Quick Navigation

Report Overview

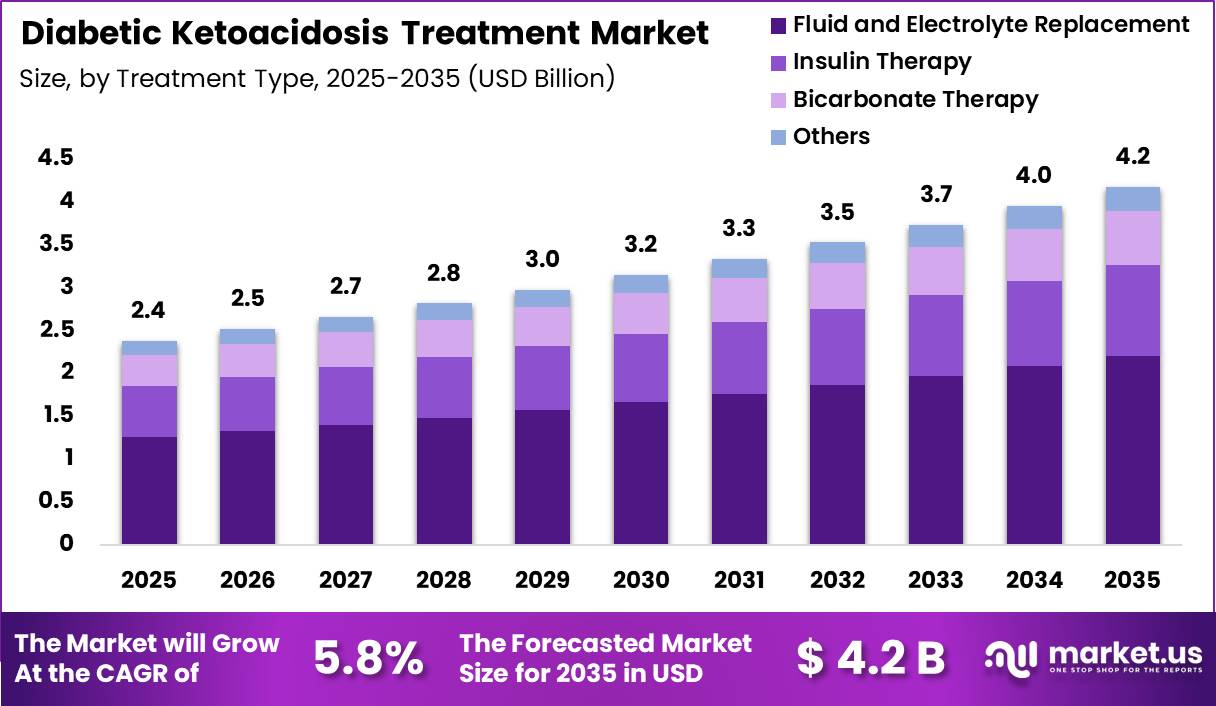

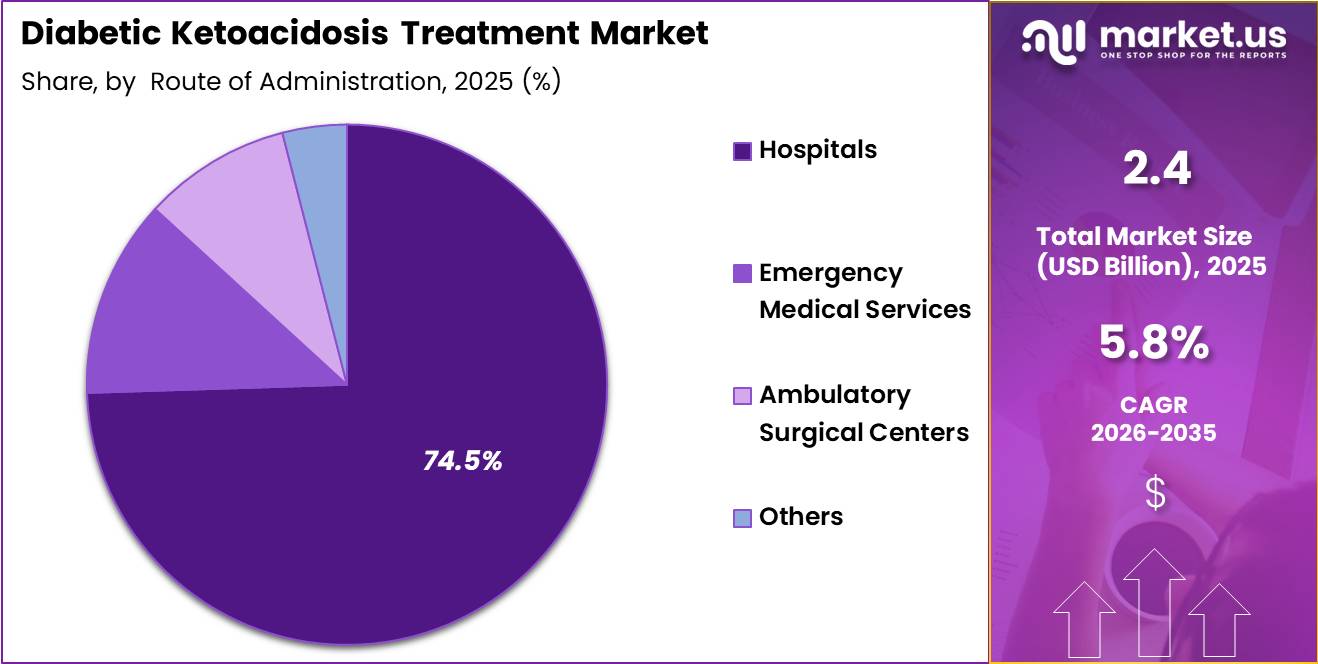

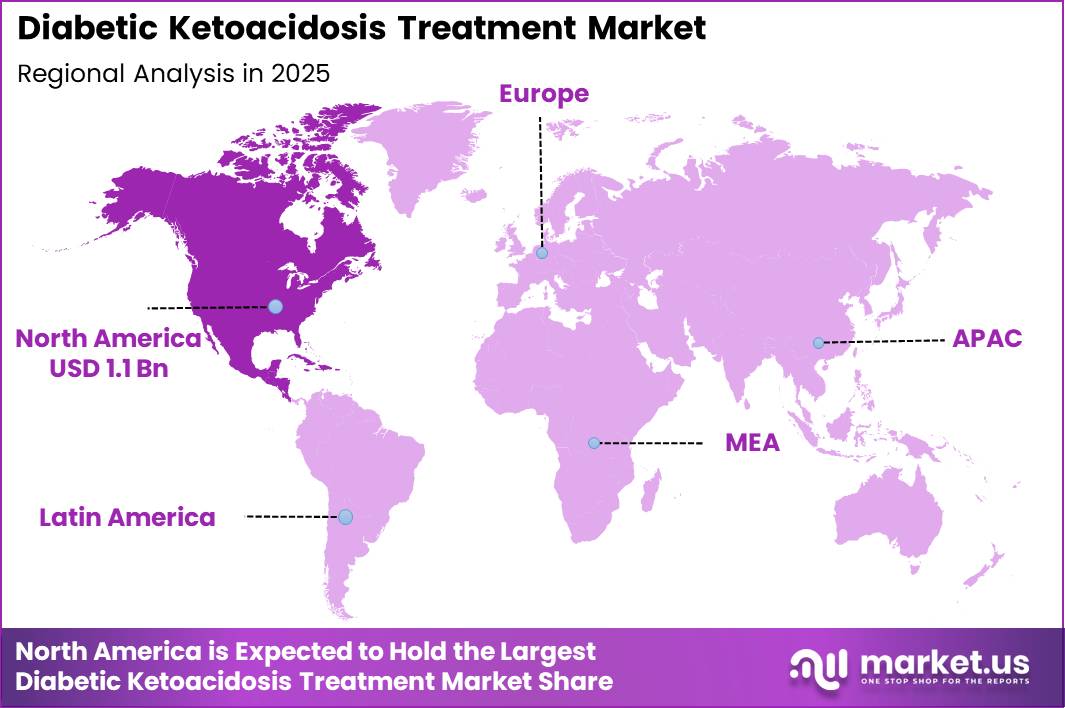

Global Diabetic Ketoacidosis Treatment Market size is expected to be worth around US$ 4.2 Billion by 2035 from US$ 2.4 Billion in 2025, growing at a CAGR of 5.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 45.2% share with a revenue of US$ 1.1 Billion.

The Diabetic Ketoacidosis (DKA) treatment market is closely associated with the growing global burden of diabetes and the increasing incidence of acute diabetic emergencies. DKA is a severe metabolic complication that occurs when the body lacks sufficient insulin, resulting in elevated blood glucose levels, ketone accumulation, and metabolic acidosis. According to the U.S. Centers for Disease Control and Prevention (CDC), DKA is one of the most serious and potentially life-threatening complications of diabetes and commonly requires emergency hospitalization and intensive medical management.

The treatment landscape for DKA primarily consists of intravenous insulin therapy, fluid resuscitation, electrolyte replacement, continuous glucose monitoring, and critical care services. Clinical guidelines indicate that prompt administration of insulin and intravenous fluids remains the standard of care for DKA management. Electrolyte correction, particularly potassium replacement, is also essential due to significant electrolyte losses during the condition.

The increasing prevalence of diabetes is creating a larger patient pool at risk of developing DKA. The International Diabetes Federation (IDF) estimates that more than 537 million adults worldwide are living with diabetes, a number expected to rise significantly over the coming decades. Furthermore, DKA remains one of the leading causes of hospitalization among individuals with type 1 diabetes. Epidemiological studies reported by the U.S. National Center for Biotechnology Information (NCBI) indicate that DKA incidence ranges from 0 to 56 cases per 1,000 person-years across different populations, highlighting a substantial healthcare burden.

Growth in the DKA treatment market is supported by increasing hospital admissions, improved access to emergency care, advancements in insulin formulations, and wider adoption of continuous glucose monitoring technologies. In addition, rising awareness regarding diabetes management and early detection of hyperglycemic emergencies is contributing to improved treatment outcomes. Healthcare systems globally are investing in diabetes care infrastructure to reduce complications and mortality associated with DKA, thereby supporting continued demand for DKA treatment products and services.

Key Takeaways

- Market Size: Global Diabetic Ketoacidosis Treatment Market size is expected to be worth around US$ 4.2 Billion by 2035 from US$ 2.4 Billion in 2025.

- Market Share: The Market growing at a CAGR of 5.8% during the forecast period from 2026 to 2035.

- Treatment Type Analysis: Fluid and Electrolyte Replacement is projected to dominate the market, accounting for 52.7% of the total market share in 2025.

- Route of Administration Analysis: The Intravenous segment is expected to hold the largest market share of 81.2% in 2025.

- End User Analysis: Hospitals are anticipated to dominate the market with a 74.5% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 45.2% share with a revenue of US$ 1.1 Billion.

Treatment Type Analysis

The treatment type segment of the Diabetic Ketoacidosis (DKA) Treatment Market is categorized into Fluid and Electrolyte Replacement, Insulin Therapy, Bicarbonate Therapy, and Others. Fluid and Electrolyte Replacement is projected to dominate the market, accounting for 52.7% of the total market share in 2025.

The segment’s leadership is attributed to its critical role as the first-line intervention in DKA management. Patients with DKA typically experience severe dehydration and electrolyte imbalances, making fluid resuscitation essential for restoring circulatory volume, improving renal perfusion, and correcting metabolic abnormalities. Growing hospital admissions related to diabetes complications and the increasing adoption of standardized DKA treatment protocols further support segment growth.

Insulin Therapy represents the second-largest segment, driven by its indispensable role in reducing blood glucose levels and suppressing ketone production. Continuous intravenous insulin administration remains a standard treatment approach in moderate to severe DKA cases.

Bicarbonate Therapy occupies a smaller share and is primarily utilized in patients with severe metabolic acidosis. The Others segment includes adjunctive therapies and supportive care measures used to address underlying triggers and associated complications, contributing to comprehensive patient management and improved clinical outcomes.

Route of Administration Analysis

Based on route of administration, the Diabetic Ketoacidosis Treatment Market is segmented into Intravenous, Subcutaneous, and Others. The Intravenous segment is expected to hold the largest market share of 81.2% in 2025. The dominance of this segment is primarily due to the urgent nature of DKA treatment, where rapid correction of dehydration, electrolyte imbalance, and hyperglycemia is required.

Intravenous administration enables immediate delivery of fluids, insulin, and electrolytes, ensuring faster therapeutic response and better clinical control in critically ill patients. Hospital-based treatment protocols and emergency care guidelines strongly favor intravenous therapy, further strengthening segment growth.

The Subcutaneous segment is gaining attention, particularly in cases of mild to moderate DKA where selected patients can be managed with rapid-acting insulin analogs outside intensive care settings. Advantages such as reduced healthcare resource utilization and simplified administration are supporting gradual adoption.

The Others segment includes alternative administration approaches used in specific clinical scenarios and supportive treatments. Increasing research on less invasive treatment strategies and efforts to reduce hospitalization costs are expected to create growth opportunities for non-intravenous administration methods, although intravenous therapy will continue to remain the standard of care throughout the forecast period.

End User Analysis

Based on end user, the Diabetic Ketoacidosis Treatment Market is segmented into Hospitals, Emergency Medical Services, Ambulatory Surgical Centers, and Others. Hospitals are anticipated to dominate the market with a 74.5% share in 2025. The segment’s leading position is attributed to the high prevalence of severe DKA cases requiring intensive monitoring, continuous insulin infusion, electrolyte management, and specialized medical care.

Hospitals possess advanced diagnostic capabilities, intensive care units, and multidisciplinary healthcare teams necessary for effective DKA management. Rising diabetes prevalence and increasing emergency admissions related to acute metabolic complications continue to support strong demand within hospital settings.

Emergency Medical Services (EMS) represent an important segment, as rapid identification and initial stabilization of DKA patients significantly improve treatment outcomes. EMS providers play a critical role in initiating fluid replacement and facilitating timely hospital transfers. Ambulatory Surgical Centers account for a smaller market share and are primarily involved in managing selected mild cases and follow-up care services.

The Others segment includes specialty clinics and outpatient healthcare facilities that provide diabetes management and monitoring services. Continued improvements in emergency response systems and healthcare infrastructure are expected to enhance treatment accessibility, while hospitals remain the primary end-user segment due to the complexity and severity of DKA treatment requirements.

Key Market Segments

By Treatment Type

- Fluid and Electrolyte Replacement

- Insulin Therapy

- Bicarbonate Therapy

- Others

By Route of Administration

- Intravenous

- Subcutaneous

- Others

By End User

- Hospitals

- Emergency Medical Services

- Ambulatory Surgical Centers

- Others

Market Dynamics

Driving Factors: Rising Burden of Diabetes and Increasing Incidence of Diabetic Ketoacidosis (DKA)

The growth of the diabetic ketoacidosis (DKA) treatment market is primarily driven by the increasing prevalence of diabetes worldwide and the associated rise in acute diabetic complications. DKA is a life-threatening condition that occurs due to severe insulin deficiency and requires immediate treatment involving insulin therapy, fluid replacement, and electrolyte management.

According to the U.S. Centers for Disease Control and Prevention (CDC), approximately 40.1 million people in the United States were living with diagnosed or undiagnosed diabetes in 2023, representing about 12.0% of the population. Furthermore, around 2.1 million individuals were diagnosed with type 1 diabetes, the population at highest risk for DKA.

The CDC has also reported increasing hospitalization rates for DKA, particularly among individuals younger than 45 years of age. Hospital admissions associated with DKA have risen due to factors such as delayed diagnosis, poor glycemic control, missed insulin doses, and increasing diabetes incidence.

Additionally, DKA remains a significant healthcare burden, with approximately 5,400 deaths in the United States in 2021 listing DKA as an underlying cause of death. The need to reduce mortality and prevent severe complications is encouraging healthcare providers to adopt advanced treatment protocols and improve access to emergency care, thereby supporting market growth.

Trending Factors: Adoption of Advanced Monitoring Technologies and Standardized Treatment Protocols

A key trend shaping the diabetic ketoacidosis treatment market is the growing adoption of advanced diabetes monitoring technologies and evidence-based treatment protocols. Healthcare systems are increasingly focusing on early detection and prevention of DKA through continuous glucose monitoring (CGM), ketone monitoring devices, and digital diabetes management platforms.

Early identification of elevated ketone levels enables timely clinical intervention and reduces the likelihood of severe DKA episodes requiring intensive care. According to the CDC, patients with blood glucose levels of 250 mg/dL or higher are advised to monitor ketone levels regularly during illness to prevent progression to DKA.

Another notable trend is the implementation of standardized hospital treatment pathways that emphasize rapid fluid replacement, intravenous insulin administration, and electrolyte correction. These protocols have contributed to a decline in DKA-related in-hospital mortality despite rising hospitalization rates. The CDC reported that while DKA admissions increased between 2009 and 2014, case-fatality rates consistently declined, reflecting improvements in clinical management and emergency care practices.

Furthermore, increasing awareness regarding euglycemic DKA, particularly among patients using sodium-glucose cotransporter-2 (SGLT2) inhibitors, is encouraging broader ketone monitoring and physician education initiatives. These developments are expected to improve patient outcomes and support demand for innovative DKA treatment and monitoring solutions.

Restraining Factors: High Treatment Costs and Limited Access to Specialized Emergency Care

Despite favorable growth prospects, the diabetic ketoacidosis treatment market faces challenges related to high treatment costs and disparities in healthcare access. DKA is considered a medical emergency that often requires hospitalization, intensive monitoring, laboratory testing, intravenous insulin administration, electrolyte replacement, and management of underlying conditions. Such comprehensive treatment can result in substantial healthcare expenditures, particularly in low- and middle-income countries where critical care infrastructure may be limited.

Limited awareness regarding early DKA symptoms and inadequate access to diabetes education programs also contribute to delayed diagnosis and treatment. The CDC notes that DKA frequently develops when insulin therapy is interrupted or when diabetes remains undiagnosed. Individuals with restricted healthcare access may be unable to receive timely medical attention, increasing the risk of severe complications and prolonged hospitalization.

In addition, mortality rates remain elevated among older adults and patients with serious comorbidities. According to the National Center for Biotechnology Information (NCBI), mortality rates exceeding 5% have been reported among elderly DKA patients and those with life-threatening concurrent illnesses.

These factors create barriers to optimal treatment adoption and may limit market expansion in resource-constrained regions where specialized diabetes and emergency care services are insufficiently developed.

Opportunity: Expansion of Preventive Care and Early Detection Programs

Significant opportunities exist in the diabetic ketoacidosis treatment market through the expansion of preventive care initiatives, early diagnosis programs, and patient education efforts. Government agencies and healthcare organizations increasingly recognize that DKA is largely preventable through effective diabetes management and timely intervention. The CDC emphasizes that improved patient education, medication adherence, routine blood glucose monitoring, and access to healthcare services can substantially reduce DKA incidence and related mortality.

The growing global diabetes population presents a large addressable patient base for preventive technologies and therapeutic services. In the United States alone, more than 40 million people were estimated to have diabetes in 2023, while over 11 million adults remained undiagnosed. Early screening and disease management programs targeting these populations can reduce severe metabolic complications and create demand for DKA prevention and treatment solutions.

Moreover, expanding utilization of continuous glucose monitors, connected insulin delivery systems, and home ketone monitoring devices provides opportunities for healthcare providers and technology developers. These tools enable earlier detection of metabolic abnormalities before hospitalization becomes necessary. Public health initiatives focused on diabetes awareness, particularly among high-risk groups and younger populations experiencing rising DKA hospitalization rates, are expected to create long-term opportunities for market participants.

Regional Analysis

North America dominated the global Diabetic Ketoacidosis (DKA) Treatment Market in 2025, accounting for over 45.2% of the total market share and generating revenue of approximately US$ 1.1 billion. The region’s leadership can be attributed to the high prevalence of diabetes, advanced healthcare infrastructure, and widespread access to emergency and critical care services.

The United States represented the largest contributor within the region, supported by increasing incidences of type 1 and type 2 diabetes, growing awareness regarding diabetic complications, and the availability of well-established treatment protocols for DKA management. Furthermore, favorable reimbursement policies and continuous investments in healthcare technologies have strengthened market growth across North America.

Europe held the second-largest share of the market, driven by a growing diabetic population, rising healthcare expenditures, and increasing adoption of advanced insulin therapies and monitoring systems. Countries such as Germany, the United Kingdom, and France continue to invest in diabetes management programs, supporting market expansion.

The Asia Pacific region is expected to witness the fastest growth during the forecast period due to the rapidly increasing prevalence of diabetes, expanding healthcare infrastructure, and improving access to medical services in countries such as China, India, and Japan. Meanwhile, Latin America and the Middle East & Africa are experiencing gradual market growth, supported by improving healthcare facilities, increasing disease awareness, and government initiatives aimed at enhancing diabetes care and treatment accessibility.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Diabetic Ketoacidosis (DKA) Treatment Market is characterized by the presence of several multinational pharmaceutical and healthcare companies focused on insulin therapies, intravenous fluid solutions, electrolyte replacement products, and critical care management.

Key players include Eli Lilly and Company, Novo Nordisk A/S, Sanofi, and Pfizer Inc., which maintain strong positions through extensive diabetes treatment portfolios and continuous investments in research and development. These companies focus on enhancing insulin formulations, improving treatment efficacy, and expanding accessibility to critical diabetes care products.

In addition, companies such as Baxter International Inc. and B. Braun SE play a vital role by supplying intravenous fluids and electrolyte replacement therapies essential for DKA management. Strategic collaborations with hospitals, healthcare providers, and diabetes care centers have enabled these organizations to strengthen their market presence.

Market participants are increasingly emphasizing technological advancements, including smart insulin delivery systems and integrated patient monitoring solutions, to improve treatment outcomes and reduce hospitalization rates. Geographic expansion into emerging markets, where diabetes prevalence is rising rapidly, remains a key growth strategy. Furthermore, mergers, acquisitions, and product portfolio diversification are shaping the competitive landscape, allowing leading companies to enhance their capabilities and maintain long-term market competitiveness within the global DKA treatment sector.

Market Key Players

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi S.A.

- Pfizer Inc.

- Merck & Co., Inc.

- Baxter International Inc.

- B. Braun Melsungen AG

- Fresenius Kabi AG

- Becton, Dickinson and Company

- Hospira, Inc. (Pfizer)

- Biocon Limited

- Wockhardt Ltd.

- Torrent Pharmaceuticals Ltd.

- Zydus Lifesciences Limited

- Intas Pharmaceuticals Ltd.

- Others

Recent Developments

- May 2025 – Eli Lilly and Company announced the expansion of its long-standing collaboration with Purdue University through a planned investment of up to USD 250 million over the next eight years. The partnership is focused on accelerating pharmaceutical innovation, strengthening supply chains, and advancing the development of next-generation therapies, including treatments for metabolic and diabetes-related conditions.

- February 2026 – Novo Nordisk A/S entered into a partnership with Vivtex Corporation to develop next-generation oral biologic medicines for obesity and diabetes. The agreement includes research funding and milestone payments that could reach USD 2.1 billion, highlighting Novo Nordisk’s continued investment in innovative diabetes treatment technologies.

- May 2025 – Sanofi S.A. completed the acquisition of DR-0201 from Dren Bio through the purchase of Dren 0201, Inc. The deal included an upfront payment of USD 600 million with potential milestone payments of up to USD 1.3 billion, reinforcing Sanofi’s commitment to advancing innovative biologic therapies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.4 Billion |

| Forecast Revenue (2035) | US$ 4.2 Billion |

| CAGR (2026-2035) | 5.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Treatment Type (Fluid and Electrolyte Replacement, Insulin Therapy, Bicarbonate Therapy, Others) By Route of Administration (Intravenous, Subcutaneous, Others) By End User (Hospitals, Emergency Medical Services, Ambulatory Surgical Centers, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Novo Nordisk A/S, Eli Lilly and Company, Sanofi S.A., Pfizer Inc., Merck & Co., Inc., Baxter International Inc., B. Braun Melsungen AG, Fresenius Kabi AG, Becton, Dickinson and Company, Hospira, Inc. (Pfizer), Biocon Limited, Wockhardt Ltd., Torrent Pharmaceuticals Ltd., Zydus Lifesciences Limited, Intas Pharmaceuticals Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |