Global Core Network Observability Market Size, Share, Growth Analysis By Component (Solutions, Services), By Deployment Mode (On-Premises, Cloud), By Network Type (5G, 4G/LTE, 3G, Others), By End-User (Telecom Operators, Enterprises, Cloud Service Providers, Others), By Application (Performance Monitoring, Fault Management, Network Optimization, Security Monitoring, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 182457

- Number of Pages: 395

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Future Predictions

- Market Outlook

- Key Market Segments

- Research-Based Segments

- By Component

- By Deployment Mode

- By Network Type

- By End-User

- By Application

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

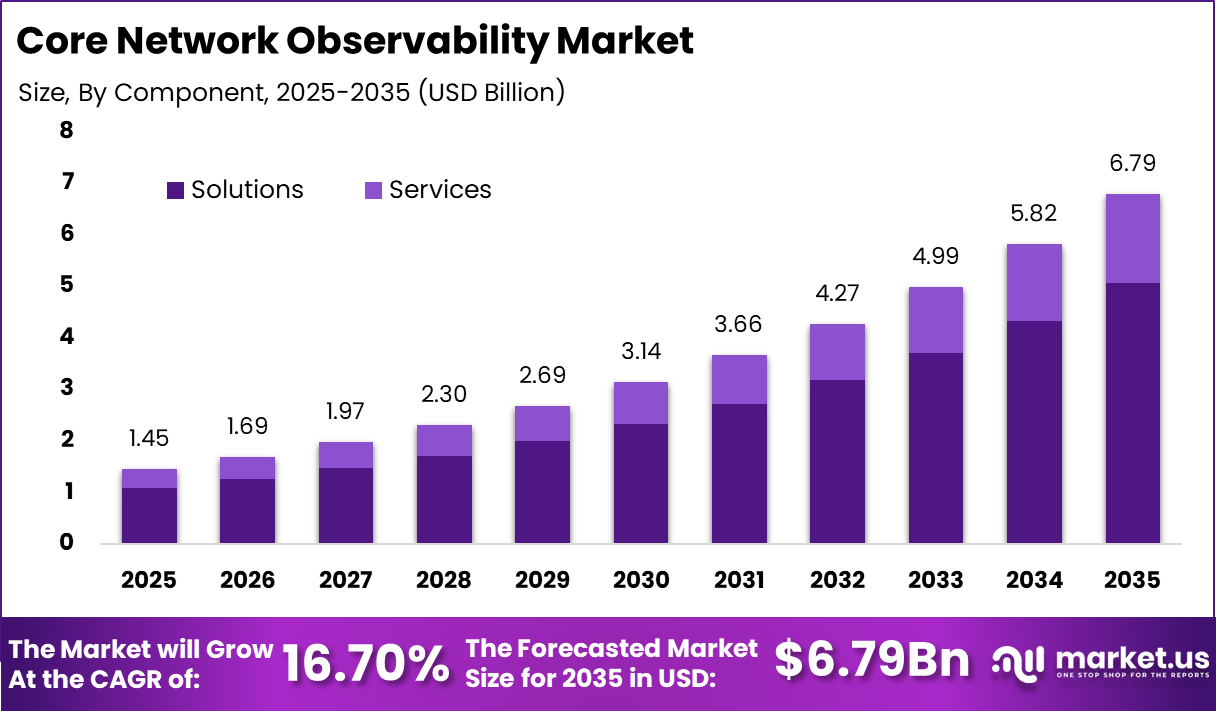

The Core Network Observability Market is gaining strong attention as telecom operators and enterprises place greater focus on real-time visibility, performance monitoring, and network reliability. In 2025, the market is valued at USD 1.45 billion and is projected to reach USD 6.79 billion by 2035, reflecting a steady CAGR of 16.7%. This growth outlook aligns with increasing data traffic, 5G expansion, and the rising complexity of distributed network environments, which require advanced observability solutions for efficient operations.

