Quick Navigation

- Market Overview

- Key Takeaways

- Product Type Analysis

- Diagnostics Type Analysis

- Therapeutics Type Analysis

- Application Analysis

- End User Analysis

- Technology Analysis

- Distribution Channel Analysis

- Key Market Segments

- Driver

- Challenge

- Restraints

- Opportunity

- Regional Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Market Overview

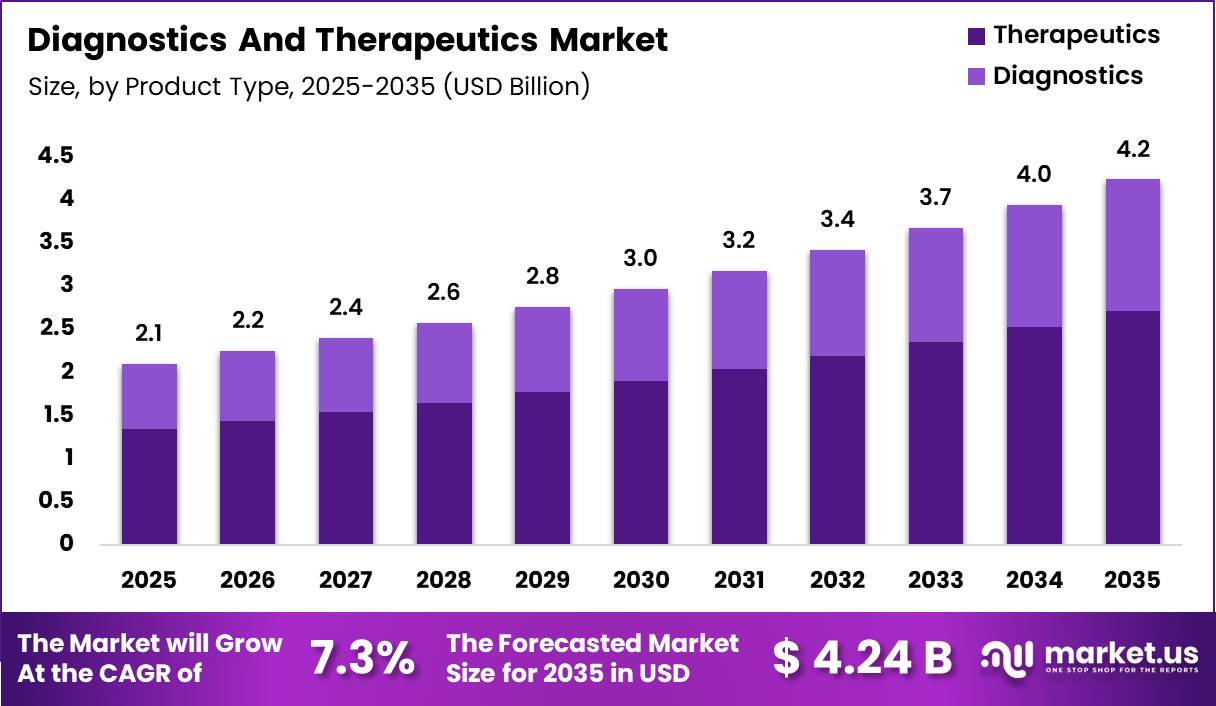

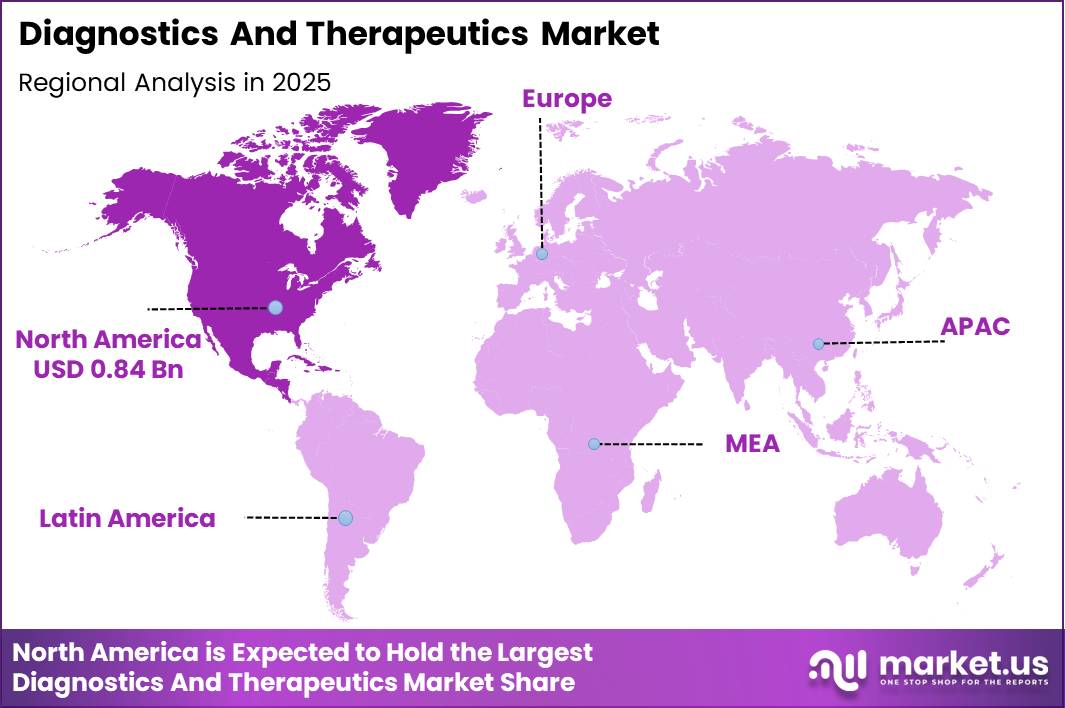

Global Diagnostics and Therapeutics Market size is expected to be worth around US$ 4.24 Billion by 2035 from US$ 2.1 Billion in 2025, growing at a CAGR of 7.30% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.00% share with a revenue of US$ 0.84 Billion.

The Diagnostics and Therapeutics Market plays a vital role in strengthening healthcare systems by enabling early disease detection, accurate clinical decision-making, and effective treatment outcomes. Diagnostics include laboratory tests, molecular assays, imaging technologies, and point-of-care tools that help identify diseases and monitor patient health.

According to the World Health Organisation, diagnostic information supports nearly 70% of medical decisions, while diagnostics account for only about 5% of total healthcare spending, highlighting major growth potential.

Therapeutics include medicines, vaccines, biologics, and advanced treatment approaches designed to prevent, manage, or cure diseases. Government-backed research institutions, such as the National Institutes of Health, continue to accelerate innovation through substantial biomedical research funding, supporting progress in cancer, cardiovascular disease, infectious diseases, and rare conditions.

Public health agencies also emphasise the value of integrating diagnostics and therapeutics, especially as chronic diseases and complex health conditions continue to rise worldwide. Overall, the market is expanding as healthcare systems prioritise early detection, precision medicine, and improved patient outcomes across diverse patient populations.

Key Takeaways

- Market Size: The Global Diagnostics and Therapeutics Market size was US$ 2.1 billion in 2025. The market is estimated to grow to US$ 4.2 billion by 2035.

- Market Share: The market’s Compound Annual Growth Rate (CAGR) from 2026 to 2035 will be 7.3%.

- Product Type: Therapeutics has the largest market share, accounting for 64% of total product type revenue.

