Global Drinkable Yogurt Market Size, Share, Report Analysis By Category (Dairy-based Yogurt, Non-dairy Based Yogurt), By Flavor (Flavored, Plain), By Sales Channel (Supermarkets/Hypermarkets, Departmental Stores, Convenience Store, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156536

- Number of Pages: 359

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

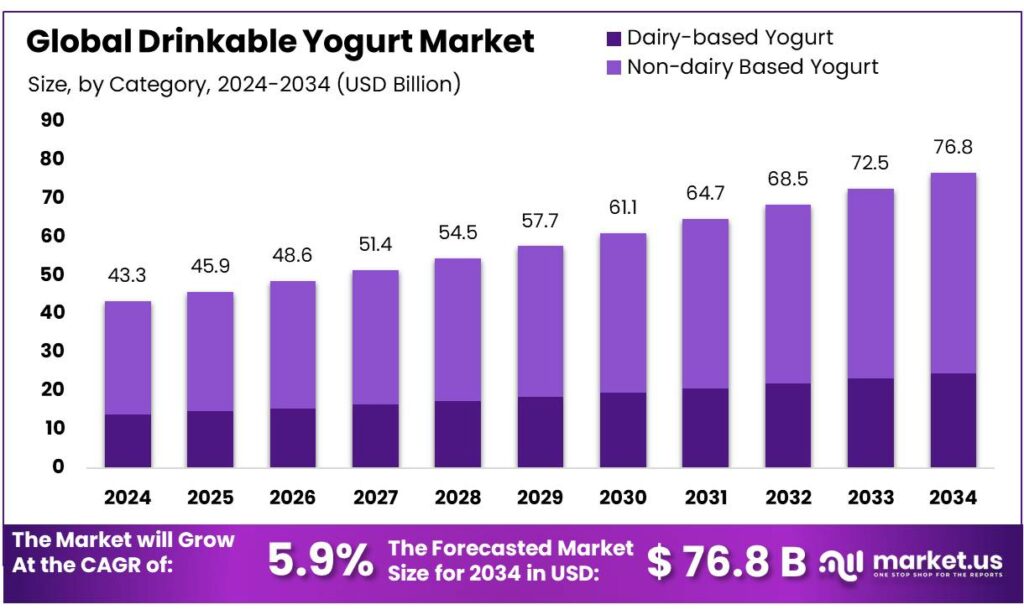

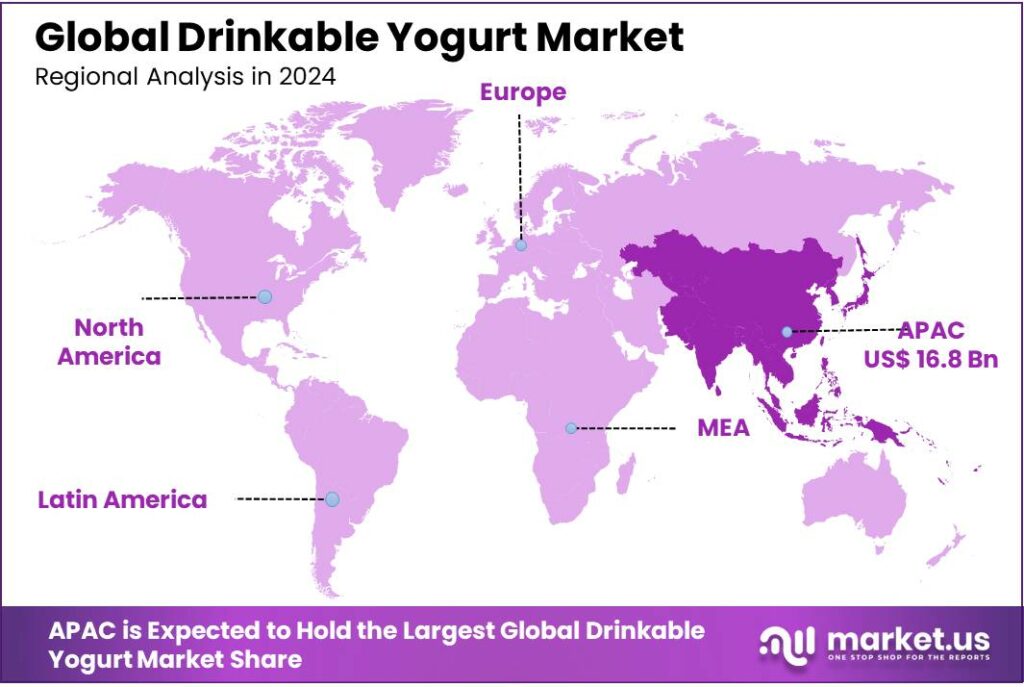

The Global Drinkable Yogurt Market size is expected to be worth around USD 76.8 Billion by 2034, from USD 43.3 Billion in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034. In 2024, Asia‑Pacific held a dominant market position, capturing more than a 38.9% share, holding USD 16.8 Billion revenue.

The drinkable yogurt segment in India is experiencing significant growth, driven by evolving consumer preferences towards health-conscious and convenient food options. This segment encompasses a variety of products, including probiotic drinks, flavored yogurts, and traditional beverages like lassi and buttermilk. The market’s expansion is underpinned by India’s robust dairy industry, which is the largest globally, accounting for 24% of the world’s milk production and supporting over 80 million farmers.

