Global Cheese Ingredient Market Size, Share, And Enhanced Productivity By Cheese Type (Natural Cheese, Process Cheese, Cheese Powder, Cheese Sauce, Cheese Spread), By Source (Cow Milk, Goat Milk, Sheep Milk, Buffalo Milk), By Application (Pizza, Pasta, Sandwiches, Burgers, Salads, Sauces, Dips, Bakery Products, Snacks), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Food Service), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: March 2026

- Report ID: 181432

- Number of Pages: 378

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

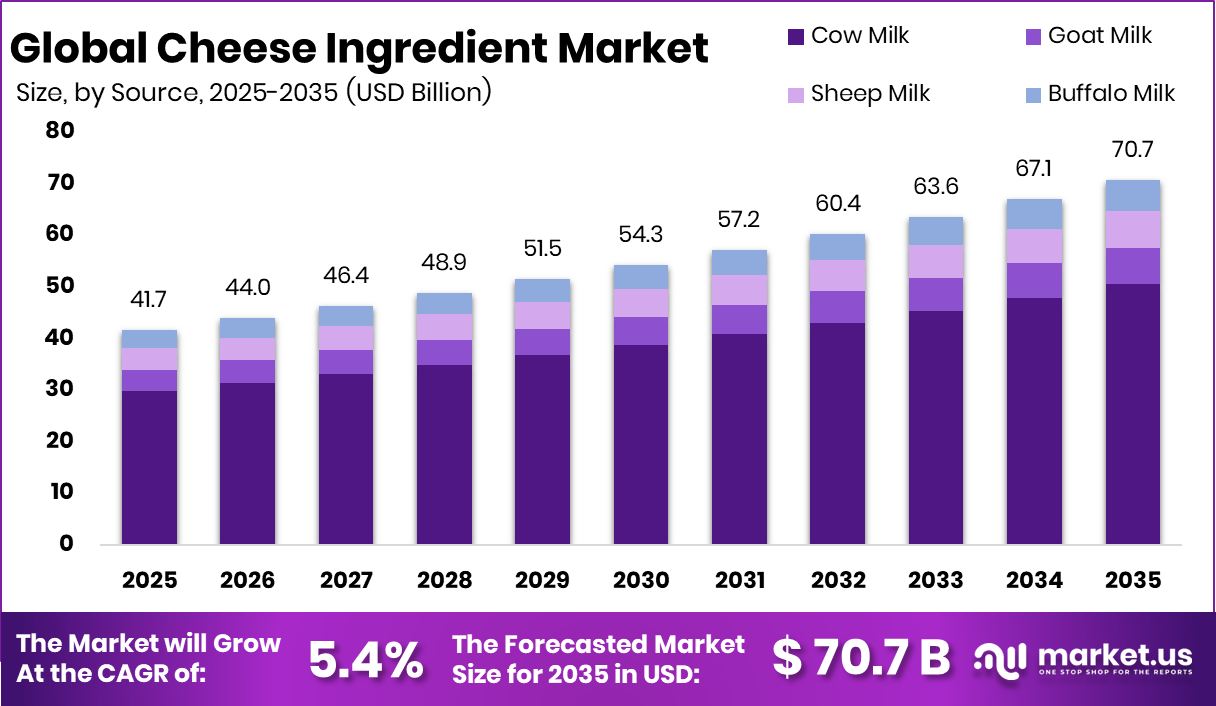

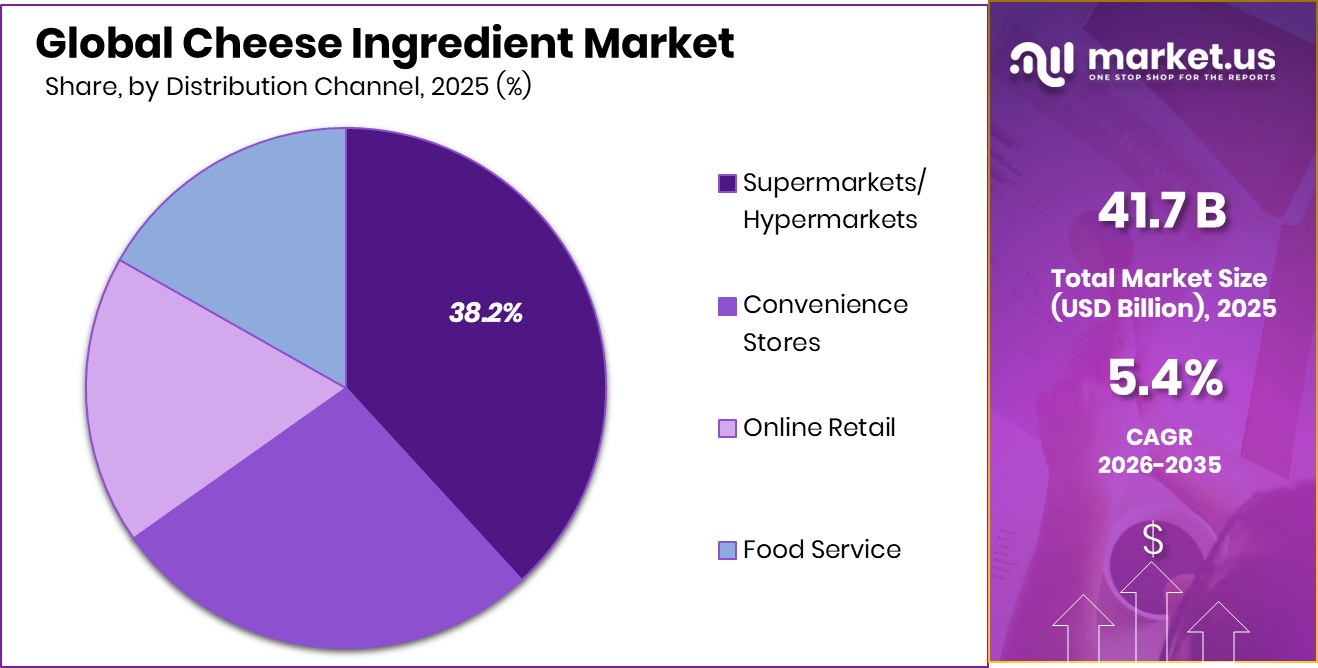

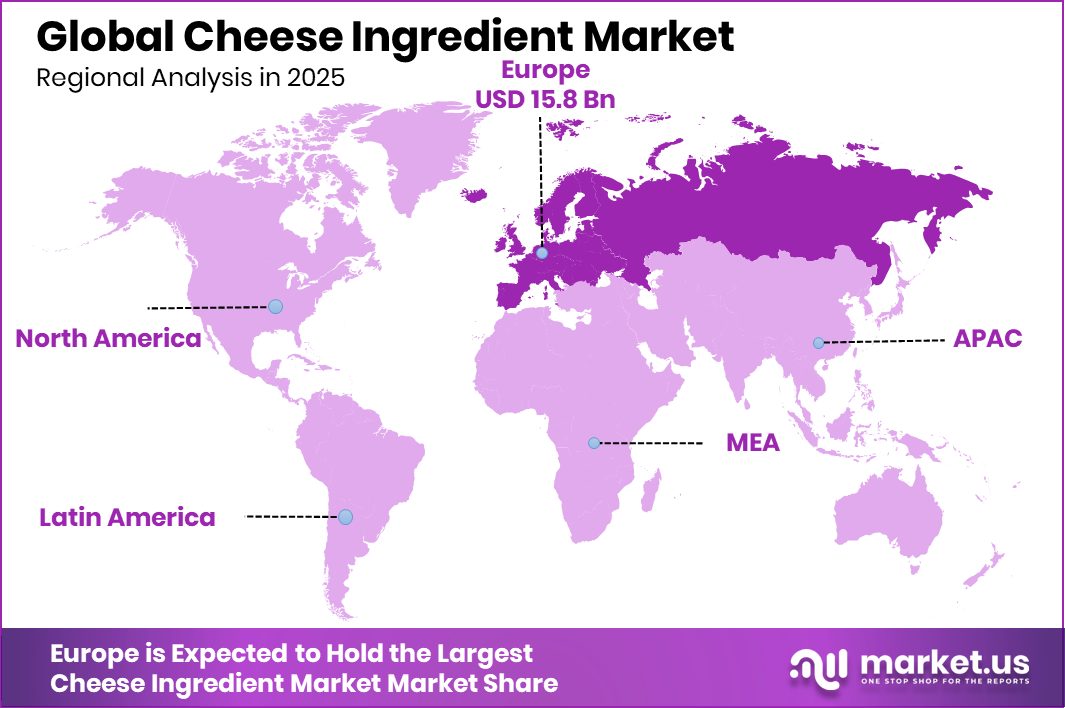

The Global Cheese Ingredient Market is expected to be worth around USD 70.7 billion by 2034, up from USD 41.7 billion in 2024, and is projected to grow at a CAGR of 5.4% from 2025 to 2034. The Cheese Ingredient Market in Europe achieved 37.9% share, valued at USD 15.8 Bn.

Cheese ingredient refers to cheese in processed or functional forms that are used as components in food preparation and manufacturing. These ingredients include natural cheese, processed cheese, cheese powder, cheese sauces, and spreads that help enhance flavour, texture, and melting properties in food products. Cheese ingredients are commonly produced from milk sources such as cow, goat, sheep, and buffalo milk. They are widely used across a variety of foods, including pizza, pasta, burgers, sandwiches, bakery products, snacks, dips, and sauces, where they contribute to taste, richness, and overall product quality.

The cheese ingredient market represents the global trade and consumption of cheese used as an ingredient in food processing, foodservice, and retail cooking applications. The market includes a broad taxonomy covering cheese types such as natural cheese, processed cheese, cheese powder, cheese sauce, and cheese spread. Distribution channels range from supermarkets and hypermarkets to convenience stores, online retail, and foodservice providers. Growth of ready-to-eat meals, fast food culture, and convenience foods has significantly increased the use of cheese ingredients in both commercial kitchens and packaged food manufacturing.

One of the key growth factors in this market is the increasing global demand for convenience foods and quick-service meals. Cheese ingredients are widely used in pizza, pasta, burgers, sandwiches, and snack products because they provide consistent flavour and melting performance. Food manufacturers and restaurants rely on these ingredients to improve taste and product appeal. Urban lifestyles and busy consumer schedules have increased demand for ready-to-cook and ready-to-eat foods that commonly incorporate cheese components.

Demand is also influenced by ongoing product innovation and investment across the broader cheese sector. Companies and investors are actively supporting new product development, particularly in alternative and speciality cheese segments. For example, Finland’s Mö Foods secured €2.4 million to scale oat-based cheese alternatives, while Climax Foods rebranded to Bettani Farms and secured $6.5 million in funding alongside new leadership. Private equity firm L Catterton acquired Good Culture in a $500 million deal, and the company previously raised $64 million to support product innovation. Additionally, Plonts launched plant-based cheese in major U.S. cities with $12 million in seed funding, while Nobell Foods raised $75 million to expand its plant-based cheese production.

Opportunities in the cheese ingredient market are expanding with the development of new dairy and plant-based ingredient solutions. Investments and funding initiatives are supporting product diversification, improved production technologies, and wider distribution capabilities. As food manufacturers continue to develop new snacks, prepared meals, and dairy alternatives, the demand for innovative cheese ingredients is expected to expand across both traditional dairy and emerging plant-based segments.

- In March 2024, Arla Foods announced an investment of about EUR 210 million to upgrade technology and expand mozzarella cheese production at its Taw Valley dairy site in the UK. Arla Foods works as a global dairy cooperative producing milk, butter, and different types of cheese used in foodservice and food manufacturing. The new investment helps increase the production of mozzarella cheese that is widely used in pizza and ready-to-eat foods. Most of the additional cheese production will be supplied to international foodservice customers and manufacturers that use cheese as an ingredient in processed foods.

Key Takeaways

- The Global Cheese Ingredient Market is expected to be worth around USD 70.7 billion by 2034, up from USD 41.7 billion in 2024, and is projected to grow at a CAGR of 5.4% from 2025 to 2034.

- Natural cheese dominates the Cheese Ingredient Market, accounting for 39.5% share due to consumer preference.

- Cow milk leads the Cheese Ingredient Market source segment with 71.4% share because of its wide availability.

- Pizza application holds 23.1% share in the Cheese Ingredient Market, driven by global fast-food demand.

- Supermarkets and hypermarkets dominate the Cheese Ingredient Market distribution channel with a 38.2% market share.

- In Europe, the Cheese Ingredient Market recorded 37.9% share, totalling USD 15.8 Bn.

By Cheese Type Analysis

Natural cheese dominates the cheese ingredient market with a significant 39.5% share.

In 2025, natural cheese accounted for 39.5% of the cheese ingredient market, reflecting strong consumer preference for minimally processed and authentic dairy products. Natural cheese ingredients are widely used in food manufacturing due to their rich flavour, functional properties, and clean-label appeal. Food processors prefer natural cheese forms such as shredded, sliced, and powdered varieties for applications in ready meals, snacks, and bakery products. The growing demand for premium and artisanal-style food products has also contributed to the increased use of natural cheese ingredients.

Additionally, consumers are becoming more aware of ingredient transparency, encouraging manufacturers to adopt natural cheese components rather than processed alternatives. The segment continues to grow as foodservice chains and packaged food brands prioritise quality ingredients that enhance taste, texture, and overall product value.

By Source Analysis

Cow milk leads the cheese ingredient market sources, accounting for a strong 71.4%.

In 2025, cow milk dominated the cheese ingredient market with a 71.4% share, mainly due to its large-scale availability and well-established dairy supply chains worldwide. Cow milk is widely preferred for cheese production because it provides consistent texture, flavour, and nutritional composition. The high protein and fat content in cow milk allows manufacturers to produce a wide variety of cheese ingredients suitable for multiple food applications.

Additionally, the global dairy industry infrastructure strongly supports cow milk processing, making it more cost-effective than other milk sources, such as goat or sheep. Food manufacturers rely heavily on cow milk-based cheese ingredients for products like frozen meals, sauces, snacks, and bakery items. The strong presence of dairy farming regions in North America and Europe further strengthens the dominance of cow milk in this market segment.

By Application Analysis

Pizza applications drive the cheese ingredient market demand, contributing a notable 23.1% share.

In 2025, pizza applications held 23.1% of the cheese ingredient market, driven by the continued global popularity of pizza across both foodservice and retail sectors. Cheese is a fundamental component of pizza, contributing to its flavour, stretchability, and melting characteristics. Mozzarella and mozzarella-based blends are the most widely used cheese ingredients in pizza production. The expansion of quick-service restaurants, pizza delivery chains, and frozen pizza products has significantly increased demand for high-performance cheese ingredients.

Manufacturers focus on developing cheese formulations that offer consistent melt, browning, and texture during baking. Additionally, the rising trend of ready-to-cook and ready-to-eat meals has boosted pizza consumption globally. As pizza remains a staple comfort food in many regions, the demand for specialised cheese ingredients designed specifically for pizza applications continues to grow.

By Distribution Channel Analysis

Supermarkets and hypermarkets dominate the cheese ingredient market distribution channels with a 38.2% share.

In 2025, supermarkets and hypermarkets accounted for 38.2% of the cheese ingredient market distribution, highlighting the importance of organised retail in reaching consumers and food buyers. These retail channels offer a wide selection of cheese ingredient products, including shredded cheese, cheese slices, blocks, and cooking blends used in home meal preparation. Consumers prefer supermarkets and hypermarkets because they provide convenience, product variety, and the ability to compare brands and prices.

In addition, large retail chains frequently promote dairy and cheese products through in-store promotions and discount campaigns, which help increase sales volume. The expansion of modern retail infrastructure in developing countries has further strengthened this distribution channel. As consumer purchasing habits increasingly favour one-stop shopping experiences, supermarkets and hypermarkets continue to play a major role in cheese ingredient market growth.

Key Market Segments

By Cheese Type

- Natural Cheese

- Process Cheese

- Cheese Powder

- Cheese Sauce

- Cheese Spread

By Source

- Cow Milk

- Goat Milk

- Sheep Milk

- Buffalo Milk

By Application

- Pizza

- Pasta

- Sandwiches

- Burgers

- Salads

- Sauces

- Dips

- Bakery Products

- Snacks

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Food Service

Driving Factors

Rising global demand for convenience foods

The increasing demand for convenience foods is a major factor supporting the growth of the Cheese Ingredient Market. Busy lifestyles and rapid urbanisation have encouraged consumers to choose ready-to-eat meals, packaged snacks, and quick preparation foods that frequently contain cheese ingredients. Products such as frozen pizza, pasta meals, sandwiches, and bakery snacks rely on cheese powders, sauces, and processed cheese to deliver flavour and texture.

As food manufacturers expand convenience food lines, the use of functional cheese ingredients continues to grow. Industry investment activity across food innovation ecosystems also reflects this demand. For instance, biomass fermentation startup MOA Foodtech secured a $15.4 million investment commitment from the European Innovation Council (EIC), supporting ingredient innovation that can influence future food formulation and ingredient technologies.

Increasing use of cheese in fast food

The expanding global fast-food sector has significantly increased the use of cheese ingredients across multiple menu categories. Cheese plays an essential role in burgers, sandwiches, pizzas, baked snacks, and sauces, making it a core ingredient for many quick-service restaurant offerings. Restaurants rely on cheese ingredients that deliver consistent melting, taste, and texture to maintain product quality at scale.

As fast-food brands expand globally, demand for a reliable cheese ingredient supply also rises. Food manufacturing businesses connected to the quick-service ecosystem are also attracting new investments to support production capacity and product development. For example, a baked foods maker recently raised $21 million, highlighting continued capital flow into food products that frequently incorporate cheese ingredients across bakery and snack applications.

Restraining Factors

Fluctuating milk prices are affecting production costs

One of the major challenges facing the Cheese Ingredient Market is the fluctuation of milk prices, which directly affects production costs for cheese manufacturers. Milk is the primary raw material used to produce most cheese ingredients, and changes in dairy supply, feed costs, and agricultural conditions can lead to price volatility. These fluctuations can create uncertainty for producers and food manufacturers who depend on stable ingredient pricing.

When milk costs increase, the overall cost of cheese powders, sauces, spreads, and natural cheese ingredients can also rise. At the same time, investment continues to flow into dairy supply chains and food production companies. For instance, Country Delight raised $108 million, led by Venturi Partners and Temasek, strengthening its dairy distribution and supply capabilities.

Growing lactose intolerance among global consumers

Another restraint influencing the Cheese Ingredient Market is the growing awareness of lactose intolerance among consumers. A rising number of individuals are seeking dairy-free or lactose-free dietary options, which can affect the consumption of traditional cheese products. This shift has encouraged food manufacturers to explore alternative ingredients or reformulated dairy products to meet changing consumer preferences.

The trend toward digestive health and specialised diets is influencing product development across the broader food industry. Investment activity in health-focused food companies reflects these evolving consumer needs. For example, Sara Lee owner Grupo Bimbo became the lead investor in a $4 million funding round for Olyra, a brand focused on nutritious snack products designed to support healthier eating habits.

Growth Opportunity

Expansion of plant-based cheese ingredient alternatives

The development of plant-based cheese ingredient alternatives is creating new opportunities within the Cheese Ingredient Market. As consumer interest in plant-based diets grows, food manufacturers are exploring innovative ingredients made from oats, nuts, legumes, and other non-dairy sources. These alternatives are being incorporated into pizza toppings, sauces, dips, and ready-to-eat meals.

Plant-based cheese ingredients provide opportunities for brands to target vegan consumers as well as individuals seeking lactose-free options. Continuous innovation and investment are supporting the development of new food products across the broader alternative food sector. For example, David recently raised $10 million in seed funding for its snack bars, reflecting ongoing interest in developing innovative food products aligned with modern dietary preferences and evolving ingredient trends.

Increasing demand from emerging food markets

Emerging food markets are presenting significant opportunities for the Cheese Ingredient Market as consumer diets evolve and exposure to global cuisines increases. Rapid urbanisation, rising disposable incomes, and expansion of modern retail infrastructure are encouraging the consumption of processed and convenience foods that often include cheese ingredients. Foodservice growth in developing economies is also contributing to greater use of cheese in pizza, burgers, bakery products, and snack items.

As global food companies expand operations into these regions, demand for cheese ingredients continues to strengthen. Investment firms are also targeting the food and agriculture sectors to support market expansion. For instance, Entrepreneurial Equity Partners raised $423 million for its inaugural fund, aiming to invest in food and agriculture businesses that support long-term supply and production growth.

Latest Trends

Rising innovation in flavoured cheese ingredients

Innovation in flavoured cheese ingredients is emerging as an important trend within the Cheese Ingredient Market. Food manufacturers are experimenting with new flavour profiles to meet evolving consumer preferences for bold and distinctive tastes. Flavoured cheese powders, sauces, and spreads are increasingly used in snack products, bakery items, and ready meals. These innovations help brands differentiate products while maintaining the core taste appeal associated with cheese.

Product development is often supported by broader food industry investment aimed at expanding production and distribution capabilities. For example, Fruitist recently closed $150 million in funding to support retail expansion, reflecting strong investor interest in scaling innovative food products and strengthening its market presence.

Growth of clean-label cheese products

Clean label products are gaining popularity as consumers increasingly look for foods made with simple, recognisable ingredients. This trend is influencing the Cheese Ingredient Market, encouraging manufacturers to develop cheese ingredients with minimal additives and transparent labelling. Natural cheese forms, reduced processing methods, and simplified ingredient lists are becoming more common across food manufacturing and foodservice applications.

Clean label positioning helps brands appeal to health-conscious consumers while maintaining traditional flavour and functionality. Continued investment across the food sector is supporting innovation and product expansion aligned with these preferences. For instance, Fruitist also secured US$150 million in funding to support global expansion, strengthening its ability to scale product offerings across international markets.

Regional Analysis

Europe held 37.9% share of the Cheese Ingredient Market, reaching USD 15.8 Bn.

The Cheese Ingredient Market demonstrates strong regional demand across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, supported by expanding food processing industries and rising consumption of cheese-based products.

Europe dominates the global market, accounting for 37.9% of total revenue, valued at USD 15.8 Bn, driven by a well-established dairy sector, strong cheese production capabilities, and widespread consumption of cheese in processed foods, bakery, and ready meals. Countries across the region maintain a strong manufacturing base for natural and speciality cheese ingredients used by foodservice and packaged food industries.

North America represents another significant regional market, supported by high demand from pizza chains, quick-service restaurants, and frozen food manufacturers that extensively utilise cheese ingredients. The Asia Pacific region is witnessing increasing market expansion due to rapid urbanisation, growing Western food adoption, and rising demand for convenience foods containing cheese ingredients.

Meanwhile, the Middle East & Africa and Latin America are emerging markets, supported by improving retail infrastructure, expanding foodservice sectors, and growing consumer exposure to cheese-based cuisines, gradually strengthening regional demand for cheese ingredient products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, Lactalis remains a significant participant in the global cheese ingredient market due to its extensive dairy expertise and broad cheese product portfolio. The company’s strong operational presence in cheese manufacturing allows it to supply a variety of cheese ingredients used in food processing, ready meals, and foodservice applications. Its ability to maintain consistent product quality and large-scale production supports the growing demand from food manufacturers requiring a reliable cheese ingredient supply. Lactalis also benefits from its well-developed dairy sourcing network, which strengthens its capacity to provide stable volumes of cheese ingredients for diverse applications across multiple food categories.

Arla Foods continues to hold a notable position in the cheese ingredient market through its cooperative-based dairy structure and focus on high-quality milk sourcing. The company produces a wide range of cheese ingredients utilised in bakery, sauces, snacks, and prepared foods. Its integrated dairy operations enable efficient milk processing and consistent ingredient production, supporting large food manufacturers and foodservice providers. Arla Foods also emphasises product functionality, developing cheese ingredients that deliver desired melting, texture, and flavour characteristics required in modern food manufacturing processes.

Savencia Fromage & Dairy contributes to the global cheese ingredient market through its specialised cheese expertise and diversified dairy product capabilities. The company focuses on delivering cheese ingredients that meet the evolving needs of food producers seeking flavour, texture, and performance consistency. Its experience in cheese production allows Savencia to support food manufacturers with ingredient solutions suitable for processed foods, culinary applications, and foodservice offerings.

Top Key Players in the Market

- Lactalis

- Arla Foods

- Savencia Fromage Dairy

- Danone

- FrieslandCampina

- Royal Aware

- Bel Group

- Hochland

- Kerry Group

- Saputo

- Groupe Lactalis

- Fonterra

Recent Developments

- In September 2024, Danone North America made an offer of about $283 million to acquire Lifeway Foods, a company known for kefir dairy products. Lifeway’s board rejected the offer, and Danone later increased the proposal to around $307 million in November 2024. Danone works in dairy and nutrition products, including yoghurt and fermented dairy beverages, and the proposed acquisition aimed to strengthen its position in probiotic dairy drinks and related dairy ingredient products.

- In March 2024, Lactalis expanded its cheese production by acquiring Sequeira & Sequeira, a Portuguese cheese brand owner that also includes the subsidiary Lacticínios do Paiva. Lactalis works in dairy products such as cheese, milk, butter, and dairy ingredients, and this acquisition helped the company strengthen its cheese manufacturing presence in Portugal. The development allows Lactalis to increase production capacity and improve the supply of cheese used in food manufacturing and ingredient applications across European markets.

Report Scope

Report Features Description Market Value (2025) USD 41.7 Billion Forecast Revenue (2035) USD 70.7 Billion CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Cheese Type (Natural Cheese, Process Cheese, Cheese Powder, Cheese Sauce, Cheese Spread), By Source (Cow Milk, Goat Milk, Sheep Milk, Buffalo Milk), By Application (Pizza, Pasta, Sandwiches, Burgers, Salads, Sauces, Dips, Bakery Products, Snacks), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Food Service) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Lactalis, Arla Foods, Savencia Fromage Dairy, Danone, FrieslandCampina, Royal Aware, Bel Group, Hochland, Kerry Group, Saputo, Groupe Lactalis, Fonterra Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Lactalis

- Arla Foods

- Savencia Fromage Dairy

- Danone

- FrieslandCampina

- Royal Aware

- Bel Group

- Hochland

- Kerry Group

- Saputo

- Groupe Lactalis

- Fonterra

Our Clients

- 181432

- March 2026