Quick Navigation

- Report Overview

- Key Takeaway

- EDI Software Statistics

- U.S. EDI Software Market Size

- Component Analysis

- Enterprise Size Analysis

- Industry Vertical Analysis

- Growth Factors Analysis

- Emerging Trend Analysis

- Key Market Segments

- Drivers

- Restraint

- Opportunities

- Challenges

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

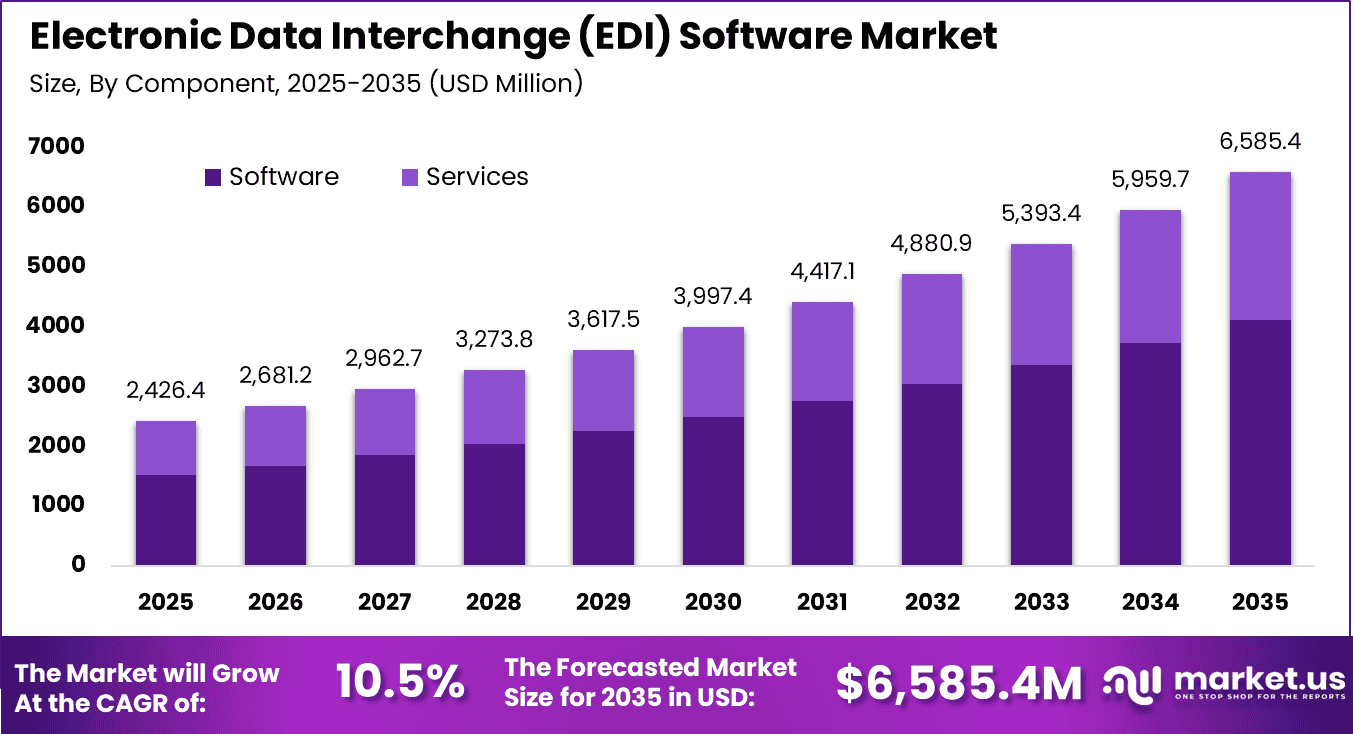

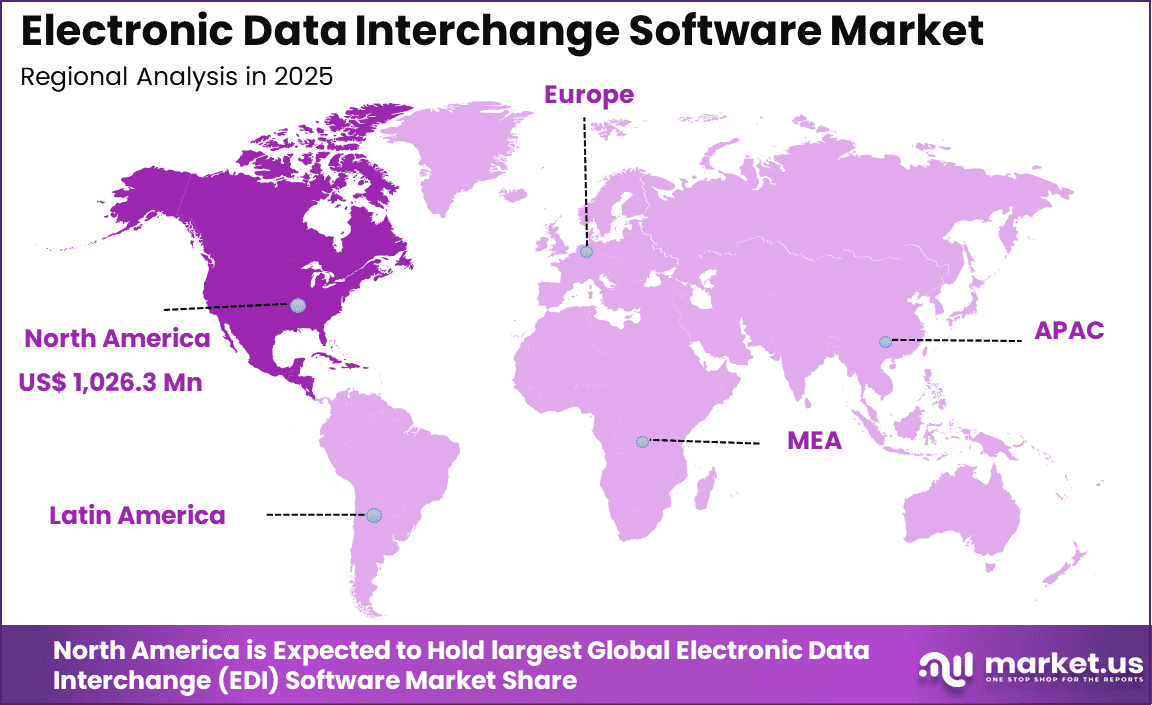

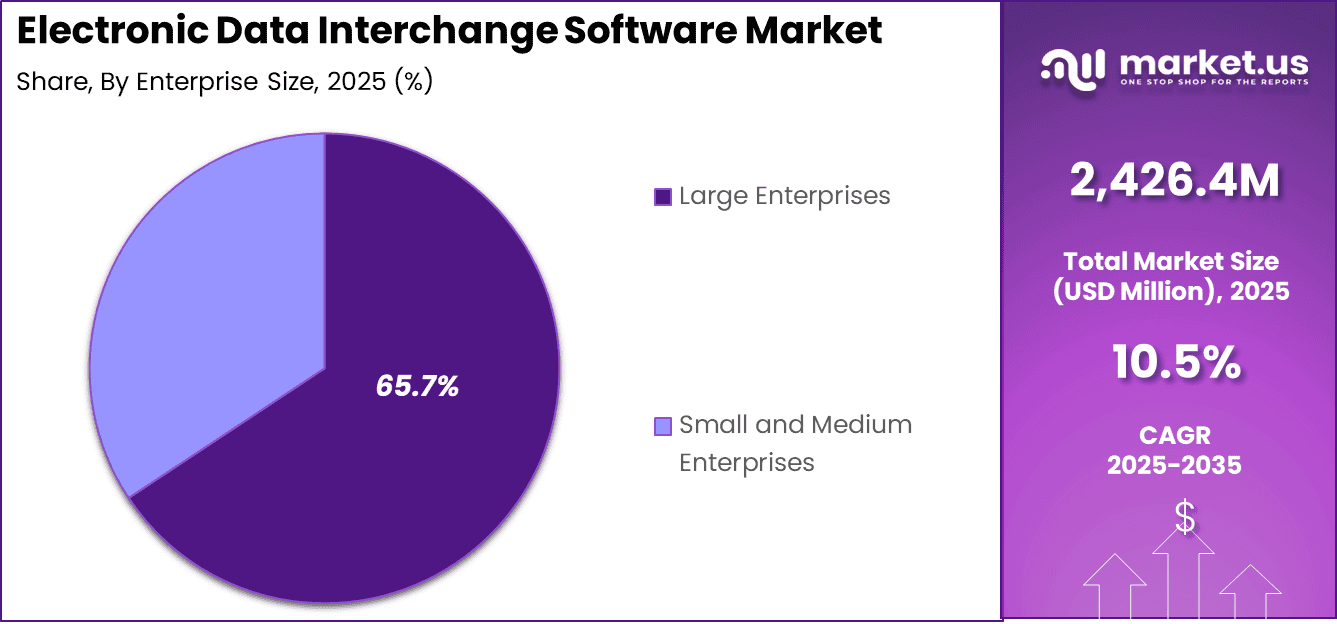

The Global Electronic Data Interchange (EDI) Software Market size is expected to be worth around USD 6,585.4 million by 2035, from USD 2,426.4 million in 2025, growing at a CAGR of 10.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 42.3% share, holding USD 1,026.3 million in revenue.

Electronic Data Interchange (EDI) software refers to a digital solution that allows businesses to exchange documents such as invoices, purchase orders, shipping notices, and payment records in a standard electronic format. It helps reduce manual entry, improves transaction accuracy, speeds up communication between partners, and supports smoother operations across supply chain and procurement activities.

Businesses are operating under greater supply chain pressure, and Electronic Data Interchange helps by connecting trading partners in real time. Around 70% of large firms report that faster data sharing supports global demand management. The rapid expansion of e-commerce is also increasing the need for dependable systems that can process large transaction volumes efficiently every day.

The market for Electronic Data Interchange (EDI) Software is driven by the growing need for faster, more accurate, and automated business document exchange. Companies are using EDI to reduce manual work, improve supply chain coordination, and support real time communication with trading partners. Rising e-commerce activity, digital compliance requirements, and wider cloud adoption are also encouraging businesses to invest in more efficient EDI solutions.

Demand for Electronic Data Interchange continues to rise as companies move away from fax-based and email-based communication. Studies show that 80% of manufacturers now depend on digital exchanges to reduce the risk of stockouts and delays. Adoption is also expanding among small businesses, as cloud-based options lower entry barriers and reduce initial investment requirements.

For instance, in November 2025, MuleSoft LLC (Salesforce) launched Anypoint EDI Connector 5.0 with native AS4 protocol support. This addresses European regulatory demands while maintaining API-first flexibility. Early feedback highlights 50% faster partner integrations versus legacy solutions.

Key Takeaway

- The software segment led the global electronic data interchange software market in 2025, accounting for 62.5% share, supported by growing demand for automated business document exchange and workflow efficiency.

- Large enterprises dominated the market with a 65.7% share, reflecting stronger investment capacity and higher transaction volumes across complex supply chains.

- The retail and consumer goods segment emerged as the leading industry vertical, capturing 22.3% share, driven by the need for faster, standardized, and error-free exchange of order and inventory data.

