Quick Navigation

Report Overview

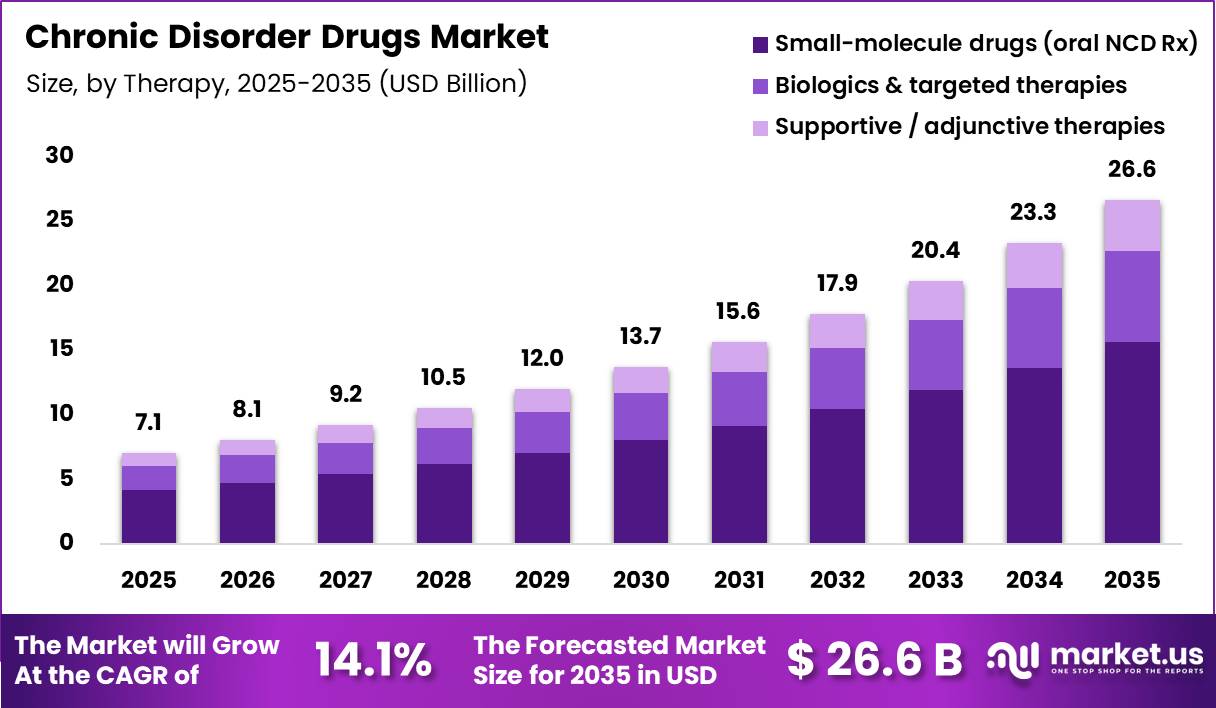

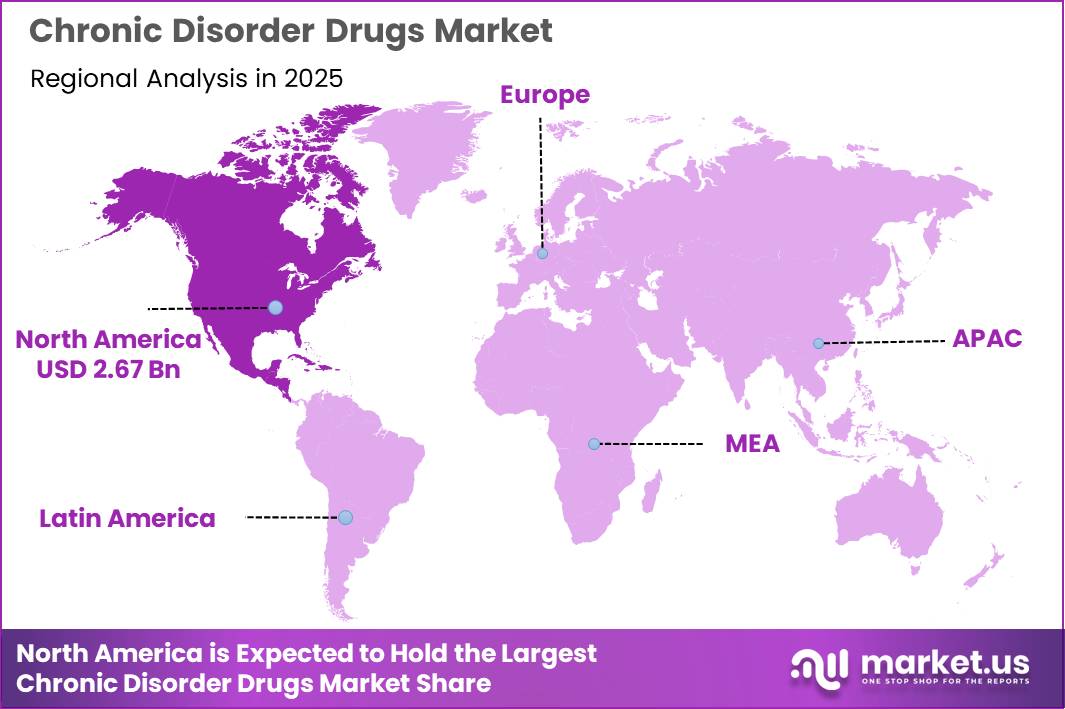

In 2025, the Global Chronic Disorder Drugs Market was valued at US$ 7.1 Billion, and between 2026 and 2035, this market is estimated to register a CAGR of 14.1%, reaching about US$ 26.6 Billion by 2035. North America held a dominant market position, capturing more than a 37.7% share, holding USD 2.67 Billion in revenue.

The chronic disorder drugs market is increasingly defined by a structural convergence between high-volume traditional pharmacotherapy and precision-driven innovation platforms. While oral small-molecule therapies continue to anchor market volume due to their scalability, established supply chains, and payer-driven cost containment strategies, the underlying growth momentum is gradually shifting toward differentiated, high-efficacy modalities such as biologics and targeted therapies.

This dual-track evolution is not substitutional, but additive, legacy small-molecule portfolios are being optimized for lifecycle extension, while next-generation biologics are being deployed to address refractory or complex chronic conditions where conventional therapies demonstrate diminishing marginal returns.

As a result, portfolio strategies across major pharmaceutical players are becoming increasingly hybridized, balancing mass-market affordability with high-margin innovation. Innovation across the Chronic Disorder Drugs Market remains supported by the continued approval of both small-molecule medicines and biologic therapies.

- In 2025, the U.S. Food and Drug Administration approved 46 novel drugs, comprising 34 new molecular entities and 12 biologics. This reflects ongoing development of treatment options for chronic conditions that require long-term disease management, including therapies designed to improve treatment response, convenience, and patient outcomes.

From a competitive standpoint, the market is witnessing intensified vertical integration and capacity consolidation, particularly in metabolic and cardiovascular therapeutic domains that represent long-duration revenue streams. Leading companies are increasing control over critical manufacturing stages, including active pharmaceutical ingredient production, sterile fill-finish operations, device assembly, and supply chain planning. This is evident in large-scale infrastructure investments and asset consolidation strategies designed to secure an uninterrupted supply of high-demand chronic therapies. For instance,

- In December 2024, Novo Nordisk A/S expanded its manufacturing footprint through the acquisition of three former Catalent fill-finish facilities, strengthening its GLP-1 supply chain and reflecting a broader industry shift toward capacity assurance as a competitive differentiator.

The transaction was designed to increase manufacturing flexibility and support future production of obesity and diabetes treatments. In parallel, companies such as Eli Lilly and Company are scaling production ecosystems to support rapidly expanding metabolic drug demand, signaling that supply-side capability is becoming as strategically critical as pipeline innovation in determining long-term market leadership.

Key Takeaways

- Market Size: Global Chronic Disorder Drugs Market size is expected to be worth around US$ 26.6 Billion by 2035 from US$ 7.1 Billion in 2025.

- Market Share: The market is growing at a CAGR of 14.1% during the forecast period from 2026 to 2035.

- Therapy Type Analysis: Small-molecule drugs (oral NCD Rx) dominate therapy type with 58.7% market share.

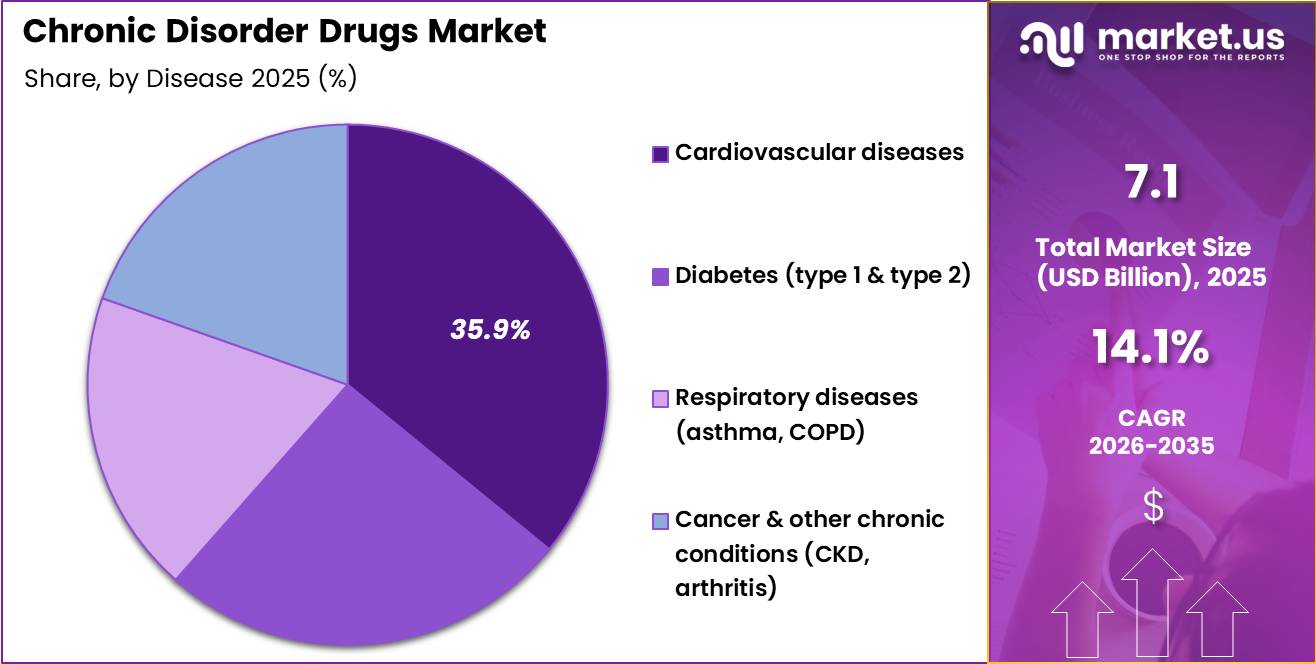

- Disease Analysis: Based on the Disease, Cardiovascular diseases command the largest disease-specific revenue pool at 35.9% share.

- Route of Administration Analysis: Based on the Route of Administration, Oral drugs led the market, comprising 61.3% of the total market.

- Regional Analysis: In 2025, North America was the most dominant region in the chronic disorder drugs market, accounting for 37.7% of the total global consumption.

Therapy Type Analysis

Small-Molecule Drugs Remain the Dominant Revenue Backbone of the Global Chronic Disorder Drugs Market.

On the basis of therapy type, small-molecule drugs (oral NCD Rx) dominate the global chronic disorder drugs market with a 58.7% share, driven by their entrenched position as first-line therapy across high-prevalence chronic conditions including cardiovascular diseases, diabetes, respiratory disorders, and arthritis. Their dominance is structurally sustained by high scalability, low production complexity, strong physician familiarity, and deep generic penetration, enabling cost-efficient long-term treatment at population scale.

As chronic disease prevalence expands globally, healthcare systems continue to prioritize oral therapies that ensure adherence, affordability, and wide accessibility, reinforcing small molecules as the default backbone of primary care prescribing. The segment’s leadership is further reinforced by reimbursement systems and payer frameworks that consistently favor cost-effective oral drugs over higher-cost biologics when comparable clinical outcomes exist.

AstraZeneca entered a collaboration with CSPC Pharmaceutical Group valued at up to USD 5.2 billion to discover and develop AI-enabled oral drug candidates for chronic diseases, highlighting continued investment in next-generation small-molecule therapies for long-term disease management.

In the same period, Merck & Co., Inc. (MSD) reinforced its diabetes and cardiometabolic franchise through widely prescribed oral therapies supporting long-term disease management. While biologics & targeted therapies are steadily gaining traction in precision medicine and complex chronic conditions, supportive/adjunctive therapies continue to expand their role in multimorbidity management and symptom-control-driven chronic care pathways.

Disease Analysis

Cardiovascular Diseases Represent the Key Revenue-Generating Disease Segment in the Global Chronic Disorder Drugs Market

Based on disease, cardiovascular diseases dominate the global chronic disorder drugs market with a 35.9% share, primarily due to their exceptionally high global prevalence and lifelong treatment requirements across conditions such as hypertension, coronary artery disease, and dyslipidemia.

The segment’s dominance is structurally driven by the need for continuous pharmacological intervention, where patients remain on therapy for decades, creating sustained prescription volumes. In addition, standardized clinical guidelines across major healthcare systems ensure early diagnosis and immediate initiation of long-term drug regimens, reinforcing consistent demand generation at the primary care level.

The segment’s leadership is further strengthened by entrenched reimbursement support and strong therapeutic standardization, which prioritize long-term risk reduction and prevention of severe cardiovascular events such as stroke and myocardial infarction.

AstraZeneca plc continues to strengthen its cardiovascular portfolio through established therapies such as its SGLT2 inhibitor-based cardiometabolic treatments, while Bristol-Myers Squibb Company (BMS) maintains a strong position in long-term cardiovascular care through its widely used anticoagulant portfolio led by Eliquis. Other disease segments, including diabetes, respiratory diseases, and cancer & other chronic conditions, are steadily expanding, supported by rising global disease burden and improved long-term treatment adherence across healthcare systems.

Route of Administration Analysis

Oral Drugs Dominate Across All Chronic Disease Categories.

Oral drugs dominate the route of administration landscape with a commanding 61.3% share, reflecting their entrenched role as the backbone of chronic disorder management. Their leadership is primarily driven by strong patient adherence in long-duration therapies, ease of self-administration without clinical intervention, and cost advantages that make them highly scalable across large patient populations.

In high-prevalence conditions such as cardiovascular diseases and diabetes, oral therapies remain the default treatment pathway for both initiation and maintenance, reinforcing consistent prescription renewals and strong payer preference across global healthcare systems.

This dominance is further reinforced by mature formulation platforms and continuous incremental innovation focused on improving bioavailability, fixed-dose combinations, and dosing convenience.

- In May 2026, Novo Nordisk made Ozempic® (semaglutide) tablets available in the United States for adults with type 2 diabetes. The introduction of the oral peptide GLP-1 therapy highlights the growing role of oral drug delivery beyond conventional small-molecule medicines, offering a pill-based treatment option for long-term diabetes management and cardiovascular risk reduction.

Meanwhile, injectable therapies and inhaled routes are gradually expanding across the 2026–2035 forecast period, driven by rising biologics penetration and chronic respiratory treatment needs, but remain secondary due to higher administration complexities, stricter clinical monitoring requirements, and elevated manufacturing costs.

Key Market Segments

By Therapy

- Small-Molecule Drugs (Oral NCD Rx)

- Biologics & Targeted Therapies

- Supportive / Adjunctive Therapies

By Disease

- Cardiovascular Diseases

- Diabetes (Type 1 & Type 2)

- Respiratory Diseases (Asthma, COPD)

- Cancer & Other Chronic Conditions (CKD, Arthritis)

By Route of Administration

- Oral Drugs

- Parenteral / Injectable

- Inhaled & Other Routes

Driver

Metabolic disease escalation expanding treated pools

The strongest structural growth driver remains the rising underlying burden of chronic disease, especially diabetes, cardiovascular conditions, obesity linked disorders, and kidney disease, because it enlarges the diagnosable and continuously treated patient base rather than only raising price per patient.

WHO states that noncommunicable diseases caused at least 43 million deaths in 2021, equivalent to 75% of non pandemic related deaths, with cardiovascular disease alone accounting for about 19 million deaths and diabetes plus diabetes related kidney disease causing more than 2 million deaths. WHO also reports that the number of people living with diabetes rose from 200 million in 1990 to 830 million in 2022, while chronic kidney disease affects an estimated 674 million people worldwide, with most patients in low and middle income countries.

In commercial terms, this pushes chronic disorder drug demand through three channels at once: more incident patients entering therapy, more comorbidity driven combination prescribing, and longer treatment duration as health systems intervene earlier to avoid downstream hospitalization, dialysis, stroke, and cardiac events. The result is a broad based lift to volume led revenue growth across antidiabetics, lipid lowering agents, antihypertensives, renal protective drugs, and obesity linked therapies, making this the most durable CAGR contributor through 2030.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metabolic disease escalation expanding treated pools | +2.4% | North America core, EU, China, India, GCC, LatAm urban centers | Medium term (2-4 years) |

| GLP-1 and incretin class broadening beyond diabetes | +2.1% | U.S. core, EU5, Japan, South Korea, China upper-tier cities | Short term (≤ 2 years) |

| Earlier diagnosis and primary-care screening for CKD/CVD/diabetes | +1.5% | U.S., EU, UK, Japan, urban APAC, selective LMIC programs | Medium term (2-4 years) |

| Regulatory expansion into adjacent chronic indications | +1.3% | U.S. first wave, EU follow-on, developed APAC | Short term (≤ 2 years) |

| Medicare negotiation and payer pressure accelerating value-tiered uptake | +0.9% | U.S. core, EU reference-pricing markets, Canada spill-over | Medium term (2-4 years) |

| Biosimilars and loss-of-exclusivity widening access in maintenance therapy | +1.1% | EU core, U.S., Brazil, MENA tender markets, Southeast Asia | Medium term (2-4 years) |

Challenge

Specialty biologics and chronic injectables fill finish bottlenecks

The chronic disorder drugs market continues to grow because underlying patient volumes are rising, but its scalable growth ceiling is constrained by concentrated upstream sourcing of active pharmaceutical ingredients and intermediates, especially for high volume generics and therapy support medicines, where even a low double digit disruption in one sourcing corridor can cascade into 8 to 16 week replenishment gaps, 15 to 30 day logistics reroutes, and working capital inflation across wholesalers and hospital buyers; this is strategically important because medicine shortages remain structurally persistent rather than episodic, with the FDA still maintaining a formal shortages architecture and ASHP reporting 253 active shortages by mid 2025, more than one third of which had been running since 2022 or earlier, while EU institutions are still treating critical medicines resilience as a policy priority through the Critical Medicines Alliance and EMA vulnerability workstreams.

In practical market terms, that translates into an estimated 1.2% point CAGR drag because companies cannot fully convert diagnosed chronic care demand into stable dispensed volume when procurement teams are forced to dual source, hold 60 to 120 days of safety stock on selected molecules, qualify backup vendors over 9 to 18 months, and absorb 3% to 7% procurement premiums to reduce dependency on a limited supplier base across China India EU US trade flows.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Multi-source API fragility | -1.2% | EU import corridors, US generics base, India-China supply chains, LATAM buyers | Medium term (2-4 years) |

| Specialty biologics fill-finish bottlenecks | -1.0% | North America core, EU regulatory hubs, Japan, affluent Gulf markets | Medium term (2-4 years) |

| Adherence and polypharmacy decay | -1.4% | North America core, EU aging markets, East Asia aging systems, urban LMICs | Long term (≥ 4 years) |

| Provider capacity mismatch | -0.8% | Sub-Saharan Africa, MENA, South Asia, rural OECD markets | Long term (≥ 4 years) |

| Quality remediation cycle risk | -0.9% | US FDA-linked exporters, EU supply network, sterile plants in India and China | Medium term (2-4 years) |

| Reimbursement migration pressure | -1.1% | US commercial and Part D channels, EU tender systems, middle-income public payers | Medium term (2-4 years) |

Restraints

Recurrent Drug Shortages Disrupting Chronic Care Supply

Supply continuity remains a material drag because FDA identifies manufacturing and quality problems, delays, discontinuations, recalls, supply interruptions, and demand surges as recurring shortage triggers, while ASHP reports 253 active drug shortages, down from the Q1 2024 peak of 323 but still elevated enough to keep procurement teams in contingency mode across hospital and retail channels.

In chronic disorder drugs, even if many shortages are molecule specific rather than category wide, a shortage environment raises safety stock requirements by an estimated 15% to 25%, lengthens replenishment planning cycles by roughly 2 to 6 weeks for exposed SKUs, increases expedited logistics and alternate sourcing costs, and forces pharmacies and payers to substitute across therapeutic classes, creating script leakage, lower compliance, and uneven revenue recognition that collectively justify a 1.2 percentage point reduction to 2026 CAGR, especially in the US, parts of Europe, and import dependent APAC markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability squeeze | -1.4% | LMICs, US high-OOP cohorts, LatAm | Short term (≤ 2 years) |

| Drug shortages | -1.2% | North America core, EU, selected APAC | Short term (≤ 2 years) |

| Price-control pressure | -1.0% | US Medicare, EU major markets | Medium term (2-4 years) |

| Generic/biosimilar drag | -0.9% | US, EU, Japan, South Korea | Medium term (2-4 years) |

| Regulatory complexity | -0.7% | EU, US, emerging markets | Medium term (2-4 years) |

| Adherence leakage | -1.1% | LMICs, US, frontier APAC, Africa | Long term (≥ 4 years) |

Opportunity

Monetizing Multi Condition Chronic Care via Bundled Models

This is an opportunity rather than a baseline driver because the chronic disorder drugs market already grows from disease prevalence and aging, but most manufacturers still monetize only the prescription itself instead of the full longitudinal care pathway; by packaging a branded chronic therapy with reimbursable remote monitoring, algorithmic titration support, refill automation, and outcomes dashboards, companies can expand revenue per treated patient by roughly 12% to 22%, improve gross retention by 400 to 700 basis points, and reduce discontinuation by an estimated 8% to 15% in high friction categories such as diabetes, cardiovascular, respiratory, and autoimmune maintenance therapy.

The model is newly actionable because CMS permits concurrent billing across chronic care management and remote patient monitoring pathways, including thresholds such as 16 device reading days per 30 day period and 20 minutes of clinical engagement for certain RPM codes, creating a financial stack that can support manufacturer provider partnerships instead of pure pill sales; for large branded portfolios, even 10% to 15% patient attachment into bundled service models could add 1.9 percentage points to market CAGR by pulling ancillary digital revenue, better persistence, and premium positioning into categories that otherwise would revert to price competition.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Multi-condition drug-device bundles | +1.9% | North America, EU, Japan, Gulf | Short term (≤ 2 years) |

| LMIC access-tier monetization | +2.4% | India, Southeast Asia, Africa, LatAm | Medium term (2-4 years) |

| Biosimilar roll-up and switch platforms | +1.6% | EU, Canada, select APAC, LatAm | Short term (≤ 2 years) |

| Specialty-to-primary care down-channeling | +1.8% | U.S., EU5, China, Brazil | Medium term (2-4 years) |

| RWE-led label and line extensions | +1.4% | U.S., EU, UK, Nordics | Medium term (2-4 years) |

| Adherence-as-a-service monetization | +1.2% | U.S., Germany, Japan, urban APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

IRA Drug Pricing Regulation, EU Pharmaceutical Legislation Reform, and China Market Access Dynamics Reshaping Competitive Strategy.

Global policy interventions are increasingly influencing pricing structures and commercial strategies in the chronic disorder drugs market, particularly through regulatory reforms aimed at controlling long-term pharmaceutical expenditure. In the United States, the Inflation Reduction Act (IRA) is introducing Medicare price negotiations for selected high-cost chronic therapies, placing sustained downward pressure on revenue expectations for mature biologics and specialty medicines.

This is prompting pharmaceutical companies to prioritize innovation-heavy portfolios and accelerate lifecycle value extraction earlier in the product cycle. In Europe, ongoing pharmaceutical legislation reforms are strengthening cost-containment mechanisms while increasing reimbursement evidence requirements, making market access for chronic therapies more complex and time-intensive across multiple member states.

In China, centralized procurement programs and expanding domestic pharmaceutical capabilities are intensifying price competition while expanding access to high-volume chronic disease treatments, particularly in cardiovascular and diabetes segments. These developments are accelerating the shift toward localized manufacturing, regional pricing strategies, and supply chain diversification as companies seek to maintain competitiveness across fragmented regulatory environments.

Collectively, these geopolitical pressures are reshaping global commercialization models, compelling manufacturers to balance affordability mandates with innovation-driven growth across key chronic care markets.

Regional Analysis

North America Dominance Driven by High Chronic Disease Burden and Advanced Treatment Adoption.

North America held a dominant position in the chronic disorder drugs market, capturing more than a 37.7% share and generating approximately USD 2.67 billion in revenue. This leadership is supported by a high prevalence of cardiovascular diseases, diabetes, and obesity-linked metabolic disorders, which collectively drive sustained long-term prescription demand across both primary and specialty care segments.

The region’s advanced healthcare infrastructure and rapid adoption of innovative therapies enable early diagnosis, consistent treatment initiation, and high adherence rates in chronic disease management, reinforcing steady volume and value growth.

The region’s dominance is further strengthened by the presence of leading pharmaceutical innovators such as Pfizer Inc., Merck & Co., Inc. (MSD), and Johnson & Johnson (J&J/Janssen), which continue to drive pipeline innovation and commercialization of advanced chronic therapies. Strong regulatory frameworks, high R&D investment intensity, and well-established reimbursement systems collectively sustain North America’s leadership position.

Meanwhile, Europe remains a structurally significant market supported by universal healthcare systems and biologics adoption, while Asia Pacific is emerging as the fastest-growing region driven by rising chronic disease prevalence and expanding healthcare access. Latin America and the Middle East & Africa represent developing markets with gradually improving treatment penetration.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The chronic disorder drugs market is moderately concentrated among a small group of diversified global pharmaceutical leaders with strong multi-indication portfolios spanning cardiovascular, metabolic, respiratory, oncology, and immunology therapies. Competitive advantage is increasingly determined by pipeline depth, speed of label expansion, and the ability to commercialize therapies across multiple chronic disease categories under unified cardiometabolic and immunology platforms.

Innovation intensity is highest in GLP-1-based metabolic therapies, precision oncology, and next-generation biologics, where companies are competing to extend indications and maximize lifecycle value across long-duration treatment pathways.

The first tier of market leadership includes Pfizer Inc., Johnson & Johnson (J&J/Janssen), Merck & Co., Inc. (MSD), Novartis AG, Roche Holding AG, AstraZeneca plc, and Sanofi S.A., each maintaining diversified chronic disease portfolios that reduce dependency on single therapeutic classes and provide resilience against patent expiry cycles.

The second tier is defined by highly specialized or franchise-dominant players, including Novo Nordisk A/S and Eli Lilly and Company, which are shaping the cardiometabolic segment through GLP-1 innovation leadership, as well as AbbVie Inc., which is successfully transitioning its immunology franchise beyond Humira® erosion through next-generation assets like Skyrizi® and Rinvoq®.

Other strategically important players include Bristol-Myers Squibb Company, Amgen Inc., Bayer AG (Pharma Division), Takeda Pharmaceutical Company Limited, and GlaxoSmithKline plc (GSK), which are strengthening positions across cardiovascular, oncology, immunology, and specialty chronic care segments through targeted pipeline expansion and biologics investment.

Market Key Players

- Pfizer Inc.

- Johnson & Johnson (J&J/Janssen)

- Merck & Co., Inc. (MSD)

- Novartis AG

- Roche Holding AG (Roche)

- Sanofi S.A.

- AstraZeneca plc

- GlaxoSmithKline plc (GSK)

- AbbVie Inc.

- Bristol-Myers Squibb Company (BMS)

- Eli Lilly and Company

- Novo Nordisk A/S

- Amgen Inc.

- Bayer AG (pharma division)

- Takeda Pharmaceutical Company Limited

- Others

Recent Development

- In January 2026, Bayer AG announced expanded investment in its cardiovascular and renal disease portfolio, advancing precision medicine approaches for chronic cardiorenal disorders through ongoing late-stage development programs.

- In June 2026, Novo Nordisk moved toward broader global expansion of oral obesity treatment by seeking regulatory approval for its oral Wegovy in China, reinforcing competition in chronic metabolic disease therapeutics.

- In April 2026, Eli Lilly advanced its obesity franchise with FDA approval and commercialization expansion of orforglipron, one of the first oral GLP-1 therapies for chronic weight management.

- In March 2025, Roche Holding AG received FDA approval for Susvimo® for diabetic retinopathy, expanding its portfolio of long-duration therapies for chronic vision-threatening diseases and strengthening its position in specialty chronic care.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 7.1 Bn |

| Forecast Revenue (2035) | US$ 26.6 Bn |

| CAGR (2026-2035) | 14.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Therapy (Small-Molecule Drugs, Biologics & Targeted Therapies, Supportive/Adjunctive Therapies); By Disease (Cardiovascular Diseases, Diabetes Type 1 & 2, Respiratory Diseases, Cancer & Other Chronic Conditions); By Route of Administration (Oral, Parenteral/Injectable, Inhaled & Other Routes) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., Johnson & Johnson (J&J/Janssen), Merck & Co. Inc. (MSD), Novartis AG, Roche Holding AG, Sanofi S.A., AstraZeneca plc, GlaxoSmithKline plc (GSK), AbbVie Inc., Bristol-Myers Squibb Company (BMS), Eli Lilly and Company, Novo Nordisk A/S, Amgen Inc., Bayer AG, Takeda Pharmaceutical Company Limited, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |