Quick Navigation

- Report Scope

- Key Takeaways

- Analyst’s Viewpoint

- Key Statistics

- Regional Analysis

- By Component

- By Deployment

- By Enterprise Size

- By Application

- By End-use

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

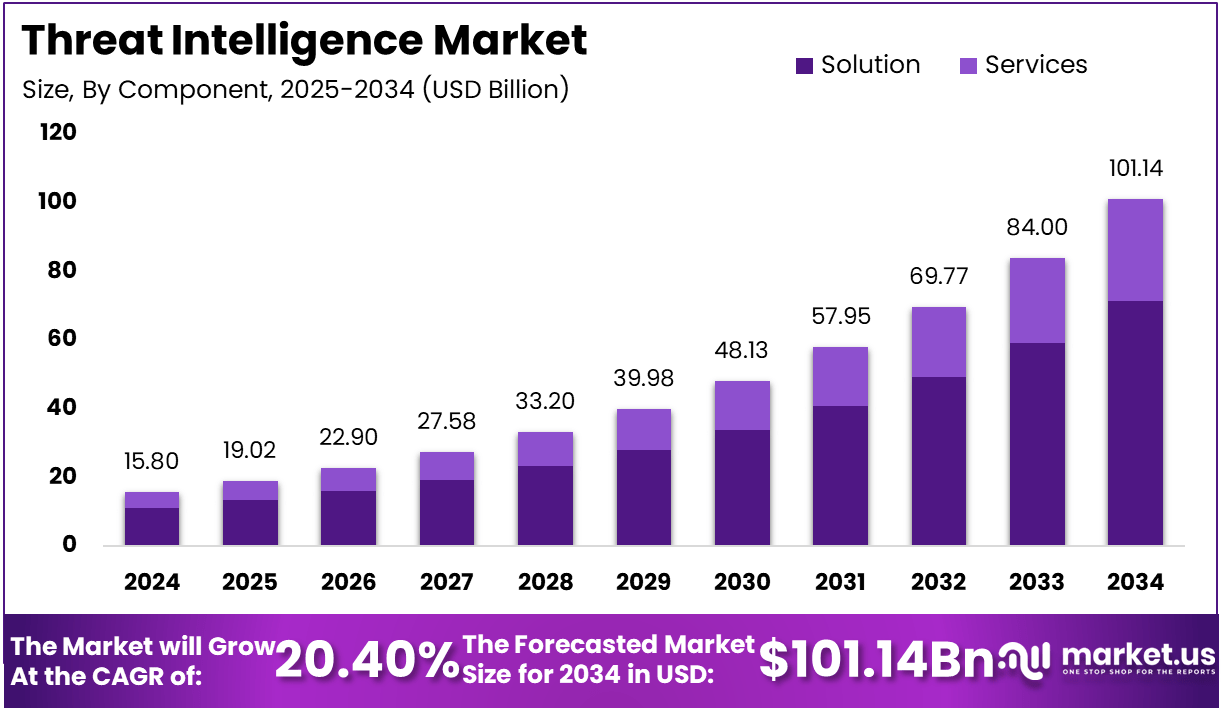

The Global Threat Intelligence Market is expected to be worth around USD 101.14 Billion By 2034, up from USD 15.8 Billion in 2024. It is expected to grow at a CAGR of 20.40% from 2025 to 2034.

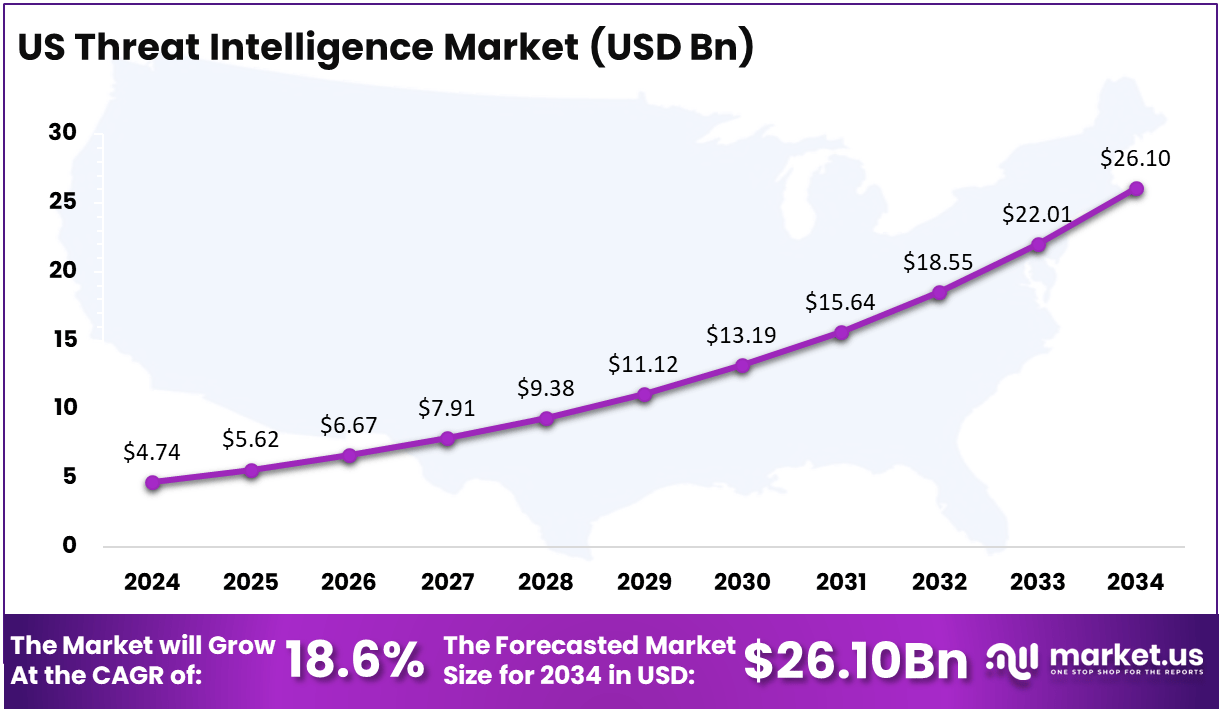

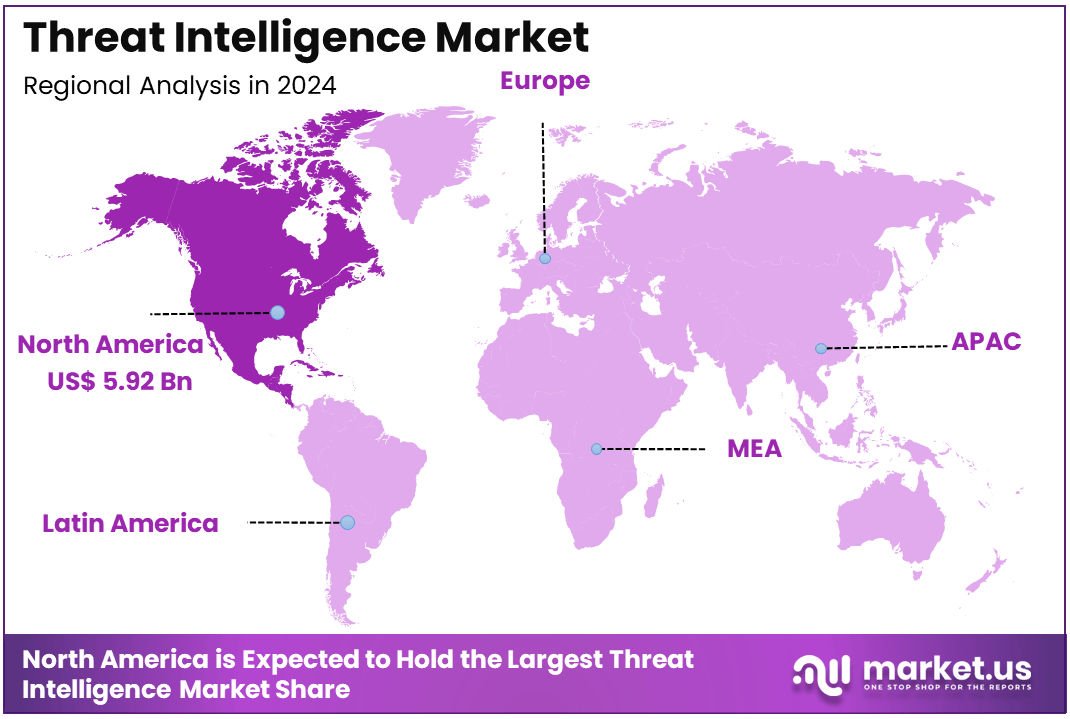

In 2024, North America held a dominant market position, capturing over a 37.5% share and earning USD 5.92 Billion in revenue. Further, the United States dominates the market by USD 4.74 Billion, steadily holding a strong position with a CAGR of 18.6%.

Threat intelligence refers to the information collected, analyzed, and used to understand the threats posed by potential cyber-attacks or data breaches. It includes information about the tactics, techniques, and procedures (TTPs) that cybercriminals use to exploit vulnerabilities in systems and networks.

The goal of threat intelligence is to provide organizations with actionable insights that help them predict, identify, and mitigate potential cyber risks. It can encompass both external threats, such as malware, phishing campaigns, and hacking attempts, as well as internal risks, such as insider threats. By gathering and analyzing data from a variety of sources—such as network traffic, logs, and external threat feeds—threat intelligence empowers organizations to protect their assets and maintain security proactively.

Key Takeaways

- Market Growth: The Threat Intelligence market is projected to grow from USD 15.8 billion in 2024 to USD 101.14 billion by 2034, with a robust CAGR of 20.40% over the forecast period.

- Component Breakdown: The solutions segment leads the market, contributing 70.5% to the total market share, as organizations increasingly adopt comprehensive threat intelligence platforms.

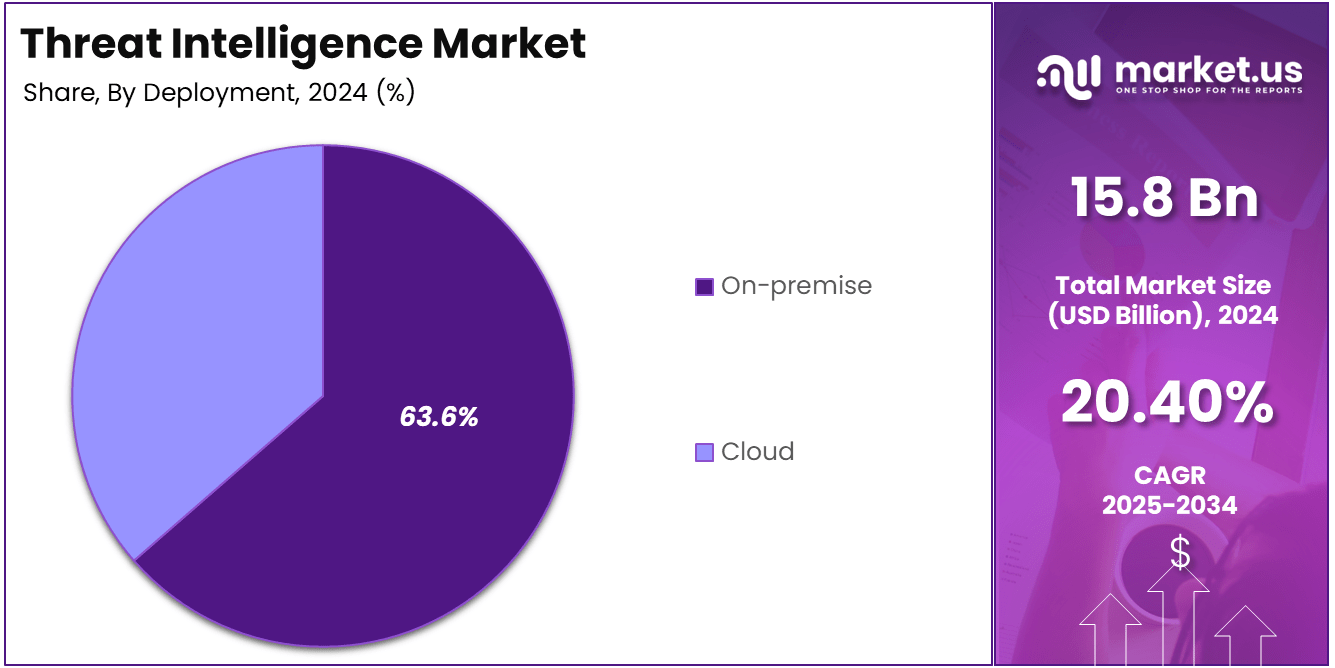

- Deployment Preference: The on-premise deployment model dominates, accounting for 63.6% of the market, as businesses prioritize control over their security infrastructure.

- Enterprise Size: Large enterprises hold the majority market share at 75.5%, driven by the high demand for robust threat intelligence solutions to safeguard vast networks and sensitive data.

- Application Focus: Security Information and Event Management (SIEM) accounts for 34.4% of the market share, underscoring its importance in real-time security monitoring and threat detection.

- End-Use Sector: The BFSI (Banking, Financial Services, and Insurance) sector is a major consumer, contributing 27.3% to the market due to the critical need for security in financial data.

- Regional Insights: North America holds the largest regional share at 37.5%, driven by high technological adoption and a mature cybersecurity landscape.

- U.S. Market: The U.S. accounts for USD 4.74 billion in market value, with a steady CAGR of 18.6%, reflecting consistent demand for advanced threat intelligence solutions.

Analyst’s Viewpoint

The threat intelligence market refers to the industry that provides tools, solutions, and services to help organizations prevent and mitigate cyber threats. This market includes a wide range of offerings, from software platforms that automate the collection and analysis of threat data to consulting services that help organizations set up and manage their threat intelligence programs.

The market is growing rapidly due to the increasing frequency and sophistication of cyberattacks, the rise of cloud-based infrastructure, and the growing need for organizations to comply with regulations around data protection and security. Threat intelligence platforms are increasingly incorporating machine learning and artificial intelligence to enhance threat detection and response times, further driving market growth.

The primary factors driving the growth of the threat intelligence market include the growing number and sophistication of cyberattacks, the need for proactive cybersecurity, and the increasing adoption of cloud technologies. As cybercriminals become more advanced and their attacks more widespread, businesses are increasingly turning to threat intelligence platforms to bolster their defenses.

Moreover, regulatory requirements, such as GDPR and CCPA, are pushing organizations to implement more robust cybersecurity measures, driving demand for threat intelligence solutions. Additionally, the growing reliance on digital infrastructure and the shift to remote work has opened up new attack vectors, heightening the need for comprehensive threat monitoring and response systems.

Key Statistics

Data Collection & Volume

- Daily, security systems generate billions of log events that need analysis for potential threats.

- A typical enterprise might ingest data from 10-50 different threat intelligence feeds.

- Some feeds can contain millions of indicators of compromise (IOCs), such as malicious IPs or hashes.

- Companies might spend upwards of $10,000 – $100,000+ annually on commercial threat intelligence feeds, depending on their scope and quality.

Usage & Adoption

- Studies show that over 80% of large enterprises now have a formal threat intelligence program.

- 70% of organizations use threat intelligence to improve incident response.

- 60% use it for vulnerability management and prioritization.

- The average security analyst spends 2-4 hours per day sifting through threat intelligence data.

Threat Intelligence Platform (TIP) Usage

- Organizations using a TIP see a 30-50% reduction in alert fatigue for security analysts.

- TIPs can automate the processing of thousands to millions of threat indicators.

- A well-implemented TIP can reduce incident response times by 15-25%.

Cybersecurity Budget Allocation

- An increasing number of organizations are allocating 5-15% of their cybersecurity budget to threat intelligence.

- Return on Investment (ROI) estimates for threat intelligence programs often range from 2x to 5x based on reduced incident impact and improved efficiency.

User Statistics

- There are approximately 500,000 – 1,000,000 cybersecurity professionals worldwide who actively consume or contribute to threat intelligence.

- The number of dedicated threat intelligence analysts per organization typically ranges from 1-10, depending on size and industry.

Quantity of Threats:

- Security vendors identify and categorize over 300,000 new malware samples daily.

- Phishing attacks account for 30-40% of reported cybersecurity incidents.

Regional Analysis

US Region Market Size

In particular, the United States is a major contributor, accounting for USD 4.74 billion in market value. This leadership is primarily driven by the region’s advanced technological infrastructure, high adoption rates of cybersecurity solutions, and continuous efforts to combat the increasing sophistication of cyber threats. The country’s strong focus on cybersecurity regulations, coupled with the presence of numerous tech giants and cybersecurity firms, fuels this dominance.

Furthermore, the increasing number of high-profile cyberattacks on government agencies, financial institutions, and businesses has heightened the demand for threat intelligence solutions, propelling market growth. With a robust CAGR of 18.6%, the U.S. market continues to demonstrate steady expansion, as enterprises across sectors such as banking, healthcare, and retail prioritize threat detection and prevention technologies.

Additionally, significant government investments in cybersecurity initiatives and the rise of advanced technologies like AI and machine learning in threat intelligence further strengthen the United States’ market position. As the region continues to innovate and expand its security infrastructure, North America is expected to maintain its leadership in the global Threat Intelligence market throughout the forecast period.

North America Market Size

In 2024, North America held a dominant market position in the global Threat Intelligence market, capturing more than 37.5% of the total share, with a revenue of USD 5.92 billion. The region’s leadership can be attributed to its advanced digital infrastructure, high levels of technology adoption, and substantial investments in cybersecurity initiatives across both private and public sectors.

The U.S., in particular, remains a key driver of this dominance, as it is home to many of the world’s largest tech and cybersecurity firms. The increasing frequency and sophistication of cyberattacks, along with stringent regulations like the GDPR in the U.S., have spurred businesses to adopt advanced threat intelligence solutions to safeguard their data and operations.

Moreover, North America is at the forefront of innovations in artificial intelligence (AI), machine learning, and automation, all of which enhance the capabilities of threat intelligence platforms. These technologies allow for faster and more accurate identification of threats, giving businesses a significant edge in proactively mitigating risks. Furthermore, government-led cybersecurity programs and initiatives, such as the National Cybersecurity Strategy, further bolster the demand for advanced threat detection and prevention solutions in the region.

By Component

In 2024, the Solution segment held a dominant market position in the global Threat Intelligence market, capturing more than 70.5% of the total share. This is largely due to the increasing demand for comprehensive, automated, and real-time solutions that can help businesses identify, assess, and respond to cybersecurity threats quickly and efficiently.

Organizations are seeking end-to-end solutions that integrate various features such as threat detection, monitoring, and analysis, all within a single platform. As cyber threats become more sophisticated, businesses are moving away from traditional methods and relying more on advanced threat intelligence solutions that leverage AI and machine learning for predictive insights.

The shift toward solutions over services is also driven by the growing need for scalable, cost-effective, and customizable cybersecurity measures. Unlike services, which often require ongoing professional engagement and are resource-intensive, solutions provide a more automated approach, reducing the need for continuous human intervention. With the rise in cybercrime, data breaches, and regulatory pressures, businesses are investing heavily in solutions that offer real-time monitoring, proactive defense, and rapid response capabilities. This growing focus on comprehensive security has fueled the expansion of the Solution segment in the Threat Intelligence market.

By Deployment

In 2024, the On-premise segment held a dominant market position in the global Threat Intelligence market, capturing more than 63.6% of the total share. The primary reason behind this preference is the enhanced control and security that on-premise deployments offer.

Many organizations, particularly large enterprises in industries like BFSI (Banking, Financial Services, and Insurance) and government sectors, require tighter control over their data and infrastructure due to the sensitivity and critical nature of the information they handle. With an on-premise setup, these companies can ensure that their threat intelligence solutions are fully integrated into their existing internal systems and processes, maintaining strict data governance and compliance with regulations.

On-premise solutions also allow for better customization and scalability, making them ideal for organizations with unique security requirements. These solutions are often more adaptable to an organization’s existing infrastructure, providing higher levels of security and a greater degree of monitoring and management.

Despite the rise in cloud adoption, the on-premise segment remains dominant due to these factors, offering a sense of assurance that cloud-based models may not fully provide when it comes to sensitive data handling. Therefore, the demand for on-premise threat intelligence solutions continues to be strong, driving the segment’s growth.

By Enterprise Size

In 2024, the Large Enterprises segment held a dominant market position in the global Threat Intelligence market, capturing more than 75.5% of the total share. Large enterprises are typically the primary adopters of threat intelligence solutions due to their complex IT infrastructures and the high volume of sensitive data they handle. These organizations operate across multiple regions and industries, making them prime targets for cyberattacks. As a result, they require robust, real-time threat intelligence capabilities to protect their networks, applications, and data.

Additionally, large enterprises have significant budgets dedicated to cybersecurity, enabling them to invest in comprehensive threat intelligence solutions that can scale with their needs. These organizations often have dedicated security teams and a higher degree of specialization, allowing them to fully leverage the sophisticated features and capabilities offered by threat intelligence platforms. Furthermore, they often face stricter regulatory and compliance requirements, particularly in sectors like BFSI (banking, financial services, and insurance), making threat intelligence a critical component of their overall risk management strategies.

While small and medium-sized enterprises (SMEs) are increasingly adopting threat intelligence solutions, the complex needs, higher budgets, and greater resources of large enterprises have allowed them to maintain a leading share of the market. This trend is expected to continue as enterprises face increasingly sophisticated cyber threats.

By Application

In 2024, the Security Information and Event Management (SIEM) segment held a dominant market position, capturing more than 34.4% of the total share in the global Threat Intelligence market. SIEM is one of the most critical components for enterprises looking to enhance their cybersecurity posture. The primary reason for its dominance is its ability to provide real-time monitoring, event correlation, and centralized logging of security events, which are vital for detecting, analyzing, and responding to potential security threats.

SIEM solutions collect data from various sources across an organization’s network and security infrastructure, such as firewalls, intrusion detection systems, and servers. By aggregating this data and applying advanced analytics, SIEM tools can identify anomalies, correlate events, and generate alerts about potential security breaches. This enables organizations to respond quickly to threats, minimize damage, and comply with industry regulations.

With the increasing frequency and sophistication of cyberattacks, organizations across all sectors require comprehensive and automated security event management. The rise in cybercrime, coupled with growing data protection regulations, continues to drive demand for SIEM solutions. This trend is expected to persist as organizations prioritize real-time security monitoring and compliance, keeping SIEM at the forefront of the threat intelligence market.

By End-use

In 2024, the BFSI (Banking, Financial Services, and Insurance) segment held a dominant market position, capturing more than 27.3% of the total share in the global Threat Intelligence market. The BFSI sector’s leadership in this space is primarily driven by its critical need to protect sensitive financial data and ensure regulatory compliance, making cybersecurity a top priority.

The BFSI sector is a major target for cyberattacks due to the value of the data it holds, such as customer financial information, transaction details, and personal identification data. As a result, financial institutions face constant threats from fraud, data breaches, and cybercrime, which increases their reliance on threat intelligence solutions to detect, prevent, and respond to these risks in real time. Moreover, regulatory frameworks like GDPR and PCI DSS mandate that these organizations implement robust security measures, further driving the demand for threat intelligence solutions.

In addition to protecting sensitive data, BFSI institutions must ensure the resilience of their operations, as cyberattacks can lead to service disruptions, financial losses, and reputational damage. As cyber threats become more sophisticated, BFSI companies are increasingly investing in advanced threat intelligence tools, making this segment the largest and most rapidly growing in the overall market.

Key Market Segments

By Component

- Solution

- Services

By Deployment

- Cloud

- On-premise

By Enterprise Size

- Large Enterprises

- SMEs

By Application

- Security Information and Event Management

- Governance

- Risk & Compliance

- Business Continuity Planning and Management

- Others

By End-use

- BFSI

- Government

- Healthcare

- IT & Telecom

- Manufacturing

- Retail

- Others

Driving Factors

Rising Cybersecurity Threats

One of the primary driving factors propelling the growth of the Threat Intelligence market is the increasing frequency and sophistication of cyberattacks. As businesses, governments, and individuals become more connected through digital platforms, cybercriminals have more opportunities to exploit vulnerabilities. High-profile data breaches, ransomware attacks, and phishing scams are becoming more common, prompting organizations to invest heavily in advanced threat intelligence solutions.

With industries such as BFSI, healthcare, IT, and government being prime targets due to the sensitive nature of their data, there is a heightened need for proactive security measures. Cybersecurity threats like ransomware can cripple operations, causing significant financial losses and damage to the brand’s reputation. As a result, companies are seeking out comprehensive threat intelligence solutions that allow them to identify, monitor, and respond to potential threats before they can cause harm.

Restraining Factors

High Implementation Costs

While the demand for threat intelligence solutions is growing, high implementation costs continue to act as a significant barrier for many organizations, particularly small and medium enterprises (SMEs). Integrating these sophisticated solutions often requires significant upfront investment in both hardware and software. In addition to the direct cost of purchasing threat intelligence platforms, organizations also need to factor in the costs of training staff, ongoing maintenance, and system upgrades.

For smaller organizations with limited budgets, these expenses may seem prohibitive, especially when there are other security tools available that appear to offer a lower-cost alternative. As such, SMEs may delay or forgo investing in comprehensive threat intelligence systems, even though they are highly vulnerable to cyberattacks. The complex integration process with existing systems and the need for skilled personnel to operate the tools effectively also contribute to these high costs.

Growth Opportunities

Integration of AI and Machine Learning

A significant growth opportunity for the Threat Intelligence market lies in the increasing integration of artificial intelligence (AI) and machine learning (ML) technologies into threat intelligence solutions. AI and ML allow for the automation of threat detection, analysis, and response, significantly improving the speed and accuracy of cybersecurity operations. These technologies can process massive amounts of data in real-time, identifying patterns and anomalies that could signal potential threats.

With the rise of advanced persistent threats (APTs) and highly sophisticated cyber-attacks, traditional manual detection methods are no longer sufficient. AI-powered systems, equipped with machine learning capabilities, are capable of learning from past incidents and constantly evolving to detect new threats without the need for constant human intervention. As a result, organizations can improve their incident response times, reduce human errors, and enhance overall security posture.

Challenging Factors

Data Privacy and Regulatory Compliance

One of the key challenges facing the Threat Intelligence market is the balance between data privacy and the need for comprehensive threat intelligence. As threat intelligence platforms rely on collecting and analyzing vast amounts of data from multiple sources—such as network traffic, user behavior, and external threat feeds—organizations must navigate the complex landscape of data privacy regulations and compliance standards.

Laws such as the General Data Protection Regulation (GDPR) in Europe, the California Consumer Privacy Act (CCPA), and the Health Insurance Portability and Accountability Act (HIPAA) impose stringent rules on the collection, storage, and processing of personal and sensitive data. Organizations that use threat intelligence tools must ensure that they are fully compliant with these regulations, or face severe penalties. This can limit the effectiveness of certain threat intelligence solutions that require the collection of large amounts of data across diverse networks.

Growth Factors

Increasing Cybersecurity Threats and Regulatory Pressures

The Threat Intelligence market is experiencing rapid growth due to the escalating frequency and sophistication of cyberattacks. As organizations face growing threats from ransomware, phishing, and APTs (Advanced Persistent Threats), there is an urgent need for proactive threat monitoring.

In 2023, cybercrime was projected to cost businesses USD 10.5 trillion annually, and these costs are only expected to increase, driving demand for more robust threat intelligence systems. Additionally, stricter regulatory frameworks, such as GDPR, CCPA, and HIPAA, require businesses to adopt advanced threat intelligence solutions to avoid hefty fines and ensure data protection. These regulatory pressures, combined with rising cybersecurity threats, are fueling market growth.

Emerging Trends

AI & Machine Learning Integration

One of the most notable emerging trends in the Threat Intelligence market is the integration of artificial intelligence (AI) and machine learning (ML) technologies into threat detection and response systems. As of 2024, AI-powered threat intelligence systems are becoming more common, improving the accuracy and speed of threat detection by automating processes that were once manually intensive.

AI and ML are helping organizations predict and respond to potential threats before they materialize. These technologies can sift through vast amounts of data in real-time, identifying patterns, anomalies, and emerging threats faster and more accurately than traditional methods.

Business Benefits

Enhanced Security and Operational Efficiency

Adopting threat intelligence solutions brings a multitude of business benefits. These solutions help companies identify, evaluate, and mitigate cyber threats in real-time, improving overall security posture. This proactive approach significantly reduces the risk of data breaches, financial losses, and reputational damage caused by cyberattacks. Additionally, threat intelligence platforms help optimize incident response times and allow organizations to prioritize threats based on their severity, which leads to more efficient resource allocation.

According to a recent report, companies using threat intelligence report a 30% reduction in response times to cyber incidents. Furthermore, the growing integration of AI and automation in threat intelligence systems reduces the reliance on manual intervention, improving operational efficiency. By embracing these technologies, organizations can stay ahead of cybercriminals while minimizing operational disruptions and maintaining compliance with evolving regulations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

BAE Systems has emerged as a leader in the Threat Intelligence market, offering comprehensive solutions to both government and private sector clients. The company focuses heavily on advanced cybersecurity and threat detection services through its Digital Intelligence division. In recent developments, BAE has continued to expand its capabilities in the cyber defense space through strategic acquisitions and partnerships.

Broadcom, through its acquisition of Symantec Corporation, has significantly enhanced its position in the Threat Intelligence market. Symantec’s well-established reputation for cybersecurity solutions was a major asset in Broadcom’s portfolio, expanding its reach in both enterprise and consumer cybersecurity products. Broadcom has continued to innovate within endpoint security and network security by integrating Symantec’s advanced threat intelligence capabilities into its offerings.

Check Point Software Technology Ltd. is a prominent player in the Threat Intelligence market, known for its cutting-edge cybersecurity solutions. The company specializes in providing comprehensive network security, endpoint protection, and cloud security services. Check Point’s products are designed to detect, prevent, and respond to cyber threats in real time, leveraging its vast expertise in cyber threat intelligence.

Top Key Players in the Market

- BAE Systems, Inc.

- Broadcom (Symantec Corporation)

- Broadcom (Symantec Corporation)

- Check Point Software Technology Ltd.

- Cisco Systems, Inc.

- FireEye, Inc.

- Fortinet, Inc.

- IBM Corporation

- Lockheed Martin Corporation

- LogRhythm, Inc.

- McAfee, LLC.

- Palo Alto Networks, Inc.

- Proofpoint, Inc.

- Sophos Ltd.

- Trend Micro Incorporated.

- Others

Recent Developments

- In 2024, Check Point Software Technologies launched a new version of its ThreatCloud security intelligence platform, further enhancing its AI-powered threat detection capabilities.

- In 2024, BAE Systems expanded its cybersecurity portfolio by acquiring Palo Alto Networks’ threat intelligence division.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 15.8 Billion |

| Forecast Revenue (2034) | USD 101.14 Billion |

| CAGR (2025-2034) | 20.40% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution, Services), By Deployment (Cloud, On-premise), By Enterprise Size (Large Enterprises, SMEs), By Application (Security Information and Event Management, Governance, Risk & Compliance, Business Continuity Planning and Management, Others), By End-use (BFSI, Government, Healthcare, IT & Telecom, Manufacturing, Retail, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | BAE Systems, Inc., Broadcom (Symantec Corporation), Check Point Software Technology Ltd., Cisco Systems, Inc., FireEye, Inc., Fortinet, Inc., IBM Corporation, Lockheed Martin Corporation, LogRhythm, Inc., McAfee, LLC., Palo Alto Networks, Inc., Proofpoint, Inc., Sophos Ltd., Trend Micro Incorporated., Others |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |