Quick Navigation

- Report Overview

- Key Takeaways

- US Market Expansion

- North America Growth

- Component Insights

- Deployment Mode Insights

- Organization Size Insights

- Application Insights

- Industry Vertical Insights

- Key Market Segments

- Emerging Trends

- Business Benefits

- Driver

- Restraint

- Opportunity

- Challenge

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

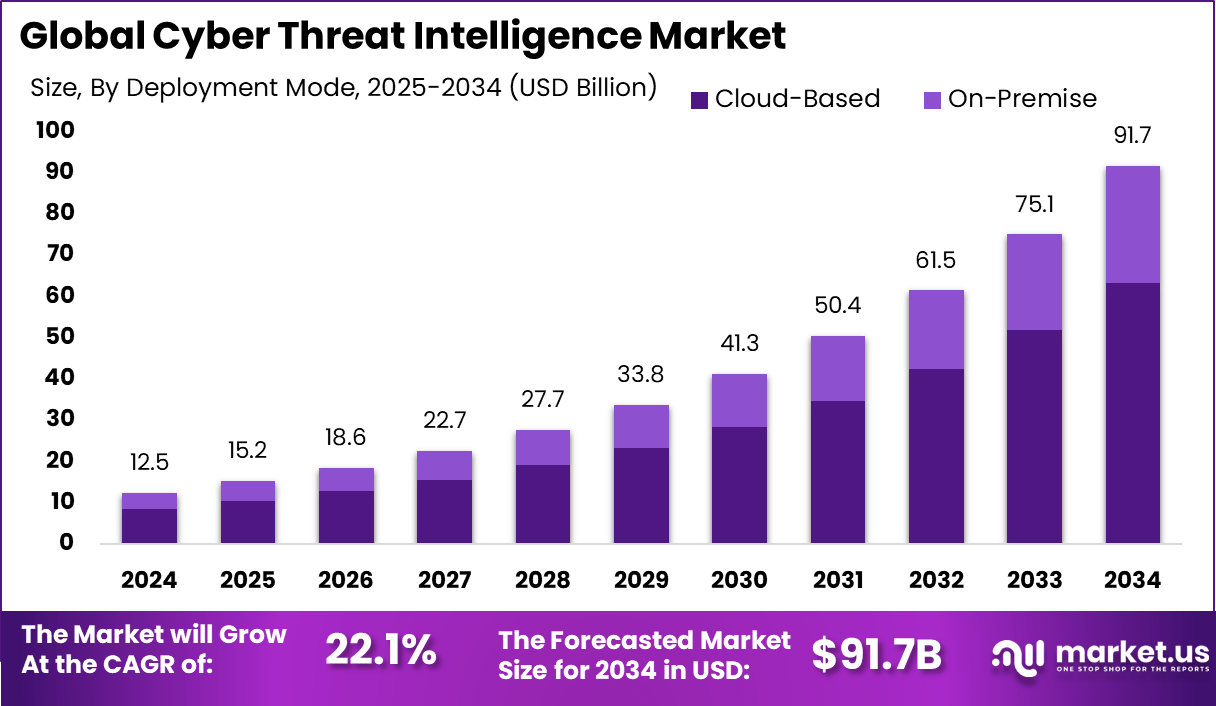

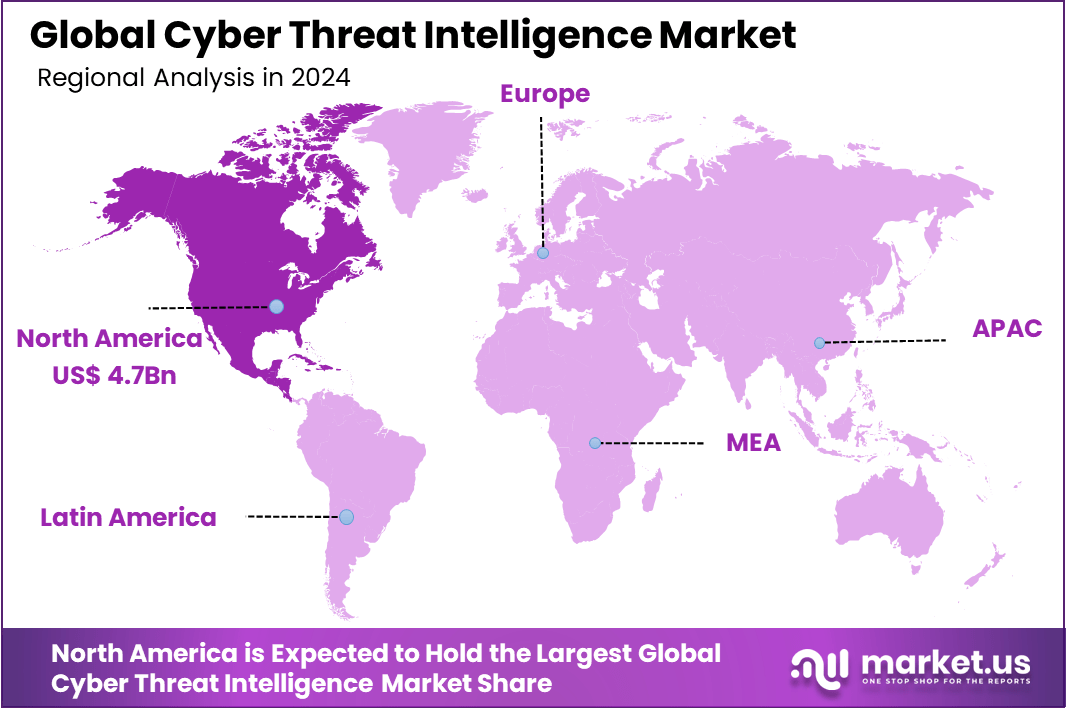

The Global Cyber Threat Intelligence Market size is expected to be worth around USD 91.7 Billion By 2034, from USD 12.5 billion in 2024, growing at a CAGR of 22.1% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 38% share, holding USD 4.7 Billion revenue.

Cyber Threat Intelligence (CTI) refers to the systematic collection, analysis, and dissemination of information regarding potential or existing cyber threats. This intelligence enables organizations to anticipate, prevent, and respond effectively to cyberattacks by understanding the behavior of threat actors, their tactics, and the vulnerabilities they exploit.

The global Cyber Threat Intelligence market has experienced significant growth in recent years. The surge in cyber threats, including ransomware and advanced persistent threats, has necessitated the adoption of CTI solutions. The proliferation of digital transformation initiatives and the expansion of cloud services have increased the attack surface, making organizations more vulnerable to cyberattacks.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into CTI platforms enhances the ability to detect and respond to threats in real-time. These technologies enable the analysis of vast datasets to identify patterns and predict potential attacks, thereby improving the efficiency of cybersecurity operations. Cloud-based CTI solutions are also gaining traction due to their scalability and flexibility.