Government initiatives such as the National Dairy Plan (NDP) and the Dairy Processing and Infrastructure Development Fund (DIDF) have been instrumental in enhancing dairy infrastructure and promoting value-added products like drinkable yogurt. For instance, the Tamil Nadu government, under the DIDF, is constructing a plant in Srivilliputhur with a capacity of 10,000 liters per day to produce yogurt and other probiotic products.

Additionally, the Dairy Entrepreneurship Development Scheme (DEDS) provides financial support to individuals and groups establishing dairy ventures, facilitating the expansion of dairy infrastructure . The Animal Husbandry Infrastructure Development Fund (AHIDF), with an allocation of ₹15,000 crore, further bolsters investment in dairy processing and chilling infrastructure.

Key Takeaways

- Drinkable Yogurt Market size is expected to be worth around USD 76.8 Billion by 2034, from USD 43.3 Billion in 2024, growing at a CAGR of 5.9%

- Dairy-based Yogurt held a dominant market position, capturing more than an 82.9% share of the global drinkable yogurt market.

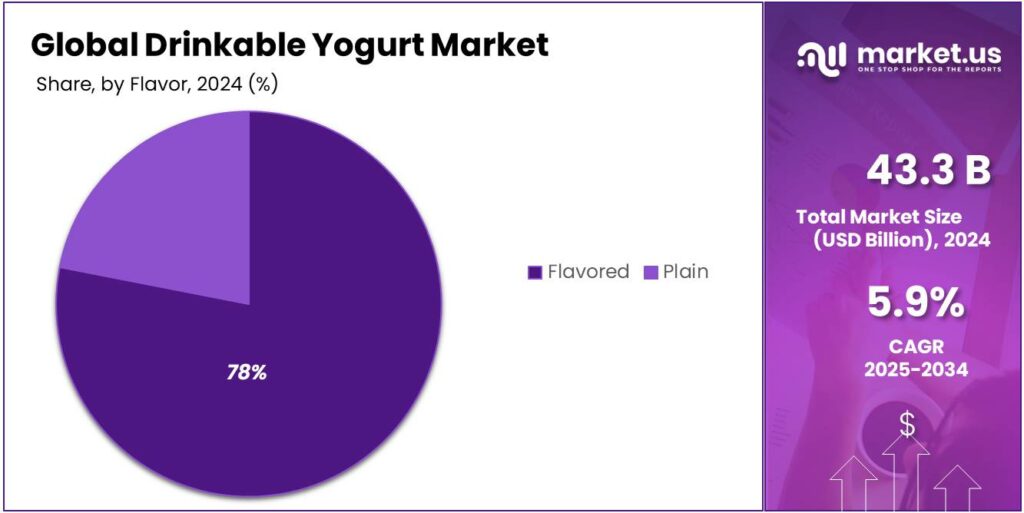

- Flavored held a dominant market position, capturing more than a 78.3% share in the global drinkable yogurt market.

- Supermarkets & Hypermarkets held a dominant market position, capturing more than a 49.6% share in the global drinkable yogurt market.

- Asia‑Pacific region held a commanding 38.9% share—equating to around USD 16.8 billion—of the global drinkable yogurt market.

By Category Analysis

Dairy-Based Yogurt Dominates with 82.9% Share in 2024 Thanks to Its Familiar Taste and Nutrition

In 2024, Dairy-based Yogurt held a dominant market position, capturing more than an 82.9% share of the global drinkable yogurt market. This overwhelming lead is largely due to its long-standing popularity, rich taste, and high protein content, which continue to resonate strongly with consumers. People trust dairy-based yogurt for its proven nutritional benefits, especially for gut health and calcium intake. Its creamy texture and natural flavor also make it more appealing for a wide range of age groups, from children to the elderly.

The segment benefits from the constant innovation seen in dairy-based drinkables—such as probiotic blends, added vitamins, and regional fruit infusions—that keep traditional dairy fresh and exciting in supermarkets. In 2025, the dairy-based category is expected to maintain its top spot as more consumers lean toward functional beverages that offer both taste and wellness. Despite the growth of plant-based alternatives, dairy-based drinkable yogurt continues to dominate due to its affordability, wide availability, and strong presence in both developed and emerging markets.

By Flavor Analysis

Flavored Drinkable Yogurt Rules 2024 with 78.3% Share Thanks to Taste Variety and Mass Appeal

In 2024, Flavored held a dominant market position, capturing more than a 78.3% share in the global drinkable yogurt market. This strong lead is clearly fueled by consumer preference for exciting taste profiles like strawberry, mango, blueberry, and mixed fruit blends, which make drinkable yogurt feel more like a treat than just a health food. Flavored options appeal to a broader demographic, especially children and young adults, who tend to reach for taste-first choices in their snack and breakfast routines.

The flavored segment has also benefited from manufacturers’ constant innovation—introducing seasonal flavors, low-sugar options, and even exotic combinations that keep the category fresh and engaging. These innovations have helped build loyalty among health-conscious consumers looking for nutritious drinks without compromising on taste.

By Sales Channel Analysis

Supermarkets & Hypermarkets Lead with 49.6% Share in 2024 Thanks to Wide Shelf Space and Easy Accessibility

In 2024, Supermarkets & Hypermarkets held a dominant market position, capturing more than a 49.6% share in the global drinkable yogurt market. These retail giants continue to be the most preferred sales channel because of their extensive shelf space, wide product variety, and ability to showcase multiple brands and flavors under one roof. Shoppers appreciate the convenience of picking up drinkable yogurt during their regular grocery runs, often drawn to in-store promotions, discounts, and combo offers that aren’t always available elsewhere.

The dominance of this segment is also driven by the visibility and reach these stores offer. Brands invest heavily in in-store marketing strategies, including attractive displays and free sampling, which boost impulse buying among customers. As health-focused beverages gain popularity, supermarkets and hypermarkets remain the key destination where consumers can physically compare nutrition labels, flavors, and prices before buying.

Key Market Segments

By Category

- Dairy-based Yogurt

- Non-dairy Based Yogurt

By Flavor

- Flavored

- Plain

By Sales Channel

- Supermarkets/Hypermarkets

- Departmental Stores

- Convenience Store

- Others

Emerging Trends

Government Initiatives and Support for the Drinkable Yogurt Industry

A pivotal factor contributing to this expansion is the Indian government’s strategic initiatives aimed at enhancing the dairy sector’s infrastructure and productivity. The National Dairy Plan (NDP), launched by the National Dairy Development Board (NDDB), focuses on increasing milk production and improving the livelihoods of rural farmers. This initiative is complemented by the Rashtriya Gokul Mission, which aims to conserve and develop indigenous bovine breeds, thereby improving milk yield and quality.

Moreover, the Dairy Entrepreneurship Development Scheme (DEDS) provides financial assistance to individuals and groups for setting up dairy units, including those producing value-added products like drinkable yogurt. Under this scheme, farmers from general categories receive a 25% capital subsidy, while those from Scheduled Castes and Scheduled Tribes are eligible for a 33% subsidy, fostering inclusive growth in the dairy sector.

The government’s commitment to enhancing dairy infrastructure is further evidenced by the establishment of the Animal Husbandry Infrastructure Development Fund (AHIDF), with an allocation of INR 15,000 crore. This fund supports the development of dairy processing units, including those focusing on probiotic-rich products like drinkable yogurt, thereby improving product availability and quality across the country.

These initiatives not only bolster the production capabilities of the dairy sector but also align with the evolving consumer preferences for health-oriented products. The increasing awareness about the health benefits of probiotics and the convenience offered by drinkable yogurt are pivotal in driving its popularity among consumers. As the government continues to invest in dairy infrastructure and support for farmers, the drinkable yogurt industry is poised for sustained growth, contributing to the overall development of the Indian dairy sector.

Drivers

Rising Health Consciousness and Demand for Functional Foods

One of the most significant drivers of the drinkable yogurt market in India is the increasing health consciousness among consumers. As lifestyles become more sedentary and health issues like digestive disorders and lifestyle diseases rise, individuals are actively seeking nutritious and convenient food options. Drinkable yogurt, rich in probiotics, offers a practical solution by promoting gut health, enhancing immunity, and aiding digestion. This shift towards health-focused dietary choices is reflected in the growing preference for functional foods and beverages.

According to a report by Agriculture and Agri-Food Canada, the health and wellness food and beverage sector in India reached US$10.3 billion in 2021, making it the 15th largest market globally. Health and wellness beverages, including functional drinks like yogurt-based beverages, represented about a quarter of this market in 2021 and are expected to account for more than a third by 2026.

The Indian government’s support for the dairy sector further bolsters this trend. Initiatives such as the National Dairy Plan and the Dairy Entrepreneurship Development Scheme aim to enhance dairy production and processing capabilities. For instance, the Dairy Entrepreneurship Development Scheme provides capital subsidies to farmers and entrepreneurs for setting up dairy units, thereby improving the supply chain for dairy products, including drinkable yogurt.

Restraints

Logistical Challenges and Cold Chain Limitations

One of the primary obstacles hindering the growth of the drinkable yogurt market in India is the inadequate cold chain infrastructure. Maintaining the integrity of probiotic-rich beverages like drinkable yogurt necessitates consistent refrigeration from production to consumption. However, in many rural regions, the absence of reliable cold storage facilities and transportation systems leads to product spoilage, quality degradation, and increased operational costs. This logistical bottleneck not only affects product availability but also limits market reach, particularly in underserved areas.

The Indian dairy sector, despite being the world’s largest producer of milk, faces challenges related to infrastructure development. While initiatives like the National Dairy Plan aim to enhance dairy farming and processing, the implementation of such programs often encounters delays and logistical hurdles. These challenges are compounded by the vast geographical expanse of the country, which makes the establishment of an efficient cold chain network both complex and capital-intensive. Consequently, ensuring the timely delivery of drinkable yogurt products without compromising their quality remains a significant challenge.

Addressing these infrastructural limitations requires substantial investment in cold storage facilities, refrigerated transportation, and last-mile delivery solutions. Furthermore, public-private partnerships and government incentives can play a pivotal role in bridging the infrastructure gap, ensuring that drinkable yogurt products can reach consumers across the country without quality degradation. Until such systemic improvements are realized, the full potential of the drinkable yogurt market in India may remain untapped.

Opportunity

Expansion of Cold Chain Infrastructure

A significant growth opportunity for the drinkable yogurt market in India lies in the development and expansion of cold chain infrastructure. Cold chain facilities are essential for preserving the quality and extending the shelf life of perishable products like drinkable yogurt. Currently, India’s cold chain infrastructure is underdeveloped, particularly in rural areas, leading to substantial post-harvest losses. The Ministry of Food Processing Industries reports that India loses over ₹92,000 crore annually due to inadequate cold storage and supply chain logistics.

To address these challenges, the Indian government has initiated several schemes aimed at enhancing cold chain infrastructure. The Integrated Cold Chain and Value Addition Infrastructure Scheme provides financial assistance of up to ₹10 crore per project to encourage the establishment of cold storage and preservation facilities across the country. Additionally, the National Centre for Cold-chain Development (NCCD) serves as a think tank to guide the development of cold-chain in India, focusing on improving infrastructure and reducing food losses.

The expansion of cold chain infrastructure not only reduces spoilage and waste but also opens new markets for drinkable yogurt producers. With improved storage and transportation facilities, producers can reach consumers in previously underserved regions, thereby increasing their market share. Moreover, the development of multi-modal logistics parks, which include cold storage facilities, is expected to further streamline the distribution of perishable goods.

Regional Insights

Asia‑Pacific (APAC) Dominates Drinkable Yogurt Market with 38.9% Share and USD 16.8 Bn Value in 2024

In 2024, the Asia‑Pacific region held a commanding 38.9% share—equating to around USD 16.8 billion—of the global drinkable yogurt market. This reflects its leading position not just in volume, but also in dynamic demand growth. Health-conscious consumers across APAC—particularly in major markets like China, India, and Japan—are embracing drinkable yogurt for its probiotic benefits, gut health support, and convenient format, which align perfectly with busy lifestyles.

The region’s leadership is driven by growing awareness of probiotic benefits and yogurt’s role in digestive health—especially among urban dwellers in China, India, Japan, and Southeast Asia. In these markets, busy schedules and rising incomes are fueling demand for convenient, nutritious beverages that blend wellness with taste. In China alone, dairy-based probiotic drinks, including drinkable yogurt, are rising to prominence as go-to gut-health choices.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Amy’s Kitchen, known for its organic and vegetarian food offerings, has steadily entered the drinkable yogurt space by catering to the health-conscious and clean-label consumer segment. The company emphasizes organic ingredients, non-GMO certification, and eco-friendly practices. In 2024, Amy’s focused on expanding its dairy-based drinkables using traditional cultures and natural fruit flavors. Their products are gaining traction in North America, especially among consumers seeking wholesome, ready-to-drink probiotic beverages with ethical and sustainable sourcing.

Pillars Drinkable Yogurt specializes exclusively in high-protein, low-sugar drinkable yogurts made with grass-fed dairy and live probiotic cultures. In 2024, the brand continued expanding across health food chains and online platforms in the U.S., gaining popularity among fitness-conscious and clean-eating consumers. With no added sugar and up to 18g of protein per bottle, Pillars sets itself apart through a clear wellness message and minimalist ingredient lists. It’s positioned as a premium, performance-driven dairy beverage brand.

Goya Foods, a leader in Latin American food products, includes drinkable yogurt as part of its dairy offerings under the “Goya Yogurt Smoothies” range. In 2024, Goya continued catering to Hispanic and multicultural markets in the U.S. with fruit-flavored yogurts enriched with protein and probiotics. Known for flavor authenticity and affordability, Goya leverages its strong brand loyalty and distribution in ethnic grocery chains, making its drinkable yogurt range accessible to a broad, community-rooted customer base.

Top Key Players Outlook

- Amy’s Kitchen, Inc.

- Bellisio Foods, Inc.

- Conagra Foods, Inc.

- Pillars Drinkable Yogurt

- Goya Foods, Inc.

- Kraft Heinz

- Iceland Foods Ltd

- General Mills Inc

- Nestle

- Kellogg Co.

Recent Industry Developments

In 2024, Amy’s Kitchen reached peak annual revenue of USD 500 million, fueling confidence in its ability to venture into adjacent wellness categories like probiotic drinks—backed by organic, non‑GMO values.

In 2024, Bellisio reached a peak revenue of USD 550 million and had around 1,385 employees, meaning each person produced about USD 397,100 in revenue—a solid measure of efficiency and output in the frozen‑food business.

Report Scope

Report Features Description Market Value (2024) USD 43.3 Bn Forecast Revenue (2034) USD 76.8 Bn CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Category (Dairy-based Yogurt, Non-dairy Based Yogurt), By Flavor (Flavored, Plain), By Sales Channel (Supermarkets/Hypermarkets, Departmental Stores, Convenience Store, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Amy’s Kitchen, Inc., Bellisio Foods, Inc., Conagra Foods, Inc., Pillars Drinkable Yogurt, Goya Foods, Inc., Kraft Heinz, Iceland Foods Ltd, General Mills Inc, Nestle, Kellogg Co. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Amy's Kitchen, Inc.

- Bellisio Foods, Inc.

- Conagra Foods, Inc.

- Pillars Drinkable Yogurt

- Goya Foods, Inc.

- Kraft Heinz

- Iceland Foods Ltd

- General Mills Inc

- Nestle

- Kellogg Co.

Our Clients

- 156536

- Aug 2025