Quick Navigation

Market Overview

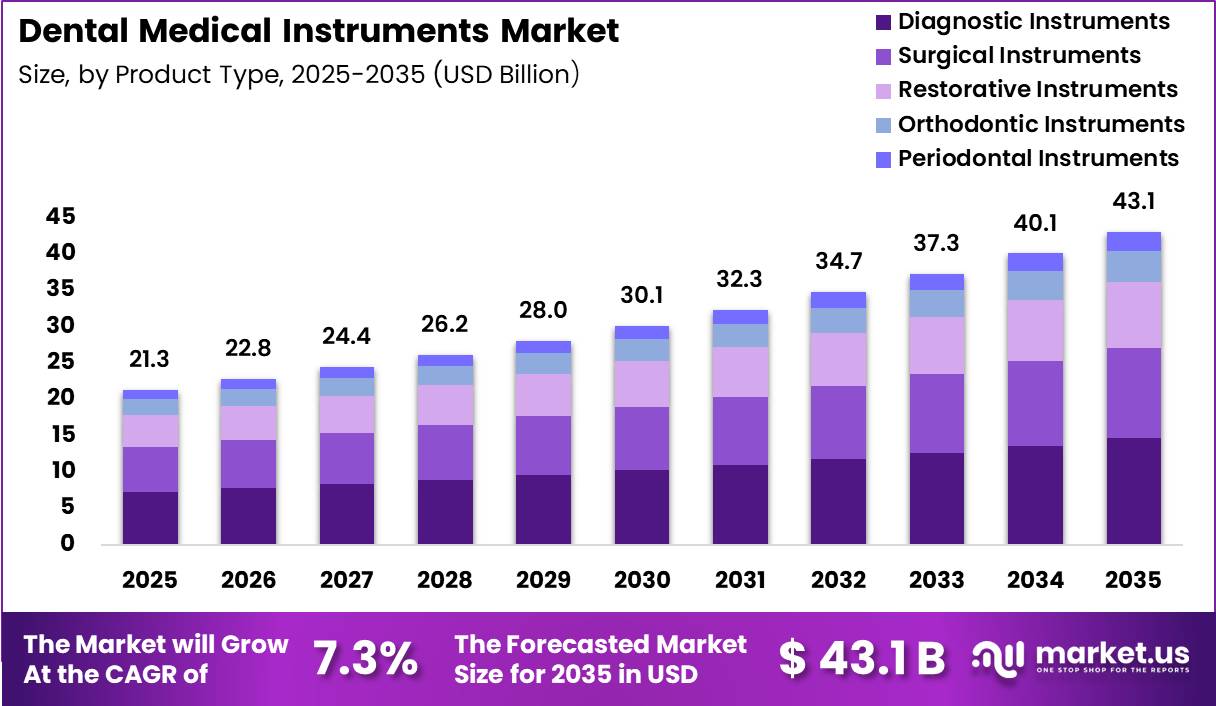

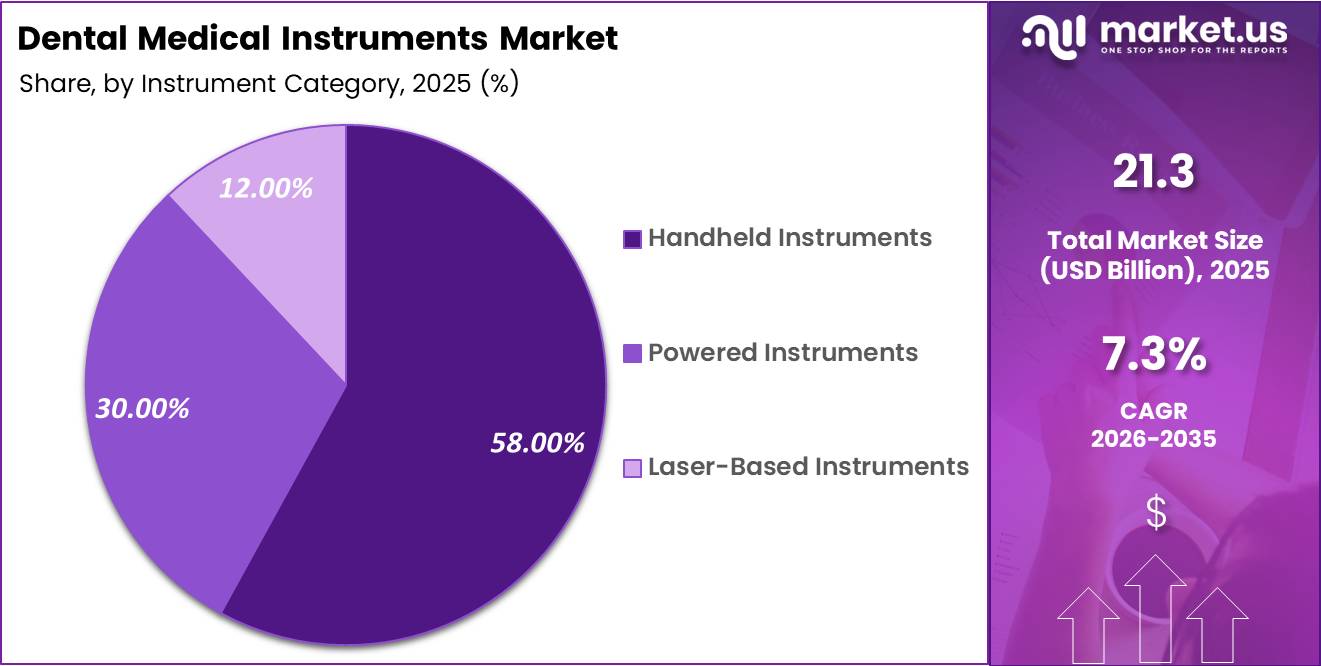

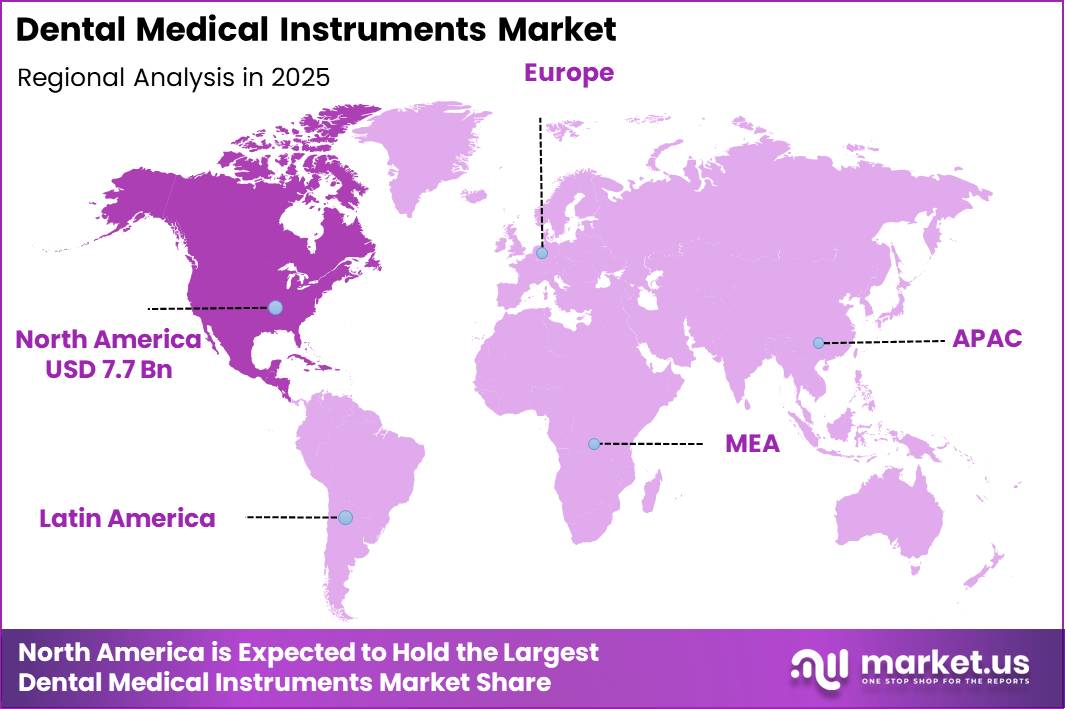

Global Dental Medical Instruments Market size is expected to be worth around US$ 43.1 Billion by 2035 from US$ 21.3 Billion in 2025, growing at a CAGR of 7.30% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 36.00% share with a revenue of US$ 7.7 Billion.

The global dental medical instruments sector is a critical segment of health technology, supporting the prevention, diagnosis, and treatment of oral conditions worldwide. According to the World Health Organisation, there are an estimated 2 million different types of medical devices in use globally, including instruments used daily by dentists for examinations, restorative procedures, and oral surgery.

Dental medical instruments encompass hand tools, diagnostic devices, surgical implements, and hygiene instruments that enable clinicians to deliver comprehensive dental care. In England alone, official NHS dental statistics for 2024/25 report 35 million courses of dental treatment delivered, with 18 million adults and 6.9 million children seen by NHS dental services over 12 months, underscoring the high procedural volume that drives instrument utilisation.

These instruments are essential in both routine check-ups and advanced procedures such as periodontal therapy, endodontics, and implant surgeries. Adoption levels correlate with overall dental treatment activity; for example, NHS data shows more than 73 million dental activity units delivered, indicating widespread procedural demand.

Globally, oral health needs remain substantial, with untreated dental caries among the most common conditions affecting billions. Continued enhancements in dental instrumentation, from ergonomics to digital integration, support more precise and efficient patient care. Supported by government health policies and expanding access to dental services, the dental medical instruments market remains pivotal to improving oral health outcomes worldwide.

Key Takeaways

- Market Size: The Global Dental Medical Instruments Market size was US$ 21.3 billion in 2025. The market is estimated to grow to US$ 43.1 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 7.3%.

- Product Type: Diagnostic Instruments has the largest market share, accounting for 34% of total sales.

- Instrument Category: Handheld Instruments dominate the segment, accounting for 58% of total revenue.

- Application: General Dentistry leads the segment, accounting for 39% of total revenue.

- End User: Dental Clinics lead the segment, accounting for 61% of total revenue.

- Distribution Channel: Direct Sales dominate the segment, accounting for 67% of total revenue.

- Regional: North America is the dominant regional market, accounting for 36% of global sales.

Product Type Analysis

The Dental Medical Instruments Market is segmented by product type into diagnostic instruments, surgical instruments, restorative instruments, orthodontic instruments, and periodontal instruments. Diagnostic instruments dominated the market with a 34.00% share in 2025, reflecting their essential role in early disease detection, treatment planning, and routine dental examinations. Instruments such as dental mirrors, probes, radiography devices, and intraoral scanners are increasingly adopted due to rising awareness of preventive oral healthcare and advancements in diagnostic accuracy.

Surgical instruments accounted for 29.00% of the market, supported by the growing number of oral surgeries, tooth extractions, and implant procedures worldwide. Restorative instruments held a 21.00% share, driven by increasing demand for fillings, crowns, bridges, and cosmetic dental procedures.

Orthodontic instruments represented 10.00%, benefiting from the rising prevalence of malocclusion and the growing popularity of aesthetic orthodontic treatments. Periodontal instruments contributed the remaining 6.00%, reflecting steady demand for scaling, root planing, and gum disease management. Together, these segments highlight the market’s balanced growth across preventive, corrective, and therapeutic dental care solutions.

Instrument Category Analysis

Based on instrument category, the market is segmented into handheld instruments, powered instruments, and laser-based instruments. Handheld instruments dominated the market with a 58.00% share in 2025, owing to their widespread use in nearly all dental procedures. Items such as forceps, scalers, curettes, and dental explorers remain indispensable due to their affordability, ease of use, and compatibility with both basic and advanced dental practices.

Powered instruments accounted for 30.00% of the market, supported by increasing adoption of electric handpieces, ultrasonic scalers, and motor-driven systems that improve procedural efficiency and precision. These instruments are particularly favoured in high-volume clinics and hospitals seeking faster treatment turnaround and enhanced patient comfort.

Laser-based instruments represented 12.00%, reflecting growing interest in minimally invasive dentistry. Dental lasers are increasingly used for soft tissue procedures, periodontal therapy, and cosmetic treatments due to reduced bleeding, faster healing, and improved clinical outcomes. Although lasers currently hold a smaller share, technological advancements and cost reductions are expected to support their faster adoption over the coming years.

Application Analysis

By application, the Dental Medical Instruments Market is segmented into general dentistry, restorative dentistry, oral surgery, orthodontics, and periodontics. General dentistry dominated the market with a 39.00% share in 2025, driven by the high frequency of routine check-ups, cleanings, diagnostics, and preventive treatments. The broad use of diagnostic and handheld instruments in everyday dental care significantly contributes to this segment’s leadership.

Restorative dentistry represents a substantial portion of the market, supported by rising demand for crowns, fillings, implants, and cosmetic restorations linked to ageing populations and increased aesthetic awareness. Oral surgery continues to generate steady demand due to growing volumes of extractions, trauma care, and implant procedures.

Orthodontics is identified as the fastest-growing segment, fueled by increasing adoption of braces, aligners, and advanced orthodontic technologies among both adolescents and adults. Periodontics maintains stable growth, supported by the rising prevalence of gum diseases and a greater emphasis on periodontal health. Overall, application segmentation reflects the expanding scope of dental services across preventive, corrective, and specialised care.

End User Analysis

The market is segmented by end user into dental clinics, hospitals, and academic & research institutes. Dental clinics dominated the market with a 61.00% share in 2025, as they serve as the primary point of care for most dental treatments. High patient footfall, increasing numbers of private practices, and growing adoption of advanced dental equipment strongly support this segment.

Hospitals represent a significant share, particularly for complex dental surgeries, trauma cases, and procedures requiring multidisciplinary care. The presence of specialised oral and maxillofacial surgery departments drives steady demand for surgical and powered dental instruments in hospital settings.

Academic and research institutes account for a smaller but important share, supported by dental education programs, clinical training, and research activities. These institutions contribute to consistent demand for a wide range of dental instruments for teaching and innovation purposes.

Overall, end-user segmentation highlights the central role of dental clinics in market revenue generation, while hospitals and academic institutions support technological advancement and workforce development within the dental healthcare ecosystem.

Distribution Channel Analysis

By distribution channel, the Dental Medical Instruments Market is segmented into direct sales, distributors, and online procurement. Direct sales dominated the market with a 67.00% share in 2025, as manufacturers increasingly prefer direct engagement with dental clinics and hospitals to offer customised solutions, technical support, and after-sales services. Direct sales channels also enable better pricing control and stronger long-term customer relationships.

Distributors represent a significant portion of the market, particularly in regions where manufacturers rely on established distribution networks to reach smaller clinics and remote areas. These intermediaries play a key role in inventory management, local market penetration, and regulatory compliance.

Online procurement accounts for a smaller but rapidly growing share, driven by increasing digitalisation and convenience in purchasing standard dental instruments and consumables. While online channels are currently limited by regulatory and service constraints for high-value equipment, their role is expected to expand as digital platforms improve logistics, transparency, and product availability across global markets.