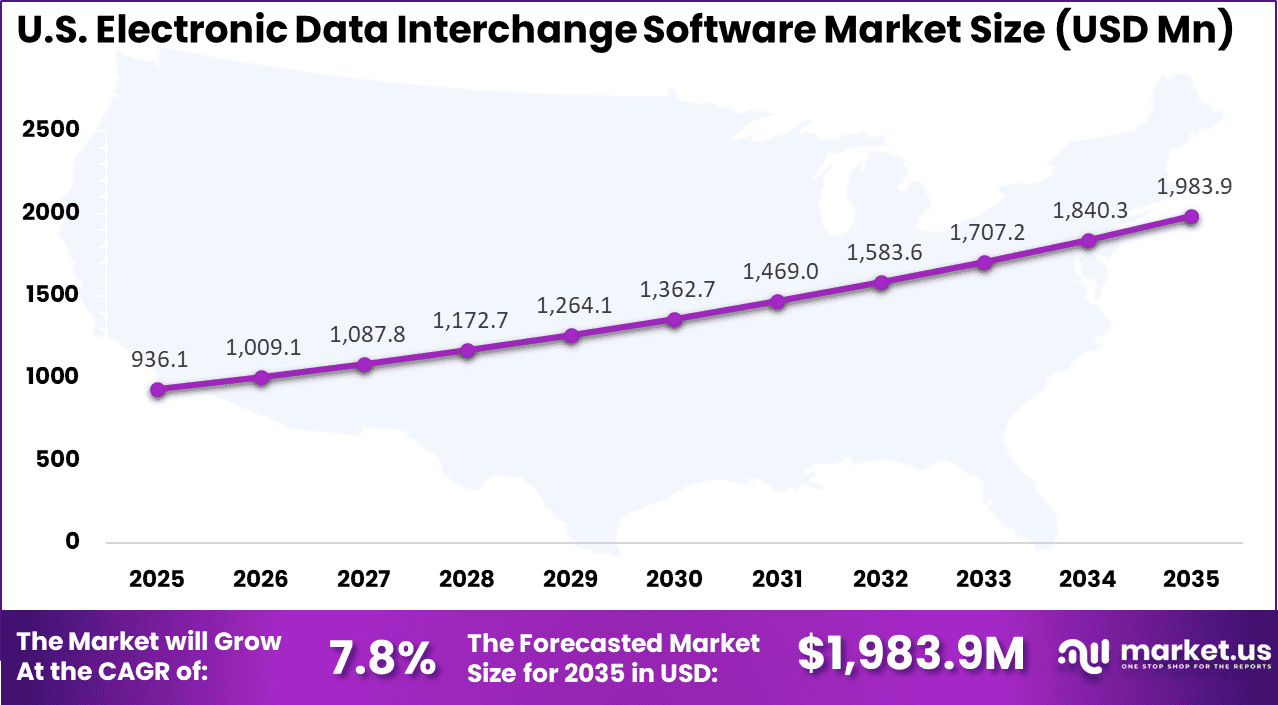

- The U.S. electronic data interchange software market reached USD 936.1 million in 2025, expanding at a CAGR of 7.8%, supported by rising digital integration across enterprise operations.

- North America maintained its leading position globally, capturing over 42.3% share, supported by mature IT infrastructure and broad adoption of supply chain automation solutions.

EDI Software Statistics

- A paper purchase order costs $30+ to process; an EDI transaction costs less than $1

- EDI can cut order processing time by 60-80% when integrated with ERP systems

- 60% of businesses fail to implement EDI successfully; 63% of IT decision-makers say partner onboarding takes too long

- 85% of SMEs using cloud-based EDI say it helps them compete with larger businesses

- ANSI ASC X12 is used by 300,000+ companies worldwide; UN/EDIFACT dominates outside the U.S.

- GS1 US estimates EDI transactions save companies $1 to $3 per document, compounding to significant ROI at scale

- EDI reduces errors from manual data entry, with 60% of B2B transactions reported to be affected or suspended due to data-related anomalies in non-EDI environments

U.S. EDI Software Market Size

The market for Electronic Data Interchange (EDI) Software within the U.S. is growing tremendously and is currently valued at USD 936.1 million, the market has a projected CAGR of 7.8%. The market is growing steadily due to rising demand for faster, more accurate, and paperless business transactions.

Companies across retail, healthcare, manufacturing, and logistics are adopting EDI to improve supply chain visibility and reduce manual errors. Growth is also supported by expanding e-commerce activity, stronger compliance needs, and increasing use of cloud-based platforms that make EDI more accessible and scalable for businesses.

For instance, in June 2025, TrueCommerce in Pennsylvania expanded its EDI platform with multi-enterprise visibility features, connecting 75,000+ trading partners across North America. Their enhanced Quote-to-Cash automation reinforces U.S. companies’ competitive edge in seamless retail and manufacturing supply chains.

