Quick Navigation

Report Overview

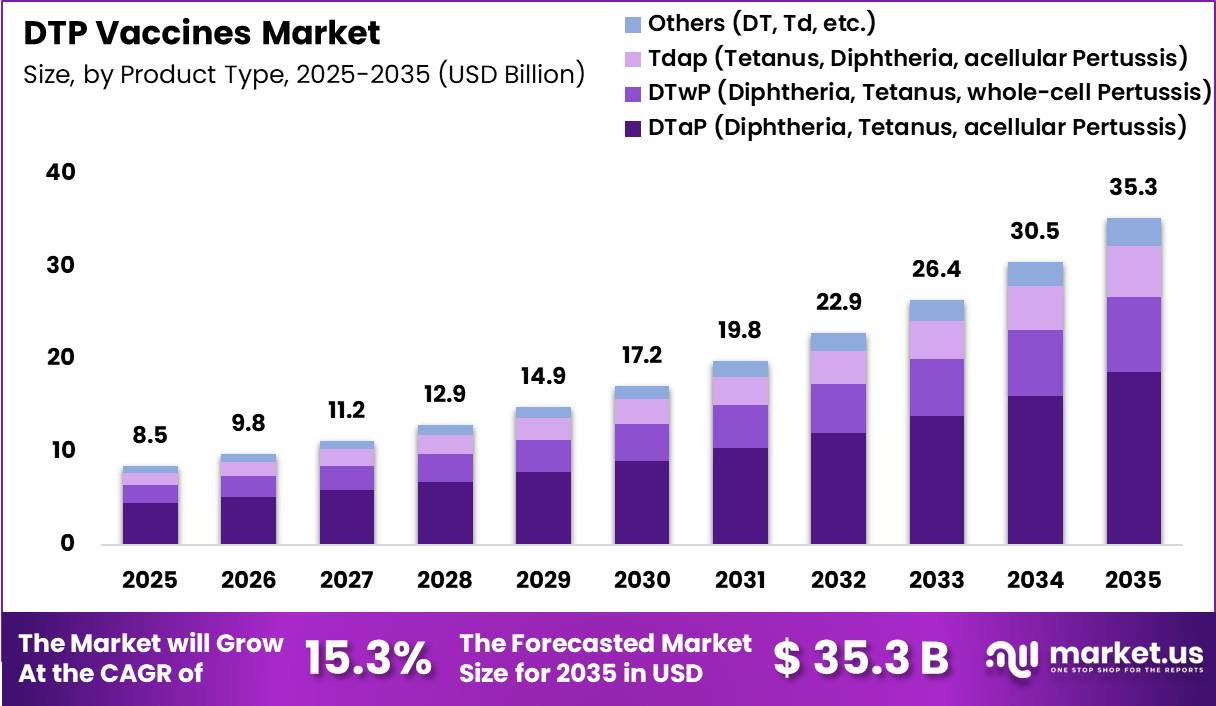

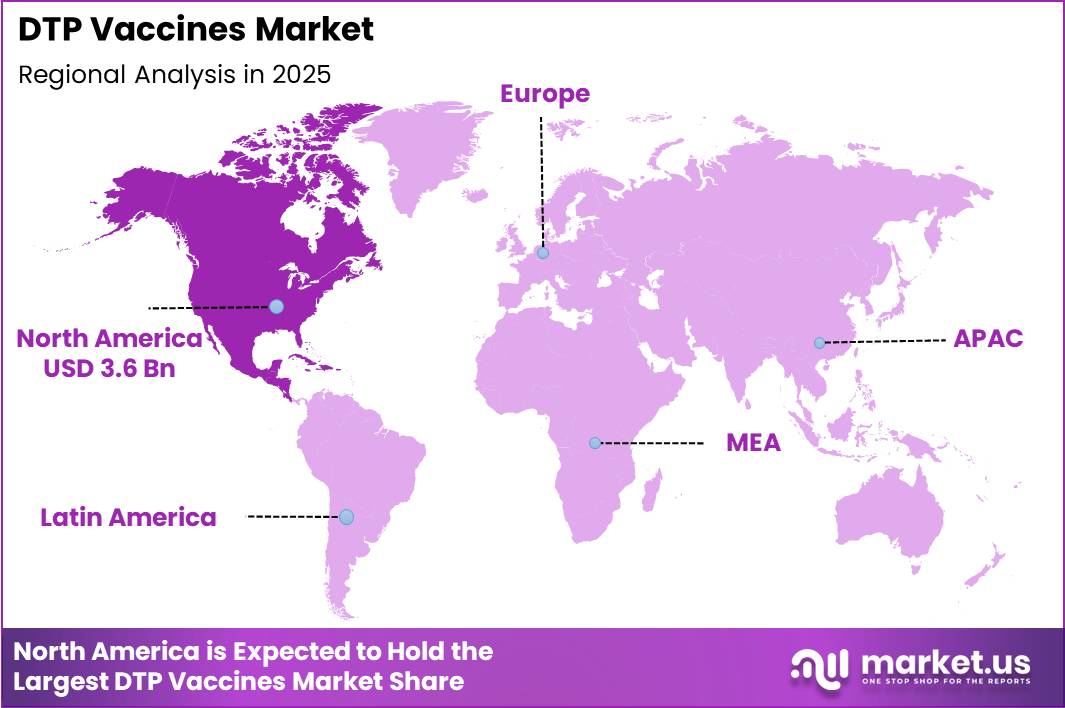

Global DTP Vaccines Market size is expected to be worth around US$ 35.3 Billion by 2035 from US$ 8.5 Billion in 2025, growing at a CAGR of 15.3% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 3.6 Billion.

The DTP vaccines market represents a critical segment of the global immunization landscape, driven by the continued need to prevent three serious infectious diseases: diphtheria, tetanus, and pertussis (whooping cough). DTP vaccines form the foundation of national childhood immunization schedules and are widely administered through routine vaccination programs supported by governments, public health agencies, and international organizations.

These vaccines are increasingly being incorporated into combination formulations, such as pentavalent and hexavalent vaccines, which provide protection against multiple diseases through a single injection, improving immunization efficiency and compliance.

The market is primarily supported by expanding immunization coverage worldwide and sustained investments in public health infrastructure. According to the World Health Organization (WHO), approximately 109 million infants globally received the third dose of a DTP-containing vaccine (DTP3) in 2024, representing 85% global coverage.

In addition, around 115 million infants received at least one dose of a DTP-containing vaccine, reflecting continued recovery and strengthening of routine immunization programs following disruptions caused by the COVID-19 pandemic. WHO and UNICEF also reported that DTP3 coverage remains a key indicator of national immunization system performance, with 111 countries achieving at least 90% coverage in 2024.

Growing efforts by organizations such as the World Health Organization, United Nations Children’s Fund, Gavi, the Vaccine Alliance, and national immunization programs are improving vaccine accessibility, particularly in low- and middle-income countries. These initiatives are aimed at reducing the burden of vaccine-preventable diseases, which continue to cause significant morbidity and mortality among infants and young children. WHO estimates indicate that immunization prevents approximately 4.4 million deaths annually worldwide, highlighting the critical role of vaccines in global public health.

Furthermore, technological advancements in vaccine development, including acellular pertussis formulations and combination vaccines, are enhancing vaccine safety, efficacy, and convenience. As governments continue to prioritize childhood immunization and disease prevention strategies, demand for DTP vaccines is expected to remain strong, supported by rising awareness, improved healthcare access, and ongoing efforts to expand routine vaccination coverage across both developed and emerging economies.

Key Takeaways

- Market Size: Global DTP Vaccines Market size is expected to be worth around US$ 35.3 Billion by 2035 from US$ 8.5 Billion in 2025.

- Market Share: The market growing at a CAGR of 15.3% during the forecast period from 2026 to 2035.

- By Product Type Analysis: The DTaP segment dominated the market with a 52.7% share in 2025.

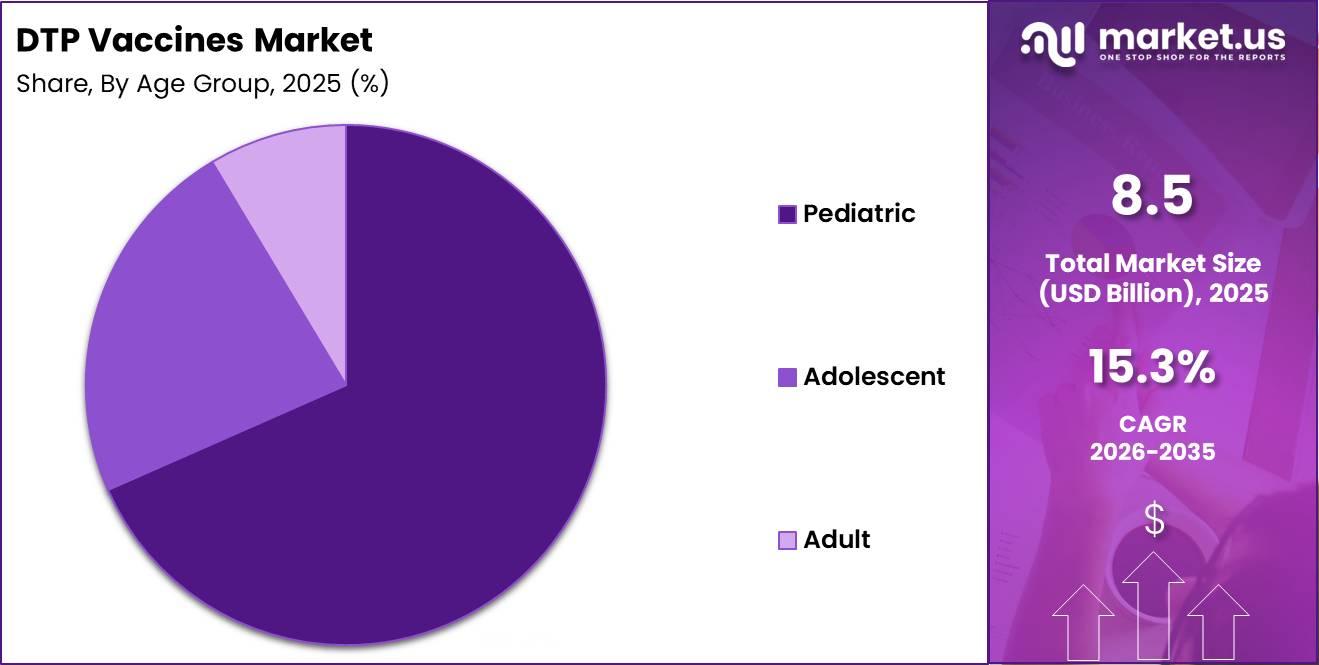

- By Age Group Analysis: The Pediatric segment accounted for the largest market share of 68.4% in 2025.

- By End User Analysis: Hospitals held the largest market share of 42.8% in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 3.6 Billion.

By Product Type Analysis

The DTP vaccines market is segmented by product type into DTaP (Diphtheria, Tetanus, acellular Pertussis), DTwP (Diphtheria, Tetanus, whole-cell Pertussis), Tdap (Tetanus, Diphtheria, acellular Pertussis), and Others (DT, Td, and related formulations). Among these, the DTaP segment dominated the market with a 52.7% share in 2025, supported by its favorable safety profile, lower incidence of adverse reactions, and widespread inclusion in national pediatric immunization schedules. The increasing preference for acellular pertussis vaccines in developed healthcare systems has further strengthened demand for DTaP products.

The DTwP segment continues to maintain a significant presence, particularly in low- and middle-income countries where cost-effectiveness and large-scale government immunization programs remain critical considerations. These vaccines are extensively utilized through public health initiatives due to their affordability and proven efficacy.

The Tdap segment is experiencing steady growth owing to increasing booster vaccination recommendations for adolescents, adults, healthcare workers, and pregnant women. Rising awareness regarding pertussis prevention across all age groups is supporting segment expansion.

The Others segment, comprising DT and Td vaccines, contributes to market growth through booster immunization programs and targeted protection against diphtheria and tetanus, particularly among adult populations and high-risk groups.

By Age Group Analysis

Based on age group, the DTP vaccines market is categorized into Pediatric, Adolescent, and Adult segments. The Pediatric segment accounted for the largest market share of 68.4% in 2025, driven by mandatory childhood immunization programs implemented across numerous countries. Strong government support, high birth rates in emerging economies, and recommendations from global health organizations have ensured consistent demand for DTP vaccines among infants and young children. Routine vaccination schedules requiring multiple doses during early childhood continue to make this segment the primary revenue contributor.

The Adolescent segment represents an important growth area, supported by increasing recommendations for booster doses to maintain immunity against diphtheria, tetanus, and pertussis. Educational campaigns, school-based vaccination programs, and growing awareness of pertussis outbreaks have contributed to higher vaccination coverage among teenagers.

The Adult segment is witnessing gradual expansion due to rising awareness regarding lifelong immunization and the need for booster vaccinations. Increasing vaccination among healthcare professionals, travelers, elderly populations, and pregnant women is driving segment growth.

Furthermore, public health initiatives promoting adult immunization and the prevention of vaccine-preventable diseases are expected to support sustained demand throughout the forecast period. The growing focus on comprehensive immunization strategies across all age groups continues to create opportunities within the adolescent and adult vaccine segments.

By End User Analysis

The DTP vaccines market is segmented by end user into Hospitals, Clinics and Vaccination Centers, Community Health Centers, and Others. Hospitals held the largest market share of 42.8% in 2025, primarily due to their role as major immunization providers for newborns, children, pregnant women, and adult patients.

Hospitals benefit from advanced cold-chain infrastructure, trained healthcare personnel, and comprehensive vaccination services, making them key distribution and administration points for DTP vaccines. The increasing number of institutional births and routine pediatric visits further supports the dominance of this segment.

The Clinics and Vaccination Centers segment represents a substantial portion of the market, driven by growing accessibility to preventive healthcare services and the expansion of private vaccination networks. These facilities offer convenient vaccination schedules, shorter waiting times, and specialized immunization services, encouraging greater patient participation.

The Community Health Centers segment plays a critical role in expanding vaccine coverage, particularly in rural and underserved regions. Government-supported immunization campaigns and public health outreach programs rely heavily on these centers to improve vaccination rates and reduce disease burden among vulnerable populations.

The Others segment, including pharmacies, mobile vaccination units, and public health agencies, contributes to market growth by increasing vaccine accessibility and supporting mass immunization initiatives. Continued investments in healthcare infrastructure and vaccination awareness programs are expected to strengthen demand across all end-user categories.

Key Market Segments

By Product Type

- DTaP (Diphtheria, Tetanus, acellular Pertussis)

- DTwP (Diphtheria, Tetanus, whole-cell Pertussis)

- Tdap (Tetanus, Diphtheria, acellular Pertussis)

- Others (DT, Td, etc.)

By Age Group

- Pediatric

- Adolescent

- Adult

By End User

- Hospitals

- Clinics and Vaccination Centers

- Community Health Centers

- Others

Driving Factors

Expansion of National Immunization Programs and Rising Vaccination Coverage

The growth of the DTP (Diphtheria, Tetanus, and Pertussis) vaccines market is primarily driven by the continued expansion of national immunization programs and increasing government investments in childhood vaccination initiatives.

DTP vaccines are included in the routine immunization schedules of nearly all countries and are strongly recommended by the World Health Organization (WHO) for protecting infants against three potentially fatal infectious diseases. As governments focus on reducing under-five mortality rates and strengthening primary healthcare systems, demand for DTP vaccines continues to increase.

According to WHO and UNICEF estimates, approximately 115 million infants worldwide received at least one dose of a DTP-containing vaccine in 2024, representing 89% global coverage. Additionally, around 109 million children completed the three-dose DTP vaccination schedule (DTP3), equivalent to 85% global coverage. These figures demonstrate the extensive adoption of DTP vaccines across national healthcare systems.

Many low- and middle-income countries are expanding vaccine access through government-funded immunization campaigns and support from international organizations. WHO identifies DTP3 coverage as a key indicator of healthcare system performance and immunization program effectiveness. The increasing emphasis on universal immunization, disease prevention, and public health preparedness is expected to sustain demand for DTP vaccines globally.

Trending Factors

Increasing Adoption of Combination and Acellular DTP Vaccines

A significant trend shaping the DTP vaccines market is the growing adoption of combination vaccines and acellular pertussis formulations. Healthcare authorities increasingly prefer combination vaccines that integrate DTP with protection against additional diseases such as hepatitis B, polio, and Haemophilus influenzae type b (Hib). These products reduce the number of injections required, improve compliance with immunization schedules, and simplify vaccine logistics for healthcare providers.

Another notable trend is the gradual shift from whole-cell pertussis vaccines to acellular pertussis vaccines in many developed healthcare systems. Acellular formulations are associated with lower reactogenicity and fewer post-vaccination adverse events, contributing to higher acceptance among parents and healthcare professionals. Continuous advancements in vaccine formulation technologies are further supporting product innovation within the market.

Additionally, the increasing integration of DTP antigens into multivalent pediatric vaccines is improving operational efficiency and supporting broader disease prevention strategies across national immunization programs.

Restraining Factors

Vaccine Hesitancy and Immunization Access Gaps

Despite strong public health support, the DTP vaccines market faces challenges from vaccine hesitancy and persistent immunization access gaps in several regions. Misinformation regarding vaccine safety, concerns about adverse reactions, and declining trust in healthcare systems have affected vaccination uptake in certain populations. These factors can reduce immunization coverage and create barriers to achieving universal vaccine access.

Approximately 14.3 million infants did not receive even a first dose of a DTP-containing vaccine, while an additional 5.6 million children were only partially vaccinated. Geopolitical instability, humanitarian crises, supply-chain disruptions, and shortages of trained healthcare personnel further contribute to uneven vaccine coverage.

Countries affected by conflict and fragility account for a disproportionately large share of unvaccinated children globally. Addressing vaccine hesitancy through public awareness campaigns and strengthening healthcare delivery systems remain critical requirements for sustaining long-term market growth.

Opportunity

Focus on Zero-Dose Children and Immunization Recovery Programs

A major opportunity for the DTP vaccines market lies in reaching zero-dose and under-vaccinated children through targeted immunization recovery programs. International health organizations, governments, and vaccine alliances are increasingly prioritizing the identification and vaccination of children who have never received routine immunizations. These initiatives create substantial demand for DTP vaccines because DTP coverage is widely used as a benchmark for measuring immunization system performance.

Achieving the Immunization Agenda 2030 goal of at least 90% global DTP coverage will require expanded vaccination campaigns, healthcare infrastructure investments, digital immunization registries, and community-based outreach initiatives.

South Asia has demonstrated notable progress, with regional DTP3 coverage increasing from 90% in 2023 to 92% in 2024. India improved DTP3 coverage from 91% to 94% during the same period, highlighting the effectiveness of strengthened immunization efforts.

As governments and international agencies continue to close immunization gaps and improve access among underserved populations, significant growth opportunities are expected to emerge for DTP vaccine manufacturers over the coming years.

Regional Analysis

North America dominated the global DTP (Diphtheria, Tetanus, and Pertussis) Vaccines Market in 2025, accounting for more than 42.5% of the total market share and generating revenue of approximately US$ 3.6 billion. The region’s leadership can be attributed to its well-established immunization infrastructure, high vaccination coverage rates, and strong government support for pediatric vaccination programs. The presence of leading vaccine manufacturers, advanced healthcare facilities, and favorable reimbursement policies further supports market expansion across the United States and Canada.

Europe represented the second-largest regional market, driven by comprehensive national immunization schedules, increasing awareness regarding vaccine-preventable diseases, and strong public healthcare systems. Consistent investments in vaccine research and development continue to support regional growth.

The Asia Pacific region is expected to witness the fastest growth during the forecast period. Rising birth rates in several developing countries, expanding healthcare access, growing government immunization initiatives, and increasing healthcare expenditure are contributing to market development. Countries such as China and India are actively strengthening vaccination programs to improve public health outcomes.

Latin America, the Middle East, and Africa are also experiencing gradual market growth, supported by expanding vaccination campaigns, international health organization initiatives, and improving healthcare infrastructure. However, challenges related to vaccine accessibility and healthcare disparities continue to influence market penetration in certain areas.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The DTP (Diphtheria, Tetanus, and Pertussis) vaccines market is characterized by the presence of several multinational pharmaceutical companies that compete through product innovation, extensive distribution networks, and strategic partnerships with governments and international health organizations. Key players such as GSK, Sanofi, Merck & Co., Pfizer, and Serum Institute of India maintain strong market positions through broad vaccine portfolios and continuous investments in research and development.

These companies focus on improving vaccine efficacy, safety profiles, and combination vaccine formulations to enhance immunization coverage and patient compliance. Emerging manufacturers from developing economies are also strengthening their presence by offering cost-effective vaccines, increasing competition in price-sensitive markets.

Additionally, collaborations with organizations such as World Health Organization and UNICEF support large-scale vaccination programs, creating opportunities for market expansion. Continuous innovation, production capacity enhancement, and global supply chain optimization remain key competitive strategies among leading market participants.

Market Key Players

- Sanofi Pasteur

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Pfizer Inc.

- Astellas Pharma Inc.

- Serum Institute of India Pvt. Ltd.

- Biological E. Limited

- Bharat Biotech International Limited

- Panacea Biotec Ltd.

- Novartis AG

- Johnson & Johnson

- Mitsubishi Tanabe Pharma Corporation

- Daiichi Sankyo Company Limited

- Emergent BioSolutions Inc.

- CSL Limited

- Others

Recent Developments

- Bharat Biotech International Limited & GSK (June 2025): Bharat Biotech entered into a licensing agreement with GSK for the development and commercialization of the investigational Shigella vaccine candidate altSonflex1-2-3. Under the agreement, Bharat Biotech will lead Phase III development, regulatory activities, and large-scale manufacturing, while GSK will continue to provide technical and strategic support. The partnership reflects the growing trend toward collaborative vaccine development among major global vaccine manufacturers.

- Sanofi Pasteur (July 2025): Sanofi entered into a definitive agreement to acquire Vicebio for approximately USD 1.15 billion, with additional milestone payments of up to USD 450 million. The acquisition adds advanced vaccine platform technologies and combination vaccine development expertise, reinforcing Sanofi’s position in next-generation vaccine innovation and supporting its broader pediatric vaccine strategy.

- GlaxoSmithKline plc (GSK) (August 2025): GSK received an upfront settlement payment of USD 370 million through the resolution of mRNA-related intellectual property litigation involving CureVac and BioNTech. The agreement also provides GSK with future royalty income from selected mRNA vaccine products, strengthening the company’s vaccine R&D and commercialization capabilities.

- Serum Institute of India Pvt. Ltd.(October 2025): The Serum Institute of India expanded its vaccine development activities through a new partnership with the Coalition for Epidemic Preparedness Innovations (CEPI). The collaboration, supported by funding of up to USD 16.4 million, focuses on developing innovative vaccine platforms for emerging infectious diseases and further strengthens the company’s global vaccine manufacturing and research footprint.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 8.5 Billion |

| Forecast Revenue (2035) | US$ 35.3 Billion |

| CAGR (2026-2035) | 15.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type(DTaP (Diphtheria, Tetanus, acellular Pertussis), DTwP (Diphtheria, Tetanus, whole-cell Pertussis), Tdap (Tetanus, Diphtheria, acellular Pertussis), Others (DT, Td, etc.)) By Age Group (Pediatric, Adolescent, Adult) By End User( Hospitals, Clinics and Vaccination Centers, Community Health Centers, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Sanofi Pasteur, GlaxoSmithKline plc, Merck & Co., Inc., Pfizer Inc., Astellas Pharma Inc., Serum Institute of India Pvt. Ltd., Biological E. Limited, Bharat Biotech International Limited, Panacea Biotec Ltd., Novartis AG, Johnson & Johnson, Mitsubishi Tanabe Pharma Corporation, Daiichi Sankyo Company Limited, Emergent BioSolutions Inc., CSL Limited, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |