Global Design-to-Source Intelligence Market By Component (Software Platforms, Services), By Deployment Mode (Cloud-based, On-premises), By Enterprise Type (Large Enterprises, Small and Medium-sized Enterprises), By Application (Product Data Intelligence, Design Optimization, Others), By Industry Vertical (Electronics and Semiconductors, Automotive and Mobility, Others (Telecommunication, etc.)), By Solution Type (Should-Cost and Cost Breakdown Analytics, Others), By Enterprise Function (Procurement and Strategic Sourcing, Engineering and Product Design, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178740

- Number of Pages: 281

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Enterprise Type

- By Application

- By Industry Vertical

- By Solution Type

- By Enterprise Function

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

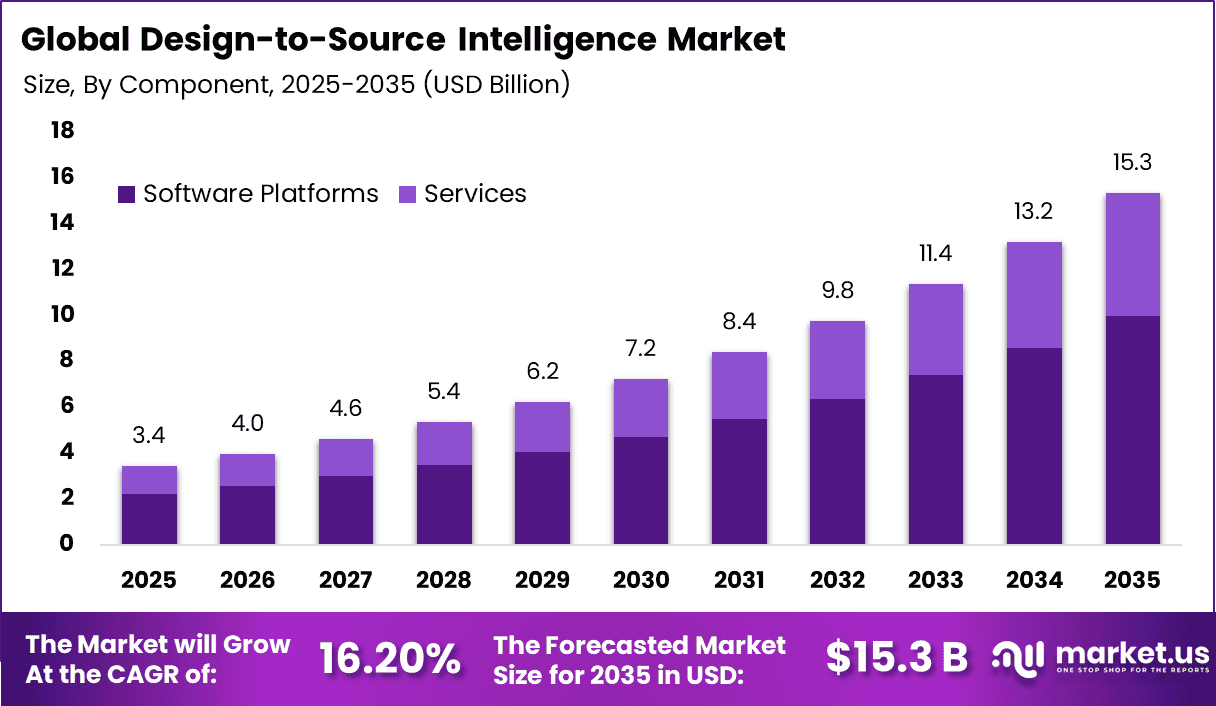

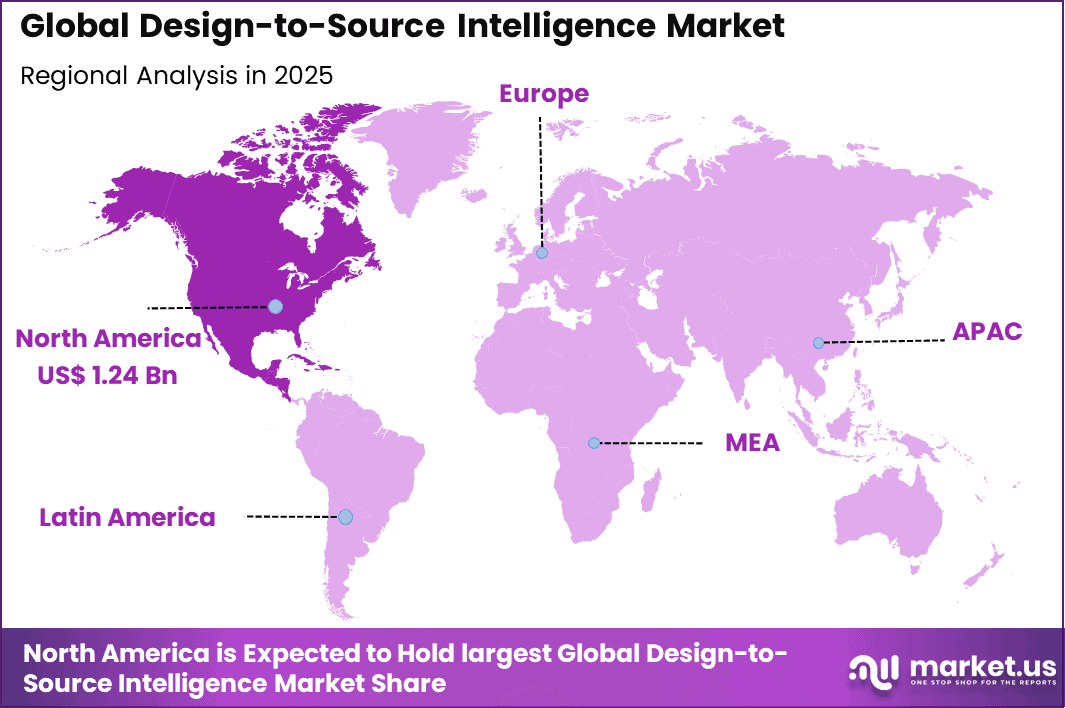

The Global Design-to-Source Intelligence Market generated USD 3.4 billion in 2025 and is predicted to register growth from USD 4 billion in 2026 to about USD 15.3 billion by 2035, recording a CAGR of 16.20% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 36.5% share, holding USD 1.24 Billion revenue.

Design-to-Source Intelligence refers to a structured approach where sourcing and supply chain insights are embedded directly into the product design process at an early stage of development. This process enables organizations to link design specifications with real-time supplier data, cost benchmarks, material availability, and compliance requirements for more informed decision-making.

