Quick Navigation

Report Overview

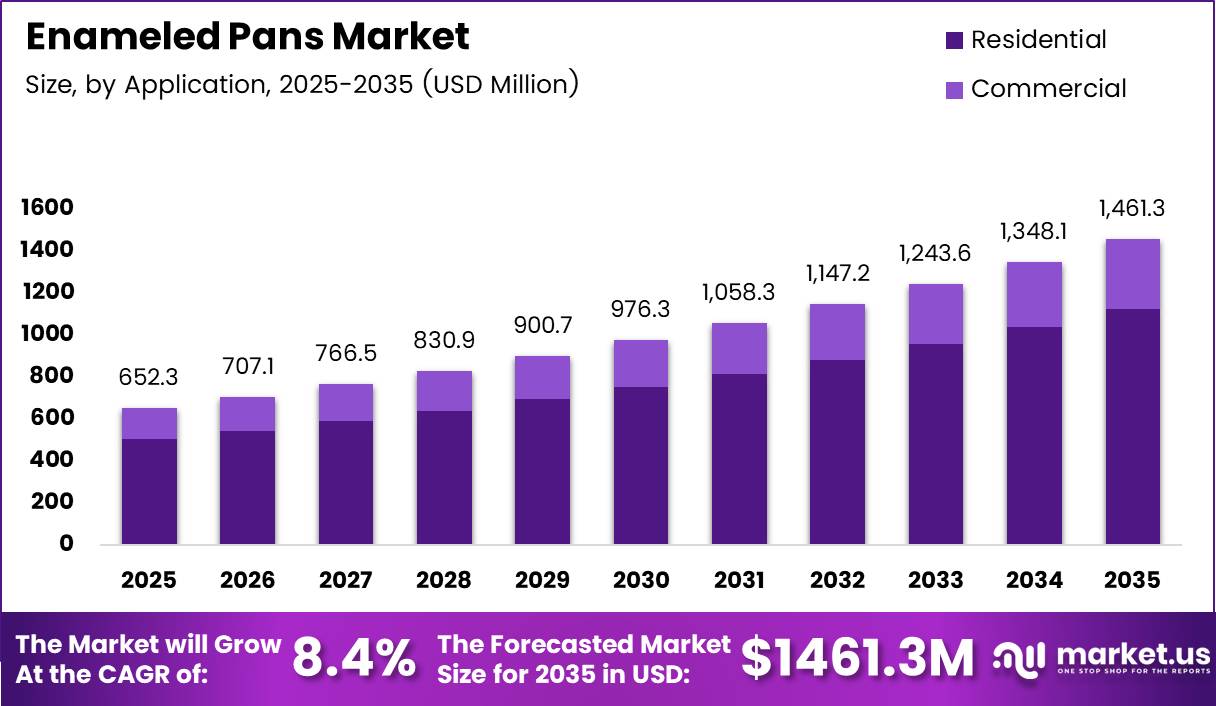

Global Enameled Pans Market size is expected to be worth around USD 1,461.3 Million by 2035 from USD 652.3 Million in 2025, growing at a CAGR of 8.4% during the forecast period 2026 to 2035.

Enameled pans combine cast iron or steel cores with a glass-derived porcelain coating that bonds at high temperatures. This construction eliminates direct metal contact with food, making the cookware non-reactive to acidic and alkaline ingredients. Home cooks and professional kitchens both rely on this property for precise flavor control and food safety.

Consumer behavior is shifting from disposable non-stick products toward cookware built to last decades. Households are replacing standard pans less frequently and investing more per unit. This trade-up behavior compresses volume growth but expands revenue per transaction, which benefits premium manufacturers with strong brand equity.

The residential segment anchors demand, with home cooking culture strengthening across North America, Europe, and Asia Pacific. Millennials and younger households treat kitchen equipment as part of home identity. Colorful, oven-safe, and stovetop-versatile enameled pans fit this preference precisely, offering both performance and visual appeal.

