Global Educational Games Market Size, Share and Analysis Report By Component (Solution, Services), By Deployment Mode (Cloud, On-premise), By Platform (Offline, Online), By Game Type (Location-Based Games, AR/VR Games, AI-Based Games, Language Learning, Skill-Based Learning, Simulation, Others), By Application (Critical Thinking & Problem-Solving, Training & Development, Evaluation, Others), By End-user (IT & Telecom, Retail, Consumer, Manufacturing, Government, Education, Healthcare & Life Sciences, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179077

- Number of Pages: 267

- Format:

-

keyboard_arrow_up

Quick Navigation

- Educational Games Market Size

- Key Takeaway

- Report Overview

- Key Statistics

- By Component

- By Deployment Mode

- By Platform

- By Game Type

- By Application

- By End-user

- Regional Analysis

- Emerging Trends Analysis

- Growth Factors

- Key Market Segments

- Drivers

- Restraint

- Opportunities

- Key Players Analysis

- Recent Developments

- Report Scope

Educational Games Market Size

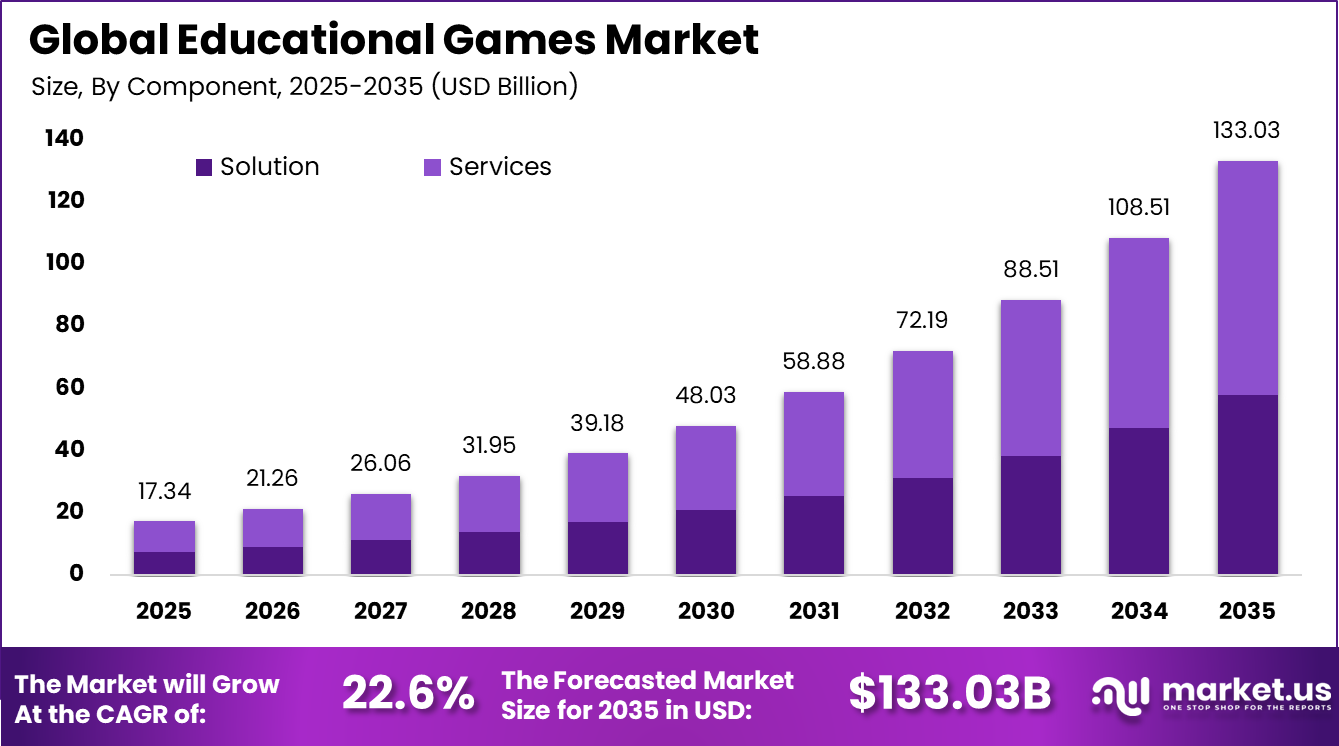

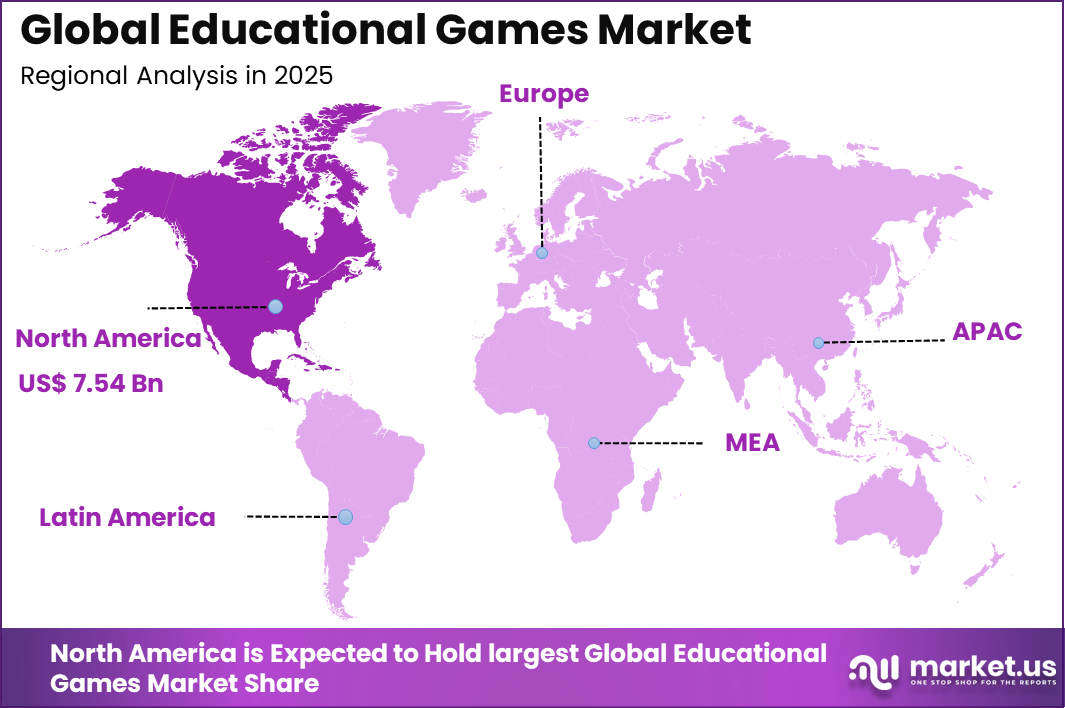

The Global Educational Games Market size is expected to be worth around USD 133.03 billion by 2035, from USD 17.34 billion in 2025, growing at a CAGR of 22.6% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 43.5% share, holding USD 7.54 billion in revenue.

More than 410,000 educational institutions worldwide have incorporated educational games into their teaching frameworks, reflecting the growing acceptance of interactive learning tools. Approximately 38% of schools have adopted gamified solutions as part of their formal curriculum delivery strategies. Educational games are currently used by over 640 million students globally, indicating strong penetration across primary, secondary, and higher education levels.

More than 72% of young learners show higher engagement levels when lessons are delivered through game-based formats compared to traditional methods. In addition, classroom efficiency improves significantly with game-based learning approaches. Studies indicate that up to 93% of class time is productively utilized when structured educational games are integrated into lesson plans, supporting better focus, participation, and knowledge retention.

Key Takeaway

- By Component, solutions accounted for 68.9%, reflecting strong demand for complete learning platforms that combine content, analytics, and engagement tools rather than standalone services.

- By Deployment Mode, cloud represented 61.2%, highlighting the shift toward scalable, remotely accessible, and centrally managed educational gaming systems.

- By Platform, online formats captured 53.1%, indicating preference for browser-based and internet-enabled access over offline installations.

- By Game Type, location-based games held 29.4%, showing growing interest in immersive and contextual learning experiences.

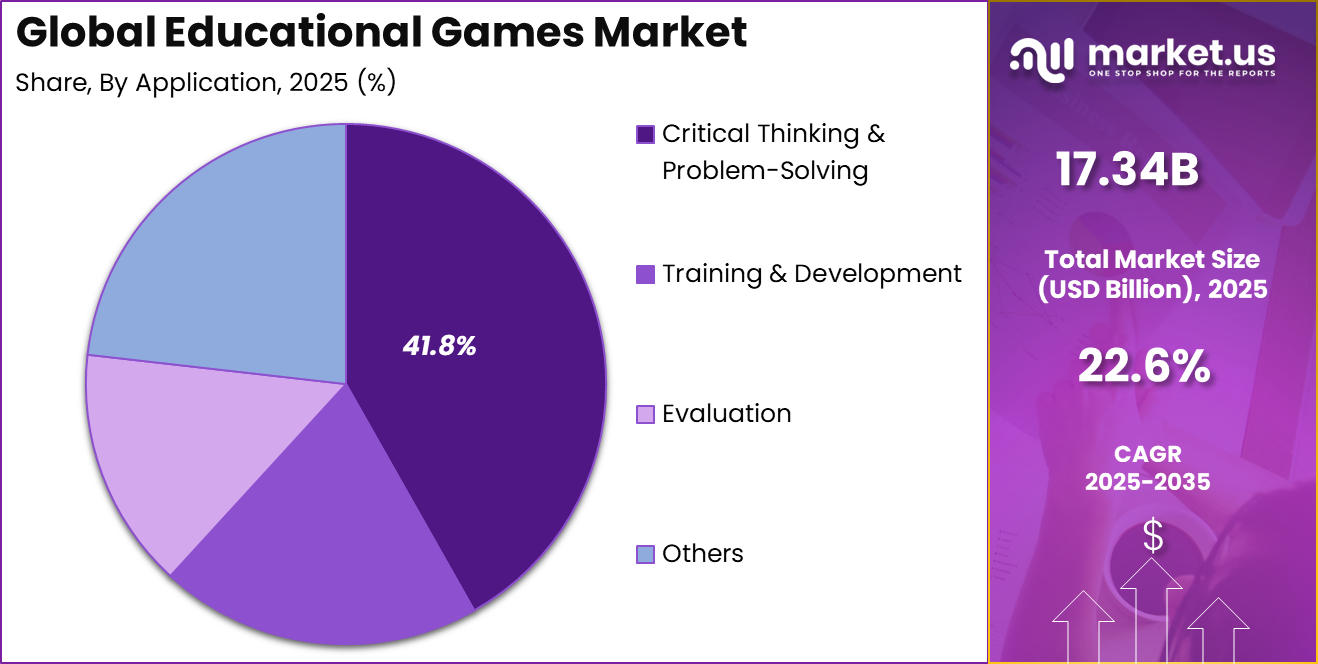

- By Application, critical thinking and problem-solving led with 41.8%, demonstrating institutional focus on higher-order cognitive skills.

- By End-user, education institutions accounted for 24.9%, confirming schools and formal learning environments as key adopters.

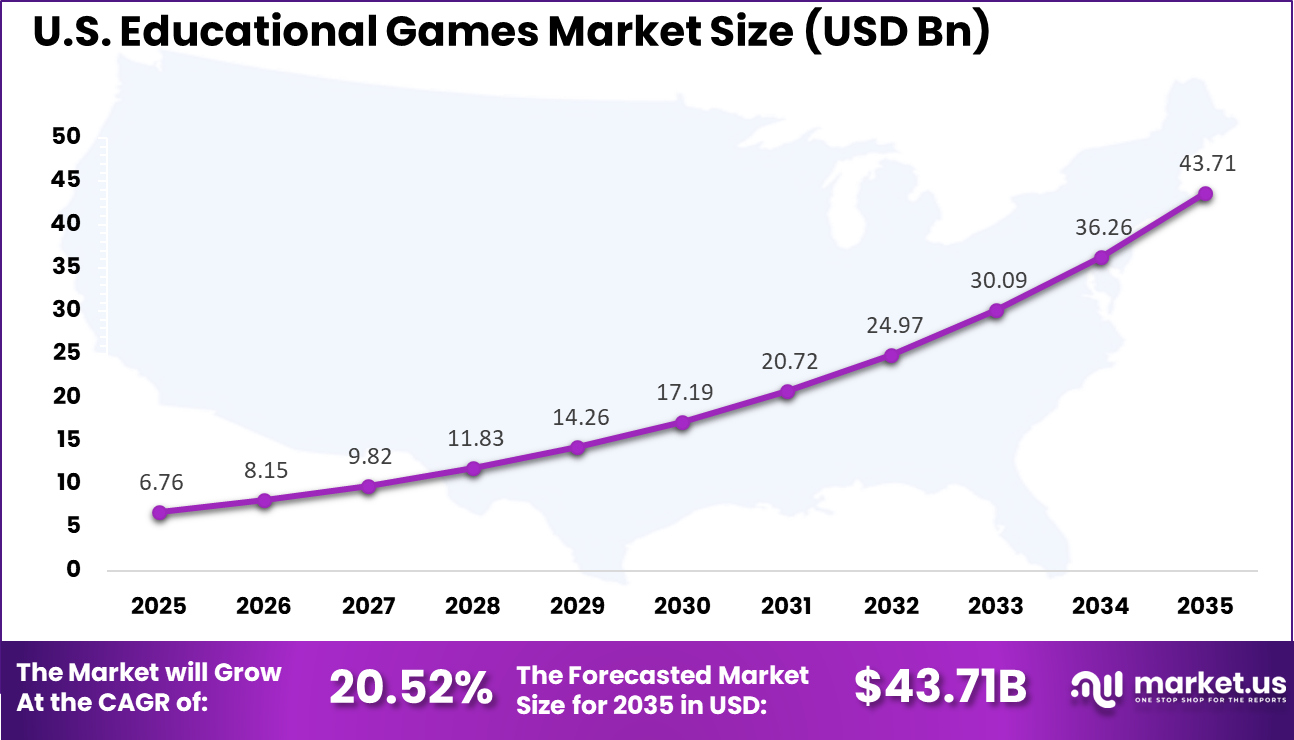

- North America represented 43.5%, with the U.S. valued at USD 6.76 Bn and reporting 20.52% CAGR as per provided inputs.

Report Overview

Educational Games Market refers to the segment of the digital learning and interactive entertainment industry where game-based formats are designed specifically to improve knowledge, cognitive ability, and skill development. These games are structured around curriculum goals, learning outcomes, or measurable competencies, and are used across schools, training institutions, and home learning environments.

The market combines pedagogy, interactive design, cloud delivery, and analytics to enhance engagement and retention. Educational games are increasingly positioned as structured learning tools rather than optional supplements. They integrate progress tracking, adaptive difficulty levels, and feedback systems that align with academic standards or skill benchmarks. Demand is driven by digital education growth and rising use of interactive learning tools.

For instance, in December 2025, Duolingo dropped Flashcard exercises and 100K+ new DuoRadio episodes across top languages. These gamified tweaks make vocab drills and listening practice feel effortless, keeping learners hooked longer.

Key Statistics

- Around 88% of teachers using digital games report higher student engagement, indicating improved classroom participation.

- Approximately 93% of class time is spent on active tasks during game-based learning sessions, compared to lower engagement levels in traditional methods.

- Selected studies show a 24.7% improvement in student performance after only two hours of structured gameplay, reflecting measurable short-term academic gains.

- In controlled assessments, student failure rates declined to 7% among game-based learners, compared to nearly 20% under conventional instruction models.

- More than 640 million students globally use educational games at least once per week, demonstrating widespread integration into learning routines.

- About 67% of K-12 schools in the United States incorporate educational gaming tools into curriculum delivery.

- Teachers identify strongest subject effectiveness in Mathematics (71%), followed by Reading (36%), while Science integration remains lower at 22%.

- Mobile-based educational games account for 54% of total usage, supported by high smartphone penetration and accessibility.

- By 2025, over 40% of game-based learning tools are expected to integrate AI-driven personalization to adapt learning paths based on student performance.

- Virtual reality learning games are expanding at a growth rate of 51.9%, reflecting increasing interest in immersive and interactive classroom experiences.

By Component

Solutions holding 68.9% indicate that buyers prefer comprehensive platforms that integrate curriculum-aligned content, assessment engines, dashboards, and teacher management tools. Institutions often require centralized systems that allow tracking of learner progress, engagement metrics, and outcome measurement. This supports adoption of bundled solutions rather than fragmented offerings.

Another reason for solution dominance is the integration of analytics and personalization features. Platforms increasingly provide adaptive learning paths where difficulty levels adjust based on student performance. This increases perceived academic value and supports measurable improvement in skill development.

In addition, education authorities and private institutions favor systems that can integrate with existing learning management systems. Compatibility with broader digital education infrastructure strengthens solution-level demand and supports long-term institutional contracts.

For Instance, in September 2025, Lumos Labs updated its brain training solutions with fresh cognitive modules. Drawing from big data insights, the enhancements focus on personalized learning paths that adapt to user progress, boosting engagement in skill-building games for schools and home use.

By Deployment Mode

Cloud-based deployment at 61.2% reflects the shift toward remote accessibility and scalable infrastructure. Schools and learning providers benefit from centralized updates, simplified maintenance, and reduced hardware dependency. Cloud models also allow easier expansion across multiple classrooms and campuses.

The cloud approach supports data synchronization across devices, enabling students to continue learning sessions seamlessly from home or school. This flexibility is important in hybrid learning models where in-person and remote instruction are combined.

Security and data protection frameworks in mature cloud environments also strengthen institutional trust. As compliance requirements in digital education rise, centralized management helps institutions maintain governance standards more efficiently.

For instance, in September 2025, Google launched Skills Boost Arcade games on cloud infrastructure. These interactive challenges teach cloud basics like storage and networking through multiplayer play, allowing seamless access across devices for global learners honing tech skills.

By Platform

Online platforms accounting for 53.1% highlight strong demand for browser-based and internet-enabled educational games. Online delivery allows quick deployment without complex installations, reducing technical barriers for schools and households. Online platforms also support multiplayer engagement, collaborative challenges, and real-time competition, which enhance motivation and engagement.

These interactive dynamics contribute to higher participation rates compared to static learning formats. Additionally, online platforms enable regular content updates and seasonal learning modules. This continuous refresh cycle helps maintain user interest and encourages recurring usage across academic terms.

For Instance, in June 2025, Quizizz rebranded to Wayground with online platform upgrades. New AI tools and curriculum-aligned bundles deliver interactive quizzes via browsers, simplifying lesson planning for teachers worldwide.

By Game Type

Location-based games representing 29.4% indicate rising interest in immersive learning experiences that blend physical movement with digital interaction. These games often encourage exploration, contextual problem-solving, and experiential learning.

This format is particularly relevant in subjects such as geography, environmental science, and cultural studies. By linking learning to real-world surroundings, engagement and retention can improve compared to traditional screen-only formats.

The expansion of mobile device penetration and improved geolocation accuracy further supports this segment. As mobile connectivity expands, location-based educational experiences are becoming more accessible and scalable.

For Instance, in February 2025, Kahoot! partnered with Sanrio for location-tied character games. Free mobile and online hunts foster collaboration using AR elements, blending virtual quests with real-world awareness for young learners.

By Application

Critical thinking and problem-solving leading at 41.8% demonstrates growing emphasis on skills that extend beyond memorization. Educational institutions increasingly prioritize analytical reasoning, logic, and decision-making abilities.

Game mechanics such as scenario-based challenges, timed puzzles, and strategy simulations are designed to develop these competencies. Such formats align well with modern curriculum reforms focused on cognitive development.

The value of these applications is also reinforced by workforce expectations. Employers increasingly demand adaptable and analytical skills, which strengthens institutional support for problem-solving-based educational games.

For Instance, in November 2025, Epic Games expanded Fortnite Creative for critical thinking lessons. UN Sustainable Development Goals maps challenge players to solve real-world problems through strategic builds and teamwork.

By End-user

Education institutions holding 24.9% confirms that schools and formal training centers remain primary adopters. Institutional procurement supports large-scale implementation across classrooms and grade levels. Structured integration into lesson plans increases repeat usage and sustained engagement.

Teachers often use educational games as reinforcement tools, assessment supplements, or interactive classroom activities. Institutional adoption also benefits from government-led digital learning initiatives. Funding support and policy alignment accelerate penetration of educational gaming solutions in public education systems.

For Instance, in September 2025, Duolingo, Inc. expanded its Chess course to Android with player-vs-player modes and advanced strategy lessons at Duocon. Integrated into school curricula, it sharpens tactics for students via competitive play. The update cements education’s lead by blending gaming with core skill-building in real classrooms.

Regional Analysis

North America at 43.5% reflects strong digital infrastructure, early adoption of edtech solutions, and higher institutional spending on digital learning tools. Schools and universities in the region frequently incorporate interactive platforms into standard curricula. High device penetration across households supports continued use beyond classrooms. Students often access educational games at home, extending engagement time and reinforcing learning outcomes.

For instance, in January 2022, Age of Learning’s My Math Academy met the highest level of evidence for improving learning outcomes, as announced by the Los Angeles-based EdTech company. This milestone underscored North America’s dominance in educational games, driven by advanced technological infrastructure, high digital adoption, and strong investments in gamified learning platforms.

The U.S. value of USD 6.76 Bn and 20.52% CAGR indicates sustained expansion within the country context provided. Growth is supported by integration of digital learning standards and emphasis on STEM education. Private investment in edtech innovation also strengthens domestic product availability. Continuous innovation in adaptive learning algorithms and gamified assessment tools supports steady demand growth.

For instance, in August 2025, Duolingo, the popular language-learning app giant, expanded into math education for kids, highlighting U.S. dominance in educational games. This Pittsburgh-based company launched elementary and middle school lessons aligned to Common Core standards, leveraging its massive user base and gamification expertise to compete with established players like Prodigy and Khan Academy Kids.

Emerging Trends Analysis

One significant trend in the Educational Games Market is the integration of adaptive learning engines within game environments. Platforms are increasingly using performance data to dynamically adjust difficulty levels, pacing, and content sequencing. This improves learner engagement and ensures that students remain challenged without feeling overwhelmed. As personalization becomes more refined, educational games are shifting from static content delivery to intelligent learning ecosystems.

Another emerging trend is the blending of immersive technologies with curriculum design. Location-based and simulation-driven formats are gaining relevance because they allow contextual and experiential learning. These approaches strengthen knowledge retention by linking theoretical instruction with interactive application. Increased mobile penetration and device accessibility further support this immersive expansion.

A parallel trend is institutional alignment with measurable outcomes. Educational buyers are placing greater emphasis on analytics dashboards, competency tracking, and skill benchmarking. This movement strengthens demand for platforms that can demonstrate academic impact rather than only entertainment value.

Growth Factors

A primary growth factor is the continued digital transformation of education systems. Schools and training institutions are expanding digital infrastructure, which enables smoother deployment of cloud-based educational games. As digital literacy increases among teachers and students, integration barriers decline and adoption becomes more sustainable.

Another growth driver is the increasing focus on skill-based learning. Educational frameworks are shifting toward competency development in critical thinking, collaboration, and analytical reasoning. Game-based learning aligns well with these objectives because it encourages problem-solving through structured challenges.

Home learning adoption also contributes to growth. Parents increasingly seek interactive educational tools that combine engagement with measurable progress. This demand supports subscription-based and online educational gaming platforms.

Key Market Segments

By Component

- Solution

- Services

By Deployment Mode

- Cloud

- On-premise

By Platform

- Offline

- Online

By Game Type

- Location-Based Games

- AR/VR Games

- AI-Based Games

- Language Learning

- Skill-Based Learning

- Simulation

- Others

By Application

- Critical Thinking & Problem-Solving

- Training & Development

- Evaluation

- Others

By End-user

- IT & Telecom

- Retail

- Consumer

- Manufacturing

- Government

- Education

- Healthcare & Life Sciences

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

The main driver in this market is the effectiveness of gamification in improving engagement levels. Traditional learning methods may struggle to maintain attention, especially among younger learners. Educational games introduce competition, rewards, and achievement systems that sustain interest over longer study periods.

Another important driver is accessibility through online and cloud platforms. With over half of platforms delivered online, educational games can be accessed from multiple devices without complex installation. This flexibility supports usage across classrooms, homes, and hybrid learning environments.

Institutional emphasis on measurable learning outcomes also drives adoption. When educational games provide assessment data and progress insights, they align more closely with curriculum standards and institutional accountability requirements.

For instance, in January 2025, Amazon Web Services rolled out eight interactive game-based training experiences, including escape rooms and AI simulations, to teach cloud skills in a hands-on way. This move taps into the growing need for engaging digital tools that make tech learning feel like play, drawing in managers and teams eager for fresh training methods. It shows how cloud giants are fueling demand by blending education with game fun.

Restraint

One restraint is uneven access to digital infrastructure across regions. While cloud and online platforms are expanding, not all institutions have stable connectivity or sufficient device availability. This digital divide can slow adoption in certain areas.

Another restraint is concerns related to screen time and digital dependency. Parents and educators may hesitate to expand usage if educational games are perceived as excessive digital exposure. This perception can limit daily usage duration and long-term engagement.

Content alignment challenges also act as a restraint. Educational institutions often require strict adherence to national or regional curriculum standards. If game content does not fully align with prescribed learning objectives, procurement decisions may be delayed.

For instance, in February 2025, Epic Games teamed up with UNC Greensboro for an Unreal Academic Partnership, picking it among 36 US schools. This gives students free access to Unreal Engine tools and training, easing the burden of pricey dev resources for educational projects. It shows how partnerships help offset steep costs in game building.

Opportunities

A major opportunity lies in expanding AI-driven personalization within educational games. Platforms that provide tailored learning pathways based on individual strengths and weaknesses can significantly improve learning outcomes. This capability enhances differentiation in a competitive landscape.

Another opportunity exists in expanding into corporate and professional training segments. Beyond schools, gamified learning tools can support employee skill development, compliance training, and leadership programs. This diversification reduces reliance on a single end-user group.

Emerging markets present additional opportunity due to rising digital adoption and growing investment in education technology. As internet penetration increases, cloud-based educational gaming solutions can scale efficiently with relatively low infrastructure requirements.

For instance, in September 2025, Duolingo launched its Chess course on Android with player-vs-player mode on iOS at Duocon. New features like mini-matches and advanced lessons adapt to skill levels, personalizing practice for better retention. This expands gamified learning into strategy games with tailored challenges.

Key Players Analysis

Competition in the Educational Games Market is influenced by infrastructure strength, content quality, and engagement design. Amazon Web Services, Inc. and Google LLC provide scalable cloud environments that support high-volume user interaction and analytics performance. Their technological ecosystems strengthen backend capabilities for educational game developers.

Content-driven platforms such as Duolingo, Inc., Kahoot! ASA, Age of Learning, Inc., and Quizizz, Inc. compete through curriculum alignment and user engagement depth. These companies emphasize adaptive features and recurring usage models that sustain learner retention and institutional contracts.

Game-focused developers including Mojang Studios, Epic Games, Filament Games, Breakaway Games, Lumos Labs, and Tangible Play, Inc. differentiate through immersive design and interactive storytelling. Their ability to combine entertainment-grade mechanics with structured educational objectives shapes competitive positioning in the evolving market landscape.

Top Key Players in the Market

- Amazon Web Services, Inc.

- Google LLC

- Duolingo, Inc.

- Mojang Studios

- Kahoot! ASA

- Epic Games

- Age of Learning, Inc.

- Breakaway Games

- Filament Games

- Lumos Labs

- Tangible Play, Inc.

- Quizizz, Inc.

- Others

Recent Developments

- In January 2025, Epic Games deepened Fortnite’s educational reach through Unreal Editor for Fortnite (UEFN) training with Duke University. Students now build interactive lessons in-game, gamifying subjects and blending development skills with real-world applications for engaging STEM learning.

- In December 2025, Google expanded education tools with AI literacy curricula in Be Internet Awesome and code-free AI Quests for middle schoolers. These game-based experiences simulate AI research lifecycles, reaching institutions worldwide via Google for Education.

Report Scope

Report Features Description Market Value (2025) USD 17.3 Bn Forecast Revenue (2035) USD 133.0 Bn CAGR(2026-2035) 22.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Solution, Services), By Deployment Mode (Cloud, On-premise), By Platform (Offline, Online), By Game Type (Location-Based Games, AR/VR Games, AI-Based Games, Language Learning, Skill-Based Learning, Simulation, Others), By Application (Critical Thinking & Problem-Solving, Training & Development, Evaluation, Others), By End-user (IT & Telecom, Retail, Consumer, Manufacturing, Government, Education, Healthcare & Life Sciences, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Amazon Web Services, Inc., Google LLC, Duolingo, Inc., Mojang Studios, Kahoot! ASA, Epic Games, Age of Learning, Inc., Breakaway Games, Filament Games, Lumos Labs, Tangible Play, Inc., Quizizz, Inc., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Amazon Web Services, Inc.

- Google LLC

- Duolingo, Inc.

- Mojang Studios

- Kahoot! ASA

- Epic Games

- Age of Learning, Inc.

- Breakaway Games

- Filament Games

- Lumos Labs

- Tangible Play, Inc.

- Quizizz, Inc.

- Others

Our Clients

- 179077

- Feb. 2026