It incorporates advanced analytics, artificial intelligence, and data from supplier networks to support sourcing decisions before mass production, which can reduce time-to-market and mitigate downstream risks. The market comprises software platforms, analytics tools, and support services designed to integrate design and procurement workflows and improve sourcing efficiency.

One of the primary drivers of the Design-to-Source Intelligence Market is the rising complexity of product design coupled with global multi-tier supply chains that include thousands of components from diverse suppliers. This complexity increases sourcing risks, cost pressures, and cycle times, prompting organizations to embed sourcing intelligence early in the design process.

By accessing real-time supplier data and comparative cost information, engineers and procurement teams can make decisions that support cost containment and supply resilience. The integration of design tools with supplier intelligence supports cross-functional collaboration and improved operational outcomes.

Top Market Takeaways

- By component, software platforms account for 65.0% of the market, combining design data, supplier intelligence, and AI-driven cost modeling in unified environments.

- By deployment mode, cloud-based solutions represent 60.0%, enabling scalable integration with ERP/PLM systems and real-time supply chain visibility.

- By enterprise type, large enterprises hold 64.0% share, leveraging platforms for global sourcing complexity and early-stage cost optimization.

- By application, sourcing and procurement intelligence captures 42.5%, delivering supplier benchmarking, component availability, and risk assessment during design.