According to Market.us, The Global Threat Intelligence Market is projected to witness substantial expansion, reaching approximately USD 101.14 Billion by 2034, up sharply from USD 15.8 Billion in 2024. This impressive growth reflects a robust CAGR of 20.40% between 2025 and 2034, driven by rising cyber threats, growing digital infrastructures, and increasing demand for proactive security frameworks across critical sectors.

According to the findings from VPNRanks, the adoption of threat intelligence is accelerating at a notable pace. By 2024, approximately 5,916 companies are expected to implement threat intelligence solutions, reflecting a growing urgency to stay ahead of evolving cyber risks. A sharp rise in the formation of dedicated Cyber Threat Intelligence (CTI) teams is also projected, with adoption expected to reach around 53.29%, highlighting a strategic shift toward proactive defense mechanisms.

Cloud-based threat intelligence is another transformative area – its role in scaling cybersecurity is expected to push the related market segment to an estimated USD 600.61 billion. Importantly, the adoption rate among small and medium enterprises is expected to climb, with 66% of SMEs forecasted to deploy threat intelligence solutions by the end of 2024, marking a crucial step in democratizing advanced cybersecurity capabilities across business sizes.

Key Takeaways

- The Global Cyber Threat Intelligence (CTI) Market is projected to grow from USD 12.5 billion in 2024 to around USD 91.7 billion by 2034, expanding at a strong CAGR of 22.1% over the forecast period.

