Quick Navigation

Report Overview

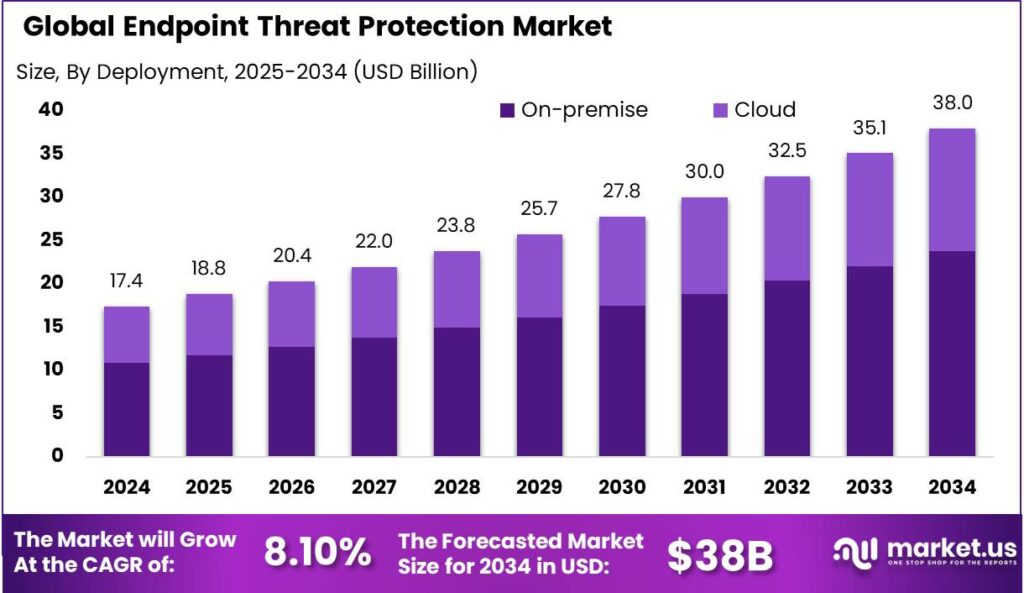

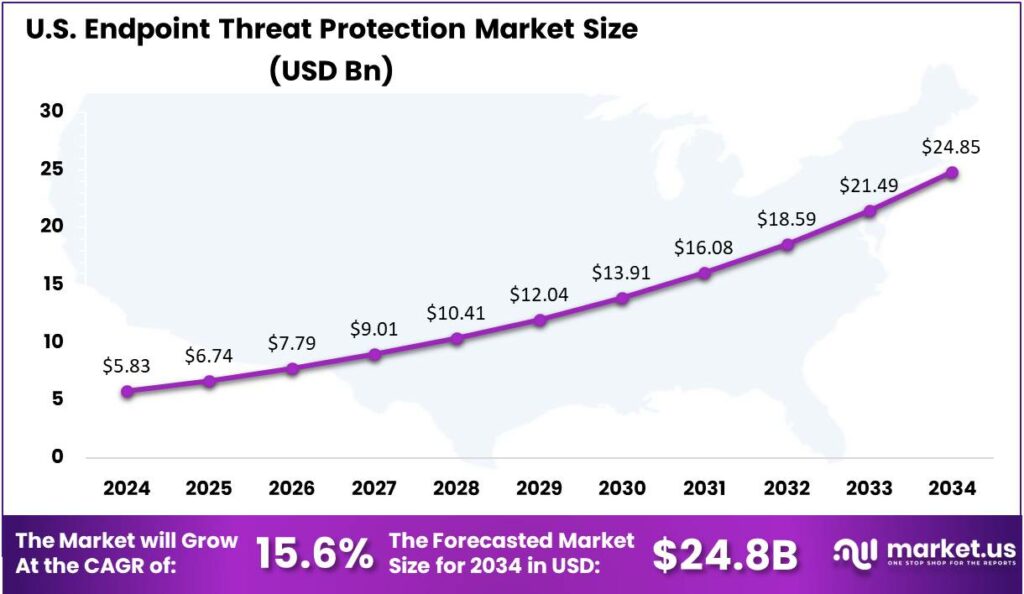

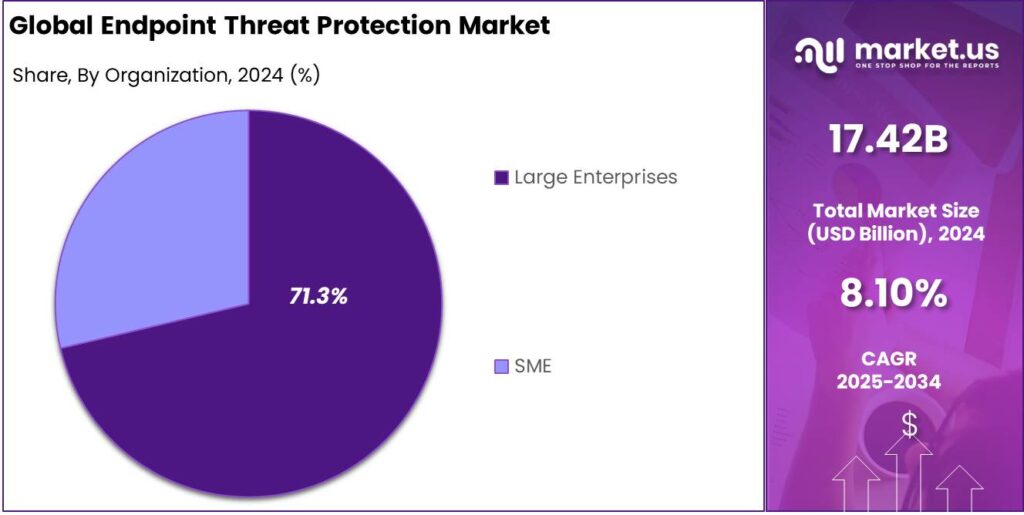

The Global Endpoint Threat Protection Market size is expected to be worth around USD 38 Billion By 2034, from USD 17.42 Billion in 2024, growing at a CAGR of 8.10% during the forecast period from 2025 to 2034. In 2024, North America led the Endpoint Threat Protection market with a 37.4% share, generating about USD 6.5 billion. The U.S. market was valued at USD 5.83 billion and is expected to grow at a 15.6% CAGR.

Endpoint Threat Protection is a comprehensive cybersecurity approach that secures endpoint devices such as desktops, laptops, mobile phones, servers and IoT devices from cyberattacks. Endpoints are entry points to networks and frequent targets of cyberattacks. Endpoint protection combines antivirus, firewalls, intrusion prevention, and advanced detection to prevent, identify, and respond to threats.

The demand for Endpoint Threat Protection solutions is driven by the escalating frequency and sophistication of cyberattacks. Organizations are prioritizing endpoint security to protect digital assets amid rising cloud adoption and hybrid work. They seek comprehensive solutions with real-time detection, automated response, and easy IT integration, reflecting increased cybersecurity awareness and proactive risk management.

Implementing strong endpoint threat protection helps organizations prevent data breaches, protect sensitive information, and maintain their reputation. It also supports regulatory compliance, reduces legal risks, and improves operational efficiency by minimizing downtime, ultimately enhancing business productivity and resilience.

The growing Endpoint Threat Protection market offers strong investment potential as businesses prioritize cybersecurity. Firms developing AI-driven threat detection and cloud-based solutions are especially attractive. Rising demand across sectors like healthcare, finance, and retail signals continued market growth and profitability.

AI and ML integration in endpoint security enhances threat detection and response. Alongside zero-trust models and growing cloud reliance, these trends enable advanced, scalable, and adaptive solutions. Vendors offering user-friendly, affordable, and comprehensive platforms are well-positioned to capitalize on these opportunities.

Governments and regulatory bodies worldwide have established stringent data protection laws and compliance requirements, compelling organizations to implement robust security measures. Regulations like GDPR and HIPAA mandate strict security measures to protect sensitive data, driving the adoption of comprehensive endpoint protection solutions and fueling market growth.

Key Takeaways

- The Global Endpoint Threat Protection Market size is expected to grow from USD 17.42 billion in 2024 to around USD 38 billion by 2034, with a CAGR of 8.10% during the forecast period from 2025 to 2034.

- In 2024, the Solution segment dominated the market, capturing more than 67.3% share of the global Endpoint Threat Protection Market.

- The On-premise segment held a leading position in 2024, accounting for over 62.8% of the global endpoint threat protection market.

- The Large Enterprise segment was the dominant end-user in 2024, capturing more than 71.3% share in the global Endpoint Threat Protection market.

- In 2024, the Government & Defense segment held a significant share, capturing over 26.7% of the global Endpoint Threat Protection market.

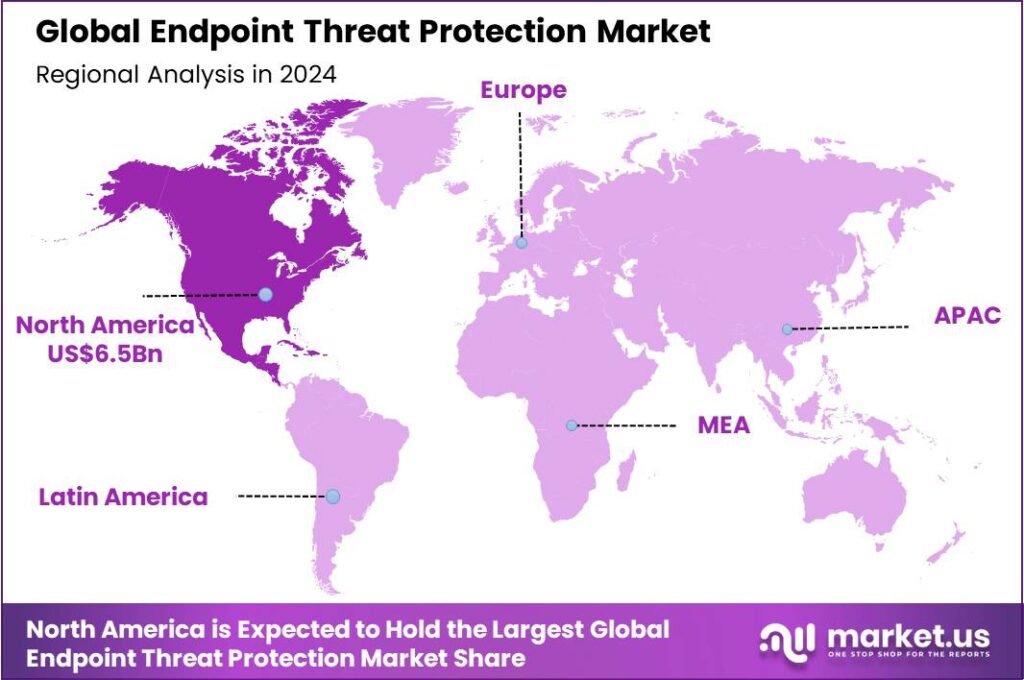

- North America dominated the regional market in 2024, capturing more than 37.4% of the global Endpoint Threat Protection market and generating approximately USD 6.5 billion in revenue.

- The U.S. Endpoint Threat Protection market was valued at USD 5.83 billion in 2024 and is projected to grow at a 15.6% CAGR.

U.S. Market Influence

In 2024, the U.S. Endpoint Threat Protection market reached a valuation of USD 5.83 billion, reflecting its critical role in securing enterprise endpoints amid rising cyber threats. Rising ransomware, phishing, and zero-day attacks, combined with remote work and BYOD trends, have increased demand for advanced endpoint security with real-time detection and multi-layered defense across industries like healthcare, BFSI, government, and IT.

The market is expected to grow at a 15.6% CAGR, driven by regulatory pressures and evolving threats. U.S. organizations are adopting AI-powered endpoint security with behavioral analytics and machine learning for proactive threat detection. Cloud-based platforms and demand for EDR/XDR solutions are rising due to their scalability and centralized threat management.

Digital transformation in SMEs and increased U.S. government investment in cybersecurity are driving demand for affordable, automated endpoint protection. Strict regulations like HIPAA and CCPA make endpoint security essential, fueling significant market growth supported by innovation and heightened security awareness.

In 2024, North America held a dominant market position, capturing more than a 37.4% share of the global Endpoint Threat Protection market and generating approximately USD 6.5 billion in revenue. This leadership can be attributed to the region’s advanced digital infrastructure, higher cybersecurity budgets, and the early adoption of endpoint protection technologies across enterprises.

The region hosts leading cybersecurity vendors like Microsoft, Cisco, Symantec, CrowdStrike, and Palo Alto Networks, driving innovation in AI-powered threat detection, automated response, and unified endpoint management. Growing adoption of cloud-native platforms and remote work increases demand for endpoint visibility and secure access in hybrid IT environments.

Government initiatives and strict regulations like CCPA and HIPAA have strengthened North America’s market by mandating endpoint protection to secure sensitive data. This pressure on public sector agencies and critical infrastructure operators has increased demand for advanced cybersecurity solutions across all government levels.

North America’s strong technology, increasing regulatory demands, and evolving threat landscape make it the epicenter of endpoint threat protection innovation and adoption. Ongoing advancements and strengthened public-private cybersecurity partnerships will sustain the region’s leadership through the forecast period.

Component Analysis

In 2024, the Solution segment held a dominant market position, capturing more than a 67.3% share of the global Endpoint Threat Protection Market. This leadership is largely driven by the increasing sophistication of cyber threats such as ransomware, zero-day exploits, and advanced persistent threats (APTs).

Among these, EDR and endpoint encryption tools have witnessed the fastest adoption rates due to their capabilities in providing real-time monitoring, incident response, and data protection. The rising adoption of remote work and BYOD (Bring Your Own Device) policies has made endpoints more vulnerable, increasing the demand for encryption and advanced application control.

Endpoint encryption plays a critical role in mitigating data breaches by protecting sensitive files on lost or stolen devices, particularly in regulated industries such as finance, healthcare, and legal services. As regulatory pressure intensifies globally, compliance requirements are further fueling the uptake of these sophisticated security components.

Mobile security tools have become essential due to the rise of the mobile workforce and growing mobile malware threats. As smartphones and tablets see greater use in enterprises, securing these endpoints is crucial. Modern mobile security solutions provide multilayered protection, including anti-malware, secure access, and data containerization to separate personal and corporate information.

Deployment Analysis

In 2024, the On-premise segment held a dominant market position, capturing more than a 62.8% share of the global endpoint threat protection market. This dominance was largely attributed to the heightened demand for internal control over cybersecurity frameworks, especially among large enterprises and critical infrastructure operators.

The growing threat landscape and increasing sophistication of cyber-attacks have compelled enterprises to seek security solutions that can be closely monitored and managed in-house. On-premise deployment models have provided such enterprises with enhanced visibility into endpoint activities, thereby supporting real-time detection and rapid incident response.

Another key factor behind the on-premise segment’s dominance is its compatibility with legacy systems. Large organizations often have complex, long-established IT environments where cloud migration can be costly and risky. On-premise solutions integrate smoothly with existing infrastructure and internal security protocols, ensuring business continuity without major changes.

While cloud solutions have grown rapidly among SMEs, large organizations have been slower to adopt them due to concerns over external data storage and multi-tenancy. In 2024, on-premise models remained dominant, offering better data governance, lower third-party risk, and customizable threat response—key factors in today’s cybersecurity landscape.

Organization Analysis

In 2024, the Large Enterprise segment held a dominant market position, capturing more than a 71.3% share in the global Endpoint Threat Protection market. This leadership is primarily driven by the extensive IT infrastructure and vast endpoint ecosystem within large organizations, which makes them more vulnerable to targeted cyberattacks.

Moreover, large enterprises typically maintain dedicated cybersecurity teams and IT budgets, which facilitates the adoption of advanced threat detection and response technologies. Solutions such as endpoint detection and response (EDR), next-generation antivirus (NGAV), and behavior-based threat analytics are more readily deployed in large-scale environments.

Additionally, compliance with regulatory frameworks such as GDPR, HIPAA, and SOX mandates strong endpoint security protocols, particularly for industries like finance, healthcare, and critical infrastructure where large enterprises dominate. The reputational and financial implications of data breaches in such sectors amplify the demand for proactive endpoint threat protection.

The surge in remote and hybrid work models has added to the attack surface for large enterprises, with endpoints becoming the first line of defense. To secure thousands of remote devices and prevent lateral movement of threats within the network, companies have significantly increased their reliance on centralized endpoint protection platforms.

Application Analysis

In 2024, the Government & Defense segment held a dominant market position, capturing more than a 26.7% share in the global Endpoint Threat Protection market. This leadership was largely driven by the increasing volume of cyber threats targeting national security systems, sensitive data repositories, and mission-critical infrastructure.

The heightened digitalization of defense networks and inter-agency communication platforms has made them more vulnerable to advanced persistent threats (APTs), ransomware, and zero-day exploits. Unlike commercial sectors, where financial loss is the primary risk, a breach in the defense ecosystem could lead to national security compromise or loss of human lives.

Government and defense sectors drive the segment’s dominance through large cybersecurity budgets and strategic procurement. They adopt advanced solutions like centralized orchestration, AI-driven threat hunting, and secure cloud endpoints. Collaborations with vendors also yield custom, defense-grade endpoint protections for military environments.

Rising geopolitical tensions and hybrid warfare have driven defense ministries to adopt stronger cybersecurity measures, focusing on securing endpoints across satellite communications, unmanned systems, and digital intelligence networks. This has positioned Government & Defense as the leading application segment, with continued dominance expected through the forecast period.

Key Market Segments

By Component

- Solution

- Antivirus

- Application Control

- Endpoint Encryption

- Endpoint Detection and Response

- Firewall

- Mobile Security Tools

- Others

- Services

- Consulting

- Managed

- Training & Support

By Deployment

- On-premise

- Cloud

By Organization

- Large Enterprise

- SME

By Application

- IT & telecom

- BFSI

- Industrial

- Education

- Retail

- Healthcare

- Government & Defense

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

AI and Machine Learning Powering Next-Gen Endpoint Security

AI and ML have greatly improved endpoint threat protection by enabling real-time analysis of large datasets to detect patterns and anomalies. Unlike traditional signature-based methods, they can identify novel and evolving threats, enhancing overall security.

AI-driven endpoint protection systems continuously learn from new data to stay effective against evolving and sophisticated threats that traditional methods may miss. Automation through AI speeds up response times and reduces the need for manual intervention, limiting damage from breaches.

Restraint

Complexity in Managing Diverse Endpoint Environments

Organizations face challenges in managing endpoint threat protection due to diverse IT environments with multiple device types, operating systems, and user behaviors. Ensuring consistent security across desktops, laptops, mobile, and IoT devices with varying requirements is complex and demanding.

Managing timely updates and patches across all endpoints is a major challenge, as delays can leave systems exposed to known vulnerabilities. Maintaining visibility and control, especially over remote or decentralized endpoints, is difficult and raises the risk of undetected breaches.

These challenges demand strong endpoint management solutions with centralized control, real-time monitoring, and automated responses though such solutions often require significant investment and expertise that not all organizations can afford.

Opportunity

Expansion of Endpoint Security in Remote Work and BYOD Trends

Remote work and BYOD policies have expanded organizational network perimeters, increasing vulnerabilities. Accessing corporate resources from diverse locations and devices outside traditional security infrastructures broadens the attack surface and raises the risk of breaches.

BYOD policies boost flexibility and employee satisfaction but introduce devices that might not meet corporate security standards. This highlights the need for advanced endpoint security solutions that protect all devices, regardless of type or location.

Features like real-time threat detection, automated response, and smooth integration with existing security systems are increasingly essential. Additionally, growing use of cloud services and collaboration tools makes strong endpoint protection critical to secure data across diverse platforms and devices.

Challenge

Balancing Security Measures with User Privacy and Experience

Stringent endpoint security measures can raise concerns about user privacy and experience, as extensive monitoring may be seen as intrusive. This can lead to user resistance and compliance challenges. EDR tools must carefully balance effective threat detection with respecting individual privacy rights to maintain trust and regulatory adherence.

Overly restrictive security measures or those that slow down systems can reduce productivity and frustrate users. Organizations must balance strong protection with usability by adopting solutions that are effective yet unobtrusive. This includes using technologies with granular data control, transparent monitoring, and optimized performance to minimize impact on the user experience.

Emerging Trends

A key trend in cybersecurity is the adoption of Zero Trust Architecture, which follows the principle of “never trust, always verify.” It ensures every access request is thoroughly authenticated, minimizing security breaches. Additionally, AI and ML play a crucial role in endpoint security by analyzing data, identifying patterns, and detecting anomalies. This helps organizations proactively detect and mitigate threats before they cause harm.

Extended Detection and Response (XDR) is another emerging trend that offers a holistic approach to threat detection and response. XDR integrates data from various security layers, providing a unified view that enhances the ability to detect and respond to threats across endpoints, networks, and cloud environments.

Remote work and BYOD policies have expanded the attack surface, making Unified Endpoint Management (UEM) essential for enforcing consistent security and compliance across all devices. Additionally, deception technology adds a proactive defense by using decoys to detect and analyze threats that may evade traditional security tools.

Business Benefits

Endpoint protection acts as a vigilant guardian for every device connected to a business network. It continuously monitors for malicious activity, quickly detecting and neutralizing threats like malware and ransomware. This proactive approach helps prevent breaches and reduces the risk of data loss and system compromise.

Endpoint protection helps businesses adhere to data protection laws by securing sensitive information across all devices. It ensures that data handling practices meet regulatory standards, thereby avoiding potential legal penalties.

By preventing security incidents before they escalate, endpoint protection reduces the financial impact associated with data breaches and system downtimes. It minimizes the need for extensive recovery efforts and potential regulatory fines. Investing in robust endpoint security is a cost-effective strategy that protects both the organization’s assets and its bottom line.

Key Player Analysis

The Endpoint Threat Protection Market is growing rapidly as cyber threats become more advanced and frequent.

Broadcom has become a major name in the endpoint threat protection space after acquiring Symantec’s enterprise security business. Broadcom offers scalable, integrated solutions with deep endpoint visibility, ideal for large enterprises. Their unified approach enhances threat management across complex IT environments, reducing risk effectively.

Trend Micro Incorporated is recognized for its strong cloud security and AI-driven threat detection. Trend Micro provides advanced endpoint protection favored by midsize and large enterprises. It stands out with predictive analytics, machine learning, and seamless integration with cloud platforms like AWS and Azure, ideal for hybrid environments.

Sophos has built a reputation for user-friendly security solutions without compromising on depth. Sophos’ Intercept X uses deep learning and anti-ransomware tech to defend against zero-day attacks. With centralized management via Sophos Central, it’s ideal for IT teams handling multiple endpoints. Sophos is also known for affordable, powerful solutions for SMBs.

Top Key Players in the Market

- Broadcom

- Trend Micro Incorporated

- Sophos Ltd.

- Microsoft

- AO Kaspersky Lab

- Panda Security

- F-Secure

- IBM Corporation

- McAfee, LLC.

- ESET, spol. s r.o.

- Cisco Systems, Inc.

- Bitdefender

- Others

Top Opportunities for Players

The endpoint threat protection industry is poised for significant growth, driven by evolving cyber threats and technological advancements.

- Integration of Artificial Intelligence and Machine Learning: AI and ML in endpoint security improve threat detection and response by recognizing patterns and anomalies, enabling proactive defense against advanced cyber threats. The growing reliance on AI-driven security measures presents a substantial opportunity for innovation and market expansion.

- Expansion of Remote Work and BYOD Policies: The shift towards remote work and the adoption of Bring Your Own Device (BYOD) policies have increased the number of endpoints accessing corporate networks. This expansion necessitates robust endpoint protection solutions capable of securing diverse devices and ensuring data integrity across various access points.

- Growth of Small and Medium Enterprises (SMEs) Market: SMEs are increasingly recognizing the importance of cybersecurity, leading to a rise in demand for affordable and scalable endpoint protection solutions. Tailoring products to meet the specific needs of SMEs, such as ease of deployment and cost-effectiveness, offers a significant market opportunity.

- Adoption of Cloud-Based Security Solutions: The transition from on-premise to cloud-based infrastructures has created a demand for endpoint security solutions that can seamlessly integrate with cloud environments. Cloud-based security offers scalability, centralized management, and real-time threat intelligence, making it an attractive option for organizations.

- Emphasis on Regulatory Compliance and Data Privacy: Increasing regulatory requirements concerning data protection and privacy are compelling organizations to invest in comprehensive endpoint security solutions. Ensuring compliance with standards such as GDPR and HIPAA necessitates advanced security measures, presenting an opportunity for providers to offer compliance-focused features.

Recent Developments

- In April 2025, Bitdefender launched GravityZone PHASR, an endpoint security solution emphasizing proactive hardening and attack surface reduction.

- In 2024, Kaspersky introduced “Kaspersky Next,” a product line combining Endpoint Protection Platform (EPP), Endpoint Detection and Response (EDR), and Extended Detection and Response (XDR) functionalities.

- In March 2024, Broadcom formed an Enterprise Security Group by merging Symantec and Carbon Black to combine Symantec’s prevention and anti-malware strengths with Carbon Black’s post-attack forensic and EDR capabilities, aiming to provide a unified, comprehensive endpoint security solution.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 17.42 Bn |

| Forecast Revenue (2034) | USD 38 Bn |

| CAGR (2025-2034) | 8.10% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solution (Antivirus, Application Control, Endpoint Encryption, Endpoint Detection and Response, Firewall, Mobile Security Tools, Others), Services (Consulting, Managed, Training & Support)), By Deployment (On-premise, Cloud), By Organization (Large Enterprise, SME), By Application (IT & telecom, BFSI, Industrial, Education, Retail, Healthcare, Government & Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Broadco, Trend Micro Incorporated, Sophos Ltd., Microsoft, AO Kaspersky Lab, Panda Security, F-Secure, IBM Corporation, McAfee, LLC., ESET, spol. s r.o., Cisco Systems, Inc., Bitdefender, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |