Quick Navigation

Market Overview

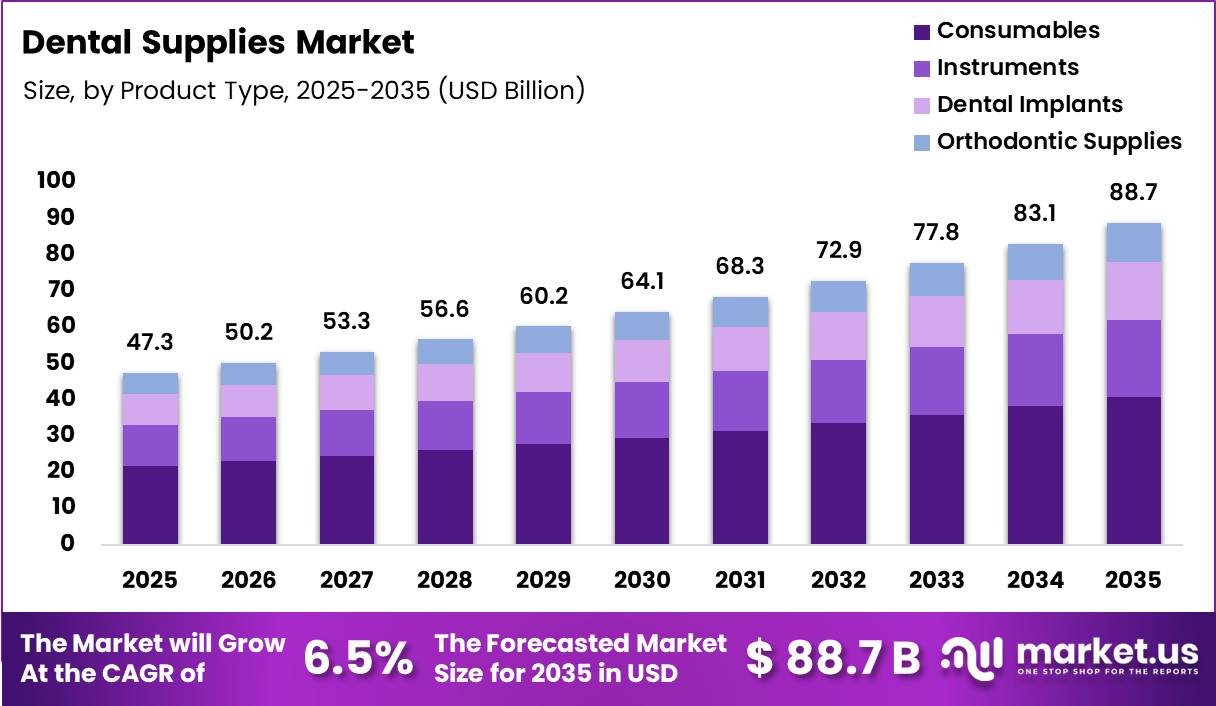

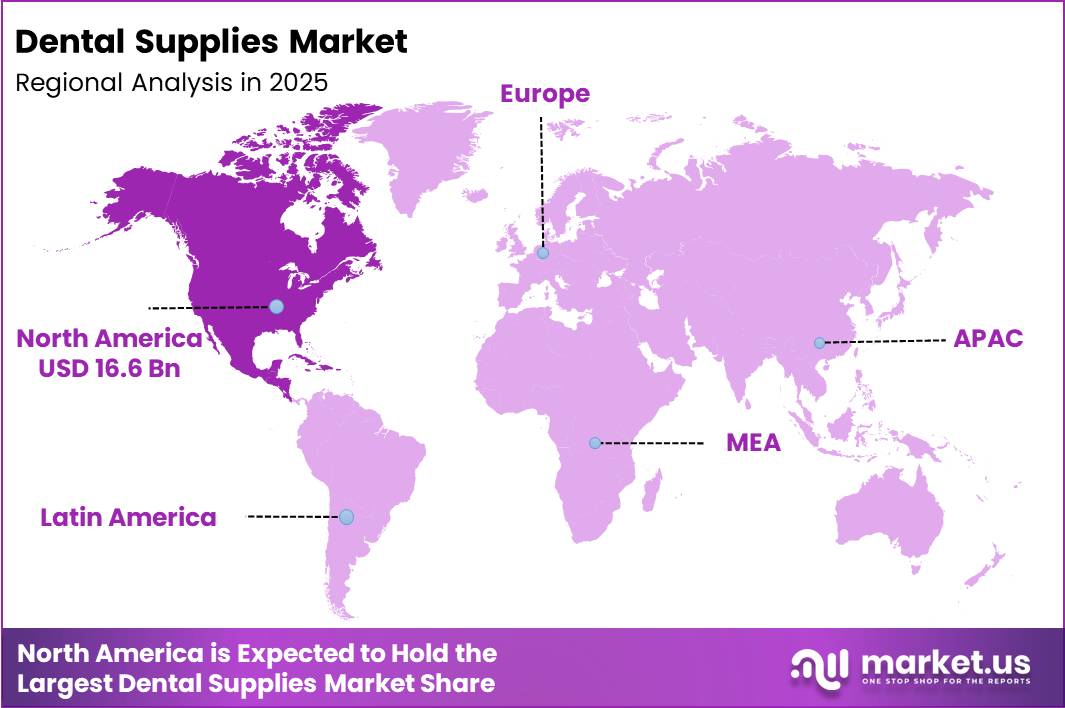

Global Dental Supplies Market size is expected to be worth around US$ 88.7 Billion by 2035 from US$ 47.3 Billion in 2025, growing at a CAGR of 6.5% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 35.0% share with a revenue of US$ 16.6 Billion.

The dental supplies market plays a vital role in supporting preventive, restorative, orthodontic, endodontic, and surgical dental procedures worldwide. The market includes a broad range of products such as dental consumables, instruments, implants, impression materials, infection control products, and digital dentistry equipment used across hospitals, dental clinics, and laboratories.

Rising awareness of oral hygiene, increasing demand for cosmetic dentistry, and the growing adoption of advanced dental technologies are strengthening demand for high-quality dental supplies across both developed and emerging healthcare systems.

According to the World Health Organization (WHO), oral diseases affect approximately 3.5 billion people globally, making them among the most common noncommunicable diseases worldwide. Untreated dental caries in permanent teeth impacts around 2.5 billion people, while severe periodontal disease affects nearly 1 billion people.

WHO also estimates that more than 380,000 new cases of oral cancer occur annually, highlighting the growing need for effective dental diagnosis and treatment solutions. In the United States, the Centers for Disease Control and Prevention (CDC) reports that 50% of children have experienced cavities by age 9, while 21% of adults aged 20–64 have at least one untreated cavity.

Furthermore, untreated dental disease contributes to the loss of approximately 34 million school hours and more than US$45 billion in productivity each year in the U.S. These public health statistics continue to encourage governments, healthcare providers, and dental professionals to expand preventive care services and invest in advanced dental supplies, supporting long-term growth across the global dental industry.

Key Takeaways

- Market Size: Global Dental Supplies Market size is expected to be worth around US$ 88.7 Billion by 2035 from US$ 47.3 Billion in 2025

- Market Share: The market is growing at a CAGR of 6.5% during the forecast period from 2026 to 2035.

- Product Type: Consumables dominated the dental supplies market with a 46.0% market share in 2025, maintaining the largest revenue contribution among all product categories.

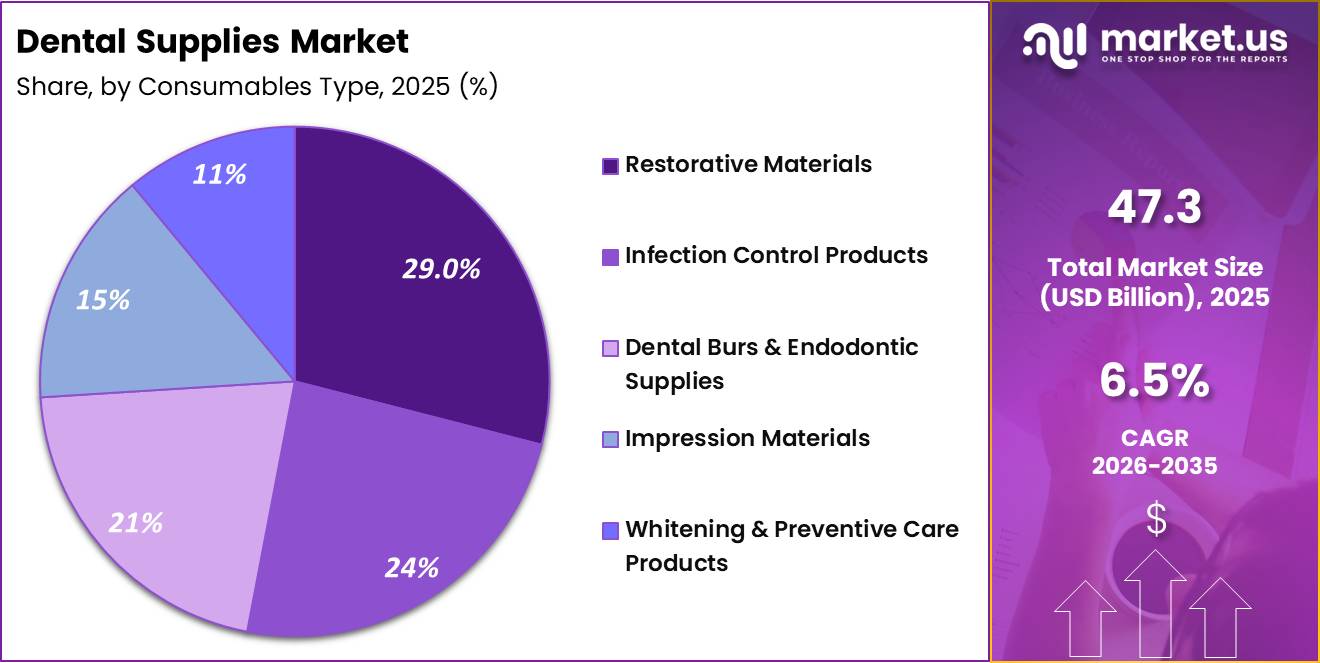

- Consumables Type: Restorative Materials accounted for the largest share of the consumables segment, representing 29.0% of the market in 2025.

- Application: General Dentistry dominated the dental supplies market with a 41.0% market share in 2025, reinforcing its position as the largest application segment.

- End User: Dental Clinics dominated the dental supplies market, capturing 64.0% of the total market share in 2025.

- Distribution Channel: Direct Sales led the dental supplies market with a 52.0% share in 2025.

- Regional: In 2025, North America led the market, achieving over 35.0% share with a revenue of US$ 16.6 Billion.

Product Type Analysis

The Consumables segment dominated the dental supplies market in 2025, accounting for 46.0% of the total market share. Its leadership is driven by the recurring demand for products used in routine dental procedures, including restorative materials, impression products, infection control items, cements, and preventive care solutions.

Unlike capital equipment, consumables require frequent replenishment, making them an essential and continuous revenue source for dental practices. The growing volume of restorative, cosmetic, and preventive dental treatments, combined with rising patient awareness of oral health, has significantly increased the consumption of disposable and single-use dental products.

Technological advancements in biocompatible materials and aesthetic restorations have further strengthened the adoption of premium consumables. Companies such as 3M Oral Care, GC Corporation, and Kuraray Noritake Dental Inc. continue to expand their restorative and preventive product portfolios, supporting sustained market growth.

The Instruments segment held 24.0% of the market in 2025, supported by the increasing adoption of precision handpieces, diagnostic tools, and surgical instruments across dental clinics. Dental Implants accounted for 18.0%, benefiting from the rising popularity of implant-supported restorations and improved implant technologies offered by companies such as Straumann Group and Osstem Implant Co., Ltd.

Meanwhile, Orthodontic Supplies represented 12.0% of the market and continue to witness healthy growth due to increasing demand for clear aligners, aesthetic braces, and digital orthodontic workflows led by innovators including Align Technology Inc.

Consumables Type Analysis

Among consumable categories, Restorative Materials dominated the market with a 29.0% share in 2025. Their leading position is attributed to the growing number of dental fillings, crowns, bridges, veneers, and cosmetic restoration procedures performed globally.

Increasing patient preference for tooth-colored, durable, and minimally invasive restorations has accelerated demand for advanced composite resins, glass ionomers, bonding agents, and ceramic materials. Continuous innovations in adhesive technologies and high-strength restorative materials have further enhanced clinical outcomes while reducing treatment time.

Manufacturers such as Ivoclar Vivadent AG, GC Corporation, and Voco GmbH continue to introduce advanced restorative solutions that improve aesthetics, durability, and ease of application, reinforcing the segment’s market leadership.

Infection Control Products accounted for 24.0% of the market, driven by stringent sterilization protocols and increasing emphasis on patient safety within dental facilities. Dental Burs & Endodontic Supplies represented 21.0%, supported by the growing volume of root canal procedures and restorative treatments requiring precision instrumentation.

Impression Materials captured 15.0% of market share and continue to benefit from the shift toward digital dentistry and high-accuracy restorative workflows. Meanwhile, Whitening & Preventive Care Products held 11.0% and are experiencing steady expansion as cosmetic dentistry, preventive oral healthcare, and at-home whitening solutions gain wider consumer acceptance worldwide.

Application Analysis

General Dentistry emerged as the largest application segment, capturing 41.0% of the dental supplies market in 2025. The segment dominates because routine dental examinations, preventive care, fillings, extractions, and basic restorative procedures account for the highest volume of treatments performed globally. Rising awareness of oral hygiene, expanding access to dental care, and increasing government initiatives promoting preventive oral health continue to drive patient visits to dental clinics.

The widespread use of consumables, instruments, and diagnostic products in everyday clinical practice further strengthens the segment’s leadership. Companies including Dentsply Sirona, Henry Schein Inc., and Patterson Companies Inc. support this segment through comprehensive product portfolios that address routine dental procedures and practice efficiency.

Implant Dentistry represents one of the fastest-growing application areas, fueled by increasing tooth loss among aging populations and growing demand for permanent tooth replacement solutions. Orthodontics is also expanding steadily with rising adoption of clear aligners, digital treatment planning, and aesthetic orthodontic therapies, particularly among adults.

Periodontics continues to gain importance as awareness of gum disease and its relationship with overall health increases, driving demand for specialized periodontal treatments. Restorative Dentistry is also witnessing consistent growth due to increasing cosmetic dental procedures and the growing preference for durable, natural-looking restorative materials across both developed and emerging healthcare markets.

End User Analysis

Dental Clinics dominated the dental supplies market in 2025, accounting for 64.0% of total market revenue. Their leadership is primarily driven by the high volume of routine dental consultations, restorative treatments, cosmetic procedures, orthodontic services, and preventive care performed in private and group practices.

The expansion of independent clinics, increasing dental insurance coverage in several countries, and growing patient preference for specialized outpatient treatment continue to boost procurement of consumables, instruments, and digital dental technologies.

Clinics also frequently replace disposable products and adopt advanced treatment solutions to improve efficiency and patient outcomes. Companies such as Henry Schein Inc., Patterson Companies Inc., and Dentsply Sirona maintain strong distribution networks that effectively serve this large customer base.

Hospitals remain an important end-user segment, particularly for complex oral surgeries, trauma management, and multidisciplinary healthcare services. Dental Laboratories continue to experience healthy growth as digital workflows, CAD/CAM technologies, and customized prosthetics increase demand for laboratory materials and equipment.

Meanwhile, Academic & Research Institutes are steadily expanding their procurement of advanced dental products to support clinical education, simulation-based learning, and research focused on innovative biomaterials, implant technologies, and digital dentistry, contributing to long-term technological advancements across the dental industry.

Distribution Channel Analysis

The Direct Sales channel led the dental supplies market in 2025 with a 52.0% market share. The dominance of direct sales is attributed to strong relationships between manufacturers and dental clinics, hospitals, and laboratory chains requiring technical support, product training, customized purchasing agreements, and after-sales services.

Direct engagement enables manufacturers to introduce new technologies efficiently while providing clinical demonstrations, maintenance services, and flexible procurement options for high-value dental products. This distribution model is particularly preferred for premium equipment, implant systems, and digital dentistry solutions. Leading companies including Dentsply Sirona, Straumann Group, and Planmeca Oy continue to strengthen their direct commercial networks to improve customer engagement and enhance product adoption.

Dental Distributors accounted for 34.0% of the market by offering broad product portfolios, efficient inventory management, and convenient access to supplies for small and medium-sized dental practices. Their established logistics infrastructure remains essential for serving geographically diverse healthcare providers.

E-Commerce & Online Procurement also represented 34.0% of the market and is rapidly gaining traction due to digital purchasing platforms, competitive pricing, faster product comparisons, and streamlined ordering processes. Increasing digitalization of procurement workflows and growing acceptance of online purchasing among dental professionals are expected to further strengthen this channel over the coming years.

Key Market Analysis

Product Type

- Consumables

- Instruments

- Dental Implants

- Orthodontic Supplies

Consumables Type

- Restorative Materials

- Infection Control Products

- Dental Burs & Endodontic Supplies

- Impression Materials

- Whitening & Preventive Care Products

Application

- General Dentistry

- Restorative Dentistry

- Implant Dentistry

- Orthodontics

- Periodontics

End User

- Dental Clinics

- Hospitals

- Dental Laboratories

- Academic & Research Institutes

Distribution Channel

- Direct Sales

- Dental Distributors

- E-Commerce & Online Procurement

Opportunity

Connected digital consumables represent an emerging opportunity as digital dentistry evolves beyond standalone hardware into integrated workflow ecosystems. The FDI digital dentistry policy emphasizes user-friendly technologies, secure data handling, and standards for quality, safety, and interoperability, supporting the shift toward connected digital workflows.

The opportunity lies in transforming products such as scan sleeves, aligner materials, bonding kits, milling blanks, print resins, sterilization supplies, and shade accessories into digitally connected consumables.

These products can incorporate features such as usage analytics, automated replenishment alerts, case-linked traceability, and device-compatibility tracking. Unlike traditional consumables sold as individual SKUs, connected products can provide ongoing workflow visibility and inventory management benefits.

This can help reduce stockouts, improve material traceability, and lower remake risks. By linking consumables with software platforms and clinical workflows, suppliers can strengthen customer retention and create recurring service-based revenue streams alongside product sales.

| Opportunity | Geographic Relevance | Execution Window |

|---|---|---|

| Primary-care supply formularies | APAC emerging, Africa, LATAM, public EU systems | Medium term (2-4 years) |

| Connected digital consumables | North America, EU, Japan, Korea, urban APAC | Medium term (2-4 years) |

| Prevention-led community packs | India, SEA, Africa, LATAM, Middle East | Long term (≥ 4 years) |

| Aging-care oral maintenance kits | Japan, EU, North America, Korea | Medium term (2-4 years) |

| Data-linked implant supply systems | North America, EU, advanced APAC | Long term (≥ 4 years) |

| Low-cost rural access bundles | South Asia, Africa, LATAM, rural West | Short term (≤ 2 years) |

Driving Factors

Prevention program consumables are a major driver for the dental supplies market because the benefits of cavity prevention are supported by clear clinical and economic outcomes. According to CDC data, properly applied dental sealants can prevent up to 80% of cavities during the first 2 years and continue to prevent about 50% of cavities for up to 4 years.

School-based sealant programs are also considered cost-effective, with each sealed tooth saving more than $11 in future dental treatment costs. These measurable outcomes support ongoing demand for sealant materials, fluoride varnishes, etchants, applicators, and curing-light accessories. The evidence-based nature of preventive care makes these products attractive for public-health programs and institutional procurement.

Demand is particularly strong in school oral-health initiatives and programs targeting underserved populations. As a result, preventive consumables are helping shift dental spending toward recurring, prevention-focused purchasing rather than treatment-driven demand alone.

| Opportunity | Geographic Relevance | Execution Window |

|---|---|---|

| Primary-care supply formularies | APAC emerging, Africa, LATAM, public EU systems | Medium term (2-4 years) |

| Connected digital consumables | North America, EU, Japan, Korea, urban APAC | Medium term (2-4 years) |

| Prevention-led community packs | India, SEA, Africa, LATAM, Middle East | Long term (≥ 4 years) |

| Aging-care oral maintenance kits | Japan, EU, North America, Korea | Medium term (2-4 years) |

| Data-linked implant supply systems | North America, EU, advanced APAC | Long term (≥ 4 years) |

| Low-cost rural access bundles | South Asia, Africa, LATAM, rural West | Short term (≤ 2 years) |

Challenges

Digital interoperability gaps remain a significant challenge as dental supplies become increasingly integrated with digital workflows and connected clinical systems. The FDI digital dentistry policy emphasizes the need for robust data-security governance, interoperability, sustainability, and standards that ensure quality, safety, and applicability across digital dental technologies.

Products such as scanner sleeves, print materials, implant components, guided-surgery consumables, bonding systems, and restorative materials increasingly depend on seamless integration with scanners, software platforms, and manufacturing equipment.

In many cases, the effectiveness of these products is influenced by how well files, device settings, scan data, implant libraries, and case records transfer between different vendors’ systems. Compatibility issues can increase customer-support requirements and create workflow inefficiencies for dental practices and laboratories.

They may also limit adoption of otherwise clinically effective products if integration challenges disrupt daily operations. As a result, product success increasingly depends not only on material performance but also on compatibility within broader digital dentistry ecosystems.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Primary-care supply integration | +2.5% | APAC, Africa, LATAM, public EU systems | Long term (≥ 4 years) |

| Prevention program consumables | +2.2% | North America, EU, India, SEA, LATAM | Medium term (2-4 years) |

| Digital workflow-linked supplies | +1.9% | North America, EU, Japan, Korea, urban APAC | Medium term (2-4 years) |

| EHR-linked clinical traceability | +1.6% | North America, EU, regulated APAC | Long term (≥ 4 years) |

| Essential medicines and prep access | +1.5% | Emerging markets, GCC, public systems | Medium term (2-4 years) |

| Rural and school outreach demand | +1.4% | South Asia, Africa, LATAM, rural West | Short term (≤ 2 years) |

Restraining Factors

High out-of-pocket dependence is a major restraint for the dental supplies market because access to oral healthcare remains heavily dependent on patients’ ability to pay. WHO notes that prevention and treatment of oral diseases are often expensive and are frequently excluded from national universal health coverage benefit packages. The organization also identifies oral healthcare costs as a leading contributor to catastrophic health expenditure for many households.

In numerous low- and middle-income countries, access to preventive and treatment services remains insufficient despite a high burden of oral disease. These financing limitations directly affect demand for dental supplies, as clinics and patients often prioritize lower-cost alternatives or defer treatment altogether.

Budget constraints can reduce purchases of preventive materials, infection-control products, and other adjunctive consumables. As a result, market growth is often limited by affordability and reimbursement challenges rather than by a lack of clinical need, particularly in high-burden regions.

| Restraint | Geographic Relevance | Impact Timeline |

|---|---|---|

| High out-of-pocket dependence | Emerging markets, U.S. private-pay segments, underserved regions | Long term (≥ 4 years) |

| Slow primary-care integration | APAC emerging, Africa, LATAM, public systems | Medium term (2-4 years) |

| Digital ecosystem fragmentation | North America, EU, Japan, Korea, urban APAC | Long term (≥ 4 years) |

| Uneven outreach conversion | Rural and school-based channels globally | Medium term (2-4 years) |

| Workforce distribution imbalance | South Asia, Africa, LATAM, rural West | Long term (≥ 4 years) |

| Prevention budget variability | North America, EU, public health systems | Short term (≤ 2 years) |

Regional Analysis

North America dominated the global Dental Supplies Market

North America dominated the global Dental Supplies Market in 2025, accounting for over 35.0% of the total market and generating approximately US$ 16.6 billion in revenue. The region’s leadership is supported by a highly developed dental healthcare infrastructure, widespread adoption of advanced dental technologies, and strong awareness of preventive oral care.

High dental expenditure, favorable reimbursement for selected dental procedures, and the presence of a large number of private dental clinics continue to drive demand for restorative, orthodontic, implant, and diagnostic dental supplies. In addition, the region benefits from continuous product innovation, digital dentistry adoption, and the strong presence of leading manufacturers, enabling faster commercialization of advanced dental materials and equipment.

The United States remains the primary contributor to regional growth due to its extensive network of dental professionals, increasing cosmetic dentistry procedures, and growing utilization of CAD/CAM systems, intraoral scanners, and 3D printing technologies in clinical practice. Canada also contributes steadily through expanding access to oral healthcare services and supportive public health initiatives aimed at improving dental care accessibility.

Meanwhile, the Asia Pacific region is projected to witness the fastest growth during the forecast period, driven by rising disposable incomes, expanding dental tourism, increasing awareness of oral hygiene, and rapid investments in healthcare infrastructure across countries such as China and India. Europe continues to maintain a significant market position owing to its well-established dental care systems, aging population, and ongoing demand for advanced dental treatment solutions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Dental Supplies Market is moderately fragmented, with global and regional manufacturers competing through broad product portfolios, continuous innovation, and integrated digital solutions. Leading players such as Dentsply Sirona, Straumann Group, Envista Holdings Corporation, Henry Schein Inc., and Align Technology Inc. are strengthening their market positions by expanding offerings across restorative materials, implants, orthodontics, digital imaging, and clinical equipment.

Competition is increasingly shaped by technological advancements, clinician training programs, and the ability to deliver complete dental workflows that improve efficiency and treatment outcomes. As digital dentistry continues to evolve, manufacturers are focusing on solutions that connect diagnostics, treatment planning, restorative design, and patient management into a unified ecosystem.

Competitive strategies are centered on sustained investments in research and development, strategic partnerships, and product innovation to address the growing demand for minimally invasive and digitally enabled dental procedures.

Companies are introducing advanced biomaterials, AI-assisted imaging systems, CAD/CAM restorations, intraoral scanners, and digital implant planning platforms to enhance clinical precision and productivity. Partnerships with dental laboratories, software developers, distributors, and educational institutions help expand market reach while accelerating technology adoption.

Many leading players are also emphasizing workflow integration by combining hardware, software, consumables, and service support into comprehensive treatment ecosystems. This ecosystem-based approach strengthens customer loyalty, simplifies practice operations, and enables manufacturers to differentiate themselves in an increasingly competitive global dental supplies market.

Top Key Players

- Dentsply Sirona

- Straumann Group

- Envista Holdings Corporation

- Henry Schein Inc.

- Patterson Companies Inc.

- 3M Oral Care

- Ivoclar Vivadent AG

- GC Corporation

- Align Technology Inc.

- Coltene Holding AG

- Planmeca Oy

- Osstem Implant Co., Ltd.

- Kuraray Noritake Dental Inc.

- Shofu Inc.

- Voco GmbH

Recent Developments

- In January 2025, Henry Schein, Inc. (Nasdaq: HSIC) completed the acquisition of substantially all assets of Acentus, a prominent national homecare medical products supplier based in Tampa, Florida. The transaction followed the initial definitive agreement announced by both companies on November 20, 2024.

- In January 2026, Dentsply Sirona renewed its U.S. dental technology distribution partnership with Patterson Companies Inc. The agreement aims to expand access to integrated digital dental technologies and strengthen product availability for dental professionals across the United States.

- In June 2025, Straumann Group announced a major investment to expand its Villeret manufacturing site in Switzerland over the next five years. The expansion will support higher production capacity for advanced implant systems, including the recently introduced iEXCEL implant platform, to meet growing global demand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 47.3 Billion |

| Forecast Revenue (2035) | US$ 88.7 Billiom |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Consumables, Instruments, Dental Implants, Orthodontic Supplies), By Consumables Type (Restorative Materials, Infection Control Products, Dental Burs & Endodontic Supplies, Impression Materials, Whitening & Preventive Care Products), By Application (General Dentistry, Restorative Dentistry, Implant Dentistry, Orthodontics, Periodontics), By End User (Dental Clinics, Hospitals, Dental Laboratories, Academic & Research Institutes), By Distribution Channel (Direct Sales, Dental Distributors, E-Commerce & Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Straumann Group, Envista Holdings Corporation, Henry Schein Inc., Patterson Companies Inc., 3M Oral Care, Ivoclar Vivadent AG, GC Corporation, Align Technology Inc., Coltene Holding AG, Planmeca Oy, Osstem Implant Co., Ltd., Kuraray Noritake Dental Inc., Shofu Inc., Voco GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |