Global Combat Aircraft Swarm Radars Market Size, Share, Growth Analysis By Radar Type (AESA (Active Electronically Scanned Array), PESA (Passive Electronically Scanned Array), Hybrid AESA-PESA, Phased Array with AI-Assisted Swarm Detection, Others), By Platform (Manned, Unmanned), By Frequency Band (X Band, L Band, S Band, C Band, Ku Band), By Application (Swarm Detection and Counter-UAS, Air-to-Air Target Tracking, Terrain Following and Obstacle Avoidance, Electronic Warfare Support, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183407

- Number of Pages: 352

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

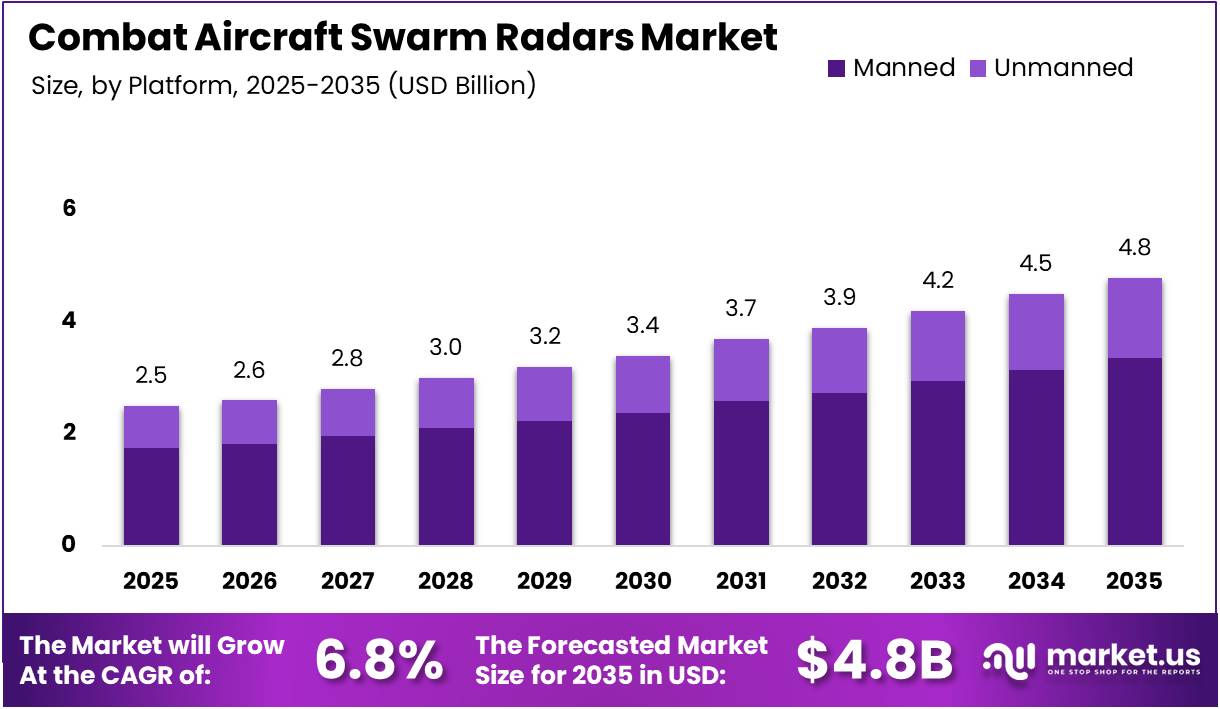

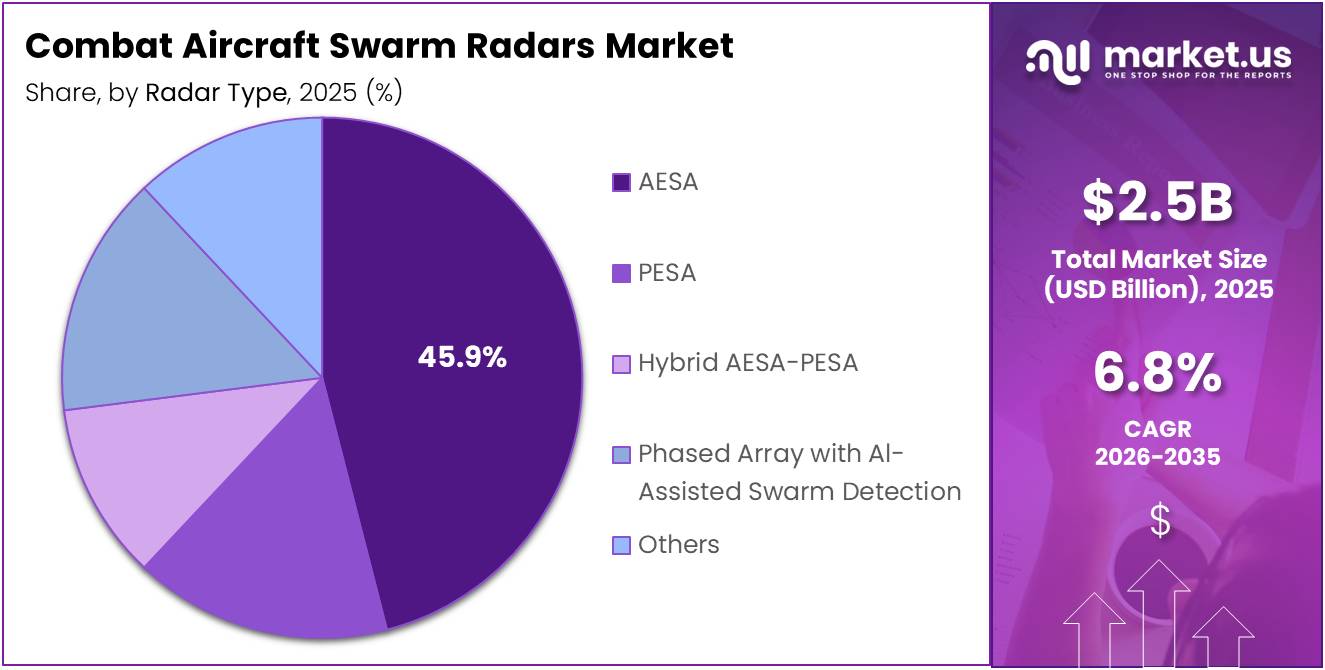

The Global Combat Aircraft Swarm Radars Market size is expected to be worth around USD 4.8 Billion by 2035 from USD 2.5 Billion in 2025, growing at a CAGR of 6.8% during the forecast period 2026 to 2035.

Combat aircraft swarm radars are advanced sensor systems designed to detect, track, and neutralize multiple simultaneous aerial targets, including drone swarms and coordinated unmanned aerial vehicles. These systems use phased array and electronically scanned antenna technologies. Moreover, they deliver real-time situational awareness to support both offensive and defensive air combat operations.

The growing prevalence of drone swarm tactics in modern warfare has made swarm radar technology a critical priority for defense programs worldwide. Military forces now require systems capable of tracking hundreds of airborne targets simultaneously. Consequently, defense agencies are accelerating procurement of next-generation radar solutions for combat aircraft platforms.

Governments across North America, Europe, and Asia Pacific are substantially increasing defense budgets to counter advanced aerial threats. Regulatory frameworks now emphasize domestic radar technology development and faster procurement cycles. Additionally, several nations have launched structured upgrade programs targeting radar systems on both manned and unmanned combat aircraft.

The integration of artificial intelligence into radar signal processing is transforming swarm detection capabilities across modern combat platforms. AI-enabled radar systems can autonomously identify and classify threats in real time. Furthermore, network-centric warfare doctrines require cooperative radar architectures that share live threat data across multiple aircraft and ground command systems.

According to IEEE Xplore, radar micro-Doppler based swarm detection and classification systems achieve 90–96% accuracy in controlled experiments. This level of precision is critical in combat environments where target misidentification carries serious operational risks. Therefore, defense programs are increasingly mandating micro-Doppler radar integration as a standard requirement in next-generation swarm radar contracts.

According to DRDO, modern AESA radars consist of approximately 1,000–2,000 transmit/receive modules and can detect targets at 50 nautical miles or more. Additionally, GaN-based T/R modules deliver up to 400 W of output power per module. These technical benchmarks highlight the high performance standards driving sustained investment across the global combat aircraft swarm radars market.

Key Takeaways

- The global Combat Aircraft Swarm Radars Market is valued at USD 2.5 Billion in 2025 and is projected to reach USD 4.8 Billion by 2035.

- The market is expected to grow at a CAGR of 6.8% during the forecast period 2026 to 2035.

- By Radar Type, AESA (Active Electronically Scanned Array) dominates the market with a 45.9% share in 2025.

- By Platform, the Manned segment holds the largest market share at 69.2% in 2025.

- By Frequency Band, X Band leads the market with a 38.4% share in 2025.

- By Application, Swarm Detection and Counter-UAS holds the dominant position with a 41.8% share in 2025.

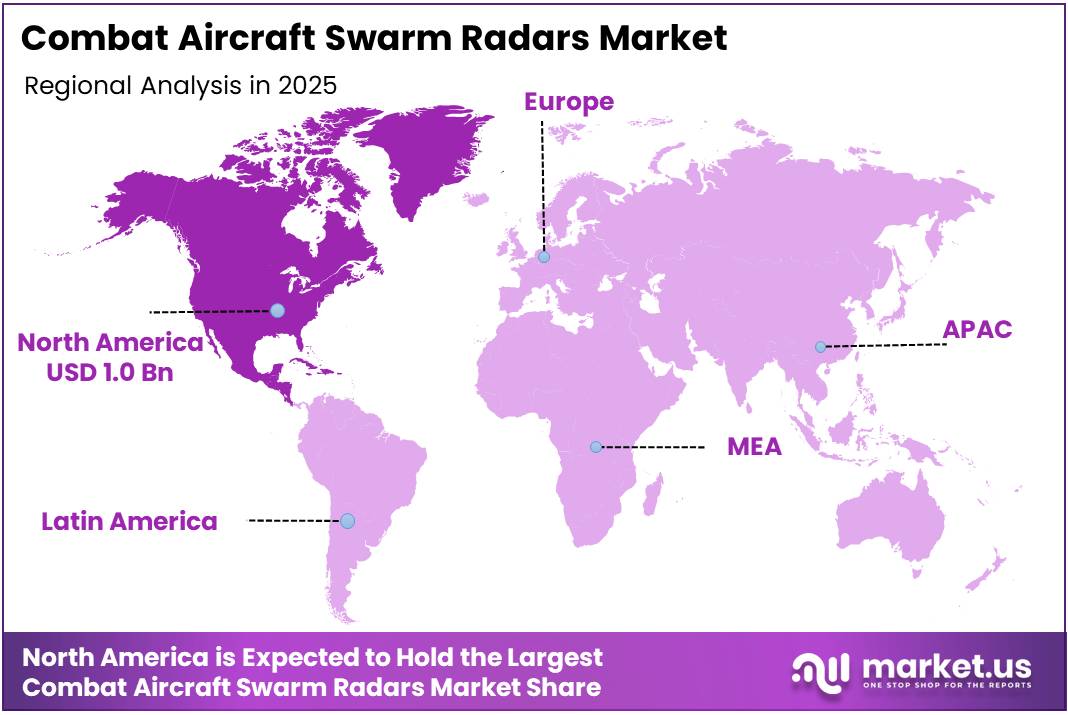

- North America dominates the regional market with a 43.70% share, valued at approximately USD 1.0 Billion in 2025.

Radar Type Analysis

AESA dominates with 45.9% due to superior beam steering agility and compatibility with AI-enabled signal processing architectures.

In 2025, AESA (Active Electronically Scanned Array) held a dominant market position in the By Radar Type segment of the Combat Aircraft Swarm Radars Market, with a 45.9% share. AESA systems offer high-speed electronic beam steering, reduced maintenance requirements, and seamless integration with AI-based signal processing. Consequently, they remain the preferred radar architecture for advanced combat aircraft programs globally.

PESA (Passive Electronically Scanned Array) systems represent a widely deployed radar type in mid-tier and legacy combat aircraft platforms. These systems offer reliable performance at comparatively lower procurement costs. However, their fixed phase shifter architecture limits adaptability for highly dynamic swarm threat detection scenarios compared to active array technologies.

Hybrid AESA-PESA configurations combine the cost management advantages of passive array systems with the enhanced performance of active array architectures. These systems are gaining traction among defense programs that must balance procurement budgets with operational capability improvements. Moreover, hybrid architectures support phased upgrade pathways for existing combat aircraft without requiring full platform replacement.

Phased Array with AI-Assisted Swarm Detection is an emerging radar type that integrates conventional phased array hardware with intelligent signal processing algorithms. These systems support adaptive scanning patterns and real-time swarm formation analysis. Additionally, they represent a growing area of research and development investment among leading defense electronics manufacturers worldwide.

Others category includes legacy radar technologies and experimental systems addressing specialized operational requirements not covered by primary radar types. These systems hold a limited combined market share. However, niche defense programs and ongoing technology trials continue to sustain demand for non-standard radar configurations in specific combat applications.

Platform Analysis

Manned dominates with 69.2% due to higher radar payload capacity and established integration across global combat aircraft fleets.

In 2025, Manned platforms held a dominant market position in the By Platform segment of the Combat Aircraft Swarm Radars Market, with a 69.2% share. Manned combat aircraft offer significantly higher radar payload capacity, sustained operational endurance, and greater mission flexibility. Consequently, they continue to represent the primary platform for advanced swarm radar system integration across major defense programs worldwide.

Unmanned platforms are emerging as a rapidly growing segment within the combat aircraft swarm radars market. UCAV programs increasingly require embedded swarm detection capabilities to support autonomous air combat and counter-drone operations. Moreover, ongoing advances in miniaturized radar technology are enabling high-performance swarm detection systems that are increasingly suitable for unmanned aerial vehicle integration.

Frequency Band Analysis

X Band dominates with 38.4% due to high resolution target discrimination and broad integration across airborne fire control radar systems.

In 2025, the X Band held a dominant market position in the By Frequency Band segment of the Combat Aircraft Swarm Radars Market, with a 38.4% share. X Band radars provide high spatial resolution and precise multi-target discrimination essential for swarm detection. Consequently, they are the most widely integrated frequency band in airborne fire control and combat radar systems globally.

The L Band is commonly used for long-range surveillance and early warning functions within combat radar architectures. L Band signals offer superior performance under adverse weather conditions and at extended detection ranges. Therefore, this frequency band is often applied in airborne early warning platforms and ground-based surveillance radar programs.

The S Band occupies a balanced position between long-range surveillance and high-resolution target tracking within combat radar systems. S Band radars are valued for their effective performance across both search and tracking operational requirements. Moreover, they are increasingly integrated into multi-function radar systems supporting comprehensive air situation awareness.

The C Band is used in select airborne radar applications where moderate range and resolution requirements must be balanced against platform size and weight constraints. C Band systems support certain precision approach and weather radar applications. Additionally, ongoing research programs are exploring C Band potential for tactical swarm detection in unmanned platform configurations.

The Ku Band supports high-resolution, short-range radar applications and is used in smaller airborne platforms and emerging compact radar technologies. Ku Band systems offer compact form factors well suited for unmanned aerial vehicles. However, their susceptibility to atmospheric signal attenuation limits operational utility in long-range swarm detection mission profiles.

Application Analysis

Swarm Detection and Counter-UAS dominates with 41.8% due to rapid drone threat proliferation and accelerating counter-UAS procurement programs globally.

In 2025, Swarm Detection and Counter-UAS held a dominant market position in the ‘By Application’ segment of the Combat Aircraft Swarm Radars Market, with a 41.8% share. The rapid proliferation of coordinated drone swarms in modern conflict has made counter-UAS detection the most critical radar application for combat aircraft. Consequently, defense programs worldwide are prioritizing investment in dedicated swarm detection and neutralization capabilities.

Air-to-Air Target Tracking remains a foundational application for combat aircraft radar systems supporting beyond-visual-range engagement scenarios. These systems enable simultaneous tracking of multiple airborne threats during complex air combat operations. Moreover, AI-enhanced signal processing is improving multi-target tracking precision and reducing radar response times in high-threat engagement environments.

Terrain Following and Obstacle Avoidance radar applications support low-altitude penetration missions and autonomous navigation in contested airspace. These systems enable combat aircraft and UCAVs to operate safely at high speeds over complex terrain. Additionally, they are critical enablers for stealth operations requiring precise low-level flight path management to avoid radar detection.

Electronic Warfare Support applications integrate radar sensing capabilities with electronic intelligence gathering functions. These systems detect and characterize enemy radar emissions to support electronic jamming and countermeasure operations. Furthermore, the convergence of radar and electronic warfare functions is driving demand for unified sensor suites across advanced multi-role combat aircraft platforms.

Others category encompasses specialized radar applications addressing emerging and mission-specific operational requirements across combat aviation. These include maritime surveillance coordination and close air support targeting functions. However, their combined market share remains significantly smaller than the dominant swarm detection and air-to-air tracking application segments.

Key Market Segments

By Radar Type

- AESA (Active Electronically Scanned Array)

- PESA (Passive Electronically Scanned Array)

- Hybrid AESA-PESA

- Phased Array with AI-Assisted Swarm Detection

- Others

By Platform

- Manned

- Unmanned

By Frequency Band

- X Band

- L Band

- S Band

- C Band

- Ku Band

By Application

- Swarm Detection and Counter-UAS

- Air-to-Air Target Tracking

- Terrain Following and Obstacle Avoidance

- Electronic Warfare Support

- Others

Drivers

Rising Demand for Real-Time Multi-Target Tracking and Swarm Neutralization Capabilities Drives Combat Aircraft Swarm Radar Market Growth

The increasing use of drone swarms and coordinated aerial attack formations in modern warfare is driving urgent demand for advanced swarm radar solutions. Defense agencies require combat aircraft equipped with systems capable of tracking multiple fast-moving targets simultaneously. Consequently, procurement programs for next-generation swarm detection radars are expanding rapidly across major defense markets globally.

The integration of AI-enabled radar signal processing is transforming the autonomous threat identification capabilities of combat aircraft radar systems. AI-driven platforms can classify and prioritize aerial threats without operator intervention, significantly improving overall response time. Therefore, defense programs are increasingly specifying AI-compatible radar architectures as a mandatory requirement in next-generation combat aircraft radar contracts.

The expansion of network-centric warfare strategies is generating sustained demand for cooperative radar systems capable of sharing real-time threat data across multiple combat platforms. Advanced swarm radars support inter-platform communication and collaborative target assessment during joint operations. Moreover, operational doctrines adopted by major defense alliances are accelerating investment in distributed radar network architectures for air combat scenarios.

Restraints

High System Complexity and Electronic Warfare Vulnerabilities Limit Adoption of Advanced Combat Aircraft Swarm Radars

The high technical complexity of integrating advanced swarm radar systems into legacy combat aircraft platforms represents a significant market restraint. Retrofitting existing airframes requires extensive compatibility assessments and often demands structural modifications. Consequently, integration timelines and costs frequently exceed initial program estimates, limiting the pace of radar modernization across established air force fleets.

Electronic warfare vulnerabilities pose a critical challenge for combat swarm radar reliability in highly contested operational environments. Sophisticated jamming and electronic countermeasure systems can degrade radar detection accuracy during high-threat engagements. Therefore, radar developers must continuously invest in anti-jamming technologies and low probability of intercept radar architectures to maintain operational effectiveness in modern combat scenarios.

The substantial development and procurement costs associated with next-generation swarm radar systems create significant budget barriers for smaller defense programs and partner nations. High per-unit procurement costs limit widespread deployment beyond primary defense forces. Additionally, extended development cycles delay operational fielding and reduce program flexibility in responding to rapidly evolving aerial threat environments.

Growth Factors

Advanced Radar Architectures and Integration with Emerging Weapons Platforms Accelerate Combat Aircraft Swarm Radar Market Expansion

The development of multi-static and distributed radar architectures is expanding swarm detection coverage for combat aircraft programs. These systems use multiple cooperating radar nodes to improve detection probability and system resilience against jamming. Consequently, defense research programs are investing substantially in distributed radar network technologies as a next-generation solution for aerial swarm threats.

The integration of combat aircraft swarm radar systems with directed energy weapons and advanced countermeasure platforms is creating significant new growth opportunities. Radar systems capable of cueing directed energy weapons for precision swarm neutralization represent a major capability advancement. Moreover, joint development programs are accelerating the convergence of radar, weapons, and countermeasure systems into unified combat aircraft platforms.

The growing adoption of unmanned combat aerial vehicles across global defense programs is generating substantial demand for embedded swarm detection radar systems. UCAV platforms require compact, high-performance radar solutions capable of autonomous operation in contested environments. Additionally, increasing UCAV procurement budgets across multiple nations are providing sustained revenue growth opportunities for swarm radar system developers and platform integrators.

Emerging Trends

Cognitive Radar Systems and Unified Sensor Architectures Are Reshaping the Combat Aircraft Swarm Radars Market

The increasing use of cognitive radar systems equipped with adaptive machine learning algorithms is a defining trend in the combat aircraft swarm radars market. These systems continuously analyze threat patterns and autonomously adjust radar parameters to optimize real-time detection performance. Consequently, cognitive radar development has become a priority investment area for leading defense electronics manufacturers and military research institutions.

The convergence of radar sensing and electronic warfare functions into unified sensor suites is transforming combat aircraft mission system architecture. Integrated platforms reduce size, weight, and power consumption while substantially expanding operational capabilities. Moreover, this convergence enables seamless coordination between radar detection and electronic countermeasure functions, improving overall combat aircraft survivability in contested airspace environments.

Growing focus on Low Probability of Intercept radar technologies is shaping procurement specifications for next-generation combat aircraft programs worldwide. LPI radar systems minimize detectable electromagnetic signatures that adversaries can exploit for counter-detection. Therefore, defense programs are increasingly prioritizing LPI-capable swarm radar solutions that maintain effective detection performance while supporting stealth operational requirements.

Regional Analysis

North America Dominates the Combat Aircraft Swarm Radars Market with a Market Share of 43.70%, Valued at USD 1.0 Billion

North America holds the leading position in the global Combat Aircraft Swarm Radars Market, accounting for 43.70% of the total market share and valued at approximately USD 1.0 Billion in 2025. The region benefits from the world’s largest defense procurement budgets and a highly developed defense industrial base. Moreover, active programs for next-generation combat aircraft and radar upgrades continue to drive sustained market growth.

Europe Combat Aircraft Swarm Radars Market Trends

Europe represents a significant and growing market for combat aircraft swarm radar systems, supported by rising defense spending commitments among NATO member nations. Countries including Germany, France, and the United Kingdom are actively investing in next-generation airborne radar development programs. Furthermore, collaborative European defense initiatives are accelerating the adoption of advanced swarm detection and electronic warfare technologies.

Asia Pacific Combat Aircraft Swarm Radars Market Trends

Asia Pacific is emerging as a high-growth region in the combat aircraft swarm radars market, driven by escalating regional security tensions and rapidly expanding national defense budgets. Nations including China, India, Japan, and South Korea are modernizing their air combat radar capabilities at pace. Additionally, domestic radar development programs are gaining momentum, reducing regional dependence on foreign-sourced radar technology.

Middle East and Africa Combat Aircraft Swarm Radars Market Trends

The Middle East and Africa region is experiencing growing demand for advanced combat radar systems, driven by ongoing regional security challenges and increasing defense procurement activity. Gulf Cooperation Council nations are actively investing in combat aircraft modernization and counter-drone programs. Moreover, rising counter-swarm defense priorities are accelerating procurement of next-generation radar technologies across the region.

Latin America Combat Aircraft Swarm Radars Market Trends

Latin America represents a developing market for combat aircraft swarm radars, with defense spending gradually increasing across several nations in the region. Brazil and Mexico are leading participants as they invest in air force modernization and radar capability upgrades. However, budget constraints and regional geopolitical priorities continue to limit the pace of advanced swarm radar technology adoption compared to other global markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lockheed Martin Corporation is a globally recognized defense technology leader with a strong portfolio of advanced radar systems for combat aircraft platforms. The company actively develops AESA radar technologies, electronic warfare systems, and integrated sensor solutions for next-generation fighter aircraft programs. Moreover, its sustained investment in AI-enabled radar signal processing reinforces its standing across the global combat aircraft swarm radars market.

Northrop Grumman is a key developer of advanced airborne radar systems and electronic warfare solutions for military aviation programs worldwide. The company’s radar technology portfolio includes active electronically scanned array systems designed for multi-role combat aircraft operations. Furthermore, Northrop Grumman is actively involved in programs focused on cognitive radar capabilities and integrated sensor architecture development for next-generation platforms.

Raytheon Technologies (RTX) is a leading provider of advanced radar and sensor technologies for defense and aerospace applications across the globe. The company develops high-performance AESA radar systems integrated across a wide range of combat aircraft platforms. Moreover, RTX holds deep expertise in radar signal processing, electronic warfare integration, and counter-UAS system development, positioning it as a central contributor to the swarm radar market.

BAE Systems is a major international defense contractor with a broad portfolio of airborne radar and electronic warfare systems serving military customers globally. The company supplies advanced radar technologies to defense clients across Europe, North America, and Asia Pacific. Furthermore, BAE Systems is developing next-generation radar sensor fusion solutions that integrate swarm detection and electronic warfare capabilities into unified combat aircraft mission systems.

Key Players

- Lockheed Martin Corporation

- Northrop Grumman

- Raytheon Technologies (RTX)

- BAE Systems

- Thales Group

- Others

Recent Developments

- February 2026 – Lockheed Martin delivered the first Sentinel A4 radar system from Low-Rate Initial Production (LRIP) 2 to the U.S. Army, marking a significant milestone in the modernization of U.S. ground-based air defense radar capabilities. This delivery advances the Army’s program to field next-generation radar protection against aerial threats.

- November 2025 – Chaos Industries raised USD 510 million in Series D funding to accelerate the development of next-generation defense technology solutions and advanced counter-drone systems. This substantial investment reflects strong private capital confidence in the growing demand for innovative defense electronics and swarm neutralization technologies.

Report Scope

Report Features Description Market Value (2025) USD 2.5 Billion Forecast Revenue (2035) USD 4.8 Billion CAGR (2026-2035) 6.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Radar Type (AESA (Active Electronically Scanned Array), PESA (Passive Electronically Scanned Array), Hybrid AESA-PESA, Phased Array with AI-Assisted Swarm Detection, Others), By Platform (Manned, Unmanned), By Frequency Band (X Band, L Band, S Band, C Band, Ku Band), By Application (Swarm Detection and Counter-UAS, Air-to-Air Target Tracking, Terrain Following and Obstacle Avoidance, Electronic Warfare Support, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Lockheed Martin Corporation, Northrop Grumman, Raytheon Technologies (RTX), BAE Systems, Thales Group, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Combat Aircraft Swarm Radars MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Combat Aircraft Swarm Radars MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Lockheed Martin Corporation

- Northrop Grumman

- Raytheon Technologies (RTX)

- BAE Systems

- Thales Group

- Others

Our Clients

- 183407

- March 2026