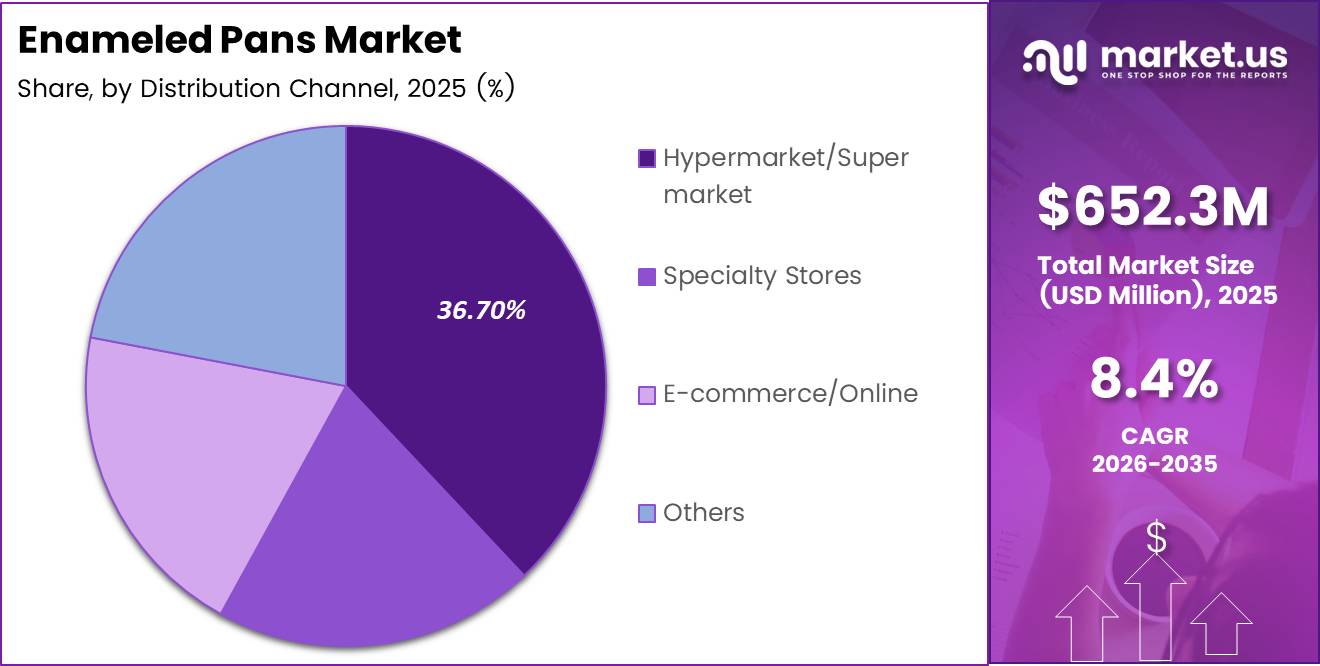

Retail channels have diversified, but online platforms now function as the primary discovery and research layer before purchase. Specialty kitchen stores retain a role in high-value conversions. Hypermarkets and supermarkets still lead distribution at 36.70% share, capturing volume-driven purchases across mass-market price tiers.

In March 2024, Le Creuset launched its Alpine Outdoor Collection, introducing enameled cast iron cookware designed specifically for open-flame outdoor cooking. This move signals that leading brands are extending the category beyond the indoor kitchen, targeting a new segment of outdoor culinary enthusiasts.

According to a 2025 cookware durability analysis by Kitchendemy, porcelain enamel cookware scored 9 out of 10 on durability, outperforming stainless steel at 6/10 and traditional cast iron at 7/10. This positions enameled pans as the highest-performing mainstream cookware material when long-term wear resistance is the buying criterion. The same analysis rated non-stick cookware at just 4 out of 10, meaning buyers replacing non-stick products face a clear and data-supported upgrade path toward enameled alternatives.

Key Takeaways

- The global Enameled Pans Market is valued at USD 652.3 Million in 2025 and is forecast to reach USD 1,461.3 Million by 2035.

- The market grows at a CAGR of 8.4% from 2026 to 2035.

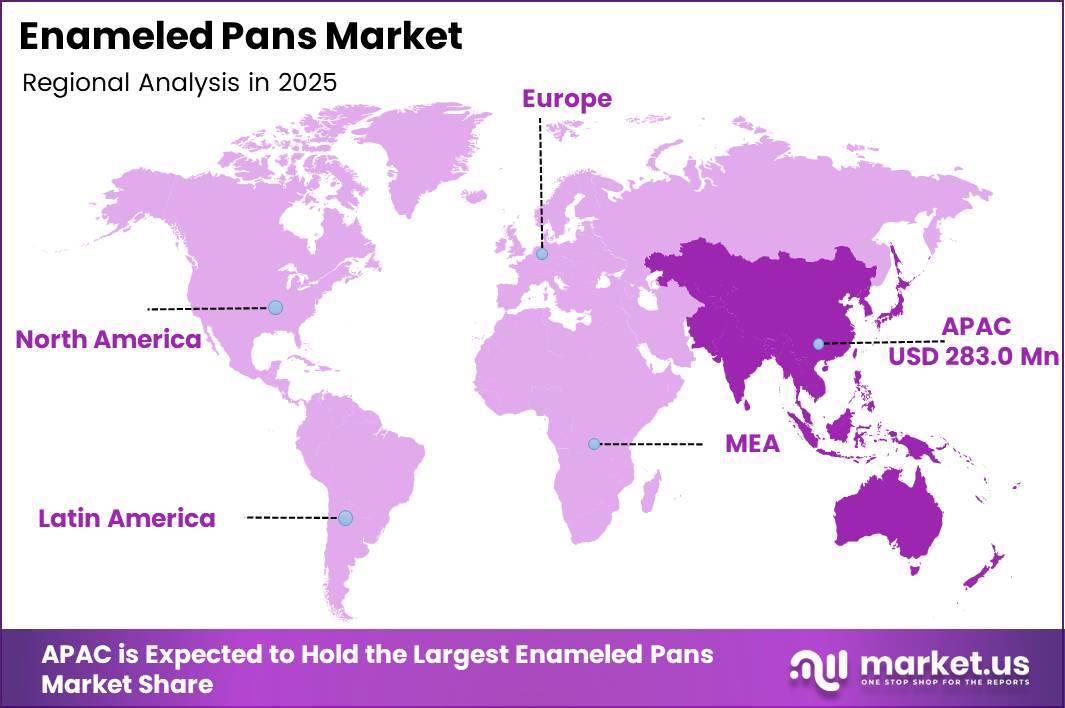

- Asia Pacific holds the largest regional share at 43.40%, valued at USD 283.0 Million in 2025.

- By Application, the Residential segment dominates with a 76.9% market share.

- By Distribution Channel, Hypermarket/Supermarket leads with a 36.70% share.

- Porcelain enamel cookware scores 9/10 on durability, compared to non-stick at 4/10, driving trade-up purchasing decisions.

- Le Creuset expanded into outdoor cooking in March 2024 and launched a single-serve hospitality line in March 2025, signaling active product category extension.

Application Analysis

Residential dominates with 76.9% due to rising home cooking and premium pan investment.

In 2025, Residential held a dominant market position in the By Application segment of the Enameled Pans Market, with a 76.9% share. Home kitchens drive the majority of enameled pan purchases because consumers increasingly invest in long-lasting cookware. According to a 2025 maintenance guide by BHG, preheating enameled cast iron for 3 minutes on low heat before cooking reduces thermal shock and improves performance, confirming that residential buyers actively seek performance-optimized products.

Commercial buyers include restaurants, hotel kitchens, and catering operations that prioritize consistent thermal retention and professional presentation. Commercial adoption has been constrained by the higher unit cost of enameled cookware relative to stainless steel alternatives. However, premium foodservice operators increasingly specify enameled cast iron for oven-to-table serving formats, creating a slow but steady volume channel in this sub-segment.

Distribution Channel Analysis

Hypermarket/Supermarket dominates with 36.70% due to high footfall and broad mid-tier product access.

In 2025, Hypermarket/Supermarket held a dominant market position in the By Distribution Channel segment of the Enameled Pans Market, with a 36.70% share. Mass retail formats give enameled pans high visibility among consumers who do not actively seek specialty kitchen stores. Volume-tier brands benefit most from this channel, converting impulse and planned purchases across a broad consumer base.

Specialty Stores serve consumers who arrive with informed buying intent and higher per-unit budgets. These outlets allow in-person product comparison and staff-assisted guidance, which suits high-ticket enameled pan purchases from brands such as Le Creuset and Staub. Conversion rates in specialty retail tend to be higher, even at lower traffic volumes compared to mass retail formats.

E-commerce and Online channels function as the primary research layer for most cookware purchases today. Consumers compare materials, reviews, and price tiers before committing. Online platforms capture a growing share of final transactions, particularly for repeat buyers and gift purchases. According to a 2025 article by Southern Living, soaking enameled cast iron in warm soapy water for 15 to 20 minutes removes stuck food safely, reflecting the depth of care content that online cookware communities generate and share, reinforcing brand loyalty in this channel.

Others include department stores, direct-to-consumer brand websites, and catalog retail. This sub-segment captures niche and premium buyers who prefer brand-direct purchasing for warranty assurance and exclusive colorways. Brand websites in particular support customer retention through loyalty programs and limited-edition product releases.

Key Market Segments

By Application

- Residential

- Commercial

By Distribution Channel

- Hypermarket/Supermarket

- Specialty Stores

- E-commerce/Online

- Others

Drivers

Consumer Rejection of Reactive and Chemical-Laden Cookware Accelerates Enameled Pan Adoption

Consumers across developed markets are actively moving away from PTFE-coated and reactive metal cookware. Health concerns around chemical leaching have reached mainstream awareness, particularly among households with young children. Enameled pans provide a glass-based barrier between food and metal, eliminating the chemical migration risk that competitors cannot resolve without a redesign.

According to a 2025 scientific study published in Coatings, elemental release from porcelain enamel surfaces remained within European Union potable-water regulatory limits during corrosion testing. This is a commercially significant finding. It means enameled pan manufacturers can credibly cite regulatory compliance in product marketing, giving them a verifiable safety advantage over alternatives that lack comparable certification data.

This regulatory backing translates directly into purchasing confidence at the point of sale. Buyers who research cookware safety find a consistent body of evidence supporting porcelain enamel. Brands that communicate this data clearly hold a structural advantage over those relying on positioning alone. The safety narrative is both scientifically grounded and accessible to a general consumer audience.

Restraints

Enamel Coating Fragility and Low-Cost Cookware Alternatives Limit Market Penetration

Enameled pans chip and crack when dropped, overheated, or washed in dishwashers repeatedly. This vulnerability is a real barrier for buyers who want low-maintenance cookware. For consumers who purchase cookware based on durability alone, the perception of fragility outweighs the chemical safety benefits, particularly in emerging markets where replacement costs are a primary concern.

According to a 2025 comparison study by Kitchendemy, copper cookware scored 9 out of 10 on durability, matching porcelain enamel cookware exactly. Copper is widely available at similar or lower price points in many markets. This creates a direct durability substitute that buyers can reference when comparing options. Enameled pans lose their differentiation when durability is the sole purchase criterion.

Stainless steel and aluminum cookware add further competitive pressure at the value end of the market. These materials resist physical damage better than enamel coatings under harsh kitchen conditions. Price-sensitive buyers in both residential and commercial segments regularly choose these alternatives. Manufacturers must address both the price gap and the durability perception to capture this buyer segment.

Growth Factors

Premiumization, Sustainability Demand, and Brand Expansion into New Geographies Create High-Value Revenue Channels

Demand for eco-friendly cookware materials is rising across Western Europe and North America, where consumers connect sustainable sourcing with purchase decisions. Enameled cast iron is mineral-based, contains no synthetic polymers, and lasts decades when maintained correctly. This product profile aligns directly with the sustainability preferences of environmentally conscious buyers who are willing to pay a premium for long-cycle goods.

According to Staub’s 2025 production data, each enameled cast iron piece requires approximately 3 days of production time and the involvement of 30 artisans during manufacturing. This production complexity is a commercial asset. It validates premium pricing, creates a natural story for brand content, and establishes a genuine quality barrier that low-cost manufacturers cannot replicate at scale.

In September 2024, GreenPan partnered with Bobby Flay to launch a new collection that included enameled Dutch ovens and cast iron cookware. Celebrity and influencer endorsements accelerate category awareness among consumers who follow culinary culture. This partnership model compresses the adoption curve for newer entrants and expands the total audience for enameled cookware beyond traditional premium kitchen buyers.

Emerging Trends

Induction Compatibility, Retro Aesthetics, and Multi-Purpose Design Are Redefining Enameled Pan Buyer Expectations

Induction cooktops now represent a large and growing share of new kitchen installations across Europe and Asia. Enameled pans with ferromagnetic bases capture buyers who are upgrading both their cooktops and cookware simultaneously. Manufacturers that certify induction compatibility and optimize heat distribution for glass-ceramic surfaces gain an immediate specification advantage in new kitchen projects.

Vintage and retro-style enamel cookware collections are attracting a buyer segment that treats kitchen tools as part of interior design. Social media platforms amplify this trend by making cookware visible as a lifestyle statement. Limited-edition colorways and heritage-inspired shapes generate strong organic engagement, creating earned media value that reduces brand acquisition costs per customer.

According to the 2025 study in Coatings, alkaline exposure caused stronger degradation effects on porcelain enamel surfaces than either pure water or acidic environments during durability testing. This finding has direct implications for oven-to-table product design. Brands investing in multi-purpose enameled pans suitable for dishwasher and high-alkaline cleaning cycles must reformulate enamel compositions to maintain surface integrity and sustain the category’s long-life value proposition.

Regional Analysis

Asia Pacific Dominates the Enameled Pans Market with a Market Share of 43.40%, Valued at USD 283.0 Million

Asia Pacific leads all regions with a 43.40% share, valued at USD 283.0 Million in 2025. Rapid urbanization, rising household incomes, and the expansion of modern retail infrastructure across China, Japan, South Korea, and India drive this position. Consumers in these markets are moving toward premium and health-conscious cookware as middle-class purchasing power expands into discretionary kitchen upgrades.

North America Enameled Pans Market Trends

North America holds a strong position built on established premium cookware culture and high consumer awareness of non-toxic cooking materials. The US market supports strong brand loyalty among established players with deep retail and e-commerce distribution. Health-driven purchasing behavior among millennial households sustains unit price growth across specialty and online channels.

Europe Enameled Pans Market Trends

Europe combines a long heritage of enameled cookware manufacturing with strong consumer preference for certified, food-safe materials. France, Germany, and the UK anchor regional demand. European buyers are highly responsive to sustainability credentials and quality provenance narratives. Regulatory standards across the EU provide a compliance floor that favors established enamel producers over low-cost imports.

Latin America Enameled Pans Market Trends

Latin America represents an underpenetrated market where urban middle-class growth is the primary demand driver. Brazil and Mexico lead adoption. Distribution infrastructure limitations and price sensitivity constrain premium cookware penetration. However, e-commerce expansion is lowering the barrier for international brands entering these markets without a physical retail footprint.

Middle East & Africa Enameled Pans Market Trends

The Middle East and Africa region shows early-stage growth anchored in Gulf Cooperation Council markets, where luxury goods spending supports premium kitchenware adoption. High-income urban households in the GCC purchase imported premium cookware as part of aspirational home furnishing behavior. Africa remains largely volume-constrained, with growth concentrated in major urban centers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Le Creuset holds the most defensible position in the global enameled pans market through consistent product innovation and deliberate category expansion. The brand launched an Alpine Outdoor Collection in March 2024 and followed with the Gourmand single-serve hospitality line in March 2025. This dual-channel strategy extends revenue beyond residential kitchens into outdoor cooking and foodservice markets simultaneously.

Staub competes on manufacturing craft and product authenticity. Each enameled cast iron piece requires 3 days of production time and 30 artisans. This production narrative directly supports premium pricing and positions Staub against volume manufacturers that cannot replicate handcraft complexity. The brand’s core strength is converting the production process itself into a marketing asset that sustains price premium.

Vermicular targets the high-precision cooking segment with Japanese manufacturing standards and tight quality tolerances in its enameled cast iron products. The brand’s technical positioning appeals to culinary enthusiasts who treat cookware as precision equipment rather than kitchen commodity. This focus limits volume but protects margin and creates a loyal buyer base resistant to promotional pricing by mass-market alternatives.

Lodge Cast Iron occupies the accessible premium tier, offering enameled cast iron products at price points that reach volume buyers beyond the luxury segment. Lodge’s domestic US manufacturing and wide retail distribution give it a structural reach advantage. The brand benefits from the broader shift away from non-stick cookware without requiring the brand-building investment that fully premium players sustain.

Key Players

- Le Creuset

- Staub

- Vermicular

- Lodge Cast Iron

- Framontina

- Williams-Sonoma Inc.

- Emile Henry Ltd.

- Fissler

- Camp Chef (Vista Outdoor Inc.)

- Cuisinart

Recent Developments

- September 2024 – Caraway launched its Enameled Cast Iron Cookware Collection featuring non-toxic, maintenance-free enameled pans with three-layer enamel coating technology, targeting health-conscious residential buyers seeking chemical-free cookware alternatives.

- March 2025 – Le Creuset launched the Gourmand Collection, its first enameled cast iron single-serve cookware line developed initially for hospitality and foodservice markets, signaling active expansion beyond the residential segment.

- February 2026 – Le Creuset introduced “Forêt,” its first new cookware color launch of 2026, expanding its enameled cast iron portfolio with a deep evergreen matte-finish design targeting design-conscious residential buyers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 652.3 Million |

| Forecast Revenue (2035) | USD 1,461.3 Million |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Residential, Commercial), By Distribution Channel (Hypermarket/Supermarket, Specialty Stores, E-commerce/Online, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Le Creuset, Staub, Vermicular, Lodge Cast Iron, Framontina, Williams-Sonoma Inc., Emile Henry Ltd., Fissler, Camp Chef (Vista Outdoor Inc.), Cuisinart |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |