Global Cauti Prevention Urology Products Market By Product (Antimicrobial & Coated Catheters, Closed Drainage Systems, External Catheters (Condom/Pouches), Intermittent (In-and-Out) Catheters, Catheter Securement Devices, Bladder Scanners and Others), By Application (Urinary Incontinence Management, Acute Surgical/Perioperative Care, Benign Prostatic Hyperplasia (BPH) and Obstructive Urology, Neurogenic Bladder & Spinal Cord Injury (SCI) and Others), By End Use (Hospitals, Long Term Care Facilities, Home Care Setting, Ambulatory Surgical Centers (ASCs) and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180489

- Number of Pages: 242

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

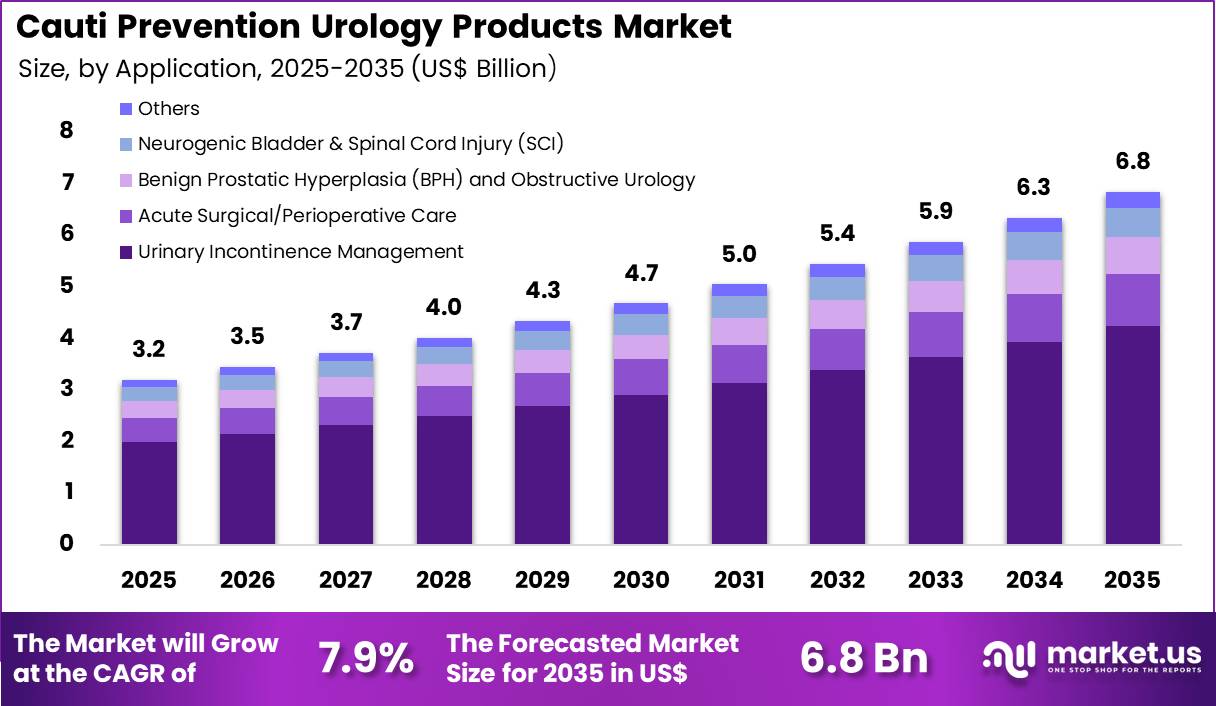

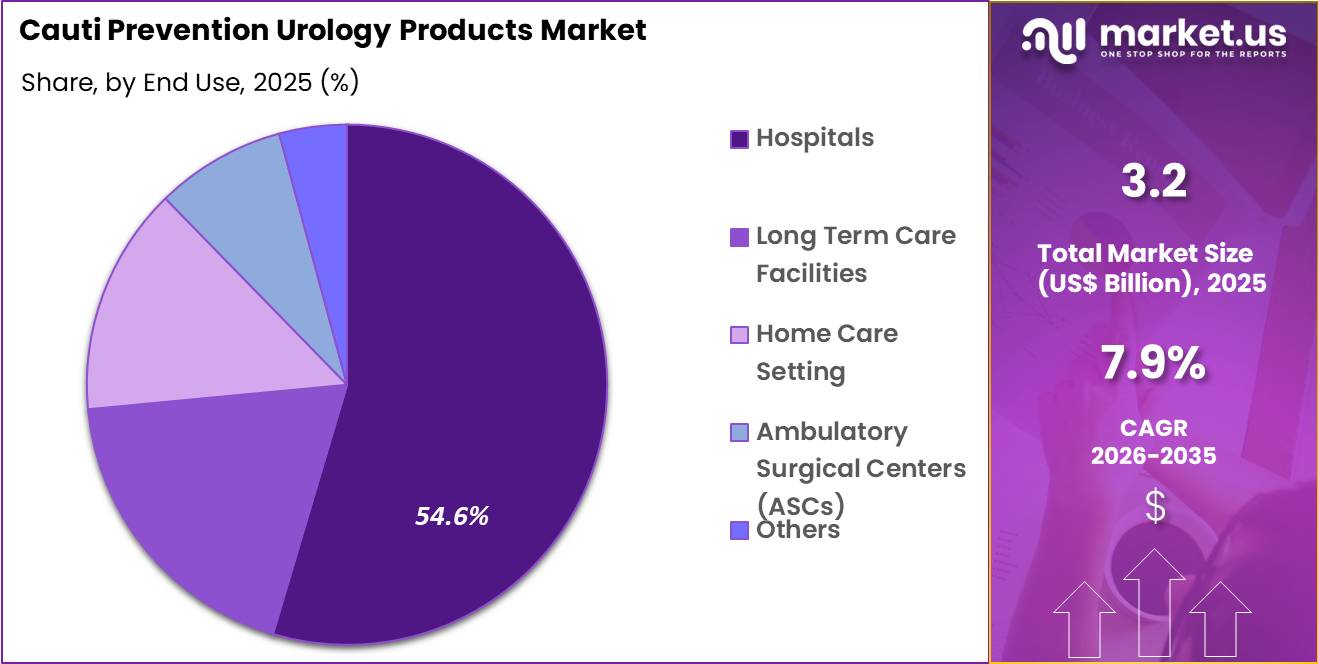

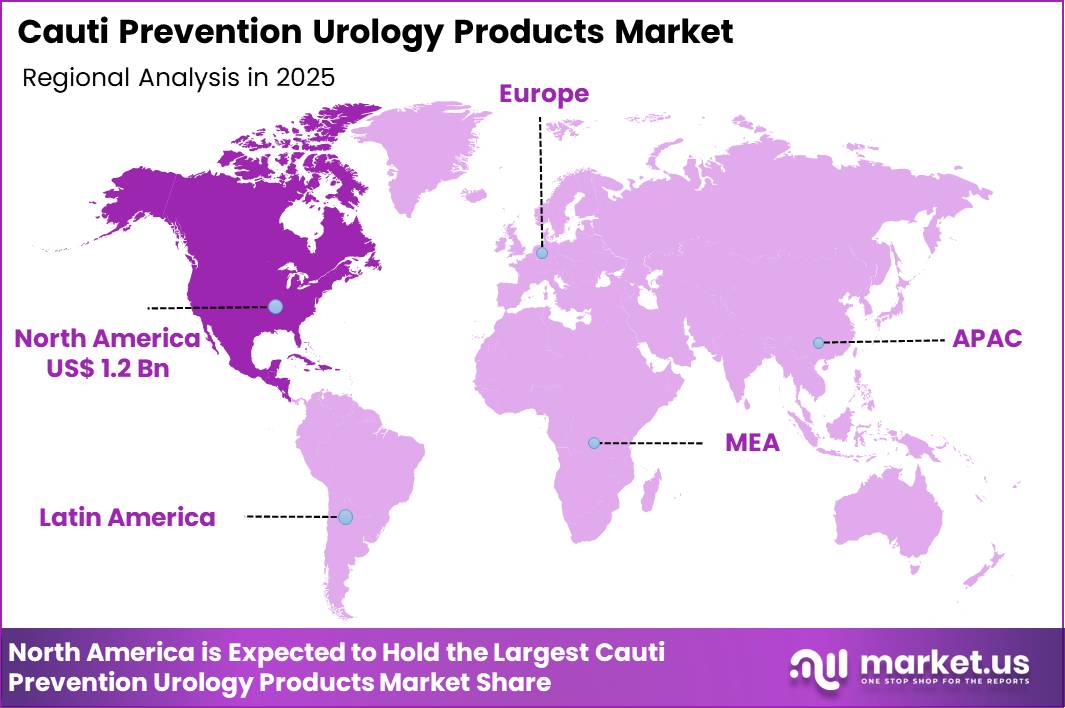

The Global Cauti Prevention Urology Products Market size is expected to be worth around US$ 6.8 Billion by 2035 from US$ 3.2 Billion in 2025, growing at a CAGR of 7.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.5% share with a revenue of US$ 1.2 Billion.

Rising incidence of catheter-associated urinary tract infections (CAUTI) compels healthcare facilities to prioritize prevention strategies that reduce infection risk and associated complications in hospitalized patients.

Urologists and critical care teams increasingly utilize antimicrobial-coated Foley catheters to inhibit bacterial adhesion and biofilm formation on the catheter surface, lowering CAUTI rates in patients requiring prolonged indwelling catheterization for postoperative recovery or acute urinary retention.

These products support intermittent catheterization programs through hydrophilic-coated catheters that minimize urethral trauma and bacterial colonization during repeated self-catheterization in neurogenic bladder patients. Nurses apply silver-alloy or antibiotic-impregnated catheters in high-risk settings such as spinal cord injury units, where long-term catheter use demands robust infection control to prevent recurrent episodes.

Closed drainage systems with pre-connected components further reduce contamination risks during insertion and maintenance in surgical and medical wards. In May 2024, Coloplast introduced a female version of its Luja intermittent catheter system designed to enable more complete bladder drainage in a single flow. The design focuses on improving urinary evacuation efficiency while helping reduce the likelihood of catheter-associated infections.

Manufacturers pursue opportunities to develop next-generation catheter systems with advanced coatings and drainage mechanisms, expanding applications in outpatient and home care settings where patients manage chronic urinary retention with intermittent self-catheterization.

Developers advance antimicrobial-impregnated intermittent catheters that maintain efficacy over multiple uses, broadening utility in spinal cord injury and multiple sclerosis populations requiring lifelong catheterization. These innovations facilitate integration with digital monitoring tools that track catheterization frequency and technique, supporting adherence and early intervention in high-risk patients.

Opportunities emerge in gender-specific designs and ergonomic features that enhance comfort and compliance, particularly for female patients. Companies invest in sustainable materials and single-use formats that align with infection control priorities.

In January 2025, Teleflex Incorporated obtained a national purchasing agreement with Vizient, a large healthcare performance improvement organization in the United States. The contract allows member hospitals to procure Teleflex arterial and central venous access catheter systems through Vizient’s sourcing network beginning in early 2025.

Recent trends emphasize evidence-based protocols and multimodal prevention bundles, positioning CAUTI prevention urology products as essential components of hospital quality improvement initiatives focused on patient safety and reduced healthcare-associated infections.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.2 Billion, with a CAGR of 7.9%, and is expected to reach US$ 6.8 Billion by the year 2035.

- The product segment is divided into antimicrobial & coated catheters, closed drainage systems, external catheters (condom/pouches), intermittent (in-and-out) catheters, catheter securement devices, bladder scanners and others, with closed drainage systems taking the lead with a market share of 37.1%.

- Considering application, the market is divided into urinary incontinence management, acute surgical/perioperative care, benign prostatic hyperplasia (BPH) and obstructive urology, neurogenic bladder & spinal cord injury (SCI) and others. Among these, urinary incontinence management held a significant share of 62.1%.

- Furthermore, concerning the end use segment, the market is segregated into hospitals, long term care facilities, home care setting, ambulatory surgical centers (ASCs) and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 54.6% in the market.

- North America led the market by securing a market share of 38.5%.

Product Analysis

Closed drainage systems accounted for 37.1% of growth within product and dominate the CAUTI prevention urology products market because they play a critical role in reducing catheter associated urinary tract infections. Healthcare organizations increasingly prioritize infection control measures that limit bacterial entry into catheter systems.

The Centers for Disease Control and Prevention reports that catheter associated infections represent one of the most common healthcare associated infections in hospitals. Hospitals therefore emphasize closed urinary drainage systems to maintain a sealed pathway between catheter and collection bag. This approach helps minimize contamination during long-term catheterization procedures.

Segment growth is expected to strengthen as hospitals implement stricter infection prevention protocols. Medical device manufacturers continue to improve drainage bag design and anti reflux valves to enhance safety.

Healthcare providers adopt standardized catheter care bundles that include closed drainage solutions. Demand is anticipated to increase as patient safety initiatives gain priority across global healthcare systems.

Application Analysis

Urinary incontinence management accounted for 62.1% of growth within application and dominate the CAUTI prevention urology products market due to the high prevalence of urinary disorders among aging populations. Clinical data show that millions of adults experience urinary incontinence worldwide, particularly among elderly patients and individuals with neurological disorders.

Healthcare providers rely on specialized catheterization and drainage solutions to maintain hygiene and prevent complications. Segment growth is projected to strengthen as global populations continue to age and chronic urological conditions increase.

Hospitals and long term care facilities implement structured incontinence management programs to reduce infection risk. Improved diagnostic awareness and early treatment also support higher adoption of urology management devices. Demand is likely to rise as patients seek improved comfort and infection prevention solutions in both clinical and home care environments.

End-Use Analysis

Hospitals accounted for 54.6% of growth within end use and dominate the CAUTI prevention urology products market because they manage the majority of catheterization procedures and infection control protocols. Hospitalized patients often require urinary catheterization during surgeries, intensive care treatments, and postoperative recovery.

Infection prevention programs implemented by hospitals emphasize strict catheter management practices to reduce complications. Segment growth is expected to strengthen as hospitals expand patient safety initiatives and adopt evidence based infection control guidelines.

Many healthcare systems monitor catheter associated infection rates as a quality performance indicator. Hospitals invest in advanced catheter systems, drainage devices, and monitoring tools to meet safety benchmarks. The segment is anticipated to continue leading as hospitals maintain high procedure volumes and prioritize infection reduction strategies.

Key Market Segments

By Product

- Antimicrobial & Coated Catheters

- Closed Drainage Systems

- External Catheters (Condom/Pouches)

- Intermittent (In-and-Out) Catheters

- Catheter Securement Devices

- Bladder Scanners

- Others

By Application

- Urinary Incontinence Management

- Acute Surgical/Perioperative Care

- Benign Prostatic Hyperplasia (BPH) and Obstructive Urology

- Neurogenic Bladder & Spinal Cord Injury (SCI)

- Others

By End Use

- Hospitals

- Long Term Care Facilities

- Home Care Setting

- Ambulatory Surgical Centers (ASCs)

- Others

Drivers

Increasing revenue from urology and critical care products is driving the market.

Becton Dickinson and Company reported Urology and Critical Care segment revenue of $1,649 million for the full fiscal year ended 30 September 2025. This figure advanced from $1,554 million in the full fiscal year ended 30 September 2024. The growth equated to 6.1 percent on a foreign-currency-neutral basis and 5.9 percent organically.

Performance stemmed from sustained demand for advanced urine management solutions designed to minimize infection risks. External collection systems within the portfolio enable avoidance of indwelling catheters in eligible patients. Hospitals integrate these technologies to align with infection prevention protocols.

The upward trajectory supports broader investment in product innovation and manufacturing capacity. Clinicians benefit from reliable options that enhance patient mobility while reducing complication rates. Supply chain enhancements further facilitate consistent availability across care settings. This driver propels ongoing expansion of prevention-focused urology offerings throughout the sector.

Restraints

Uneven reductions in CAUTI rates across hospital locations is restraining the market.

The Centers for Disease Control and Prevention documented a 10 percent national decrease in CAUTI standardized infection ratio for acute care hospitals in 2024 compared with 2023. Intensive care unit locations achieved a 15 percent reduction over the same interval. Ward locations recorded only an 8 percent decline during this period.

The disparity highlights inconsistencies in protocol implementation and resource allocation. Facilities with limited staffing or training programs experience slower progress in prevention adoption. Variability in patient acuity and device utilization further complicates uniform outcomes. Such uneven results limit the perceived urgency for widespread equipment upgrades in lower-acuity areas.

Manufacturers encounter moderated demand from segments demonstrating slower improvement. The pattern affects overall market velocity as institutions prioritize high-impact settings first. This restraint moderates the pace of comprehensive penetration for advanced prevention technologies.

Opportunities

Strong double-digit growth in the PureWick franchise is creating growth opportunities.

Becton Dickinson and Company highlighted strong double-digit growth within its PureWick franchise as a key contributor to Urology and Critical Care performance in fiscal year 2025. The portfolio encompasses male and female external urine collection systems that serve as alternatives to traditional indwelling catheters.

Opportunities arise for expanded application in home care and long-term settings where mobility preservation is essential. Providers can leverage these systems to improve patient comfort and reduce associated complications. The growth trajectory enables deeper penetration into outpatient and post-acute markets.

Manufacturers gain capacity to develop complementary accessories and digital monitoring integrations. Educational initiatives for caregivers can accelerate adoption beyond hospital walls. The strengthened franchise supports portfolio diversification without proportional increases in traditional catheter reliance.

Such opportunities foster resilient revenue streams and enhanced therapeutic alignment. This framework positions participants for scalable advancement in infection prevention strategies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the CAUTI prevention urology products market through hospital operating budgets, infection control spending, and procurement priorities. Inflation raises the cost of antimicrobial coatings, medical grade plastics, packaging materials, and sterilization processes, which increases production and supply expenses for manufacturers.

Higher interest rates limit capital flexibility for healthcare facilities, which can slow bulk purchasing of advanced catheter systems and monitoring tools. Geopolitical tensions affect global sourcing of specialty polymers, coatings, and manufacturing inputs, creating uncertainty in supply continuity.

Current US tariffs on imported medical components and raw materials raise overall procurement costs and compress supplier margins. These pressures may delay purchasing cycles in cost-sensitive healthcare systems.

At the same time, providers strengthen domestic supply partnerships and focus on infection prevention programs to reduce hospital-acquired complications. Growing regulatory emphasis on patient safety and infection control continues to support steady and confident market growth.

Latest Trends

National reductions in CAUTI SIR across acute care hospitals is driving the market.

The Centers for Disease Control and Prevention reported a 10 percent decrease in the national CAUTI standardized infection ratio for acute care hospitals when comparing 2024 data with 2023. This improvement reflects intensified utilization of evidence-based prevention products and protocols nationwide.

Intensive care units contributed a 15% reduction while wards achieved an 8 percent decline within the same timeframe. The progress underscores the effectiveness of coordinated interventions in high-volume settings. Facilities achieving superior outcomes gain recognition through public reporting mechanisms.

The trend encourages continued investment in technologies that support catheter avoidance and maintenance best practices. Stakeholders observe accelerated integration of external management systems into standard care pathways.

The documented reductions validate clinical and economic value across diverse hospital types. Such advancements stimulate innovation in device design and training programs. Overall, the 2024 pattern establishes a benchmark that sustains forward momentum in urology prevention solutions.

Regional Analysis

North America is leading the Cauti Prevention Urology Products Market

North America accounted for 38.5% of the CAUTI prevention urology products market in 2025 as hospitals intensified infection control programs and strengthened surveillance protocols across inpatient care units. Catheter associated urinary tract infections remain one of the most common healthcare associated infections in the United States, and the Centers for Disease Control and Prevention reports that about 75% of hospital UTIs are linked to urinary catheter use.

Hospitals therefore expanded procurement of antimicrobial coated catheters, closed drainage systems, and catheter securement technologies to reduce infection risk and improve patient safety metrics. Federal quality reporting programs and hospital accreditation standards encouraged healthcare providers to adopt advanced catheter management protocols.

Health systems also invested in nurse training programs and catheter stewardship initiatives that emphasize early removal and infection monitoring. Growth in surgical procedures and intensive care admissions increased catheter utilization, which in turn strengthened demand for preventive devices designed to reduce infection complications.

Device manufacturers collaborated with hospital networks to introduce improved coatings and antimicrobial technologies that enhance infection resistance. Increased focus on patient safety outcomes and reimbursement incentives for infection reduction further supported adoption across healthcare facilities. These combined factors contributed to sustained expansion of CAUTI prevention solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to register notable growth during the forecast period as healthcare systems strengthen infection control programs and expand access to hospital care across developing economies. Many countries in the region are improving hospital hygiene infrastructure while addressing a high burden of healthcare associated infections.

The World Health Organization reported in 2022 that healthcare associated infections affect about 15% of hospitalized patients in low and middle income countries, highlighting a substantial need for improved infection prevention practices. Governments across China, India, and Southeast Asia are investing in hospital modernization programs and national infection control guidelines that promote safer catheter management.

Hospitals are increasing procurement of antimicrobial catheters, closed drainage systems, and bladder monitoring technologies to reduce complications during long term catheterization. Medical training institutions are also strengthening clinical education on catheter handling and infection prevention protocols.

Expansion of tertiary hospitals and private healthcare networks is improving availability of advanced urology care across urban and semi urban regions. Regional manufacturers are introducing affordable infection control devices tailored for cost sensitive healthcare systems. Rising awareness of hospital safety standards and regulatory improvements are expected to encourage broader adoption of infection prevention technologies throughout Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key participants in the Cauti Prevention Urology Products market expand their presence by investing in antimicrobial catheter technologies, closed drainage systems, and non-invasive urine management solutions that help hospitals reduce infection risk.

Companies strengthen growth through clinical training programs, infection-control collaborations with healthcare providers, and continuous product innovation aimed at lowering catheter-associated urinary tract infection rates.

Medical device manufacturers increasingly introduce coated catheters and external urine collection systems designed to limit microbial adhesion and decrease indwelling catheter usage in hospitals and long-term care facilities.

Becton, Dickinson and Company represents a major participant in the Cauti Prevention Urology Products market and operates as a global medical technology firm founded in 1897 with headquarters in New Jersey, United States. The company develops a wide range of medical devices and infection-prevention technologies used across hospitals worldwide.

Industry competitors also pursue regulatory approvals, research collaborations, and targeted product launches to strengthen infection-control portfolios and expand clinical adoption. These strategic initiatives improve patient safety, support hospital infection-reduction programs, and reinforce competitive positioning across the Cauti Prevention Urology Products market.

Top Key Players

- BD (Becton, Dickinson and Company)

- B. Braun SE

- Coloplast

- Teleflex Incorporated

- Cook Medical

- Medtronic

- Hollister Incorporated

- ConvaTec Group PLC

- Boston Scientific Corporation

- Cardinal Health

- Merit Medical

- Medline Industries, LP.

- Poiesis Medical LLC

Recent Developments

- In November 2025, Becton, Dickinson and Company introduced the PureWick Portable Collection System, a cordless urine collection solution designed specifically for wheelchair users. The device enables discreet fluid management while allowing patients greater freedom of movement in home and community environments.

- In June 2025, Teleflex Incorporated shared results from an international observational study assessing its Arrow central venous catheters treated with chlorhexidine. The research evaluated more than 6,600 patients treated across intensive care units in several countries and examined how the antimicrobial technology supports infection prevention during vascular access procedures.

- In February 2023, Coloplast released a redesigned male catheter developed to enhance safety during intermittent catheterization by lowering the potential risk of urinary tract infections.

- In March 2023, Coloplast presented clinical evaluation results indicating that the Luja catheter demonstrated more effective bladder emptying performance compared with a standard competing catheter product.

Report Scope

Report Features Description Market Value (2025) US$ 3.2 Billion Forecast Revenue (2035) US$ 6.8 Billion CAGR (2026-2035) 7.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Antimicrobial & Coated Catheters, Closed Drainage Systems, External Catheters (Condom/Pouches), Intermittent (In-and-Out) Catheters, Catheter Securement Devices, Bladder Scanners and Others), By Application (Urinary Incontinence Management, Acute Surgical/Perioperative Care, Benign Prostatic Hyperplasia (BPH) and Obstructive Urology, Neurogenic Bladder & Spinal Cord Injury (SCI) and Others), By End Use (Hospitals, Long Term Care Facilities, Home Care Setting, Ambulatory Surgical Centers (ASCs) and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape BD, B. Braun, Coloplast, Teleflex, Cook Medical, Medtronic, Hollister, ConvaTec, Boston Scientific, Cardinal Health, Merit Medical, Medline, Poiesis Medical. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Cauti Prevention Urology Products MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Cauti Prevention Urology Products MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BD (Becton, Dickinson and Company)

- B. Braun SE

- Coloplast

- Teleflex Incorporated

- Cook Medical

- Medtronic

- Hollister Incorporated

- ConvaTec Group PLC

- Boston Scientific Corporation

- Cardinal Health

- Merit Medical

- Medline Industries, LP.

- Poiesis Medical LLC

Our Clients

- 180489

- March 2026