In 2025, North America held a dominant market position in the Global Electronic Data Interchange (EDI) Software Market, capturing more than a 42.3% share, holding USD 1,026.3 million in revenue. This dominance is due to its strong digital infrastructure, high enterprise technology adoption, and mature supply chain networks.

Businesses across retail, healthcare, manufacturing, and logistics have widely integrated EDI into daily operations to improve speed and accuracy. The region also benefits from strict compliance standards, strong cloud adoption, and early investment in automation, which continues to support market leadership.

For instance, in March 2025, SPS Commerce from Minneapolis enhanced North America’s EDI dominance by launching AI-powered supply chain analytics within its Fulfillment Cloud platform. This innovation helps retailers achieve 99.9% EDI compliance while gaining real-time insights, solidifying U.S. leadership in automated B2B commerce networks.

Component Analysis

In 2025, The Software segment held a dominant market position, capturing a 62.5% share of the Global Electronic Data Interchange (EDI) Software Market. This dominance is due to the essential role software plays in managing digital document exchange and automation. It enables businesses to connect systems, validate transactions, and streamline workflows. Companies rely on software to reduce manual effort and ensure smooth communication across partners in complex supply chain environments.

Software solutions also support integration with enterprise systems, improving data flow and operational visibility. They help organizations handle large transaction volumes with better accuracy and consistency. As businesses focus on efficiency and digital transformation, software continues to be the backbone of modern EDI operations.

For Instance, in March 2026, SPS Commerce Inc. launched a new software update focused on faster data mapping for partners. This move helps businesses handle more transactions without slowdowns. Companies love it because the setup feels straightforward now, cutting down on tech headaches during busy seasons.

Enterprise Size Analysis

In 2025, the Large Enterprises segment held a dominant market position, capturing a 65.7% share of the Global Electronic Data Interchange (EDI) Software Market. This dominance is due to the high transaction volumes and complex operations handled by large enterprises. These organizations require structured systems to manage communication with multiple partners. EDI helps them maintain consistency, improve speed, and reduce manual errors across different departments and supply chain networks.

Large enterprises also invest more in advanced integration and automation tools to improve efficiency. Their need for real time data exchange and compliance with industry standards further supports adoption. This allows them to strengthen coordination, improve visibility, and maintain strong relationships with global partners.

For instance, in January 2026, OpenText Corporation teamed up with big manufacturers for enterprise-wide EDI rollouts. The partnership targets complex networks, making integration less of a chore. Large firms appreciate the scalability that matches their growth without constant tweaks.

Industry Vertical Analysis

In 2025, The Retail and Consumer Goods segment held a dominant market position, capturing a 22.3% share of the Global Electronic Data Interchange (EDI) Software Market. This dominance is due to the fast paced nature of retail operations, where timely and accurate data exchange is critical. Businesses in this sector depend on EDI to manage orders, shipments, and inventory updates efficiently. It helps improve coordination between suppliers and retailers while reducing delays and errors.

Retail and consumer goods companies also benefit from improved visibility across their supply chains. EDI supports better inventory planning and faster response to changing customer demand. This enables smoother operations, improved service levels, and stronger collaboration between all parties involved in the distribution process.

For Instance, in February 2026, MuleSoft LLC expanded its retail EDI options with API links for e-commerce. Shoppers and managers see faster order confirmations, easing peak season rushes. The focus on consumer trends makes it practical for chains handling varied demands.

Growth Factors Analysis

Supply Chain Automation and Faster B2B Data Exchange

The growth of the Electronic Data Interchange software market is being supported by the continued push toward supply chain automation and standardized digital business messaging. GS1 states that EDI standards enable automated business transactions, while GS1 guidance also highlights benefits such as higher productivity, cost efficiency, faster exchange, and improved accuracy. These advantages remain important for industries that depend on high-volume order, invoice, shipment, and inventory communication across trading partners.

Another growth factor is the movement toward cloud-based and managed EDI environments. AWS states that its B2B Data Interchange service automates EDI transformation at scale with elasticity and cost efficiency, while IBM positions cloud-based B2B integration as a way to streamline EDI and API transactions and simplify partner onboarding. This shows that the market is expanding not only because EDI remains essential, but also because deployment is becoming more flexible and easier to scale.

Emerging Trend Analysis

Convergence of EDI with APIs and Modern Integration Layers

A major trend in the EDI software market is the convergence of traditional EDI with API-led and event-driven integration models. IBM notes that EDI and B2B API solutions are increasingly being positioned together, and MuleSoft describes a modern approach where API-led connectivity helps organizations build on top of EDI document standards without losing control of critical enterprise data. This reflects a clear market shift from standalone EDI tools toward broader B2B integration platforms.

Another trend is the use of AI-assisted mapping and automation to reduce implementation effort. AWS says its B2B Data Interchange offering uses generative AI-assisted mapping to reduce the time, complexity, and cost of bi-directional EDI implementations. In practical terms, the market is moving toward platforms that not only exchange standardized documents, but also make onboarding, mapping, and workflow management easier for business users.

Key Market Segments

By Component

- Software

- On-Premises

- Cloud-based

- Services

- Implementation Services

- Consulting Services

- Managed Services

- Support and Maintenance Services

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By Industry Vertical

- Retail and Consumer Goods

- Manufacturing

- Healthcare and Life Sciences

- Automotive

- Logistics and Transportation

- Financial Services and Banking

- Telecom and IT

- Other Industry Verticals

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Supply Chain Automation

Supply chain automation is a key factor supporting the adoption of EDI software across industries. Businesses are moving toward digital workflows to replace manual processes and improve transaction speed. EDI enables faster exchange of orders, invoices, and shipping data, helping organizations manage operations with better accuracy and efficiency.

Automation also improves coordination between suppliers, distributors, and logistics partners. It reduces delays and minimizes errors caused by manual data entry. As companies aim to build responsive and efficient supply chains, EDI software continues to play an important role in supporting seamless communication and operational control.

For instance, in January 2026, SPS Commerce rolled out fresh tools to speed up supply chain tasks for retailers. Their new features turn emailed orders into digital ones right away, helping suppliers keep up with rising demands without manual work. This move lets teams focus on growth instead of paperwork, making daily flows much smoother for everyone involved.

Restraint

Integration Complexity

Integration complexity remains a major challenge in the adoption of EDI software, especially for organizations with legacy systems. Connecting EDI platforms with existing ERP or internal applications often requires technical expertise and time. This can slow down implementation and create additional costs for businesses with limited resources.

Many companies also face difficulties in standardizing data formats across multiple partners. Each partner may follow different protocols, which adds complexity to system configuration. These challenges can limit adoption among smaller firms and create barriers to achieving full operational efficiency through digital data exchange.

For instance, in February 2026, Cleo Communications faced pushback from users over linking their platform to legacy warehouse software, as mismatched data formats caused weeks of tweaks. Teams spent extra hours mapping fields between old ERPs and new EDI lines, slowing partner setups. The company now offers more templates to ease these common snags.

Opportunities

Cloud and Compliance

Cloud based EDI solutions are creating new opportunities by offering flexible and scalable deployment options. Businesses can adopt EDI without heavy infrastructure investment, making it more accessible for small and medium enterprises. Cloud platforms also support faster implementation and easier updates, improving overall system performance.

Compliance requirements related to electronic invoicing and digital reporting are further driving adoption. Organizations are using EDI to meet regulatory standards and maintain accurate records. This creates strong demand for solutions that combine cloud capabilities with compliance support, helping businesses operate more efficiently and securely.

For instance, in July 2025, OpenText updated its cloud suite with built-in tools for tracking regulatory changes in trade docs, making audits simpler for global shippers. Firms can now adjust EDI formats on the fly to match new rules, without downtime. This opens doors for expansion into stricter markets like Europe.

Challenges

Data Security

Data security remains a major challenge for the Electronic Data Interchange Software market. EDI systems handle sensitive business information such as pricing, order details, payment records, and shipping data. Any breach or unauthorized access can disrupt operations, damage trust, and create serious financial and legal concerns for businesses.

As cyber threats continue to grow, companies must invest in secure networks, encryption, access controls, and monitoring systems. Maintaining security across multiple partners and connected platforms can be difficult, especially when data moves across large supply chains. This makes protection of digital transactions a constant priority for EDI users.

For instance, in February 2026, OpenText dealt with a vulnerability alert in its directory service that exposed risks in unpatched EDI gateways, prompting urgent client notifications. Security teams had to scan networks for weak points in data handoffs, which disrupted some operations. Patches rolled out quickly to lock down sensitive order flows.

Key Players Analysis

In the Electronic Data Interchange (EDI) Software market, SPS Commerce Inc., TrueCommerce Inc., and OpenText Corporation are among the leading players due to their strong transaction management and partner connectivity capabilities. These companies help businesses automate document exchange across supply chains, retail networks, and distribution systems. Their platforms are widely used to improve order accuracy, reduce manual processing, and support compliance with trading partner requirements.

Cleo Communications Inc., IBM Corporation, MuleSoft LLC, and Dell Boomi Inc. hold an important position in this market through integration-led EDI solutions. Their offerings support hybrid IT environments, API connectivity, and secure data exchange across enterprise systems. Comarch SA, DiCentral Corporation, and Seeburger AG also strengthen the market with scalable tools designed for global B2B communication and process automation.

Descartes Systems Group Inc., E2open Holdings LLC, TIE Kinetix N.V., DataTrans Solutions Inc., 1 EDI Source Inc., Axway Software SA, Rocket Software Inc., Software AG, Edicom Group S.L., and B2BGateway.Net add strong competitive depth to the market. These companies serve a wide range of industries by offering cloud-based EDI, managed services, and specialized partner onboarding capabilities. Other key players continue to expand the market by improving interoperability, compliance support, and end-to-end visibility across digital trading networks.

Top Key Players in the Market

- SPS Commerce Inc.

- TrueCommerce Inc.

- Cleo Communications Inc.

- OpenText Corporation

- Comarch SA

- IBM Corporation

- MuleSoft LLC

- Dell Boomi Inc.

- DiCentral Corporation

- Seeburger AG

- Descartes Systems Group Inc.

- E2open Holdings LLC

- TIE Kinetix N.V.

- DataTrans Solutions Inc.

- 1 EDI Source Inc.

- Axway Software SA

- Rocket Software Inc.

- Software AG

- Edicom Group S.L.

- B2BGateway.Net

- Others

Recent Developments

- In February 2026, TrueCommerce Inc. launched TrueCommerce Cloud EDI 360, a next-gen platform with AI-powered error detection. Retailers reported 30% fewer manual interventions after deployment. This upgrade strengthens TrueCommerce’s leadership in multi-standard EDI compliance across North America and Europe.

- In April 2026, OpenText Corporation unveiled Trading Grid AI, leveraging machine learning for predictive EDI mapping. Early adopters in automotive reported 25% reduction in mapping maintenance costs. OpenText’s move positions it ahead in the AI-driven EDI transformation race.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2,426.4 Mn |

| Forecast Revenue (2035) | USD 6,585.4 Mn |

| CAGR (2026-2035) | 10.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Software, Services), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By Industry Vertical (Retail and Consumer Goods, Manufacturing, Healthcare and Life Sciences, Automotive, Logistics and Transportation, Financial Services and Banking, Telecom and IT, Other Industry Verticals) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SPS Commerce Inc., TrueCommerce Inc., Cleo Communications Inc., OpenText Corporation, Comarch SA, IBM Corporation, MuleSoft LLC, Dell Boomi Inc., DiCentral Corporation, Seeburger AG, Descartes Systems Group Inc., E2open Holdings LLC, TIE Kinetix N.V., DataTrans Solutions Inc., 1 EDI Source Inc., Axway Software SA, Rocket Software Inc., Software AG, Edicom Group S.L., B2BGateway.Net, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Software Market")