- By industry vertical, electronics and semiconductors command 30.0%, addressing rapid cycles, chip shortages, and precision component sourcing.

- By solution type, should-cost and cost breakdown analytics represent 34.0%, providing granular pricing transparency and teardown-based cost validation.

- By enterprise function, procurement and strategic sourcing lead with 38.0%, embedding intelligence to shorten cycles and improve TCO.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Increasing supply chain disruptions requiring proactive sourcing intelligence +4.2% North America, Europe Short to medium term Rising adoption of digital procurement and supplier analytics platforms +3.6% Global Medium term Growing complexity in global component sourcing and compliance tracking +3.2% Asia Pacific, North America Medium term Expansion of AI-driven cost modeling and design optimization tools +2.9% Global Medium term Focus on sustainability and responsible sourcing transparency +2.5% Europe, North America Medium to long term Restraints Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High implementation costs for integrated sourcing intelligence systems -3.1% Emerging Markets Short to medium term Integration challenges with legacy ERP and PLM platforms -2.7% North America, Europe Medium term Data inconsistency across supplier networks- 2.3% Global Medium term Limited adoption among small and mid-sized manufacturers -2.0% Asia Pacific, Latin America Medium term Cybersecurity and supplier data confidentiality concerns -1.8% Global Medium to long term By Component

Software platforms dominate with 65.0% as enterprises prioritize integrated analytics environments over standalone tools. These platforms centralize design specifications, supplier data, and cost models within unified dashboards. This structured approach supports faster evaluation of sourcing alternatives and product cost scenarios.

Advanced platforms provide real time collaboration between engineering and procurement teams. Changes in design parameters can immediately reflect in cost forecasts and supplier impact assessments. This dynamic capability reduces delays and improves transparency.

Scalability is another advantage of software centric solutions. Enterprises can expand analytics coverage across multiple product lines and supplier networks. Continuous updates and integration with enterprise systems enhance operational efficiency.

By Deployment Mode

Cloud based deployment accounts for 60.0% due to demand for scalable and accessible analytics infrastructure. Cloud platforms enable distributed teams to collaborate across regions without hardware limitations. This is particularly valuable for multinational manufacturing organizations.

Cloud environments also support continuous updates and integration with supplier databases. Procurement teams can access benchmarking data and cost libraries in real time. This flexibility improves responsiveness to market fluctuations.

Security and compliance frameworks within enterprise cloud systems have strengthened adoption confidence. Organizations increasingly recognize that structured cloud governance can meet internal control requirements while supporting global accessibility.

By Enterprise Type

Large enterprises represent 64.0% of market adoption because they manage extensive supplier ecosystems and complex product portfolios. These organizations require detailed cost visibility across multiple tiers of suppliers.

Design to source intelligence platforms provide structured analytics for such large scale operations. Financial resources and digital transformation initiatives further support adoption in large corporations. Implementation often involves integration with enterprise resource planning and product lifecycle management systems.

Larger enterprises are better positioned to invest in these integrated environments. However, mid sized enterprises are gradually recognizing the value of cost transparency. As supply chains become more competitive, structured analytics tools are expanding beyond large organizations.

By Application

Sourcing and procurement intelligence leads with 42.5% because cost optimization remains a strategic priority. Enterprises use analytics to evaluate supplier performance, pricing structures, and contract terms. This improves negotiation leverage and reduces procurement risk.

Data driven sourcing decisions also strengthen supply chain resilience. Analytics platforms identify alternative suppliers and simulate cost impacts of material substitution. This capability has gained importance amid global supply disruptions.

Integration with spend management systems further enhances application value. Procurement teams can align strategic sourcing objectives with financial performance metrics. This linkage supports measurable return on investment.

By Industry Vertical

Electronics and semiconductors hold 30.0% due to highly complex component structures and rapid product innovation cycles. Cost visibility at the component level is critical in these industries where margins can fluctuate significantly. Design to source intelligence tools provide granular breakdown of materials and manufacturing inputs. Global supplier networks in electronics increase exposure to geopolitical and logistical risks.

Structured analytics helps organizations evaluate sourcing concentration and cost volatility. This strengthens strategic planning. High research and development intensity in semiconductors also drives integration between design and procurement functions. Early stage cost modeling influences product feasibility and pricing strategies.

By Solution Type

Should cost and cost breakdown analytics represent 34.0% as enterprises seek transparency into supplier pricing structures. These tools estimate the expected cost of materials and production processes based on market benchmarks. This provides a reference point during supplier negotiations. Cost breakdown analytics also support internal budgeting and margin planning.

By understanding component level cost drivers, organizations can redesign products to improve profitability. This approach enhances collaboration between engineering and procurement teams. The ability to simulate pricing under different sourcing scenarios further strengthens solution adoption. Enterprises use these insights to mitigate risk and optimize supplier selection strategies.

By Enterprise Function

Procurement and strategic sourcing functions account for 38.0% because these teams directly manage supplier relationships and cost performance. Design to source intelligence platforms provide actionable insights tailored to procurement objectives. This strengthens negotiation outcomes and supplier evaluation processes. Cross functional collaboration is increasing between procurement and product development teams.

Early stage design decisions significantly influence final product cost. Integrated analytics ensures that sourcing considerations are embedded within engineering workflows. Performance measurement frameworks also reinforce adoption within procurement departments. Structured reporting supports accountability and long term supplier optimization initiatives.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Procurement intelligence software providers Very High Medium North America, Europe Strong SaaS scalability Supply chain analytics vendors High Medium Global Platform integration growth Private equity firms Medium Medium North America, Europe Consolidation of mid-sized vendors Venture capital investors High High North America Innovation in AI-driven sourcing tools Strategic manufacturing investors Medium Low to Medium Global Operational efficiency enhancement Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline AI-based supplier risk analytics engines +4.6% Predictive sourcing risk assessment Global Short to medium term Cloud-native procurement intelligence platforms +3.9% Centralized sourcing visibility Global Medium term Real-time component pricing and availability monitoring +3.4% Cost optimization North America, Asia Pacific Medium term Integration with digital twin and product lifecycle systems +2.8% Design optimization alignment Europe, North America Medium to long term ESG and sustainability compliance dashboards +2.4% Responsible sourcing reporting Europe Long term Key Challenges

- Difficulty in integrating sourcing tools with existing product lifecycle and procurement systems

- Limited visibility into real time supplier cost and availability data

- Data inconsistency across engineering, procurement, and finance teams

- High dependency on accurate cost modeling for reliable decision support

- Resistance to process change within traditional sourcing and design functions

Emerging Trends

The Design-to-Source Intelligence market is evolving as procurement and product development teams move toward fully connected digital workflows. A key trend is the integration of engineering design data directly with sourcing platforms, allowing cost visibility at an early stage of product development.

It is estimated that nearly 70% of a product’s total cost is determined during the design phase, which is pushing organizations to embed supplier intelligence and cost modeling tools within CAD and PLM environments.

Another visible shift is the use of advanced analytics and AI based insights to assess supplier risk, material availability, and compliance requirements in real time. This integration is helping companies reduce design revisions, shorten sourcing cycles, and improve cross functional collaboration between engineering and procurement teams.

Growth Factors

Market growth is being driven by increasing pressure on manufacturers to control input costs and manage supply chain volatility. Frequent disruptions in global sourcing networks have highlighted the need for early supplier visibility and alternative component analysis during product design. The adoption of digital twins, automated bill of materials analysis, and predictive cost estimation tools is improving sourcing accuracy and reducing manual effort.

In addition, regulatory compliance and sustainability requirements are encouraging companies to evaluate material origin and supplier practices at the design stage. As organizations aim to improve margin control and reduce time to market, investment in design linked sourcing intelligence platforms is expected to strengthen steadily.

Key Market Segments

By Component

- Software Platforms

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Enterprise Type

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Application

- Product Data Intelligence

- Design Optimization

- Sourcing and Procurement Intelligence

- Supply Chain Risk Management

- Cost and Compliance Management

- Others

By Industry Vertical

- Electronics and Semiconductors

- Automotive and Mobility

- Aerospace and Defense

- Industrial Equipment

- Medical Devices and IoT

- Others (Telecommunication, etc.)

By Solution Type

- Should-Cost and Cost Breakdown Analytics

- Risk, Compliance and ESG Intelligence

- Supplier Discovery and Market Intelligence

- Bill of Materials Optimization

- Others

By Enterprise Function

- Procurement and Strategic Sourcing

- Engineering and Product Design

- Sustainability and ESG Teams

- Supply Chain Management

- Others

Regional Analysis

North America accounts for 36.5% of the design-to-source intelligence market, supported by strong presence of electronics, automotive, and industrial manufacturing sectors. Enterprises in the region are adopting design-to-source platforms to improve cost visibility, supplier collaboration, and component risk assessment during early product development stages. Demand is driven by increasing supply chain complexity, need for should-cost analysis, and pressure to reduce time-to-market while maintaining margin control.

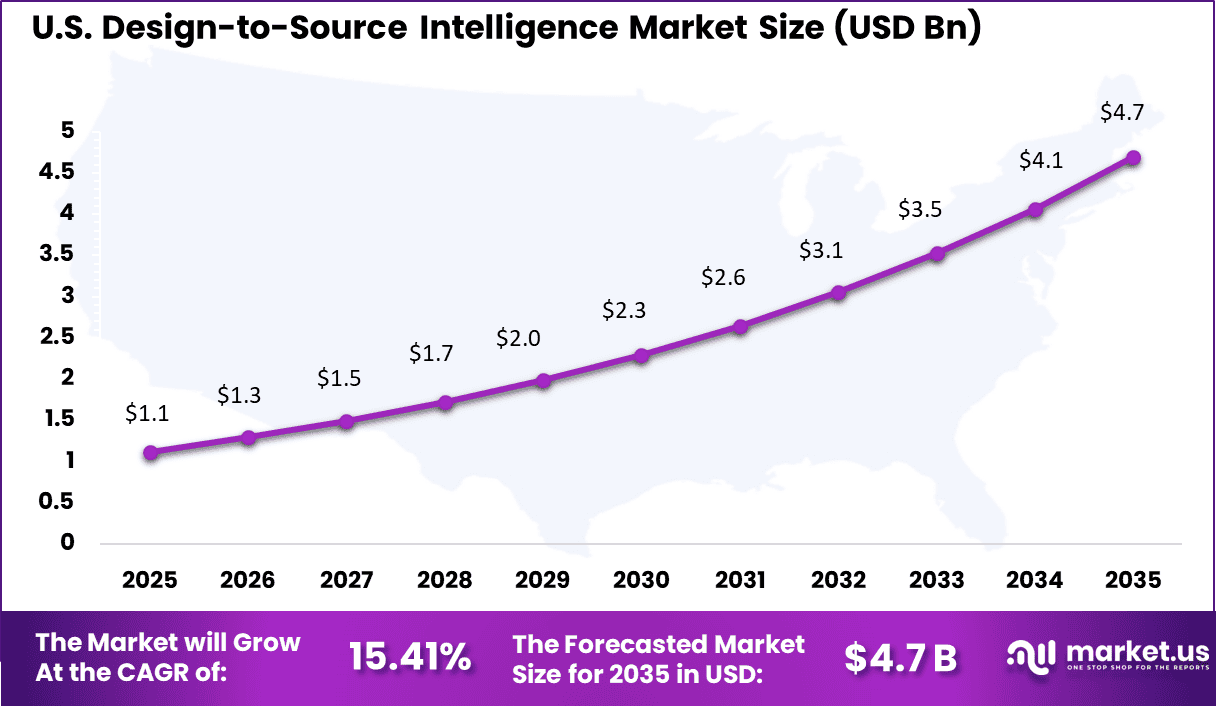

The United States market is valued at USD 1.12 Bn and is growing at a CAGR of 15.41%, reflecting accelerated integration of procurement intelligence within product design workflows. Adoption is influenced by rising focus on supply risk mitigation, real-time component pricing visibility, and cross-functional collaboration between engineering and sourcing teams. Growth is further supported by digital transformation initiatives across manufacturing enterprises and increasing reliance on data-driven sourcing strategies to enhance competitiveness and operational resilience.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The Design to Source Intelligence market is led by procurement and supply chain technology providers such as Supplyframe under Siemens, JAGGAER, Ivalua, Coupa Software, SAP SE, Samsung SDS, and HCL Technologies.

These companies compete on end to end sourcing visibility, supplier risk monitoring, and integration with enterprise resource planning and procurement systems. Their platforms are widely adopted by large manufacturers and electronics companies that require component level cost insight, supplier availability data, and compliance tracking during product design.

Specialized and mid sized providers including Luminovo, Source Intelligence, Zensar Technologies, Edited, ITMAGINATION, Linagora, IndSpec, TradeEdge, and others compete through focused analytics and flexible deployment.

Competition in this segment is driven by real time component intelligence, alternative part identification, and faster supplier evaluation. These vendors are often selected by companies seeking practical design stage sourcing insights and improved resilience across global supply chains.

Top Key Players in the Market

- Supplyframe (a Siemens company)

- Luminovo GmbH

- JAGGAER

- Ivalua

- Source Intelligence

- HCL Technologies Limited

- Zensar Technologies

- Edited

- ITMAGINATION

- Linagora

- IndSpec

- TradeEdge

- Samsung SDS

- Coupa Software Inc.

- SAP SE

- Others

Future Outlook

The future outlook for the Design-to-Source Intelligence Market is positive as companies increasingly seek smarter ways to link product design with sourcing decisions. Demand for design-to-source intelligence solutions is expected to grow because these tools help teams find the best suppliers, reduce costs, and speed up development.

Adoption of data analytics, automation, and real-time insights will improve decision making and collaboration across design and procurement. Growth can be attributed to rising focus on supply chain efficiency, cost management, and faster product innovation. Overall, the market is expected to expand as organizations prioritize connected and intelligent sourcing processes.

Recent Developments

- January, 2026, Luminovo rolled out ElectronicsGPT, the first AI agent tailored for electronics procurement, making sourcing faster and more precise for buyers.

- December, 2025, JAGGAER snapped up DocSkiff to supercharge its AI-driven contract tools, helping procurement teams handle autonomous commerce more smoothly.

Report Scope

Report Features Description Market Value (2025) USD 3.4 Billion Forecast Revenue (2035) USD 15.3 Billion CAGR(2025-2035) 16.20% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software Platforms, Services), By Deployment Mode (Cloud-based, On-premises), By Enterprise Type (Large Enterprises, Small and Medium-sized Enterprises), By Application (Product Data Intelligence, Design Optimization, Others), By Industry Vertical (Electronics and Semiconductors, Automotive and Mobility, Others (Telecommunication, etc.)), By Solution Type (Should-Cost and Cost Breakdown Analytics, Others), By Enterprise Function (Procurement and Strategic Sourcing, Engineering and Product Design, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Supplyframe (a Siemens company), Luminovo GmbH, JAGGAER, Ivalua, Source Intelligence, HCL Technologies Limited, Zensar Technologies, Edited, ITMAGINATION, Linagora, IndSpec, TradeEdge, Samsung SDS, Coupa Software Inc., SAP SE, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Design-to-Source Intelligence MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Design-to-Source Intelligence MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Supplyframe (a Siemens company)

- Luminovo GmbH

- JAGGAER

- Ivalua

- Source Intelligence

- HCL Technologies Limited

- Zensar Technologies

- Edited

- ITMAGINATION

- Linagora

- IndSpec

- TradeEdge

- Samsung SDS

- Coupa Software Inc.

- SAP SE

- Others

Our Clients

- 178740

- Feb. 2026