. Growth was driven by broader adoption of advanced navigation systems integrated with Scopis software and increasing use of MiniFESS instrumentation designed to improve efficiency in functional endoscopic sinus surgery across hospital and ambulatory care environments.

Report Scope

Report Features Description Market Value (2025) US$ 9.9 Billion Forecast Revenue (2035) US$ 18.4 Billion CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Hearing screening devices, Flexible Endoscopes and Rigid Endoscopes), By Applications (ENT clinics, Ambulatory settings and Hospitals) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Olympus Corporation, Karl Storz, Stryker, Richard Wolf, Medtronic, Smith & Nephew, HOYA Corporation, ConMed, Pentax Medical, ATMOS MedizinTechnik Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Olympus Corporation

- Karl Storz

- Stryker

- Richard Wolf

- Medtronic

- Smith & Nephew

- HOYA Corporation

- ConMed

- Pentax Medical

- ATMOS MedizinTechnik

Our Clients

- 179002

- Feb 2026