Key Market Segments

By Product Type

- Diagnostic Instruments

- Surgical Instruments

- Restorative Instruments

- Orthodontic Instruments

- Periodontal Instruments

By Instrument Category

- Handheld Instruments

- Powered Instruments

- Laser-Based Instruments

By Application

- General Dentistry

- Restorative Dentistry

- Oral Surgery

- Orthodontics

- Periodontics

By End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

By Distribution Channel

- Direct Sales

- Distributors

- Online Procurement

Driving Factors

Oral disease burden and ageing-led restorative demand

Oral disease remains the broadest volume engine for dental instruments because the addressable patient base is already enormous and still expanding with population ageing: WHO states oral diseases affect nearly 3.7 billion people globally and severe periodontal disease affects more than 1 billion people, while edentulism remains a major late-stage treatment burden.

This matters commercially because restorative and periodontal case growth raises recurring use of examination tools, hand instruments, scaling systems, surgical sets, sterilisation loads, and replacement demand for operatory equipment rather than only one-time aesthetic purchases.

In mature markets, older cohorts disproportionately consume prosthodontic and periodontal services; U.S. evidence cited in recent literature shows 64.8% of adults visited a dentist in a year and 67.1% of adults aged 65+ did so, indicating that senior cohorts remain active service users once insured income and care access are present.

That combination supports a roughly +1.4 percentage-point uplift to forward CAGR because ageing does not just add patients; it lifts treatment intensity per patient, especially for extractions, implant planning, radiography, prophylaxis, and prosthetic maintenance.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oral disease burden and ageing-led restorative demand | +1.4% | North America core, Western Europe, Japan, urban China, Brazil | Long term (≥ 4 years) |

| Digital workflow shift in scanning, CAD/CAM, and chairside productivity | +1.7% | North America core, EU, South Korea, Japan, China tier-1/2 cities, GCC | Medium term (2-4 years) |

| Implant and prosthodontic case mix expansion | +1.2% | North America, DACH/Italy/Spain, South Korea, Japan, Brazil, Turkey | Medium term (2-4 years) |

| DSO and group-practice procurement standardisation | +0.9% | U.S. core, UK, Nordics, Australia, GCC | Short term (≤ 2 years) |

| 3D imaging, AI diagnostics, and integrated software ecosystems | +1.0% | U.S., EU, Japan, South Korea, premium APAC corridors | Medium term (2-4 years) |

| Emerging-market clinic modernisation and local access expansion | +1.3% | India, Southeast Asia, China lower-tier cities, Latin America, Middle East | Long term (≥ 4 years) |

Challenges

Trade Concentration Exposure

The dental instruments market remains highly exposed to trade concentration risk because a significant share of global manufacturing and export capacity is concentrated in a limited number of production hubs, particularly within HS 9018 trade categories. This structural dependency makes the supply chain vulnerable to corridor-specific tariff changes, customs delays, and forced sourcing realignments rather than underlying demand weakness.

Trade flow patterns indicate that major exporting countries continue to supply a wide range of destination markets, reinforcing reliance on a small set of global manufacturing nodes for both components and finished instruments. As a result, even isolated tariff or customs disruptions can create immediate pricing and logistics impacts, with observed category-level inflation of approximately 9–14%, while also triggering 30–90 days of supplier-switching friction as manufacturers requalify alternate sources.

Companies often respond by increasing safety stock by 15–25%, which raises working capital requirements and reduces supply-chain efficiency. Because meaningful diversification requires revalidation, tooling transfers, and regulatory documentation across jurisdictions, supply-chain resilience typically depends on 24–48 months of restructuring rather than short-term procurement adjustments, making trade concentration a persistent structural constraint on the industry.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Clinical labour bottlenecks | -1.4% | North America core, EU care markets, Africa access gaps | Medium term (2-4 years) |

| Sterilisation throughput strain | -0.8% | North America core, EU regulatory hubs, APAC hospital clusters | Medium term (2-4 years) |

| Input-cost volatility | -1.0% | US import channels, EU manufacturing belts, APAC sourcing bases | Medium term (2-4 years) |

| Trade concentration exposure | -0.9% | US-China routes, EU import nodes, APAC logistics corridors | Long term (≥ 4 years) |

| Digital compliance overload | -0.7% | US FDA pathway, EU MDR markets, advanced APAC systems | Medium term (2-4 years) |

| Procedure workflow fragmentation | -1.2% | North America DSO networks, EU mixed practices, urban APAC clinics | Long term (≥ 4 years) |

Restraining Factors

U.S. tariff-led import inflation

U.S. dental instrument demand is being constrained by imported cost inflation rather than by clinical need, as 2025 tariff actions introduced a 10% baseline import tariff and much higher rates on some China-linked goods, with industry commentary indicating resulting dental supply price increases in the high-single-digit to low-double-digit range during 2025 and limited relief expected before late 2026.

Because a large share of hand instruments, consumables, small equipment subassemblies, and accessory components remains globally sourced, distributors and practices are absorbing landed-cost increases that can plausibly add 8–15% to selected product categories, while manufacturers either compress gross margin or push through staged price lists that reduce reorder elasticity for non-urgent upgrades.

In market terms, this does not eliminate procedure volume, but it does delay scanner replacements, sterilisation room upgrades, and multi-chair expansion projects, especially in independent practices where reimbursement has not kept pace with overhead; that translates into a modelled 1.4% point CAGR decrement in 2026, with the sharpest damage concentrated in U.S. private practices and DSO procurement budgets exposed to imported equipment baskets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU MDR recertification drag | -1.2% | EU core, UK-linked supply, CEE | Medium term (2-4 years) |

| U.S. tariff-led import inflation | -1.4% | North America core | Short term (≤ 2 years) |

| Chairside labour shortage | -1.0% | North America core, Western Europe, ANZ | Medium term (2-4 years) |

| Device/component shortages | -0.8% | U.S., EU, selected APAC import hubs | Short term (≤ 2 years) |

| Logistics and lead-time volatility | -0.7% | APAC corridors, EU, North America | Short term (≤ 2 years) |

| Reimbursement and practice margin stress | -1.1% | U.S., parts of the EU, LatAm private-pay markets | Medium term (2-4 years) |

Opportunity

DSO Platform Bundling

Dental Support Organisations (DSOs) are increasingly acting as procurement aggregators in the dental instruments market, shifting purchasing power away from fragmented independent clinics toward centralised, multi-site enterprise buyers.

This creates a structural opportunity for suppliers to move beyond traditional one-off equipment sales toward integrated DSO-focused contracts that bundle instruments, maintenance services, training, consumables, and financing into unified commercial packages.

In this model, vendors can increase revenue per clinic location by an estimated 12–18% through higher attachment of services and recurring consumables, while reducing customer acquisition costs per chair by approximately 20–30% due to centralised purchasing and lower sales complexity.

The shift also enables more stable multi-site agreements with stronger retention dynamics and improved visibility of utilisation across networks. As DSOs expand their share of practice ownership, suppliers that align pricing, service-level agreements, and analytics-driven utilisation models to enterprise buyers are better positioned to capture share-of-wallet and improve operating leverage across consolidated dental networks.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

| DSO platform bundling | +1.8% | North America core, Western Europe, ANZ | Short term |

| Chairside digital subscriptions | +2.2% | North America, EU, Japan, Korea, tier-1 China | Short term |

| Value-tier emerging market lines | +1.6% | India, ASEAN, LATAM, MEA | Medium term |

| Oral-systemic care channels | +1.3% | U.S., EU5, GCC, urban APAC | Medium term |

| Implant-orthodontic roll-ups | +1.9% | North America, Europe, China, Brazil | Medium term |

| Mobile and public-care kits | +1.1% | India, Africa, ASEAN, rural LATAM | Long term |

Regional Analysis

In 2025, North America led the market, achieving over 36.00% share with a revenue of US $ 7.7 billion. The region’s dominance is primarily driven by high dental care awareness, strong reimbursement coverage for oral health procedures, and the widespread adoption of advanced dental technologies.

A well-established network of dental clinics, hospitals, and speciality practices, along with frequent dental visits per capita, continues to sustain robust demand for diagnostic, surgical, and restorative instruments. Continuous investment in digital dentistry, including CAD/CAM systems and advanced imaging tools, further strengthens market growth across the United States and Canada.

Europe represents the second-largest regional market, supported by universal healthcare systems, favourable government oral health initiatives, and a growing elderly population requiring restorative and periodontal treatments. Countries such as Germany, the United Kingdom, and France demonstrate steady demand for high-quality dental instruments due to stringent clinical standards and strong professional dental associations.

The Asia-Pacific region is witnessing the fastest growth, fueled by rising disposable incomes, expanding dental tourism, and increasing penetration of private dental clinics in countries like China, India, and South Korea. Latin America and the Middle East & Africa show moderate growth, supported by improving healthcare infrastructure and gradual increases in dental care expenditure, though market penetration remains comparatively lower than in developed regions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global dental medical instruments market is achieved through a comprehensive product portfolio breadth spanning diagnostic, surgical, restorative, orthodontic, and periodontal instrument categories, established distribution relationships with dental clinics and institutional buyers globally, and continued investment in powered and laser-based instrument technology development addressing growing clinical demand for precision and efficiency improvements.

Major strategic priorities for leading manufacturers include expansion of digital diagnostic instrument integration, development of ergonomic handheld instrument designs reducing clinician fatigue during extended procedures, and investment in regulatory compliance infrastructure supporting medical device certification across multiple international markets simultaneously.

Strong direct sales relationships with dental clinic networks, combined with growing distributor partnerships across emerging Asia Pacific markets, represent a critical competitive differentiator for manufacturers seeking sustained institutional procurement volume across both general dentistry and speciality practice settings.

Top Key Players

- Dentsply Sirona

- Envista Holdings

- Straumann Group

- Align Technology

- Planmeca Oy

- GC Corporation

- Ivoclar Vivadent

- Hu-Friedy (STERIS)

- Henry Schein Inc.

- Carestream Dental

- Vatech Co., Ltd.

- 3M Oral Care

- NSK Nakanishi Inc.

- Brasseler USA

- Osstem Implant Co., Ltd.

Recent Developments

- In January 2026, Dentsply Sirona launched an expanded diagnostic imaging instrument line featuring enhanced digital sensor technology, targeting dental clinics and hospital dental departments seeking improved diagnostic precision for restorative and orthodontic treatment planning.

- In February 2026, Straumann Group introduced a new powered surgical instrument system designed for implantology and oral surgery procedures, targeting dental clinics and academic research institutes seeking improved procedural efficiency and reduced operative time.

- In March 2026, Planmeca Oy expanded its laser-based diagnostic and treatment instrument portfolio with new periodontal and restorative dentistry applications, targeting speciality dental practices across European and Asia Pacific markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 21.3 Billion |

| Forecast Revenue (2035) | US$ 43.1 Billion |

| CAGR (2026-2035) | 7.30% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Diagnostic Instruments, Surgical Instruments, Restorative Instruments, Orthodontic Instruments, Periodontal Instruments), By Instrument Category (Handheld Instruments, Powered Instruments, Laser-Based Instruments), By Application (General Dentistry, Restorative Dentistry, Oral Surgery, Orthodontics, Periodontics), By End User (Dental Clinics, Hospitals, Academic & Research Institutes), By Distribution Channel (Direct Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Envista Holdings, Straumann Group, Align Technology, Planmeca Oy, GC Corporation, Ivoclar Vivadent, Hu-Friedy (STERIS), Henry Schein Inc., Carestream Dental, Vatech Co., Ltd., 3M Oral Care, NSK Nakanishi Inc., Brasseler USA, Osstem Implant Co., Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |