Global Earth Observation Satellite Market Size, Share, Growth Analysis By Platform (Satellite-Based EO, UAV/Drone-Based EO, Ground-Based EO, Airborne EO), By Orbit Type (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO)), By Technology (Optical Imaging, Radar Imaging (Synthetic Aperture Radar), Thermal Imaging, LiDAR Technology), By Application (Environmental Monitoring, Disaster Management, Agriculture and Forestry, Urban Planning and Infrastructure, Maritime Surveillance, Energy and Power Sector, Climate Change Research), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182906

- Number of Pages: 254

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

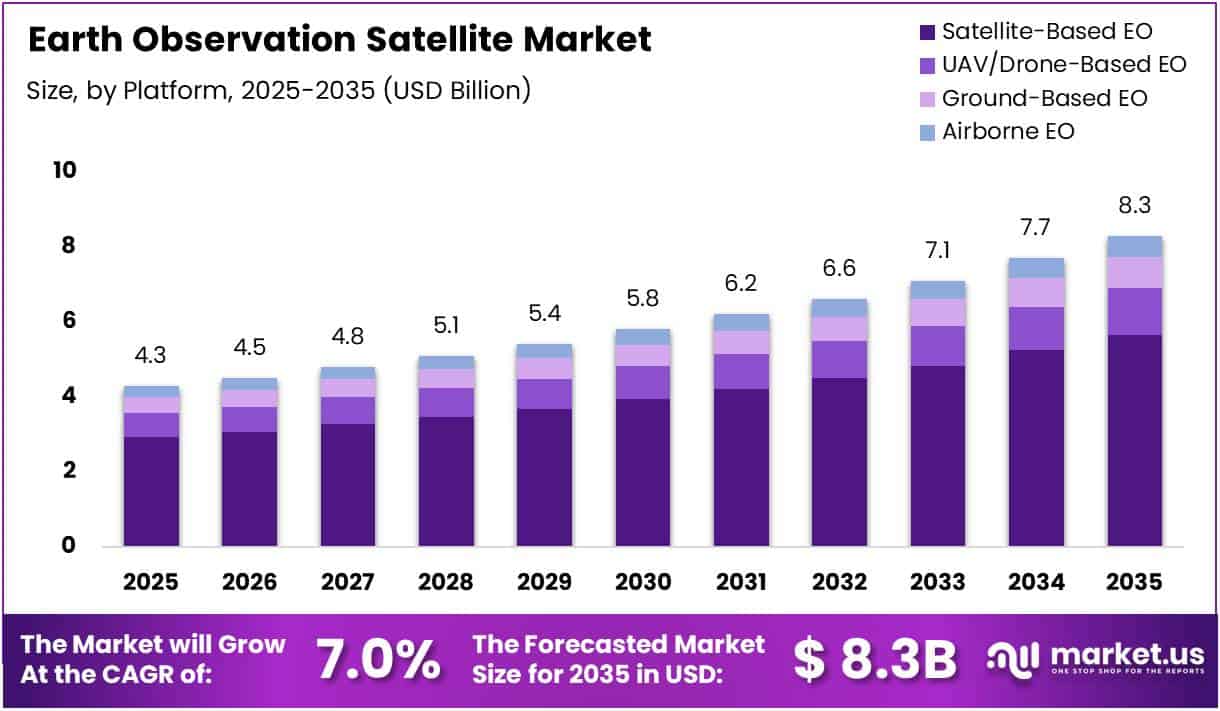

The Global Earth Observation Satellite Market size is expected to be worth around USD 8.3 Billion by 2035 from USD 4.3 Billion in 2025, growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

Earth Observation Satellites are spacecraft that orbit Earth to continuously collect data about the planet’s surface, atmosphere, and oceans. They use optical, radar, thermal, and LiDAR imaging technologies to capture high-resolution imagery. These satellites support a wide range of applications, from climate research and natural disaster response to national security and infrastructure management.

The market spans multiple platforms, including satellite-based, UAV/drone-based, airborne, and ground-based systems. Satellite-based Earth Observation remains the dominant platform, driven by growing LEO constellation deployments. Moreover, the availability of multiple orbit types — LEO, MEO, and GEO — enables diverse coverage needs and varying data refresh cycles for different use cases.

Government investments continue to be a key market driver globally. Agencies including NASA, ESA, and ISRO are actively expanding their EO satellite programs. Consequently, commercial opportunities are growing as governments partner with private firms for data collection, satellite manufacturing, analytics services, and constellation management.

Regulatory frameworks governing satellite licensing, data access, and orbital slot management are evolving across jurisdictions. However, these regulations also introduce compliance challenges for smaller market entrants and commercial operators. Therefore, companies are increasingly investing in regulatory expertise and international partnerships to navigate these complex frameworks effectively.

According to research published on arXiv, AI-based scheduling optimization has achieved a greater than 60% reduction in unusable or low-quality satellite images, while optimized satellite maneuvering has delivered up to a 78% reduction in energy waste. Additionally, advanced onboard processing has improved image resolution quality by approximately 10%, with up to an 83% reduction in monitoring frequency variance.

According to the ESA EO Framework, Earth observation satellites achieve spatial resolution ranging from approximately 5 meters to 40 meters depending on imaging mode, while satellite swath width can reach up to 400 km in a single pass. Moreover, revisit cycles improve to around 6 days with constellation-based systems, compared to approximately 12 days for single satellites.

Key Takeaways

- The Global Earth Observation Satellite Market was valued at USD 4.3 Billion in 2025 and is projected to reach USD 8.3 Billion by 2035.

- The market is growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

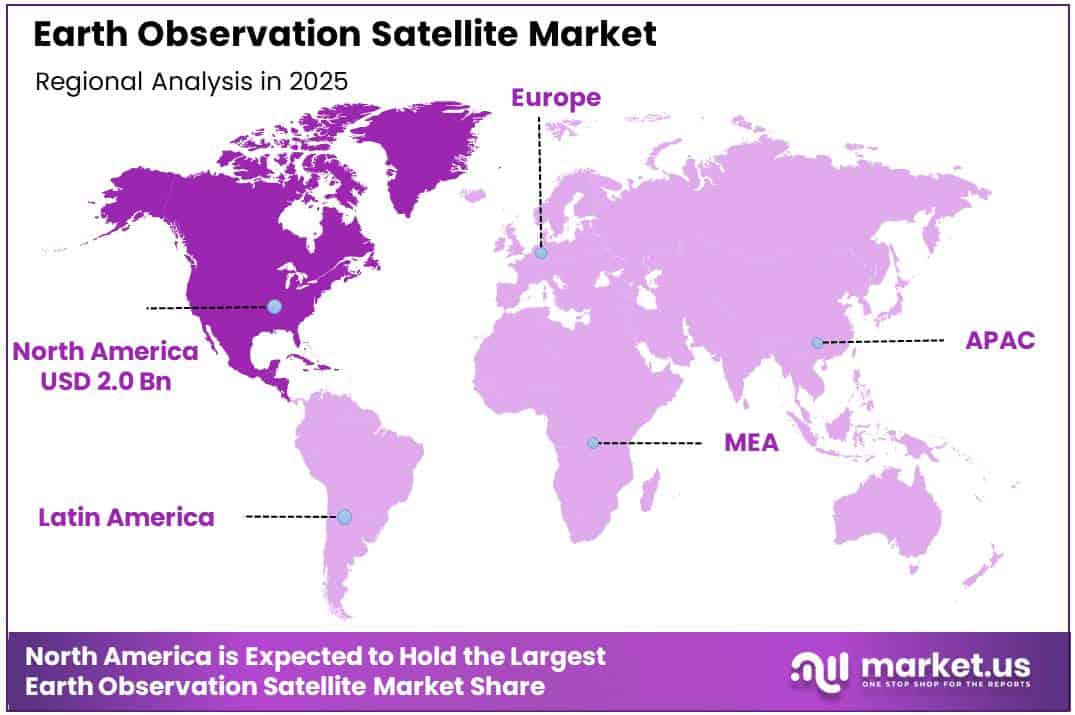

- North America dominated the global market with a 46.9% share, valued at USD 2.0 Billion in 2025.

- By Platform, Satellite-Based EO held the dominant position with a 67.8% market share in 2025.

- By Orbit Type, Low Earth Orbit (LEO) led the segment with a 78.2% share in 2025.

- By Technology, Optical Imaging accounted for the largest share at 51.7% in 2025.

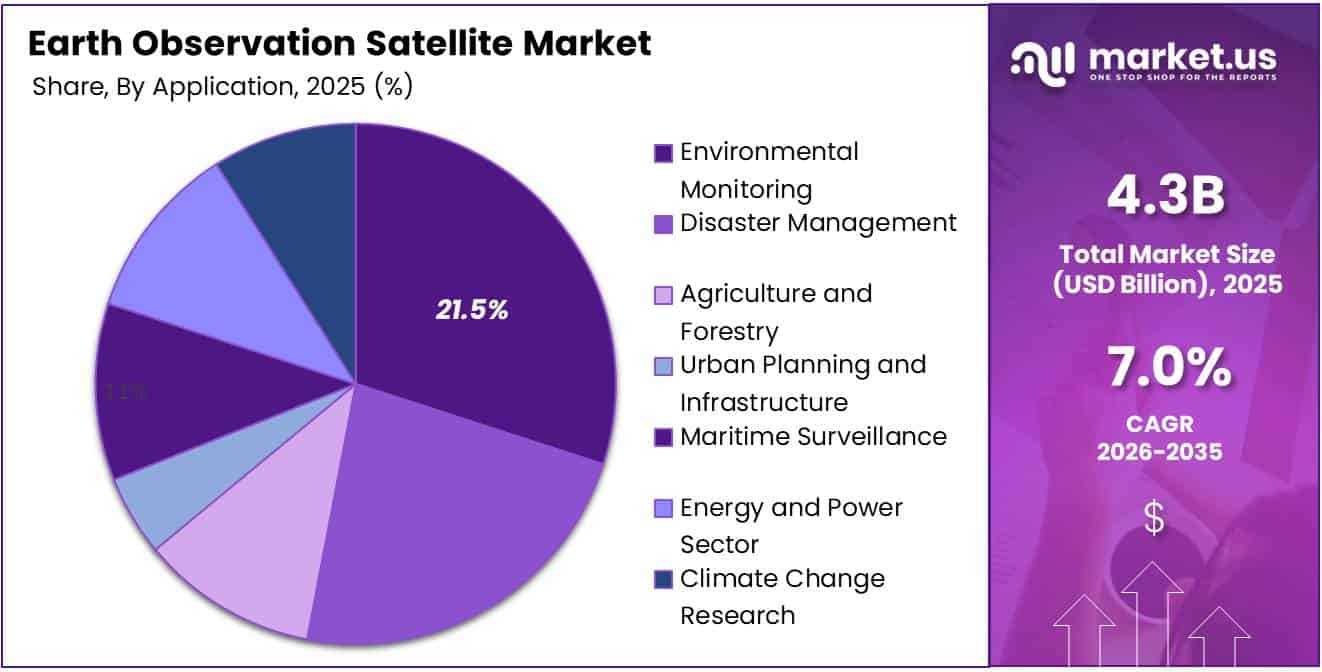

- By Application, Environmental Monitoring held the leading position with a 21.5% share in 2025.

By Platform Analysis

Satellite-Based EO dominates with 67.8% due to large-scale LEO constellation deployments and declining launch costs.

In 2025, Satellite-Based EO held a dominant market position in the By Platform segment of the Earth Observation Satellite Market, with a 67.8% share. This dominance is driven by large-scale LEO constellation deployments enabling continuous global coverage. Additionally, declining satellite launch costs have accelerated adoption across both commercial and government EO programs worldwide.

UAV/Drone-Based EO is the fastest-growing platform in this segment. Drones offer high-resolution localized imaging at significantly lower operational costs compared to traditional satellite systems. Consequently, they are increasingly deployed for precision agriculture, disaster response, and infrastructure inspection at regional and local levels.

Ground-Based EO systems complement satellite and aerial platforms by providing continuous, real-time data from fixed or mobile observation stations. These systems are widely used in meteorological monitoring, seismic observation, and border surveillance. Moreover, they serve as calibration references for satellite imagery, improving overall data accuracy.

Airborne EO platforms, including manned aircraft and high-altitude unmanned systems, provide flexible, on-demand imaging capabilities. They bridge the gap between wide-area satellite coverage and ground-level observation. Therefore, airborne EO is widely deployed for border monitoring, emergency management, and military reconnaissance with faster deployment timelines than satellites.

By Orbit Type Analysis

Low Earth Orbit (LEO) dominates with 78.2% due to lower altitudes enabling higher resolution imaging and reduced launch costs.

In 2025, Low Earth Orbit (LEO) held a dominant market position in the By Orbit Type segment of the Earth Observation Satellite Market, with a 78.2% share. LEO satellites operate at lower altitudes, enabling higher-resolution imaging and faster data transmission. Moreover, reduced launch costs have made LEO the preferred orbit for commercial EO constellations globally.

Medium Earth Orbit (MEO) satellites aoperate t altitudes between LEO and GEO, offering a balance between area coverage and imaging resolution. However, MEO hosts fewer dedicated Earth observation satellites compared to LEO. Consequently, MEO is primarily leveraged for navigation and communication systems, with limited but growing EO-specific applications.

Geostationary Orbit (GEO) satellites remain stationary relative to Earth’s surface, providing persistent coverage over fixed geographic areas. This makes GEO ideal for weather monitoring, climate observation, and large-scale environmental surveillance. Additionally, GEO platforms are widely used by meteorological agencies for continuous atmospheric data collection across broad regions.

By Technology Analysis

Optical Imaging dominates with 51.7% due to its wide deployment for land mapping, urban planning, and agricultural monitoring.

In 2025, Optical Imaging held a dominant market position in the By Technology segment of the Earth Observation Satellite Market, with a 51.7% share. Optical sensors capture high-resolution visible-light imagery for land mapping, urban planning, and agricultural monitoring. Therefore, optical imaging remains the most widely deployed EO technology across both commercial and government satellite programs.

Radar Imaging (Synthetic Aperture Radar) is a critical technology enabling all-weather, day-and-night Earth observation. Synthetic Aperture Radar penetrates cloud cover and operates regardless of lighting conditions. Consequently, it is widely used for maritime surveillance, disaster assessment, and environmental monitoring in regions with persistent cloud coverage or limited sunlight availability.

Thermal Imaging technology detects heat signatures from Earth’s surface, making it valuable for wildfire detection, energy efficiency assessments, and industrial facility monitoring. Moreover, thermal sensors are increasingly integrated into multi-payload satellites alongside optical and radar systems. This supports more comprehensive environmental analysis and infrastructure safety monitoring.

LiDAR Technology uses laser pulses to create precise three-dimensional maps of terrain, vegetation, and built environments. It is increasingly used for flood modeling, forestry management, and urban infrastructure planning. Additionally, advancements in miniaturized airborne and satellite-based LiDAR are expanding deployment across Earth observation missions globally.

By Application Analysis

Environmental Monitoring dominates with 21.5% due to growing global reliance on satellite data for policy decisions and compliance reporting.

In 2025, Environmental Monitoring held a dominant market position in the By Application segment of the Earth Observation Satellite Market, with a 21.5% share. EO satellites track land cover changes, deforestation, and water quality with high precision. Therefore, environmental agencies increasingly rely on satellite data for regulatory compliance and evidence-based policy decisions.

Disaster Management is a critical EO application, enabling rapid assessment of flood zones, earthquake damage, and wildfire spread. Satellite imagery provides emergency responders with timely, accurate situational awareness. Consequently, governments worldwide are integrating EO data into national disaster preparedness, early warning, and crisis response frameworks.

Agriculture and Forestry applications leverage EO satellite data to monitor crop health, soil conditions, and deforestation rates. Multispectral imaging enables precision agriculture practices, improving yield forecasting and resource management. Moreover, forestry agencies use satellite-derived data to track illegal logging and assess forest carbon stocks effectively.

Urban Planning and Infrastructure is a growing application segment supported by high-resolution optical and SAR imagery. City planners and infrastructure developers use EO data for land-use mapping, transportation planning, and construction monitoring. Additionally, satellite data supports smart city initiatives by providing updated spatial information for urban growth analysis.

Maritime Surveillance benefits from EO satellites through vessel tracking, illegal fishing detection, and port activity monitoring. SAR technology is especially effective for maritime applications as it operates in all weather conditions. Therefore, defense and coast guard agencies globally are increasingly adopting satellite-based maritime monitoring solutions.

Energy and Power Sector applications use EO satellite data to monitor pipelines, power lines, solar farms, and oil installations. Thermal and optical imagery helps detect equipment anomalies, leaks, and unauthorized activities. Consequently, energy companies are integrating satellite monitoring into their asset management and operational safety programs.

Climate Change Research is one of the fastest-growing EO application areas, supported by increasing global awareness of environmental risks. EO satellites monitor sea level rise, ice cap shrinkage, and atmospheric CO2 concentrations. Moreover, research institutions and climate agencies depend on long-term satellite data archives to model and predict future climate scenarios.

Key Market Segments

By Platform

- Satellite-Based EO

- UAV/Drone-Based EO

- Ground-Based EO

- Airborne EO

By Orbit Type

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

By Technology

- Optical Imaging

- Radar Imaging (Synthetic Aperture Radar)

- Thermal Imaging

- LiDAR Technology

By Application

- Environmental Monitoring

- Disaster Management

- Agriculture and Forestry

- Urban Planning and Infrastructure

- Maritime Surveillance

- Energy and Power Sector

- Climate Change Research

Drivers

Growing LEO Constellation Deployments and Multi-Technology Imaging Drive Earth Observation Satellite Market Growth

The rapid deployment of Low Earth Orbit satellite constellations is a primary driver of growth in the Earth Observation Satellite Market. LEO satellites offer near-continuous global coverage with shorter revisit cycles. Consequently, governments and commercial operators are accelerating constellation investments to meet rising demand for real-time geospatial intelligence across multiple sectors.

Growing reliance on Optical and SAR imaging technologies is further expanding market demand. These technologies enable multi-condition monitoring, operating effectively in all weather and lighting environments. Moreover, their combined use provides comprehensive Earth observation capabilities, supporting critical applications across defense, agriculture, environmental compliance, and infrastructure sectors globally.

The expanding use of EO data across environmental monitoring, agriculture, and maritime surveillance is creating sustained demand. Decision-makers across public and private sectors rely on satellite-derived insights for operational efficiency and risk management. Therefore, this broad cross-sector adoption continues to be a consistent long-term driver of market growth.

Restraints

Regulatory Complexities and Data Management Challenges Restrain Earth Observation Satellite Market Growth

Stringent regulatory and licensing frameworks governing Earth observation data access present significant barriers for market participants. Countries impose varying rules on data sharing, imagery resolution limits, and satellite orbital operations. Consequently, navigating these environments increases compliance costs and delays market entry for commercial and smaller-scale EO operators.

Data processing complexity remains a key restraint, as EO satellites generate massive volumes of raw imagery and sensor data daily. Managing, storing, and analyzing this data requires significant computational infrastructure and specialized technical expertise. However, many organizations lack the resources to process large-scale EO datasets effectively, limiting full utilization of satellite capabilities.

Additionally, large-volume data management limitations across distributed EO systems create bottlenecks in data delivery and analytics pipelines. Latency in processing and distributing satellite imagery reduces its operational value, especially in time-sensitive applications like disaster response. Therefore, investments in scalable data infrastructure remain essential to overcome this growing market restraint.

Growth Factors

Technological Advancements in LiDAR, Thermal Imaging, and Drone-Based EO Accelerate Market Expansion

Advancements in LiDAR and thermal imaging technologies are creating significant growth opportunities in the Earth Observation Satellite Market. These technologies enable precise terrain mapping, volcanic activity monitoring, and high-precision climate analysis. Consequently, research institutions and government agencies are increasing strategic investment in these emerging and complementary EO imaging capabilities.

The increasing adoption of UAV and drone-based EO platforms is expanding access to high-resolution localized data collection. Drones offer cost-effective, flexible deployment for precision agriculture, infrastructure inspection, and disaster mapping applications. Moreover, advancements in sensor miniaturization are making drone-based EO increasingly accessible to a broader range of commercial and government users.

The expanding role of EO data in climate change research and sustainability initiatives represents a strong long-term growth factor. Governments and international organizations rely on satellite data to track environmental targets and policy compliance. Therefore, growing demand for climate monitoring capabilities continues to drive strategic investment in EO satellite infrastructure globally.

Emerging Trends

Multi-Orbit Integration and Hybrid EO Platforms Reshape the Earth Observation Satellite Market Landscape

A rapid shift toward multi-orbit satellite integration — combining LEO, MEO, and GEO constellations — is emerging as a defining trend in the Earth Observation Satellite Market. This integration enhances data reliability through continuous coverage across latitudes and timescales. Moreover, operators benefit from improved revisit frequencies and built-in redundancy across multiple orbital layers.

The increasing combination of optical and radar imaging is enabling all-weather, day-and-night observation capabilities. Optical sensors excel under clear conditions, while SAR provides reliable data through clouds and darkness. Consequently, dual-sensor satellite configurations are becoming standard in next-generation EO missions, delivering more complete and dependable Earth surface coverage.

The emergence of hybrid EO platforms — integrating satellite, airborne, and ground-based systems — represents a transformative trend in the industry. These platforms combine the wide-area coverage of satellites with the high-resolution, on-demand capability of drones and aircraft. Additionally, ground-based sensors provide validation data, improving the overall accuracy and reliability of integrated EO datasets.

Regional Analysis

North America Dominates the Earth Observation Satellite Market with a Market Share of 46.9%, Valued at USD 2.0 Billion

North America holds the dominant position in the Earth Observation Satellite Market, with a 46.9% market share valued at USD 2.0 Billion in 2025. The United States drives this leadership through strong defense investments, NASA programs, and a growing commercial space ecosystem. Additionally, Canada strengthens the region’s position with contributions in Arctic surveillance and environmental satellite monitoring.

Europe Earth Observation Satellite Market Trends

Europe is a significant player in the Earth Observation Satellite Market, with ESA and national space agencies investing heavily in satellite programs. Countries including Germany, France, and Italy maintain active EO programs. Moreover, the European Union’s Copernicus initiative provides open-access EO data supporting environmental, agricultural, and security applications across the region.

Asia Pacific Earth Observation Satellite Market Trends

Asia Pacific is the fastest-growing region in the Earth Observation Satellite Market, driven by major national space program expansions. Countries including China, Japan, India, and South Korea are significantly increasing satellite investment. Furthermore, space agencies such as ISRO and JAXA are expanding EO constellations to support agriculture, disaster management, and national security applications.

Middle East and Africa Earth Observation Satellite Market Trends

The Middle East and Africa region is witnessing growing adoption of EO satellite technology, driven by demand for resource management and border security. Countries including the UAE, Saudi Arabia, and South Africa have launched or commissioned sovereign satellite programs. Additionally, partnerships with international space agencies are accelerating regional EO capability development.

Latin America Earth Observation Satellite Market Trends

Latin America represents a developing market for Earth observation satellites, with growing interest in agricultural monitoring, deforestation tracking, and natural disaster management applications. Brazil leads the region through its national space program and EO investments. Moreover, increasing government awareness of climate vulnerabilities is driving demand for satellite-based environmental monitoring across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Airbus is a global leader in Earth observation satellite manufacturing and space systems integration, with operations spanning multiple continents. The company’s Defence and Space division designs and builds advanced optical and radar EO satellites for commercial and government clients. Airbus plays a central role in European space programs, including long-term ESA partnerships for environmental, security, and scientific satellite missions.

Planet Labs PBC operates one of the world’s largest commercial Earth observation satellite constellations, providing daily global imaging of Earth’s landmass. The company specializes in high-cadence optical imagery delivered through cloud-based analytics platforms for near-real-time geospatial insights. Additionally, Planet Labs serves diverse customers across agriculture, defense, forestry, and financial analytics with flexible subscription-based data services.

Lockheed Martin Corporation is a major provider of advanced satellite systems for defense, intelligence, and civilian Earth observation applications. The company develops high-resolution imaging satellites and space-based reconnaissance systems primarily for U.S. government agencies, including the Department of Defense. Moreover, Lockheed Martin continues to integrate next-generation SAR and optical sensor technologies into sovereign EO satellite programs.

L3Harris Technologies, Inc. is a key player in the Earth observation satellite market, specializing in advanced electro-optical sensor systems, space-based intelligence payloads, and satellite communications. The company provides mission-critical systems for U.S. government civil and military EO satellite programs. Consequently, L3Harris has built a strong, long-standing presence in high-performance space reconnaissance and environmental monitoring systems.

Key Players

- AIRBUS

- Planet Labs PBC.

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Northrop Grumman

- ICEYE

- Thales

- SARsat Arabia

- ImageSat International NV

Recent Developments

- February 2026 – Algeria successfully launched the Alsat-3B Earth observation satellite from the Jiuquan Satellite Launch Centre in China, expanding the country’s sovereign space-based remote sensing and monitoring capabilities.

- January 2026 – The Swedish government committed SEK 1.3 billion (approximately €121 million) to purchase ten satellites, aiming to establish a sovereign intelligence, surveillance, and reconnaissance (ISR) system for national security purposes.

- January 2026 – India’s ISRO initiated its 2026 launch calendar with the PSLV C62 mission, deploying the EOS-N1 Earth observation satellite alongside 14 other payloads into orbit to strengthen India’s EO capabilities.

- December 2025 – ICEYE raised €150 million in a Series E funding round led by General Catalyst, with proceeds earmarked to expand the company’s SAR satellite constellation and broaden global coverage.

- December 2025 – Marble Imaging raised €5.3 million ahead of its planned 2026 satellite launch, with the funding aimed at scaling the company’s very high-resolution (VHR) Earth observation capabilities.

- July 2025 – ISRO and NASA successfully launched the NISAR satellite, a joint mission designed to map Earth’s minute surface features and continuously monitor environmental and geological changes globally.

- February 2025 – Japan’s SKY Perfect JSAT announced plans to invest approximately $230 million to build a low-Earth orbit satellite constellation, partnering with Planet Labs to leverage the Pelican satellite platform for EO data services.

Report Scope

Report Features Description Market Value (2025) USD 4.3 Billion Forecast Revenue (2035) USD 8.3 Billion CAGR (2026-2035) 7.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Platform (Satellite-Based EO, UAV/Drone-Based EO, Ground-Based EO, Airborne EO), By Orbit Type (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO)), By Technology (Optical Imaging, Radar Imaging (Synthetic Aperture Radar), Thermal Imaging, LiDAR Technology), By Application (Environmental Monitoring, Disaster Management, Agriculture and Forestry, Urban Planning and Infrastructure, Maritime Surveillance, Energy and Power Sector, Climate Change Research) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape AIRBUS, Planet Labs PBC., Lockheed Martin Corporation, L3Harris Technologies, Inc., Northrop Grumman, ICEYE, Thales, SARsat Arabia, ImageSat International NV Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Earth Observation Satellite MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Earth Observation Satellite MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- AIRBUS

- Planet Labs PBC.

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Northrop Grumman

- ICEYE

- Thales

- SARsat Arabia

- ImageSat International NV

Our Clients

- 182906

- March 2026