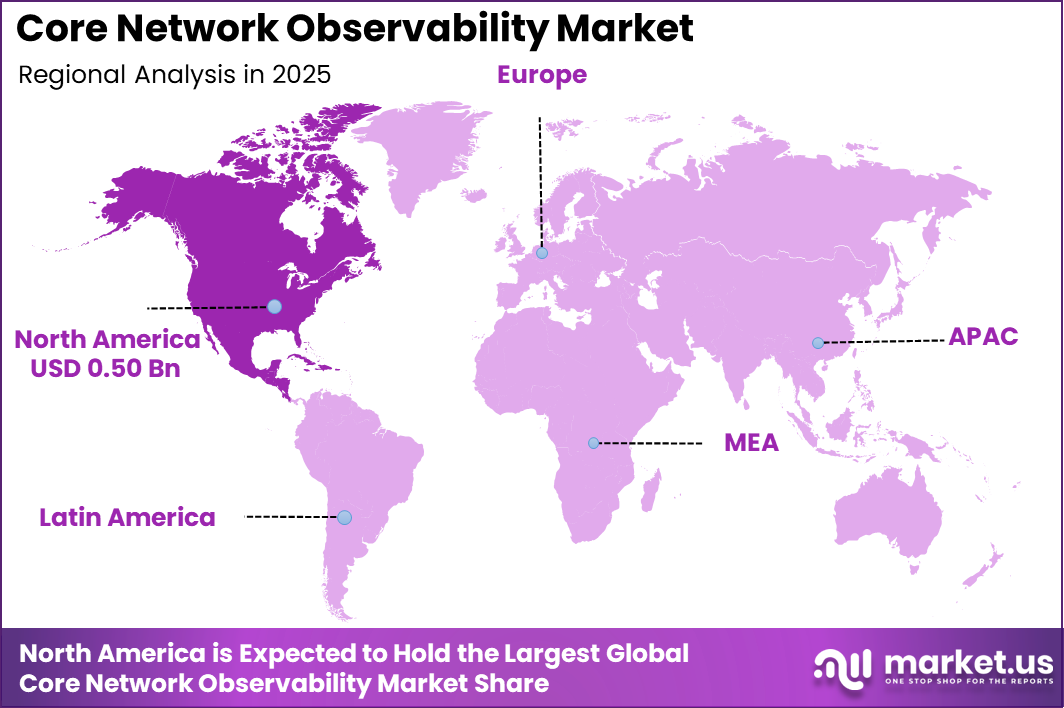

From a regional perspective, North America holds a leading position with a 34.5% share, accounting for approximately USD 0.50 billion in 2025. The region benefits from early adoption of advanced network technologies, strong telecom infrastructure, and continuous investments in cloud-native architectures.

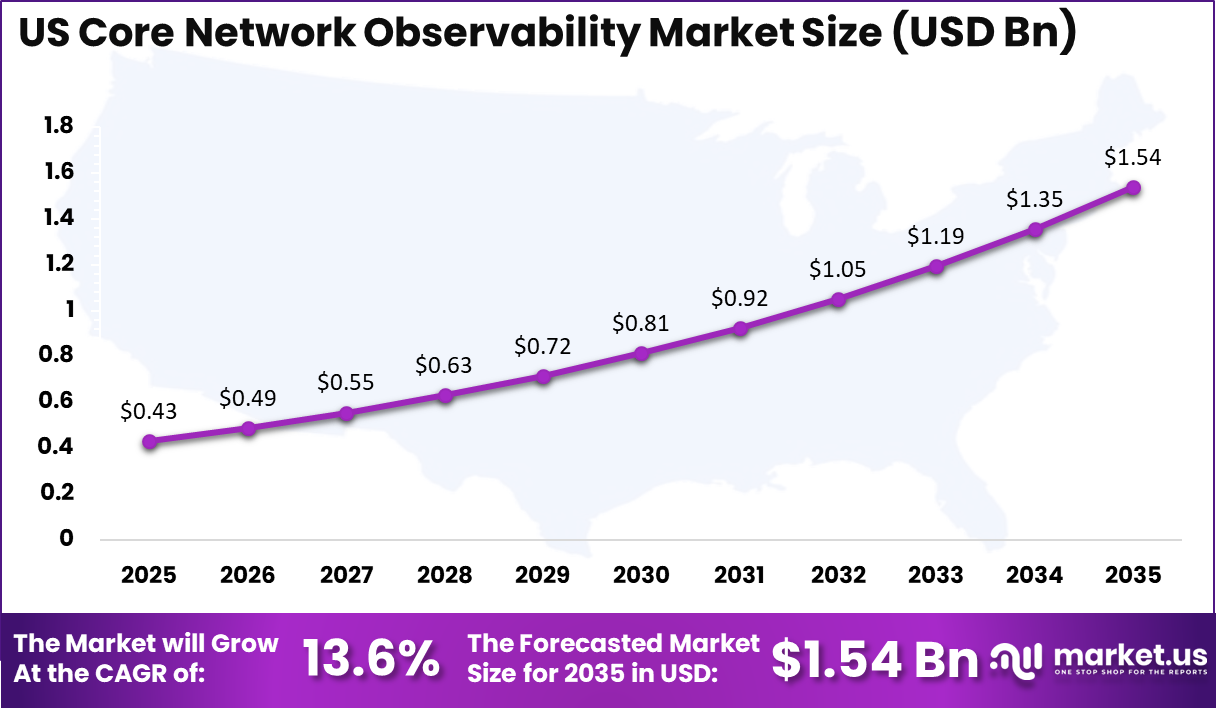

Within North America, the US represents a significant portion of the market, valued at USD 0.43 Billion in 2025 and projected to reach USD 1.54 billion by 2035, growing at a CAGR of 13.6%. This growth is supported by the presence of major telecom providers, increasing demand for automated network monitoring, and the need to manage complex hybrid and multi-cloud environments.

Global telecom data traffic continues to expand rapidly, creating strong demand for core network observability solutions. According to Ericsson Mobility Report, global mobile data traffic crossed 130 exabytes per month in 2023 and is anticipated to exceed 400 exabytes per month by 2029, driven by video streaming, IoT devices, and 5G adoption. This sharp increase in traffic is placing pressure on core networks, making real-time monitoring and analytics essential.

Deployment of 5G technology is another key contributor. Data from GSMA indicates that 5G connections surpassed 1.6 billion globally in 2024 and are projected to account for more than half of all mobile connections by 2030. This shift toward high-speed networks is increasing network complexity and requiring advanced observability tools to maintain service quality.

In the US, telecom investment remains strong. Federal Communications Commission data highlights that broadband and network infrastructure investments exceeded USD 90 billion annually in recent years. Additionally, cloud adoption is accelerating, with International Data Corporation reporting that over 70% of enterprises now rely on hybrid or multi-cloud environments. These trends collectively reinforce the need for continuous network visibility, fault detection, and performance optimization across core networks.

Core Key Insights

- Global market size in 2025: USD 1.45 billion, projected to reach USD 6.79 billion by 2035, reflecting strong long-term expansion.

- Overall market growth rate: 16.7% cagr, supported by rising network complexity and data traffic.

- North America: 34.5% share, valued at USD 0.50 billion in 2025, indicating leading regional adoption.

- US market: USD 0.43 billion in 2025, projected to reach USD 1.54 billion by 2035, growing at 13.6% cagr.

- By component: solutions: 74.5%, indicating a higher demand for software-driven observability platforms over services.

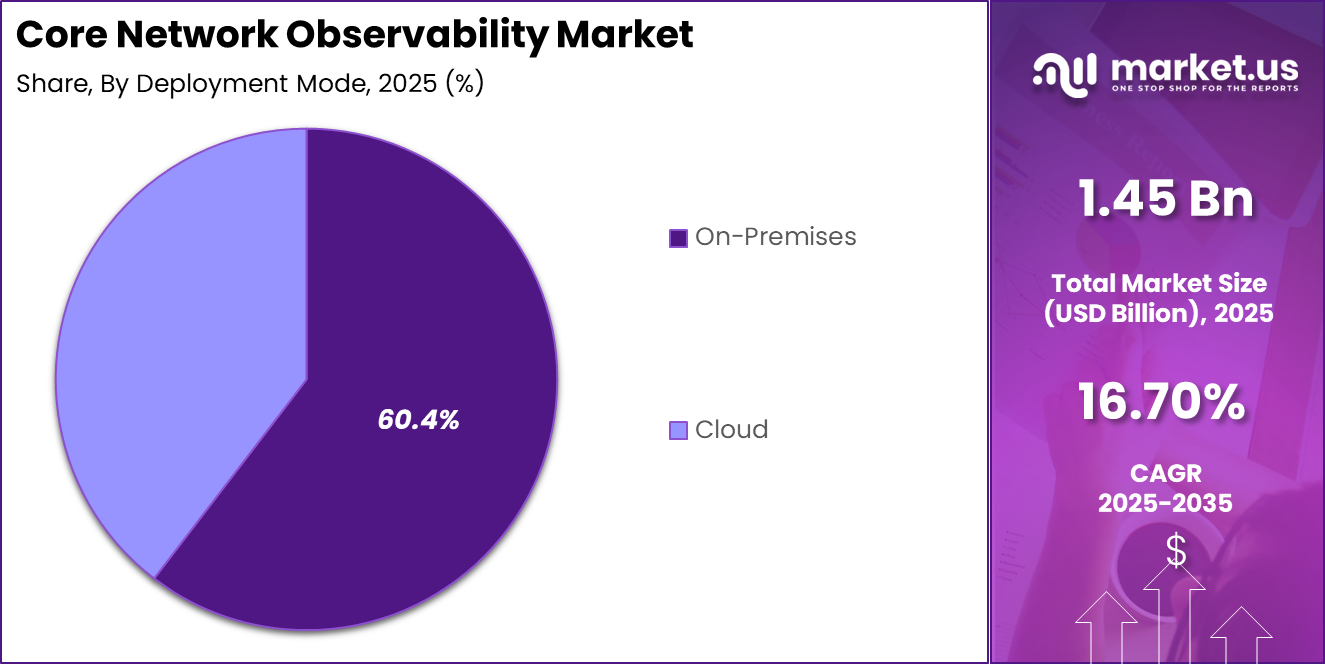

- By deployment mode: on-premises: 60.4%, reflecting preference for control, security, and legacy integration.

- By network type: 4g/LTE: 39.3%, showing continued reliance on existing network infrastructure alongside 5G transition.

- By end-user: telecom operators: 45.6%, highlighting their dominant role in managing and optimizing core networks.

- By application: performance monitoring: 42.4%, driven by the need for real-time visibility, fault detection, and service quality assurance.

Future Predictions

The future of the Core Network Observability Market is closely tied to the rapid expansion of global data traffic, connected devices, and next-generation networks. Global mobile network traffic reached nearly 200 exabytes per month in 2025 and is expected to scale significantly as digital services expand.

Internet traffic is also rising sharply, with total global traffic approaching 1.3 zettabytes annually, reflecting growing pressure on core network infrastructure. This surge in data volumes is expected to accelerate the need for real-time observability, anomaly detection, and predictive analytics across telecom networks.

The increasing adoption of 5G and IoT will further reshape the market landscape. Around 3 billion 5G subscriptions are already active globally, covering over half of the world’s population, and this footprint is expected to expand rapidly. At the same time, connected IoT devices are projected to grow from 18.5 billion in 2024 to nearly 39 billion by 2030.

Significantly increasing network endpoints and monitoring complexity. With mobile data traffic growing at around 20% annually and 5G expected to carry nearly 80% of traffic by 2030, network operators are expected to invest heavily in advanced observability platforms to ensure performance, security, and service continuity.

Market Outlook

The Core Network Observability Market is expected to witness steady expansion as telecom ecosystems become more complex and data-intensive. The growing reliance on digital services such as video streaming, cloud applications, and real-time communication is increasing pressure on network performance.

As operators manage higher traffic loads and more distributed architectures, the need for continuous visibility across core networks is expected to strengthen, supporting long-term market growth. The transition toward cloud-native and virtualized network functions is also shaping the market outlook.

Telecom providers are gradually moving from traditional hardware-based systems to software-defined and containerized environments, which require advanced observability tools for monitoring and troubleshooting. This shift is expected to drive the adoption of intelligent platforms that can provide end-to-end visibility across hybrid and multi-cloud infrastructures.

In addition, the expansion of 5G networks and edge computing is expected to further accelerate demand. These technologies introduce new layers of complexity, including network slicing and low-latency applications, making real-time monitoring critical for service assurance.

Enterprises are also increasing investments in private networks and digital transformation, which is expected to create new opportunities for observability solutions beyond telecom operators. Overall, the market outlook remains positive, supported by continuous innovation, rising network complexity, and the growing importance of maintaining high service quality and operational efficiency.

Key Market Segments

The solutions segment accounted for 74.5% of the market, reflecting the strong demand for advanced software platforms that enable real-time monitoring, analytics, and fault detection across core networks. This dominance is supported by the increasing need for centralized visibility and automation as network architectures become more complex with virtualization and cloud integration. Solutions are expected to remain the primary revenue contributor as telecom operators prioritize intelligent observability tools over standalone services.

On-premises deployment held 60.4% share, driven by the preference for greater control over sensitive network data and infrastructure. Many telecom operators continue to rely on legacy systems that require localized deployment for integration and security compliance. This segment is expected to maintain its relevance, although gradual adoption of cloud-based models is anticipated as operators modernize their infrastructure.

4G/LTE accounted for 39.3% of the market, indicating the continued reliance on existing network infrastructure despite the expansion of 5G. A large portion of global telecom networks still operates on 4G/LTE, requiring consistent monitoring and optimization. This segment is expected to sustain demand as operators manage coexistence between legacy and next-generation networks.

Telecom operators represented 45.6% of end-users, as they are the primary stakeholders responsible for maintaining network performance and service quality. Their investments in observability platforms are expected to grow with increasing subscriber bases and data consumption.

Performance monitoring led applications with 42.4%, driven by the need for real-time insights, proactive issue detection, and improved user experience across core network environments.

Research-Based Segments

By Component

- Solutions

- Services

By Deployment Mode

- On-Premises

- Cloud

By Network Type

- 5G

- 4G/LTE

- 3G

- Others

By End-User

- Telecom Operators

- Enterprises

- Cloud Service Providers

- Others

By Application

- Performance Monitoring

- Fault Management

- Network Optimization

- Security Monitoring

- Others

By Component

The solutions segment accounted for 74.5% of the market, highlighting its dominant role in enabling comprehensive visibility and control across core network environments. This dominance is driven by the increasing complexity of telecom infrastructure, where operators require integrated platforms for real-time monitoring, analytics, and automated fault detection.

Solutions offer centralized dashboards, AI-driven insights, and predictive capabilities, which are expected to enhance operational efficiency and reduce downtime. As networks evolve with virtualization and cloud-native architectures, demand for scalable and intelligent observability solutions is anticipated to remain strong.

The services segment holds a comparatively smaller share but continues to play a critical supporting role in the market. These services include consulting, system integration, deployment, and ongoing support, which help organizations effectively implement and optimize observability platforms. As telecom operators upgrade legacy systems and adopt new technologies, the need for specialized expertise is expected to grow.

Managed services are also gaining traction as companies seek to outsource monitoring and maintenance tasks to improve efficiency. While solutions lead in revenue generation, services are projected to expand steadily by enabling seamless adoption, customization, and long-term performance management of observability frameworks.

By Deployment Mode

The on-premises segment accounted for 60.4% of the market, reflecting the strong preference among telecom operators for maintaining direct control over core network infrastructure and sensitive data. This dominance is driven by strict regulatory requirements, data security concerns, and the need to integrate with legacy systems that are deeply embedded within telecom environments.

On-premises deployment enables operators to ensure higher reliability, lower latency, and customized configurations, which are critical for managing large-scale network operations. As core networks continue to handle mission-critical services, this segment is expected to retain a significant share despite ongoing digital transformation efforts.

The cloud segment is gaining momentum as operators gradually shift toward more flexible and scalable network management models. Cloud-based deployment allows faster implementation, reduced infrastructure costs, and improved accessibility across distributed network environments. It supports advanced capabilities such as real-time analytics, AI-driven monitoring, and seamless updates without heavy capital investment.

As telecom companies adopt cloud-native architectures and virtualized network functions, the demand for cloud-based observability is anticipated to grow steadily. While currently smaller in share, the cloud segment is expected to expand at a faster pace, driven by increasing adoption of hybrid and multi-cloud strategies across the telecom ecosystem.

By Network Type

The 4G/LTE segment accounted for 39.3% of the market, reflecting its continued dominance as the backbone of global telecom infrastructure. A large share of mobile users and enterprise applications still rely on 4G/LTE networks, which require consistent monitoring to maintain performance and service quality. Telecom operators are expected to continue investing in observability solutions to manage traffic loads, optimize network efficiency, and support the coexistence of legacy and next-generation systems.

The 5G segment is gaining strong traction as operators expand next-generation network deployments. The increasing adoption of use cases such as ultra-low latency applications, network slicing, and connected devices is driving the need for advanced observability tools. These solutions are expected to help operators monitor complex, software-defined environments and ensure seamless service delivery. As 5G coverage expands globally, this segment is anticipated to grow at a faster pace compared to traditional networks.

The 3G segment is gradually declining as many regions phase out older network technologies. However, it still holds relevance in certain developing markets where infrastructure upgrades are ongoing. Observability tools continue to support these networks to maintain basic connectivity and service continuity until full migration to newer technologies is achieved.

The other segment includes emerging and specialized network types such as private networks and early-stage technologies. This segment is expected to witness gradual growth as enterprises adopt customized network solutions that require dedicated monitoring and performance management capabilities.

By End-User

The telecom operators segment accounted for 45.6% of the market, reflecting their central role in managing and maintaining core network infrastructure. This dominance is driven by the continuous need to monitor network performance, ensure service reliability, and handle increasing data traffic across large subscriber bases. Telecom operators are expected to invest heavily in observability platforms to gain real-time insights, reduce downtime, and optimize network efficiency as architectures become more complex.

The enterprises segment is gaining importance as organizations adopt private networks and digital transformation strategies. Businesses across industries are increasingly deploying advanced communication systems and require visibility into network performance to support critical operations. Observability solutions are expected to help enterprises manage hybrid environments, improve application performance, and enhance user experience, driving steady growth in this segment.

Cloud service providers represent a growing segment due to the expansion of cloud-native infrastructure and multi-cloud environments. These providers require advanced monitoring tools to ensure uptime, manage workloads, and deliver consistent service quality to clients. As cloud adoption accelerates, the need for scalable and automated observability solutions is anticipated to increase significantly within this segment.

The other segment includes government organizations, system integrators, and smaller network operators that require basic to advanced monitoring capabilities. This segment is expected to witness gradual growth as digital infrastructure expands and more entities seek reliable network visibility and performance management solutions.

By Application

The performance monitoring segment accounted for 42.4% of the market, reflecting its critical role in ensuring real-time visibility into network performance and service quality. Telecom operators and enterprises rely on these solutions to track latency, throughput, and user experience across complex network environments. This dominance is driven by the need to detect issues early, maintain uptime, and support high data traffic, especially with the growing adoption of cloud and next-generation networks.

The fault management segment plays a vital role in identifying, isolating, and resolving network issues before they impact end users. As network architectures become more distributed and software-driven, the need for automated fault detection and root cause analysis is expected to increase. This segment is anticipated to grow steadily as organizations focus on minimizing service disruptions and improving operational efficiency.

The network optimization segment is gaining traction as operators aim to improve resource utilization and enhance overall network performance. Observability tools help in analyzing traffic patterns, balancing loads, and optimizing bandwidth usage. This segment is expected to expand as telecom providers seek to deliver consistent and high-quality services across increasingly complex infrastructures.

The security monitoring segment is becoming increasingly important due to rising cyber threats and vulnerabilities in telecom networks. Observability platforms are expected to support threat detection, anomaly identification, and compliance monitoring. As network security becomes a top priority, this segment is anticipated to witness strong growth.

The other segment includes applications such as capacity planning and predictive analytics, which are expected to grow gradually as organizations adopt more proactive network management strategies.

Regional Analysis

North America accounted for 34.5% of the market, with a value of USD 0.50 billion in 2025, reflecting its leading position in the Core Network Observability Market. This dominance is supported by the region’s advanced telecom infrastructure and early adoption of next-generation technologies.

Telecom operators in the region are actively investing in network modernization, virtualization, and cloud-native architectures, which is expected to increase the demand for real-time monitoring and observability solutions.

The presence of large-scale data centers, high internet penetration, and strong digital transformation initiatives across industries further strengthens market growth in the region. Organizations are increasingly relying on high-performance networks to support applications such as streaming, cloud computing, and enterprise communication, which is expected to drive the need for continuous network visibility and performance optimization.

In addition, the rapid rollout of 5G networks and increasing adoption of edge computing are expected to create new opportunities for observability platforms. These technologies introduce higher network complexity, requiring advanced tools for fault detection, traffic analysis, and service assurance.

The US plays a major role within the region, supported by significant investments in telecom infrastructure and innovation. Overall, North America is expected to maintain its leadership due to strong technological capabilities, continuous investments, and the growing importance of maintaining network reliability and efficiency.

US Market Size

The US Core Network Observability Market was valued at USD 0.43 billion in 2025 and is projected to reach USD 1.54 billion by 2035, growing at a CAGR of 13.6%. This steady growth reflects the country’s strong focus on advanced telecom infrastructure and continuous investments in network modernization. Telecom operators across the US are expanding their capabilities to manage increasing data traffic, which is expected to drive demand for real-time monitoring and observability solutions.

The rapid adoption of cloud-native technologies and virtualization is transforming how networks are managed in the US. Operators are shifting toward software-defined architectures, which require enhanced visibility and analytics to ensure performance and reliability. This transition is expected to accelerate the adoption of intelligent observability platforms that support automation and predictive insights.

Additionally, the expansion of 5G networks and edge computing is contributing to market growth. These technologies introduce greater network complexity, making continuous monitoring essential for maintaining service quality. Enterprises are also increasing investments in private networks and digital infrastructure, further supporting demand.

The presence of a mature technology ecosystem and strong innovation capabilities is expected to keep the US at the forefront of adopting advanced observability solutions, ensuring sustained market expansion over the forecast period.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The primary driver for the Core Network Observability Market is the rapid surge in global data traffic and connected devices. According to Ericsson, mobile data traffic exceeded 130 exabytes per month in 2023 and is expected to grow nearly threefold by the end of the decade. This sharp increase is putting pressure on telecom core networks to maintain performance and reliability.

At the same time, over 5.4 billion people are using the internet globally, as reported by the International Telecommunication Union, further increasing demand for seamless connectivity. Telecom operators are required to monitor network behavior in real time to avoid congestion and downtime.

Additionally, the growth of cloud services and streaming platforms is generating higher traffic loads across networks. These factors are expected to drive the adoption of advanced observability tools that provide real-time insights, predictive analytics, and automated responses, enabling operators to maintain service quality and improve operational efficiency.

Restraint Factors

One of the key restraints in the Core Network Observability Market is the high complexity involved in integrating observability tools with existing legacy systems. Many telecom networks still rely on older infrastructure that was not designed for modern analytics or real-time monitoring.

According to GSMA, a significant portion of global telecom infrastructure still operates on 4G and earlier technologies, creating compatibility challenges when deploying new solutions. Additionally, the cost of upgrading infrastructure and deploying advanced observability platforms can be substantial, especially for smaller operators.

Cybersecurity concerns also act as a barrier, as increased monitoring requires access to sensitive network data. Organizations must ensure compliance with strict data protection regulations, which can slow down implementation. The shortage of skilled professionals capable of managing advanced observability tools further adds to the challenge. These factors collectively restrict faster adoption, particularly in developing regions where infrastructure modernization is still in progress.

Growth Opportunities

The expansion of 5G networks and the Internet of Things presents significant growth opportunities for the Core Network Observability Market. According to GSMA, 5G connections are expected to surpass 2 billion globally in the coming years, creating more complex and dynamic network environments.

At the same time, IoT Analytics estimates that the number of connected IoT devices could reach around 40 billion by 2030. This rapid increase in endpoints is expected to generate vast amounts of network data that require continuous monitoring and analysis. Observability platforms are anticipated to play a critical role in managing these complex ecosystems by providing real-time visibility and automated insights.

Additionally, enterprises are increasingly deploying private 5G networks and edge computing solutions, which further expands the need for advanced monitoring tools. These trends are expected to create new revenue opportunities for solution providers and drive innovation in analytics, automation, and AI-driven observability capabilities.

Trending Factors

A major trend shaping the Core Network Observability Market is the growing adoption of artificial intelligence and automation in network management. Telecom operators are increasingly using AI-based tools to analyze network data, predict failures, and optimize performance.

According to International Data Corporation, global spending on AI systems is expected to exceed USD 300 billion within the next few years, indicating strong momentum in AI-driven technologies. Another important trend is the shift toward cloud-native and software-defined networking, which allows operators to manage networks more flexibly and efficiently.

The rise of edge computing is also influencing observability strategies, as data processing moves closer to end users. This requires decentralized monitoring solutions capable of handling distributed environments. Furthermore, there is an increasing focus on real-time analytics and user experience monitoring, as service quality becomes a key differentiator. These trends are expected to reshape how telecom networks are managed, making observability a core component of future network operations.

Competitive Analysis

The competitive landscape of the Core Network Observability Market is moderately fragmented, with a mix of telecom equipment providers, network analytics vendors, and software-driven observability platforms competing for market share.

The broader network monitoring ecosystem, which includes observability solutions, was valued at over USD 3.4 billion in 2026 and is expected to cross USD 5.2 billion by 2031, indicating strong vendor activity and continuous innovation. This environment encourages companies to differentiate through AI-driven analytics, automation, and real-time performance insights.

Leading players such as Cisco Systems, Nokia, Ericsson, and Juniper Networks are focusing on integrating observability into their broader telecom and cloud portfolios. These companies leverage large-scale telecom contracts and infrastructure capabilities to maintain a competitive advantage. At the same time, specialized vendors such as SolarWinds and IBM are expanding their presence through advanced analytics platforms and hybrid cloud monitoring solutions.

Competition is increasingly driven by technological differentiation rather than pricing. Vendors are investing heavily in AI-based monitoring, with industry data indicating that nearly 30% of enterprises are automating a significant portion of network operations.

Strategic partnerships, acquisitions, and integration with cloud ecosystems are also shaping the competitive dynamics. Overall, the market is expected to remain innovation-driven, with companies focusing on scalability, automation, and real-time intelligence to strengthen their positioning.

Top Key Players in the Market

- Cisco Systems

- Ericsson

- Nokia

- Huawei Technologies

- Juniper Networks

- NetScout Systems

- Spirent Communications

- Keysight Technologies

- VIAVI Solutions

- Amdocs

- EXFO

- Ribbon Communications

- Sandvine

- Radcom

- Anritsu Corporation

- Accedian

- Infovista

- Teoco Corporation

- Comarch

- Polystar (part of Elisa Polystar)

- Others

Recent Developments

- In 2025, enterprise investment in AI-driven network operations is expected to rise sharply, with more than 40% of telecom operators adopting automation tools to improve network efficiency and reduce downtime.

- In 2025, the number of connected IoT devices is expected to reach over 20 billion globally, significantly increasing the volume of network endpoints that require continuous monitoring and performance management.

- In 2024, global spending on cloud infrastructure exceeded USD 300 billion, reflecting growing reliance on hybrid and multi-cloud environments that require advanced network observability and monitoring solutions.

Report Scope

Report Features Description Market Value (2025) USD 1.45 Billion Forecast Revenue (2035) USD 6.79 Billion CAGR(2025-2035) 16.70% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Component (Solutions, Services), By Deployment Mode (On-Premises, Cloud), By Network Type (5G, 4G/LTE, 3G, Others), By End-User (Telecom Operators, Enterprises, Cloud Service Providers, Others), By Application (Performance Monitoring, Fault Management, Network Optimization, Security Monitoring, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Cisco Systems, Ericsson, Nokia, Huawei Technologies, Juniper Networks, NetScout Systems, Spirent Communications, Keysight Technologies, VIAVI Solutions, Amdocs, EXFO, Ribbon Communications, Sandvine, Radcom, Anritsu Corporation, Accedian, Infovista, Teoco Corporation, Comarch, Polystar (part of Elisa Polystar), Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Core Network Observability MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Core Network Observability MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Cisco Systems

- Ericsson

- Nokia

- Huawei Technologies

- Juniper Networks

- NetScout Systems

- Spirent Communications

- Keysight Technologies

- VIAVI Solutions

- Amdocs

- EXFO

- Ribbon Communications

- Sandvine

- Radcom

- Anritsu Corporation

- Accedian

- Infovista

- Teoco Corporation

- Comarch

- Polystar (part of Elisa Polystar)

- Others

Our Clients

- 182457

- Mar 2026