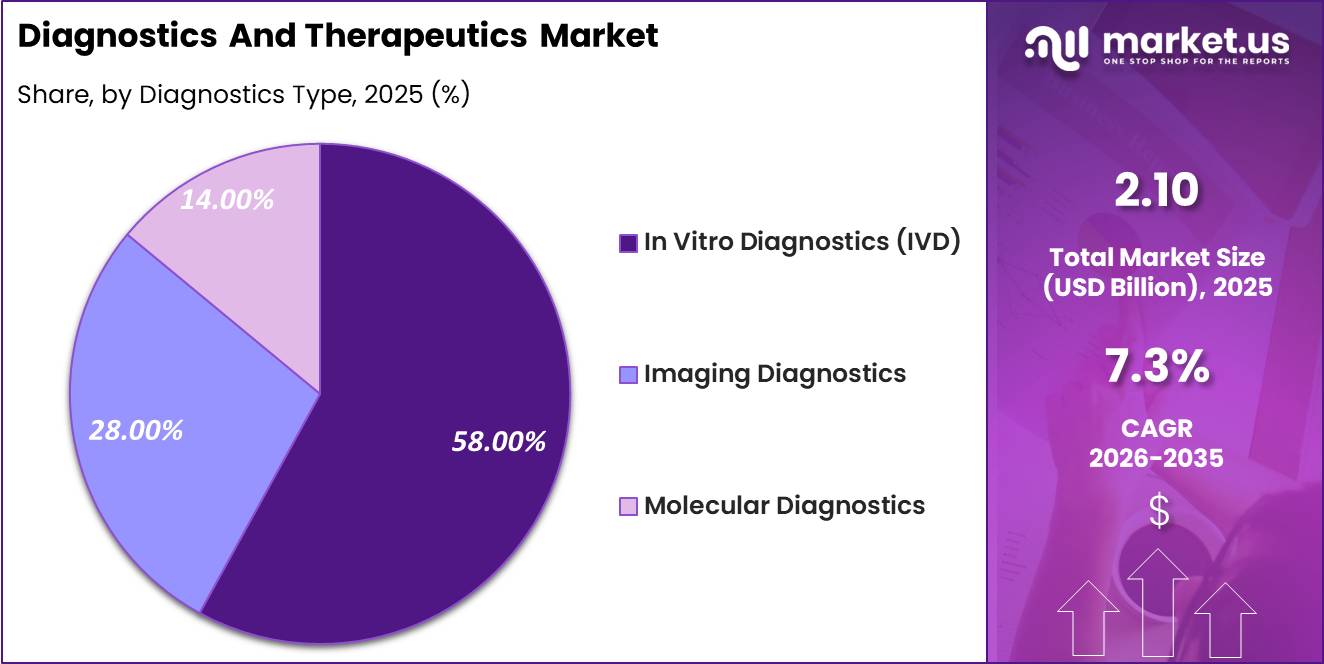

- Diagnostics Type: In Vitro Diagnostics (IVD) leads the segment, accounting for 58% of total diagnostics type revenue.

- Therapeutics Type: Pharmaceuticals leads the segment, accounting for 61% of total therapeutics type revenue.

- Application: Oncology leads the segment, accounting for 29% of total application revenue.

- End User: Hospitals lead the segment, accounting for 46% of total end-user revenue.

- Technology: Conventional Diagnostics & Therapies dominate the segment, accounting for 57% of total technology revenue.

- Distribution Channel: Hospital Procurement leads the segment, accounting for 43% of total distribution channel revenue.

- Regional: North America is the dominant regional market, accounting for 40% of global revenue.

Product Type Analysis

The Diagnostics and Therapeutics Market is broadly segmented into Therapeutics and Diagnostics, with Therapeutics dominating the landscape by accounting for 64.00% of the total market share in 2025.

This dominance reflects the sustained and recurring demand for treatment solutions across chronic, acute, and lifestyle-related diseases, where long-term medication use and therapy continuation drive higher value generation. Therapeutics benefit from ongoing innovation in drug formulations, combination therapies, and personalised treatment approaches, which continue to expand clinical adoption across global healthcare systems.

The Diagnostics segment represents 36.00% of the market, playing a foundational role in disease detection, monitoring, and treatment planning. While diagnostics typically generate lower per-unit revenue than therapeutics, their volume-driven demand remains strong due to increasing screening programs, preventive healthcare initiatives, and rising awareness of early diagnosis.

The integration of diagnostics with treatment decision-making, particularly in oncology and infectious diseases, further strengthens their strategic importance. Overall, the product type segmentation reflects a healthcare ecosystem where diagnostics act as the entry point for care, while therapeutics capture sustained economic value through disease management and long-term patient engagement.

Diagnostics Type Analysis

By diagnostics type, the market is led by In Vitro Diagnostics (IVD), which holds a commanding 58.00% market share in 2025. IVD’s leadership is supported by its widespread use in routine testing, disease screening, and monitoring of chronic and infectious conditions through blood, urine, and tissue-based assays. The scalability, automation potential, and cost efficiency of IVD platforms make them essential across hospitals and laboratories.

Imaging Diagnostics, accounting for 28.00% of the market, continues to play a critical role in disease visualisation, staging, and treatment follow-up, particularly in oncology, cardiovascular, and neurological applications. Advances in digital imaging and hybrid modalities have improved diagnostic accuracy while supporting non-invasive care.

Molecular Diagnostics, with a 14.00% share, represents the most innovation-driven segment, benefiting from growing adoption in genetic testing, precision medicine, and infectious disease identification. Although smaller in share, molecular diagnostics demonstrate strong growth momentum due to increasing demand for high-sensitivity and high-specificity testing. Together, these segments highlight a diagnostics landscape balancing high-volume routine testing with advanced, data-intensive technologies.

Therapeutics Type Analysis

Therapeutics type segmentation shows Pharmaceuticals as the dominant category, capturing 61.00% of the market share in 2025. This segment benefits from the extensive use of small-molecule drugs across a wide range of disease areas, including cardiovascular, metabolic, and infectious disorders. Established manufacturing processes, broad prescribing familiarity, and affordability relative to advanced therapies continue to support pharmaceutical dominance.

Biologics represent a rapidly expanding segment, driven by their targeted mechanisms of action and strong clinical efficacy in complex diseases such as cancer and autoimmune disorders. Although biologics account for a smaller share than pharmaceuticals, their higher treatment costs and expanding indications significantly contribute to market value growth.

Cell and Gene Therapies remain an emerging but transformative segment, focused on addressing unmet medical needs and rare or treatment-resistant conditions. While currently limited by high development costs and specialised infrastructure requirements, these therapies are gaining strategic importance due to their curative potential and long-term healthcare impact. Overall, the therapeutics landscape reflects a transition from traditional drug models toward biologically complex and personalised treatment solutions.

Application Analysis

Application-based segmentation highlights Oncology as the leading segment, accounting for 29.00% of the market share in 2025 and also representing the fastest-growing application area. The high prevalence of cancer, combined with continuous innovation in diagnostics, targeted therapies, and combination treatment regimens, drives sustained demand across both diagnostic and therapeutic products.

Cardiovascular Diseases form another significant application segment, supported by the global burden of heart-related conditions and the need for long-term disease management. Infectious Diseases continue to generate strong demand, particularly for diagnostics and therapeutics related to outbreak preparedness, antimicrobial treatments, and vaccination programs.

Neurological Disorders benefit from increasing diagnosis rates and growing research into disease-modifying therapies, while Metabolic Disorders, including diabetes, drive consistent demand for both monitoring tools and lifelong treatment solutions. The Others category captures applications such as respiratory and autoimmune diseases. Overall, application segmentation reflects a shift toward complex, high-burden diseases where integrated diagnostic and therapeutic solutions are essential for improving patient outcomes.

End User Analysis

End user segmentation is led by Hospitals, which account for 46.00% of the total market share in 2025. Hospitals serve as the primary centres for diagnosis, treatment initiation, and complex care delivery, making them the largest consumers of both diagnostic tools and therapeutic products. Their dominance is reinforced by access to advanced infrastructure, multidisciplinary expertise, and higher patient volumes.

Diagnostic Laboratories represent a significant secondary segment, driven by the growing outsourcing of testing services, expansion of preventive screening programs, and increasing test volumes for chronic and infectious diseases.

Speciality Clinics continue to gain importance as focused care centres for oncology, cardiology, and neurology, offering targeted diagnostic and treatment services with faster patient access.

Research Institutes form a smaller but strategically vital segment, contributing to clinical trials, technology validation, and translational research that supports long-term market innovation. Collectively, end-user segmentation illustrates a healthcare delivery model where hospitals anchor care pathways, while laboratories, clinics, and research institutions enhance efficiency, specialisation, and innovation across the diagnostics and therapeutics ecosystem.

Technology Analysis

From a technology perspective, Conventional Diagnostics & Therapies dominate the market with a 57.00% share in 2025. This segment includes established laboratory tests, imaging systems, and standard drug therapies that remain widely adopted due to their reliability, regulatory familiarity, and cost-effectiveness. Conventional technologies continue to serve as the backbone of healthcare delivery, particularly in large patient populations and resource-constrained settings.

Precision Medicine represents a rapidly advancing segment, leveraging genetic, molecular, and clinical data to tailor diagnostics and treatments to individual patients. Although smaller in share, precision medicine is reshaping clinical decision-making by improving treatment efficacy and reducing adverse outcomes.

AI-Enabled Diagnostics are emerging as a transformative technology, enhancing image interpretation, pattern recognition, and workflow efficiency across diagnostic processes. While adoption is still in early stages, AI-driven solutions demonstrate strong potential to improve accuracy and reduce time to diagnosis. Overall, technology segmentation reflects a gradual transition from standardised care models toward data-driven, personalised, and digitally enabled healthcare solutions.

Distribution Channel Analysis

Distribution channel segmentation shows Hospital Procurement as the leading channel, accounting for 43.00% of the market share in 2025. Hospitals rely on centralised procurement systems to ensure a consistent supply of diagnostics and therapeutics, particularly for inpatient care and complex treatment protocols.

Retail Pharmacies represent a major channel for outpatient therapeutics, supporting prescription fulfilment and chronic disease management at the community level. Speciality Pharmacies play an increasingly important role in distributing high-cost and complex therapies, including biologics and advanced treatments that require specialised handling and patient support services.

Online Pharmacies & Platforms are the fastest-evolving distribution segment, driven by digital health adoption, improved logistics, and growing consumer preference for convenience and accessibility. While online channels currently hold a smaller share, they are reshaping purchasing behaviour and expanding reach, particularly in urban and semi-urban markets.

Together, distribution channel segmentation highlights a balanced ecosystem where institutional procurement ensures clinical continuity, while retail, speciality, and digital platforms enhance patient access and treatment adherence.

Key Market Segments

By Product Type

- Therapeutics

- Diagnostics

By Diagnostics Type

- In Vitro Diagnostics (IVD)

- Imaging Diagnostics

- Molecular Diagnostics

By Therapeutics Type

- Pharmaceuticals

- Biologics

- Cell & Gene Therapies

By Application

- Oncology

- Cardiovascular Diseases

- Infectious Diseases

- Neurological Disorders

- Metabolic Disorders

- Others

By End User

- Hospitals

- Diagnostic Laboratories

- Specialty Clinics

- Research Institutes

By Technology

- Conventional Diagnostics & Therapies

- Precision Medicine

- AI-Enabled Diagnostics

By Distribution Channel

- Hospital Procurement

- Retail Pharmacies

- Specialty Pharmacies

- Online Pharmacies & Platforms

Driver

GLP-1-led chronic care expansion is raising therapy and monitoring demand

The chronic-care therapy base is widening materially as GLP-1 medicines move beyond diabetes into obesity-linked long-term management. The World Health Organisation issued its first guideline on GLP-1 medicines for obesity in late 2025 and stated that obesity affects more than 1 billion people globally, while also confirming that GLP-1 therapies had been added to the Essential Medicines List for managing type 2 diabetes in high-risk groups in September 2025.

That shift supports higher therapeutic volumes and also lifts diagnostic demand because broader use of semaglutide, liraglutide, and tirzepatide requires patient identification, metabolic monitoring, comorbidity screening, and therapy follow-up across primary care and speciality channels.

Structurally, this pushes the market away from isolated treatment episodes toward longitudinal care models in which diagnostics, prescribing, and monitoring become recurring revenue layers rather than one-time interventions.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision diagnostics linked to accelerated device approval pathways | +2.2% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| GLP-1-led chronic care expansion is raising therapy and monitoring demand | +2.0% | North America core, EU5, Australia, Gulf markets, developed APAC | Short term (≤ 2 years) |

| Medicare and public reimbursement support for clinical lab utilisation | +1.5% | U.S. core, Western Europe spill-over, Japan reference effect | Short term (≤ 2 years) |

| Evidence-heavy regulatory transition improving quality and market consolidation | +1.2% | EU core, U.S., UK, Canada, export-focused APAC | Medium term (2-4 years) |

| Decentralised infectious disease testing sustaining routine diagnostic throughput | +0.9% | U.S., EU, India urban centres, Southeast Asia, and Latin America cities | Short term (≤ 2 years) |

Challenge

Clinical Talent Availability as a Growth Constraint

Clinical workforce bottlenecks remain a persistent market challenge because diagnostics and therapeutics growth depends on enough trained personnel across laboratories, hospital systems, trial sites, pharmacovigilance teams, and data operations, while the World Health Organisation still points to a projected global shortfall of 11 million health workers by 2030, indicating that labour scarcity is not a temporary post-pandemic distortion but a structural operating deficit.

In practical market terms, this creates recurring friction through slower site activation, longer test-to-report turnaround, constrained patient enrollment, and higher overtime and contractor intensity, which together can lift operating expense by roughly 4–7% in labour-sensitive functions and defer commercialisation ramp-up by 2–4 quarters in complex programs, justifying an estimated –1.2% drag on achievable market CAGR in 2026 baseline conditions.

To navigate this, companies are being forced into durable redesign rather than short-term hiring fixes, including centralised reading hubs, digital pathology triage, automation in sample prep and adjudication, hybrid trial operations, and multi-year training pipelines with academic centres, yet the long credentialing cycle for specialised staff and continued concentration of talent in major metro clusters make normalisation a long-term issue rather than a near-term correction.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Clinical workforce bottlenecks | -1.2% | North America, EU, Emerging Asia | Long term (≥ 4 years) |

| Biomanufacturing execution strain | -1.1% | US, EU, East Asia | Long term (≥ 4 years) |

| Multi-layer evidence burden | -0.9% | US, EU, China, Japan | Medium term (2-4 years) |

| Cold-chain network volatility | -0.8% | APAC corridors, EU-US lanes, Gulf hubs | Medium term (2-4 years) |

| Reimbursement timing dispersion | -1.0% | US, EU-5, China, Brazil | Long term (≥ 4 years) |

| Data integration inefficiency | -0.7% | North America core, EU hospital systems | Medium term (2-4 years) |

Restraints

Reimbursement Risk in Diagnostics and Therapeutics

Reimbursement pressure remains one of the clearest constraints on diagnostics and therapeutics growth because cost inflation across care delivery is not being matched evenly by payment systems, forcing laboratories, hospitals, and therapy providers to absorb rising operating expense before they can fully pass it through into realized revenue Centers for Medicare & Medicaid Services.

It confirms that the Clinical Laboratory Fee Schedule remains the governing reimbursement backbone for many diagnostic tests and that the next reporting cycle feeds future rate-setting, while hospital-sector evidence from the American Hospital Association shows that care delivery costs continue to rise faster than pricing, increasing pressure on all downstream purchasing and treatment decisions.

The operational bottleneck is that even modest reimbursement compression can disproportionately hurt diagnostics platforms and speciality therapy pathways because labour, quality systems, validation work, software integration, and instrument-service overhead are largely fixed, which reduces contribution margins, narrows the viable menu for low-volume assays, and makes providers more selective on premium treatment adoption where prior authorisation or step edits slow patient conversion.

Strategically, this results in slower rollout of higher-cost platforms, tighter commercial prioritisation around better-covered indications, and delayed expansion into community settings, supporting an estimated 1.3 percentage-point drag on forward CAGR in North America and reimbursement-sensitive European markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement pressure | -1.3% | North America core, EU | Medium term |

| Regulatory compliance burden | -1.2% | EU core, UK-linked supply chains | Short term |

| Trade and input-cost volatility | -1.0% | U.S., EU import channels, APAC export hubs | Short term |

| Provider budget stress | -0.9% | U.S., Western Europe, urban APAC | Short term |

| Supply-chain disruption risk | -0.8% | North America, EU, global sourcing nodes | Medium term |

| Evidence and access hurdles | -1.0% | U.S., EU, Japan | Long term |

Opportunity

Untapped Companion Diagnostics Potential in Non-Oncology Therapies

This is an opportunity rather than a baseline driver because the current diagnostics-and-therapeutics market already reflects established use of companion diagnostics in oncology, while the underexploited upside lies in extending biomarker-linked treatment selection into immunology, neurology, rare disease, and cardiometabolic pathways where testing is still not routinely embedded in prescribing workflows.

The economic upside can reasonably add about 2.2% points to baseline CAGR because broader CDx use can improve therapy match rates by an estimated 8% to 14%, reduce avoidable non-response cost by 12% to 25%, and create premium reimbursement leverage where a diagnostic becomes essential for safe and effective product use, which is consistent with U.S. Food and Drug Administration’s definition of companion diagnostics and with the continuing expansion of FDA-cleared or approved CDx pathways.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Non-oncology CDx expansion | +2.2% | US, EU, Japan | Medium term |

| Integrated Dx-Rx care models | +2.0% | US, EU5, China | Short term |

| Decentralised test-to-treat | +1.7% | APAC, LATAM, Africa, US retail | Short term |

| AI-enabled pathology economics | +1.5% | US, EU, South Korea, GCC | Medium term |

| WHO-linked access expansion | +1.8% | Africa, South Asia, ASEAN | Medium term |

| Speciality assay roll-up | +1.4% | US, EU, developed APAC | Long term |

Regional Analysis

In 2025, North America led the market, achieving over 40.00% share with a revenue of US$0.84 billion. North America dominates the market due to its advanced healthcare infrastructure, high healthcare spending, and early adoption of innovative diagnostic technologies and targeted therapies.

Strong presence of leading biotechnology and pharmaceutical companies, widespread use of precision medicine, and supportive reimbursement frameworks continue to drive market leadership. In addition, high awareness of early disease detection and routine screening supports sustained demand across diagnostics and therapeutics.

Europe represents the second-largest regional market, supported by well-established public healthcare systems and an increasing focus on personalised medicine. Countries such as Germany, the UK, and France are investing in molecular diagnostics, oncology therapeutics, and digital health integration, contributing to steady market expansion.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Rapid population growth, rising burden of chronic and infectious diseases, improving healthcare infrastructure, and increasing government investments in diagnostics are accelerating market adoption. Expanding access to healthcare in China, India, and Southeast Asia further strengthens growth prospects.

Latin America, the Middle East & Africa are emerging markets, driven by improving healthcare access and the gradual modernisation of diagnostic services. However, limited infrastructure and affordability challenges still restrain growth compared to developed regions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Suppliers in the global diagnostics and therapeutics market are working to gain a competitive edge by developing integrated theranostic platforms. These platforms combine the identification of diagnostic biomarkers with corresponding therapeutic interventions. In addition, there is significant investment in AI-enabled diagnostics, which aim to enhance the accuracy of disease detection and facilitate earlier interventions for oncology, cardiovascular, and neurological disorders.

Key strategic focus areas include the creation of precision medicine platforms that allow for biomarker-stratified patient selection for targeted therapy programs. Companies are also expanding their molecular diagnostics portfolios to meet the increasing demand for emerging infectious diseases and companion diagnostics in oncology. Furthermore, investments in cell and gene therapy pipelines represent the fastest-growing segment in therapeutics.

To secure long-term supply agreements with institutions, businesses are actively investing in building relationships with hospital procurement departments, forming partnerships with speciality clinic networks, and expanding regulatory approval programs in global markets.

The convergence of artificial intelligence with diagnostic imaging and in vitro diagnostics (IVD) platforms is driving a transformative technology trend. This integration enables automated disease detection, monitoring treatment responses, and predictive outcome modelling, reshaping competitive positioning in the diagnostics sector throughout the forecast period, leading up to 2035.

Top Key Players

- Roche Holding AG

- Abbott Laboratories

- Siemens Healthineers AG

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- GE HealthCare

- Pfizer Inc.

- Merck & Co., Inc.

- Johnson & Johnson

- Novartis AG

- AstraZeneca PLC

- Bristol Myers Squibb Company

- Sanofi S.A.

- Becton, Dickinson and Company

- QIAGEN N.V.

- Other Key Players

Recent Developments

- In January 2026, Roche Holding AG launched its next-generation AI-enabled IVD platform for oncology biomarker detection across North American and European hospital laboratory institutional buyers, targeting improved early cancer diagnosis accuracy.

- In February 2026, Danaher Corporation expanded its molecular diagnostics portfolio through the acquisition of a speciality infectious disease diagnostic platform, strengthening its institutional laboratory procurement relationships across hospital and reference laboratory buyers globally.

- In March 2026, AstraZeneca secured regulatory approval for its companion diagnostic and targeted therapy combination platform for non-small cell lung cancer, enabling integrated precision medicine treatment protocols across European oncology centre institutional buyers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.1 Billion |

| Forecast Revenue (2035) | US$ 4.24 Billion |

| CAGR (2026-2035) | 7.30% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Therapeutics, Diagnostics), By Diagnostics Type (In Vitro Diagnostics (IVD), Imaging Diagnostics, Molecular Diagnostics), By Therapeutics Type (Pharmaceuticals, Biologics, Cell & Gene Therapies), By Application (Oncology, Cardiovascular Diseases, Infectious Diseases, Neurological Disorders, Metabolic Disorders, Others), By End User (Hospitals, Diagnostic Laboratories, Specialty Clinics, Research Institutes), By Technology (Conventional Diagnostics & Therapies, Precision Medicine, AI-Enabled Diagnostics), By Distribution Channel (Hospital Procurement, Retail Pharmacies, Specialty Pharmacies, Online Pharmacies & Platforms) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Roche Holding AG, Abbott Laboratories, Siemens Healthineers AG, Danaher Corporation, Thermo Fisher Scientific Inc., GE HealthCare, Pfizer Inc., Merck & Co., Inc., Johnson & Johnson, Novartis AG, AstraZeneca PLC, Bristol Myers Squibb Company, Sanofi S.A., Becton, Dickinson and Company, QIAGEN N.V., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |