Global Energy Ingredients Market Size, Share, And Industry Analysis Report By Product (Caffeine, Creatine, Taurine, Ginseng, Others), By Application (Beverage, Food, Supplements, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183021

- Number of Pages: 338

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

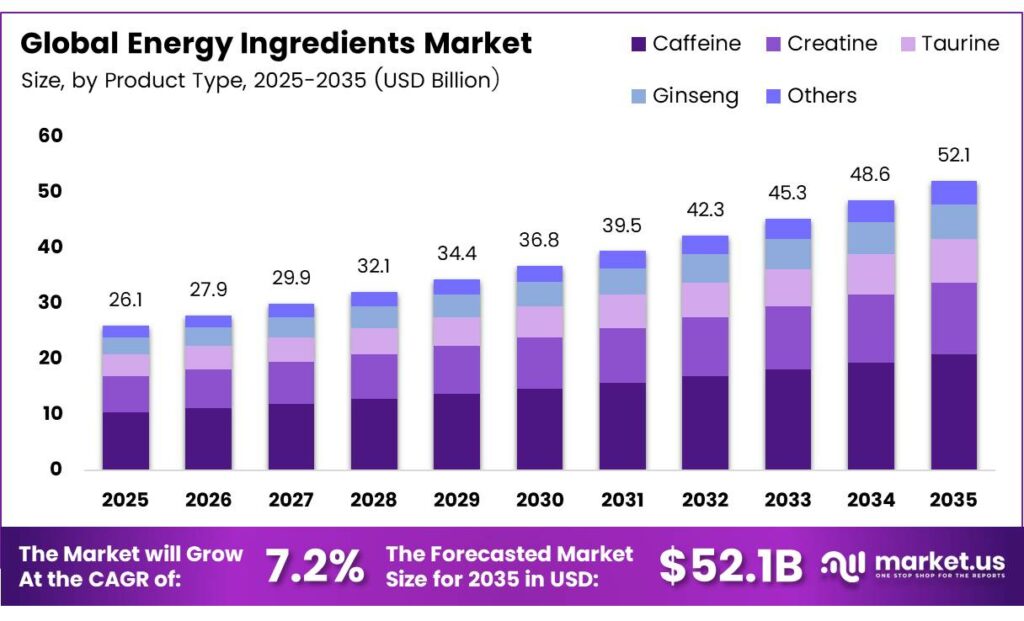

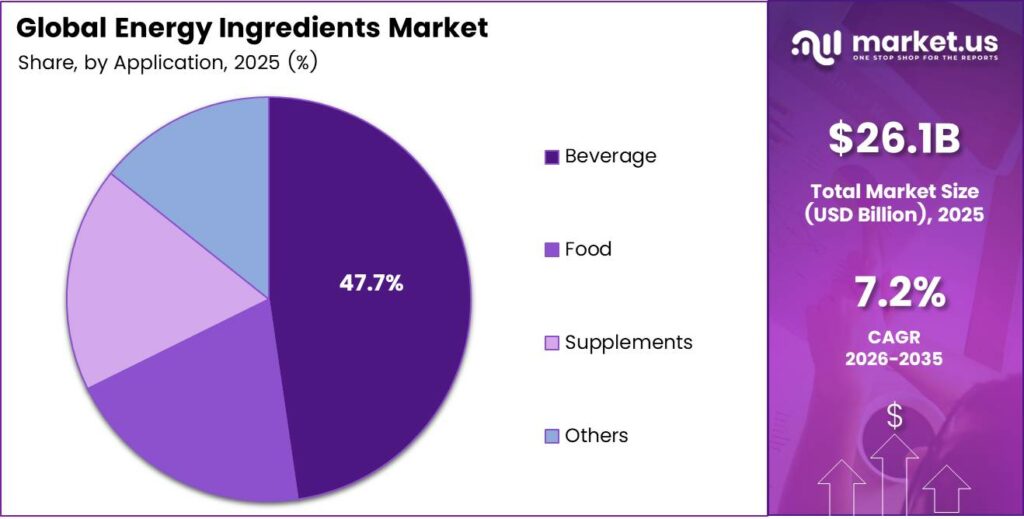

The Global Energy Ingredients Market size is expected to be worth around USD 52.1 billion by 2035 from USD 26.1 billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026 to 2035.

The energy ingredients market covers a broad set of bioactive compounds used to boost energy, endurance, and mental performance. Key ingredients include caffeine, creatine, taurine, ginseng, B vitamins, and electrolytes. Manufacturers incorporate these compounds into beverages, food products, and dietary supplements.

Modern consumer lifestyles drive strong demand for functional energy solutions. Busy professionals, athletes, and fitness-focused individuals actively seek products that support alertness and physical performance. Consequently, food and beverage companies increase their use of high-performance energy ingredients across multiple product categories.

According to the USDA National Agricultural Library, caffeine products such as NOS Energy Drink contain 163 mg of caffeine per 16 fl oz serving, providing a government-verified benchmark for caffeine dosage in commercial beverages. This data confirms the centrality of caffeine as the leading energy ingredient across the beverage segment.

Indonesia’s Robusta coffee production reached 11.0 million 60-kg bags in 2025/26, with green coffee exports at 7.8 million bags. This supply volume underscores the robust availability of caffeine-source crops that directly support energy ingredient manufacturing at scale.

The sports nutrition sector represents one of the fastest-growing application areas. Amino acid complexes, creatine formulations, and plant-based adaptogens gain significant traction among health-conscious consumers. Additionally, clean-label trends push manufacturers to source natural botanical extracts over synthetic alternatives.

Key Takeaways

- The Global Energy Ingredients Market is valued at USD 26.1 billion in 2025 and is projected to reach USD 52.1 billion by 2035 at a CAGR of 7.2% during the forecast period 2026 to 2035.

- Caffeine holds the dominant share at 45.2% in 2025.

- Beverage leads with a 47.7% market share in 2025.

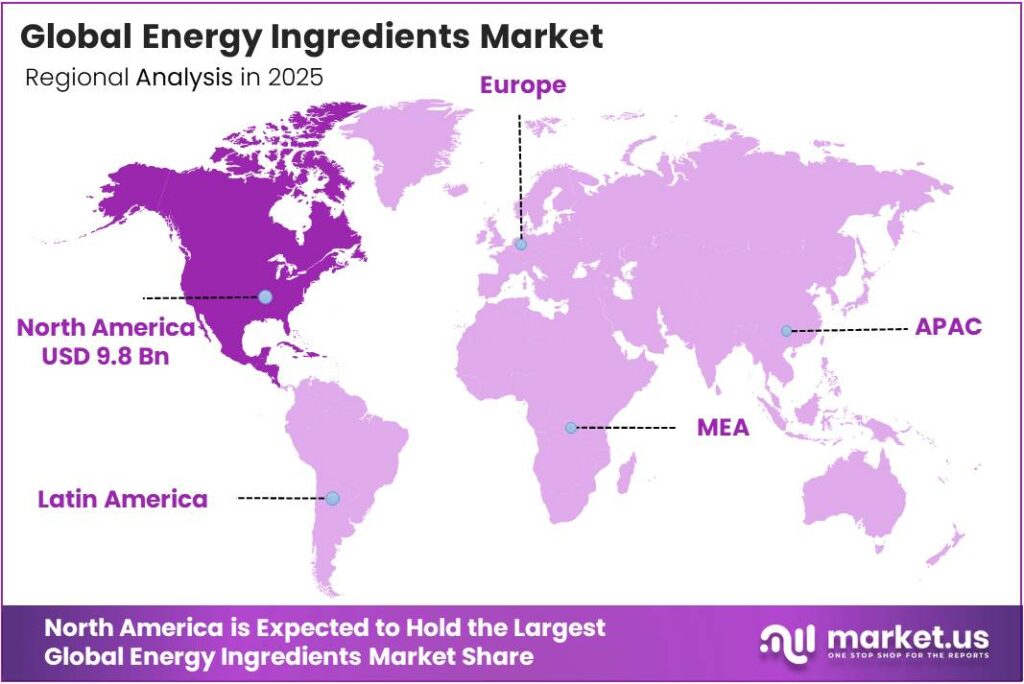

- North America dominates the regional landscape with a 37.9% share, valued at USD 9.8 billion.

By Product Analysis

Caffeine dominates the By Product segment with 45.2% due to its widespread use across beverages and performance supplements.

In 2025, Caffeine held a dominant market position in the By Product segment of the Energy Ingredients Market, with a 45.2% share. Caffeine remains the most widely used energy compound globally. Its proven efficacy in boosting alertness and physical endurance makes it the preferred choice for beverage formulators and supplement manufacturers. Moreover, consistent raw material availability supports its continued market leadership.

Creatine captures a significant share in the by-product segment, driven by strong demand from sports nutrition and performance supplement brands. Athletes and fitness enthusiasts actively use creatine to improve strength and muscle recovery. Additionally, growing scientific evidence supporting its safety and effectiveness accelerates its adoption across functional food and supplement formulations worldwide.

Taurine serves as a key co-ingredient in energy beverage formulations, often combined with caffeine to enhance its stimulant effect. Manufacturers value taurine for its role in cellular hydration and cardiovascular support. Consequently, taurine demand grows steadily as energy drink brands expand their product portfolios, targeting both performance athletes and general wellness consumers.

By Application Analysis

Beverage dominates the By Application segment with 47.7% due to high consumer demand for ready-to-drink energy products.

In 2025, Beverage held a dominant market position in the By Application segment of the Energy Ingredients Market, with a 47.7% share. Ready-to-drink energy beverages represent the largest end-use channel for energy ingredients. Consumers actively choose energy drinks, sports beverages, and functional waters. Moreover, aggressive product innovation by beverage brands sustains high ingredient procurement volumes across this segment.

Food applications represent a growing channel as manufacturers fortify snacks, cereals, and meal replacements with energy-active compounds. Consumers increasingly seek everyday food products that deliver functional benefits beyond basic nutrition. Consequently, ingredient suppliers develop specialized formats that integrate caffeine, creatine, and vitamins seamlessly into solid food matrices without affecting taste or texture.

Supplements form a strong and rapidly expanding application category, particularly within the sports nutrition and wellness industries. Capsule, powder, and gummy formats allow precise dosing of active energy compounds. Additionally, e-commerce growth accelerates supplement accessibility globally. The Others category includes applications such as pharmaceutical-grade energy formulations, cosmetics, and topical products incorporating bioactive stimulant compounds.

Key Market Segments

By Product

- Caffeine

- Creatine

- Taurine

- Ginseng

- Others

By Application

- Beverage

- Food

- Supplements

- Others

Emerging Trends

Clean-Label Sourcing and Botanical Ingredients Reshape Energy Formulations

Brand owners and ingredient suppliers actively embrace clean-label sourcing, replacing synthetic stimulants with traceable botanical alternatives. Botanical extracts such as ashwagandha, rhodiola, and green tea now appear alongside caffeine in multi-ingredient energy formulas. EU production and trade data for botanical extracts and beverage additives confirm steady volume growth across European markets. This shift reflects broader consumer demand for transparency.

Personalized Nutrition and Electrolyte Blends Gain Momentum in Energy Supplements

Technology-enabled personalization transforms the energy supplement segment. Brands develop customized blends combining vitamin B complex, electrolytes, and amino acids tailored to individual health profiles. Moreover, a surge in digital health platforms enables consumers to select precise ingredient combinations for energy, recovery, and cognition support. Consequently, manufacturers invest in flexible, small-batch production capabilities to meet growing demand for personalized solutions.

Drivers

Rising Demand for Functional Beverages and Performance Nutrition Fuels Ingredient Growth

Modern lifestyles increase consumer reliance on energy-fortified beverages and functional foods. Professionals, athletes, and students actively seek products that support sustained mental alertness and physical endurance. Foreign Agricultural Service, Ghana imported USD 1.24 billion of food processing ingredients in 2024, up from USD 857 million in 2023, reflecting the surging global appetite for functional ingredient-based products.

Sports Nutrition Expansion and Consumer Health Awareness Drive Amino Acid and Creatine Demand

The sports nutrition sector actively expands its use of creatine, amino acids, and plant-based adaptogens. Health-conscious consumers increasingly prioritize physical performance enhancement and mental clarity through targeted supplementation. Additionally, growing scientific validation of ingredients like taurine and ginseng strengthens consumer confidence. Consequently, manufacturers scale production of these high-demand compounds to meet rising global formulation requirements.

Restraints

Regulatory Complexity and Safety Scrutiny Increase Compliance Burden for Stimulant Ingredients

Regulatory agencies worldwide impose rigorous safety assessments on synthetic and high-dose stimulant compounds. Manufacturers must navigate complex approval processes in multiple jurisdictions before launching new energy ingredient products. A single serving of highly concentrated caffeine liquid may expose consumers to approximately 5 times the caffeine of a standard energy shot, highlighting the serious safety concerns that intensify regulatory oversight globally.

High Raw Material and Production Costs Limit Access to Premium Natural Energy Ingredients

Premium natural energy ingredients such as organic ginseng and botanical adaptogens carry significantly higher production and sourcing costs than synthetic alternatives. Small and mid-sized manufacturers face margin pressure when formulating clean-label products. Moreover, supply chain volatility for plant-derived ingredients adds further cost uncertainty. Consequently, many producers in price-sensitive emerging markets delay the adoption of natural premium energy compounds in their formulations.

Growth Factors

Functional Food Fortification and Emerging Market Urbanization Open New Revenue Channels

Everyday snack categories and ready-to-eat food products represent an untapped growth avenue for energy ingredient suppliers. Manufacturers increasingly fortify cereals, protein bars, and baked goods with caffeine, B vitamins, and electrolytes. According to U.S. eCFR 21 CFR Part 101, all food ingredients must be listed by descending weight, mandating clear disclosure of caffeine and botanical extracts. This regulatory transparency builds consumer trust and accelerates fortified food adoption.

Strategic Partnerships and Innovative Delivery Systems Expand Market Potential

Ingredient companies form strategic alliances with food brands to integrate organic and clean-label energy compounds into mainstream product lines. Simultaneously, innovation in sustained-release delivery systems enables controlled energy absorption over longer periods. Additionally, rising urbanization and fitness culture in the Asia Pacific, Latin America, and Africa create substantial new consumer bases actively seeking affordable, high-performance energy ingredient solutions.

Regional Analysis

North America Dominates the Energy Ingredients Market with a Market Share of 37.9%, Valued at USD 9.8 Billion

North America commands a leading 37.9% share of the global energy ingredients market, with a regional valuation of USD 9.8 billion in 2025. The United States drives this dominance through its mature energy beverage industry and well-established sports nutrition sector. Moreover, high consumer spending on functional food and supplements, combined with strong domestic ingredient manufacturing, reinforces North America’s leadership position throughout the forecast period.

Europe represents a significant and innovation-driven market for energy ingredients. Stringent EU food safety regulations push manufacturers toward clean-label and natural ingredient sourcing. Additionally, growing health awareness among European consumers accelerates demand for botanical adaptogens, B vitamins, and electrolyte blends in both food and supplement categories.

Asia Pacific emerges as the fastest-growing regional market for energy ingredients. Rapid urbanization, rising disposable incomes, and expanding fitness culture in China, India, and Southeast Asia fuel ingredient demand. Furthermore, a large and youthful consumer base actively adopts energy beverages and sports supplements, making this region a primary growth engine for global ingredient suppliers.

The Middle East and Africa region presents emerging growth opportunities for energy ingredient producers. Young, urban populations in GCC countries and South Africa increasingly adopt sports nutrition and energy beverage products. Moreover, expanding retail infrastructure and rising health awareness support ingredient market development. Nevertheless, price sensitivity and limited local manufacturing capacity remain key challenges for sustained market penetration.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE operates as a global leader in the production of specialty chemicals and nutritional ingredients, including energy-active compounds such as vitamins, amino acids, and bioactive extracts. The company leverages its extensive R&D infrastructure and global manufacturing network to supply high-quality energy ingredients to food, beverage, and supplement manufacturers across multiple regions. Its broad ingredient portfolio positions it as a preferred partner for functional product developers.

Spectrum Chemical Mfg. Corp. supplies a comprehensive range of high-purity laboratory and industrial-grade chemicals, including energy ingredient compounds used in supplement and beverage manufacturing. The company maintains strong quality control standards that align with FDA and USP regulatory requirements. Moreover, Spectrum’s broad catalog of fine chemicals and reference standards makes it a valued supplier for formulators seeking consistent, traceable energy ingredient inputs at scale.

RFI Ingredients specializes in botanical extracts, standardized herbal compounds, and functional ingredient blends for the nutraceutical and functional food sectors. The company focuses on clean-label sourcing and sustainable supply chain practices, addressing rising industry demand for transparent ingredient origins. Additionally, RFI’s custom formulation capabilities enable beverage and supplement brands to develop differentiated energy products using natural and plant-derived active compounds.

Korea Ginseng Corporation stands as the world’s leading authority in ginseng cultivation, processing, and distribution of ginseng-based energy ingredients. The company commands deep expertise in standardizing ginsenoside content across its extract portfolio. Furthermore, its government-affiliated quality certification and decades of research backing provide global buyers with unmatched confidence in product efficacy and safety, making it a cornerstone supplier in the botanical energy ingredient category.

Top Key Players in the Market

- BASF SE

- Spectrum Chemical Mfg. Corp.

- RFI Ingredients

- Korea Ginseng Corporation

- Orkla

- ILHWA CO., LTD.

- Applied Food Sciences, Inc. (AFS)

- Naturalin Bio-Resources Co., Ltd.

- Changsha Huir Biological-Tech Co., Ltd.

- Sinochem Pharmaceutical Co., Ltd.

- KOEI KOGYO CO., LTD

- Aarti Industries Ltd

Recent Developments

- In September 2025, BASF completed the sale of its Food and Health Performance Ingredients business (including plant sterol esters, conjugated linoleic acid/CLA, omega-3 oils, and other health ingredients for human nutrition) to Louis Dreyfus Company. The company is now focusing its Nutrition Ingredients business unit on core platforms like vitamins and carotenoids to strengthen its position in vital nutrition ingredients.

- In March 2025, KGC/JungKwanJang showcased functional red ginseng solutions at Natural Products Expo West, including new sports nutrition lineup products under the “Everytime” brand (for energy, blood circulation, and performance) and GLPro (blood-sugar support). It highlighted caffeine-free options like Hong Sam Won (a red ginseng beverage with cinnamon, ginger, and jujube), positioned for sustained energy.

Report Scope

Report Features Description Market Value (2025) USD 26.1 Billion Forecast Revenue (2035) USD 52.1 Billion CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Caffeine, Creatine, Taurine, Ginseng, Others), By Application (Beverage, Food, Supplements, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, Spectrum Chemical Mfg. Corp., RFI Ingredients, Korea Ginseng Corporation, Orkla, ILHWA CO., LTD., Applied Food Sciences, Inc. (AFS), Naturalin Bio-Resources Co., Ltd., Changsha Huir Biological-Tech Co., Ltd., Sinochem Pharmaceutical Co., Ltd., KOEI KOGYO CO., LTD, Aarti Industries Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Energy Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Energy Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Spectrum Chemical Mfg. Corp.

- RFI Ingredients

- Korea Ginseng Corporation

- Orkla

- ILHWA CO., LTD.

- Applied Food Sciences, Inc. (AFS)

- Naturalin Bio-Resources Co., Ltd.

- Changsha Huir Biological-Tech Co., Ltd.

- Sinochem Pharmaceutical Co., Ltd.

- KOEI KOGYO CO., LTD

- Aarti Industries Ltd

Our Clients

- 183021

- March 2026