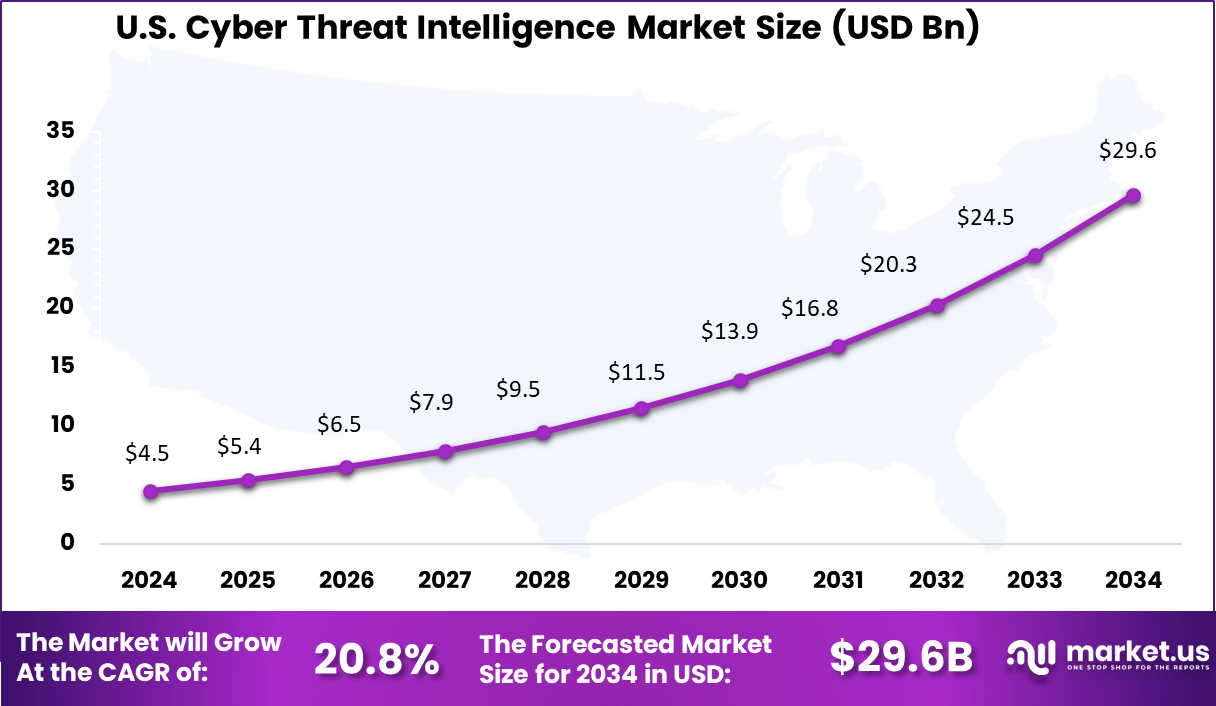

- In 2024, North America led the global market with more than a 38% share, generating USD 4.7 billion in revenue, with the United States alone contributing USD 4.5 billion.

- The U.S. market is forecasted to grow to nearly USD 29.6 billion by 2034, supported by an estimated 20.8% CAGR from 2025 to 2034.

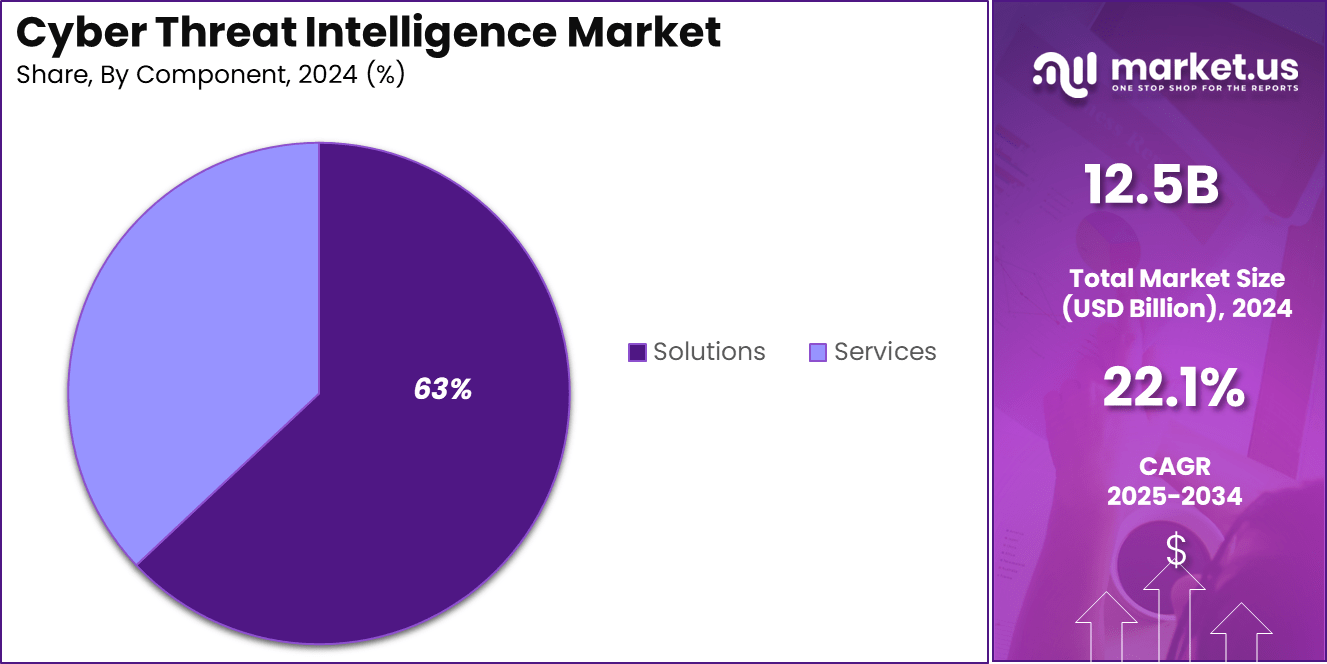

- By component, Solutions accounted for 63% of the global revenue share in 2024, driven by growing adoption of advanced threat detection tools.

- In terms of deployment, Cloud-Based models dominated with 69% share, supported by scalable infrastructure and faster integration with other security layers.

- By organization size, Large Enterprises captured 61% of the market, reflecting increased investments in CTI platforms for real-time threat hunting and risk management.

- Among applications, Security Information and Event Management (SIEM) emerged as the top-performing segment, holding a 26% share in 2024 due to its central role in consolidating threat data.

- By industry vertical, BFSI led with a 20% share, fueled by rising cyberattacks on financial institutions and increased regulatory compliance requirements.

US Market Expansion

The US Cyber Threat Intelligence Market is valued at approximately USD 4.5 Billion in 2024 and is predicted to increase from USD 11.5 Billion in 2029 to approximately USD 29.6 Billion by 2034, projected at a CAGR of 20.8% from 2025 to 2034.

North America Growth

In 2024, North America held a dominant position in the global Cyber Threat Intelligence (CTI) market, capturing over a 38% share and generating approximately USD 4.7 billion in revenue. This leadership is primarily attributed to the region’s advanced digital infrastructure, high adoption of cutting-edge technologies, and substantial investments in cybersecurity initiatives across both public and private sectors.

The region’s dominance is further reinforced by the increasing frequency and sophistication of cyber threats targeting critical infrastructure, financial institutions, and government agencies. This has necessitated the deployment of advanced CTI solutions to proactively detect, analyze, and mitigate potential cyber risks.

Component Insights

In 2024, the Solutions segment held a dominant position in the Cyber Threat Intelligence (CTI) market, capturing over 63% of the total market share. This leadership is attributed to the escalating demand for advanced security tools such as Threat Intelligence Platforms (TIPs), Security Information and Event Management (SIEM) systems, log management solutions, and risk and compliance management tools.

Organizations increasingly rely on these solutions to proactively detect, analyze, and respond to sophisticated cyber threats. The integration of artificial intelligence and machine learning into these platforms enhances real-time threat detection and response capabilities, making them indispensable for modern cybersecurity strategies.

The prominence of the Solutions segment is further reinforced by the growing complexity and frequency of cyberattacks targeting critical infrastructure and sensitive data across various industries. Sectors such as finance, healthcare, and government are investing heavily in robust CTI solutions to safeguard against data breaches and ensure compliance with stringent regulatory standards.

The scalability and adaptability of these solutions, especially cloud-based implementations, offer organizations the flexibility to address evolving security challenges effectively. Consequently, the Solutions segment is expected to maintain its leading position as organizations prioritize comprehensive and proactive cybersecurity measures.

Deployment Mode Insights

In 2024, the Cloud-Based segment held a dominant position in the Cyber Threat Intelligence (CTI) market, capturing over 69% of the total market share. This leadership is attributed to the escalating demand for scalable, flexible, and cost-effective security solutions that can adapt to the dynamic nature of cyber threats.

Organizations increasingly favor cloud-based CTI solutions for their ability to provide real-time threat detection, seamless integration with existing systems, and reduced infrastructure costs. The shift towards remote work and the proliferation of cloud services have further propelled the adoption of cloud-based CTI, as businesses seek to secure their digital assets across distributed environments.

The prominence of the Cloud-Based segment is further reinforced by the rapid advancements in artificial intelligence and machine learning technologies, which enhance the capabilities of CTI solutions in identifying and mitigating sophisticated cyber threats. Cloud-based platforms offer the agility to update and deploy security measures swiftly, ensuring organizations remain resilient against emerging threats.

Additionally, the pay-as-you-go model of cloud services aligns with the budgetary constraints of small and medium-sized enterprises, enabling broader access to advanced cybersecurity tools. As cyber threats continue to evolve in complexity and frequency, the reliance on cloud-based CTI solutions is expected to intensify, solidifying their leading position in the market.

Organization Size Insights

In 2024, the Large Enterprises segment held a dominant position in the Cyber Threat Intelligence (CTI) market, capturing over 61% of the total market share. This dominance is primarily attributed to the substantial investments these organizations make in advanced cybersecurity infrastructure to protect their extensive digital assets and complex networks.

Large enterprises often operate across multiple regions and sectors, making them prime targets for sophisticated cyber threats. To mitigate these risks, they adopt comprehensive CTI solutions that offer real-time threat detection, analysis, and response capabilities. Furthermore, compliance with stringent regulatory frameworks such as GDPR, HIPAA, and CCPA necessitates the implementation of robust threat intelligence systems to ensure data protection and privacy.

The capacity of large enterprises to allocate significant budgets towards cybersecurity initiatives enables them to integrate cutting-edge technologies like artificial intelligence and machine learning into their CTI frameworks. These technologies enhance the ability to predict and neutralize potential threats proactively. Additionally, large organizations often have dedicated security operations centers (SOCs) and specialized teams that continuously monitor and analyze threat landscapes, facilitating swift incident response and mitigation.

Application Insights

In 2024, the Security Information and Event Management (SIEM) segment held a dominant position in the Cyber Threat Intelligence (CTI) market, capturing more than 34.4% of the total market share. This leadership is attributed to the escalating demand for real-time threat detection, compliance management, and advanced analytics capabilities.

SIEM systems have become integral to organizations’ cybersecurity strategies, providing centralized visibility into security events and facilitating prompt incident response. The integration of artificial intelligence and machine learning into SIEM platforms has further enhanced their ability to identify and mitigate sophisticated cyber threats.

The prominence of the SIEM segment is further reinforced by the increasing complexity of IT infrastructures and the proliferation of cloud-based services. Organizations are adopting SIEM solutions to manage security across diverse environments, ensuring consistent monitoring and compliance.

The scalability and adaptability of modern SIEM platforms enable businesses to address evolving security challenges effectively. As cyber threats continue to grow in frequency and sophistication, the reliance on SIEM solutions is expected to intensify, solidifying their leading position in the market.

Industry Vertical Insights

In 2024, the Banking, Financial Services, and Insurance (BFSI) segment held a dominant position in the Cyber Threat Intelligence (CTI) market, capturing more than a 20% share. This leadership is attributed to the sector’s heightened vulnerability to cyber threats, driven by the increasing digitization of financial services and the critical nature of the data they handle.

The proliferation of online banking, mobile payments, and digital financial platforms has expanded the attack surface, making BFSI institutions prime targets for cybercriminals. Consequently, there is a growing emphasis on implementing advanced CTI solutions to proactively detect, analyze, and mitigate potential threats.

The BFSI sector’s commitment to cybersecurity is further reinforced by stringent regulatory requirements and compliance standards. Regulations such as the General Data Protection Regulation (GDPR), the Payment Card Industry Data Security Standard (PCI DSS), and various national cybersecurity laws mandate robust security frameworks to protect sensitive financial data.

Key Market Segments

By Component

- Solutions

- Threat Intelligence Platforms

- Security Information and Event Management (SIEM)

- Log Management

- Risk and Compliance Management

- Services

- Managed Services

- Professional Services

- Consulting

- Training

- Integration

By Deployment Mode

- On-Premise

- Cloud-Based

By Organization Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

By Application

- Security Information and Event Management (SIEM)

- Risk Management

- Incident Response

- Security Analytics

- Others (e.g., malware analysis, threat hunting)

By Industry Vertical

- BFSI

- IT & Telecom

- Government & Defense

- Healthcare

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

AI-Powered Threats and Deepfake Tactics

In 2024, cybercriminals increasingly leveraged artificial intelligence to enhance the sophistication and scale of their attacks. A notable development was the use of deepfake technology to create synthetic identities, enabling attackers to bypass traditional security measures such as Know Your Customer (KYC) protocols and biometric verification. These AI-generated personas were employed to probe and exploit vulnerabilities in financial institutions and digital platforms, presenting a significant challenge to existing cybersecurity frameworks.

Standardization of Threat Actor Naming Conventions

The cybersecurity industry recognized the confusion caused by inconsistent naming of threat actors, leading to fragmented threat intelligence. In response, major cybersecurity firms initiated efforts to standardize the nomenclature for state-sponsored hacker groups and cybercriminals. This initiative aims to enhance clarity and coordination in threat analysis and response, facilitating more effective collaboration across organizations and sectors.

Business Benefits

Proactive Risk Mitigation and Operational Continuity

Implementing cyber threat intelligence (CTI) enables organizations to transition from reactive to proactive cybersecurity strategies. By analyzing threat actors’ tactics, techniques, and procedures, businesses can anticipate potential attacks and implement preventive measures, thereby reducing the likelihood of successful breaches. This proactive approach not only safeguards sensitive data but also ensures uninterrupted business operations, maintaining customer trust and organizational reputation.

Enhanced Decision-Making and Resource Allocation

CTI provides actionable insights that inform strategic decision-making, allowing organizations to allocate resources effectively to areas of highest risk. By understanding the threat landscape, businesses can prioritize investments in cybersecurity measures that address the most pressing vulnerabilities. This targeted approach optimizes security budgets and enhances the overall resilience of the organization’s digital infrastructure.

Driver

Surge in AI-Powered Cyber Threats

In 2024, the cyber threat landscape witnessed a significant escalation, with AI-driven attacks becoming more prevalent. Automated scanning activities surged to 36,000 scans per second, marking a 16.7% year-on-year increase. Cybercriminals increasingly targeted vulnerable digital assets, including Remote Desktop Protocols and IoT systems, earlier in their attack cycles.

Notably, there was a 500% increase in logs from compromised systems, leading to over 1.7 billion stolen credentials circulating on the dark web. This proliferation of AI-enhanced cyber threats underscores the urgent need for advanced cyber threat intelligence solutions to detect and mitigate sophisticated attacks.

The evolving tactics of cyber adversaries, such as leveraging legitimate software tools to avoid detection, have made traditional security measures less effective. Organizations are now compelled to adopt proactive and intelligent threat detection systems that can anticipate and neutralize threats in real-time.

Restraint

High Implementation and Operational Costs

Despite the growing necessity for robust cyber threat intelligence, the high costs associated with implementing and maintaining these solutions pose a significant barrier, especially for small and medium-sized enterprises (SMEs).

The initial investment required for advanced threat intelligence tools, coupled with ongoing operational expenses, can be prohibitive for organizations with limited budgets. This financial hurdle often leads to delayed adoption or reliance on less comprehensive security measures, leaving businesses vulnerable to cyber threats.

Moreover, the complexity of integrating cyber threat intelligence systems into existing IT infrastructures necessitates specialized expertise and continuous training, further escalating costs. For many organizations, balancing the need for advanced cybersecurity with budgetary constraints remains a challenging endeavor, potentially compromising their ability to effectively counter sophisticated cyber threats.

Opportunity

Integration of AI in Threat Intelligence

The integration of artificial intelligence (AI) into cyber threat intelligence presents a significant opportunity for enhancing cybersecurity measures. AI-driven threat intelligence platforms can analyze vast amounts of data in real-time, identifying patterns and anomalies that may indicate potential security breaches. This capability enables organizations to respond to threats more swiftly and accurately, reducing the risk of data breaches and other cyber incidents.

Furthermore, AI can automate routine security tasks, freeing up cybersecurity professionals to focus on more complex issues. The predictive capabilities of AI also allow for the anticipation of emerging threats, enabling proactive defense strategies. As cyber threats continue to evolve in complexity, the adoption of AI-enhanced threat intelligence solutions is poised to become a critical component of effective cybersecurity frameworks.

Challenge

Cybersecurity Talent Shortage Impedes CTI Deployment

A significant challenge facing the CTI market is the shortage of skilled cybersecurity professionals. The cybersecurity industry is experiencing a critical talent gap, with projections indicating 457,000 job openings nationwide by 2025. This shortage hampers the effective deployment and management of CTI solutions, as organizations struggle to recruit and retain qualified personnel.

The talent deficit not only delays the implementation of CTI systems but also increases the risk of security breaches due to inadequate threat monitoring and response capabilities. Addressing this challenge requires strategic investments in workforce development, including training programs and partnerships with educational institutions to cultivate a pipeline of cybersecurity professionals.

Key Player Analysis

IBM Corporation has strategically repositioned its cybersecurity portfolio to emphasize AI-driven solutions. In 2024, IBM divested its QRadar SaaS assets to Palo Alto Networks, aligning with a broader focus on generative AI security and data protection. Subsequent acquisitions, including HashiCorp and Seek AI, have bolstered IBM’s capabilities in hybrid cloud security and AI-powered data analysis.

Optiv Security, Inc. has expanded its cybersecurity offerings through strategic acquisitions and innovative product development. The 2023 acquisition of ClearShark significantly increased Optiv’s federal market presence, enhancing its ability to serve government clients. In 2024, Optiv launched the Optiv Market System (OMS), a proprietary security architecture providing comprehensive insights across clients’ cybersecurity infrastructures.

Dell Technologies, Inc. has realigned its cybersecurity strategy by divesting Secureworks to Sophos in a $859 million deal in 2024, allowing Dell to concentrate on AI and infrastructure innovations. The company has introduced the Dell AI Factory with NVIDIA, offering advanced AI solutions to accelerate enterprise adoption and enhance data center capabilities.

Top Key Players Covered

- IBM Corporation

- Optiv Security, Inc.

- Dell Technologies, Inc.

- Lookingglass Cyber Solutions, Inc.

- Webroot Inc.

- LogRhythm, Inc.

- Check Point Software Technologies Ltd.

- McAfee LLC

- Anomali

- Farsight Security, Inc.

- Splunk, Inc.

- Juniper Networks, Inc.

- Symantec Corporation

- Others

Recent Developments

- In May 2024, IBM announced the sale of its cloud-based QRadar cybersecurity software to Palo Alto Networks. This move is part of IBM’s broader strategy to focus on generative AI security and eliminate product overlaps. The partnership aims to jointly develop AI-powered security products, with QRadar customers transitioning to Palo Alto’s Cortex XSIAM platform.

- In May 2024, Dell Technologies reported a data breach affecting approximately 49 million customers. The breach exposed personal information through a poorly secured API, raising significant concerns about targeted phishing attacks and other potential cyber threats.

- In April 2024, ZeroFox completed its acquisition of LookingGlass Cyber Solutions, a leader in external attack surface management and global threat intelligence. This acquisition expands ZeroFox’s external cybersecurity portfolio, enhancing its capabilities in attack surface management and vulnerability intelligence.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 12.5 Bn |

| Forecast Revenue (2034) | USD 91.7 Bn |

| CAGR (2025-2034) | 22.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solutions (Threat Intelligence Platforms, Security Information and Event Management (SIEM), Log Management, Risk and Compliance Management), Services (Managed Services, Professional Services – Consulting, Training, Integration)), By Deployment Mode (On-Premise, Cloud-Based), By Organization Size (Small and Medium-sized Enterprises (SMEs), Large Enterprises), By Application (Security Information and Event Management (SIEM), Risk Management, Incident Response, Security Analytics, Others (e.g., malware analysis, threat hunting)), By Industry Vertical (BFSI, IT & Telecom, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IBM Corporation, Optiv Security, Inc., Dell Technologies, Inc., Lookingglass Cyber Solutions, Inc., Webroot Inc., LogRhythm, Inc., Check Point Software Technologies Ltd., McAfee LLC, Anomali, Farsight Security, Inc., Splunk, Inc., Juniper Networks, Inc., Symantec Corporation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |