Quick Navigation

Report Overview

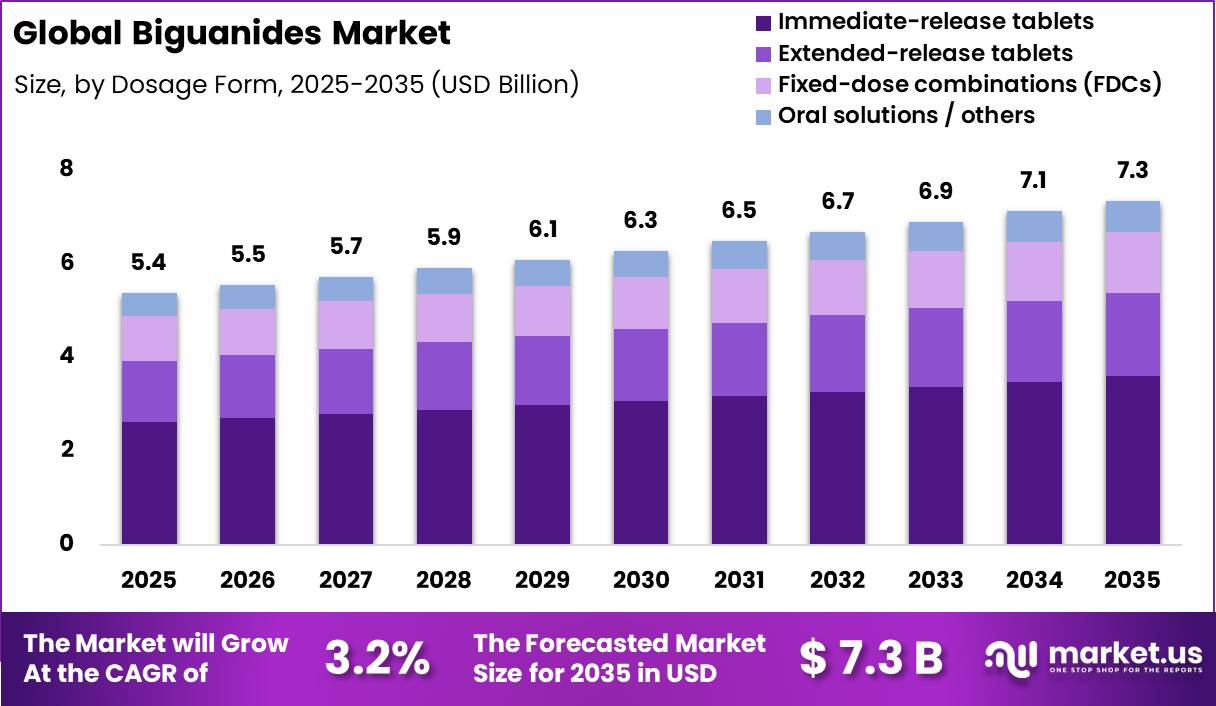

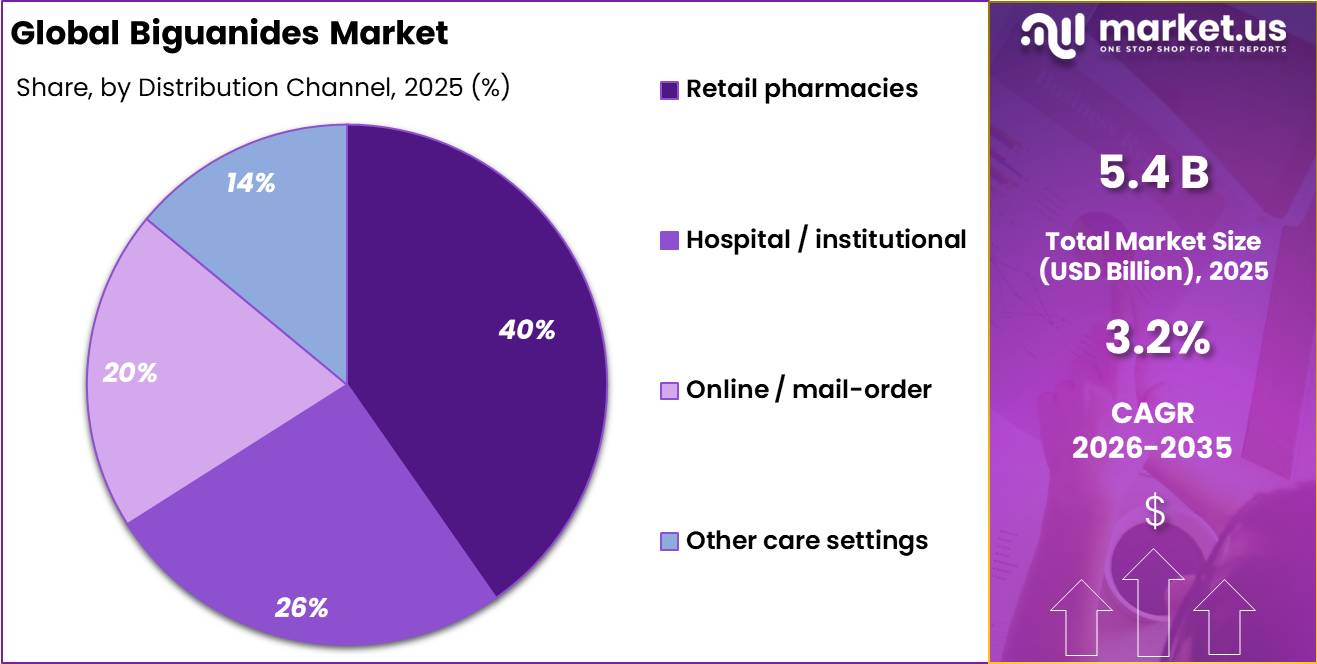

Global Biguanides Market size is expected to be worth around US$ 7.3 Billion by 2035 from US$ 5.4 Billion in 2025, growing at a CAGR of 3.2% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.1% share with a revenue of US$ 2.15 Billion.

Biguanides are a class of oral medicines widely used for the management of Type 2 Diabetes. The most commonly prescribed biguanide is Metformin, which is recommended as a first-line treatment alongside healthy lifestyle changes for many adults with the condition.

Biguanides primarily work by reducing glucose production in the liver, improving the body’s sensitivity to insulin, and decreasing the absorption of glucose from the intestine. Unlike some other diabetes medicines, metformin generally does not cause significant weight gain and carries a low risk of hypoglycemia when used alone.

According to the World Health Organization, approximately 830 million people worldwide were living with diabetes in 2022, highlighting the growing need for effective and accessible treatments. In addition, the Centers for Disease Control and Prevention estimates that more than 38 million people in the United States have diabetes, with 90–95% of cases being type 2 diabetes. These figures emphasize the important role of established therapies such as metformin in diabetes management.

Healthcare professionals recommend that biguanides should be used under medical supervision, particularly in patients with kidney disease or other underlying health conditions, as dosage adjustments or alternative therapies may be required.

Regular monitoring of blood glucose levels, kidney function, and overall treatment response helps ensure safe and effective long-term use. Lifestyle measures, including balanced nutrition, regular physical activity, and weight management, remain essential components of comprehensive diabetes care alongside biguanide therapy.

Key Takeaways

- Market Size: Global Biguanides Market size is expected to be worth around US$ 7.3 Billion by 2035 from US$ 5.4 Billion in 2025.

- Market Share: The market is growing at a CAGR of 3.2% during the forecast period from 2026 to 2035.

- Dosage Form Analysis: Immediate-release tablets dominated the market, accounting for 48.9% of the total market share in 2025.

- Type Analysis: Metformin remained the leading segment, constituting 85.1% of the global biguanides market.

- Application Analysis: Type 2 diabetes represented the largest segment, holding 80.1% of the market share due to its widespread use as a first-line therapy.

- Distribution Channel Analysis: Retail pharmacies led the market, accounting for 40.3% of total revenue in 2025.

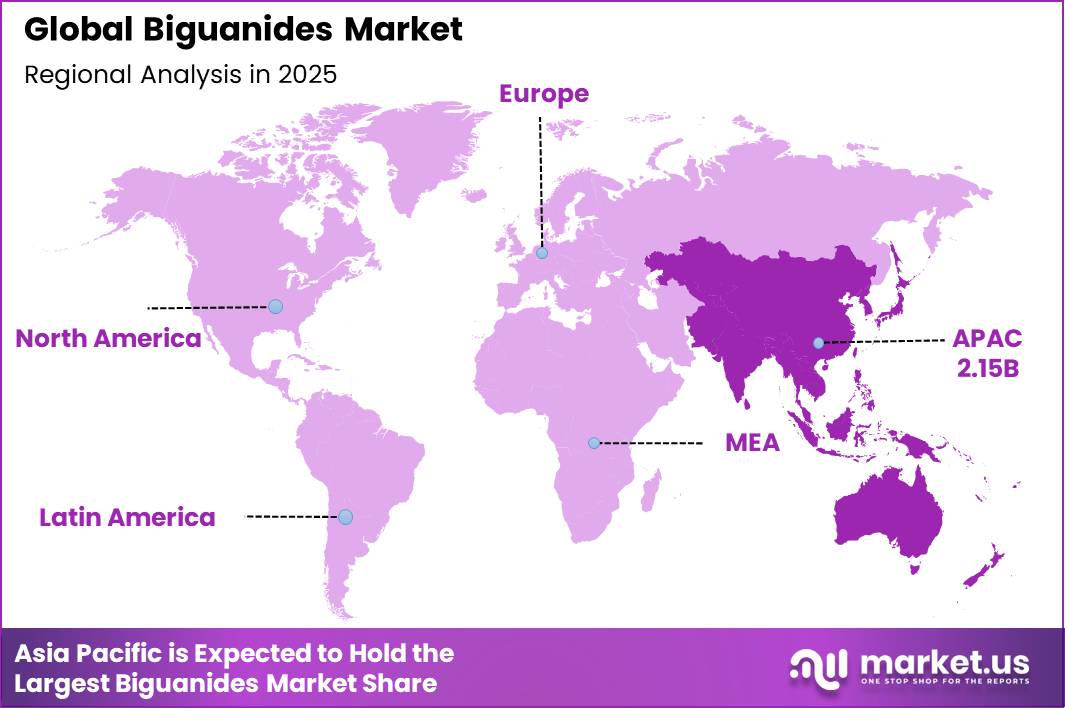

- Regional Analysis: Among regions, Asia Pacific emerged as the dominant regional market, capturing 40.1% of the global market share, supported by the high prevalence of diabetes and expanding access to affordable antidiabetic medications.

Dosage Form Analysis

Immediate-Release Tablets represents the dominant segment of the Biguanides Market.

The global biguanide market was dominated by immediate-release tablets, which accounted for 48.9% of total sales. The global biguanide market was dominated by immediate-release (IR) tablets, which accounted for 48.9% of total sales.

This leadership is primarily driven by the manufacturing efficiency, high patient compliance, and unparalleled cost-effectiveness of immediate-release formulations compared to extended-release (ER) alternatives or liquid suspensions. Affordability remains the critical macroeconomic factor supporting this segment’s growth.

According to the International Diabetes Federation (IDF), around 26.9% of households in low-income countries struggle to afford basic diabetes medicines. Because they are significantly cheaper to produce, low-cost generic immediate-release tablets serve as the most accessible oral antidiabetic option for a massive share of the global population. This compelling combination of reliable pharmacokinetics and budget-conscious pricing ensures immediate-release tablets will sustain their dominance in the dosage form market.

Type Analysis

Metformin a significant type

Metformin maintained a commanding presence in the global biguanides market in 2025, accounting for 85.1% of total market revenue. This dominance is a direct reflection of its deeply entrenched role as the most clinically endorsed first-line therapy for type 2 diabetes worldwide.

Its leadership is supported by one of the largest prescription bases in modern healthcare; globally, the drug is used by approximately 150 million people every day. In the United States alone, metformin was the second most prescribed medication in 2023, with more than 85 million prescriptions dispensed.

The drug’s market position is fortified by the World Health Organization (WHO), which includes metformin on its Essential Medicines List—a procurement reference in over 150 countries. Furthermore, leading organizations like the American Diabetes Association (ADA) and the International Diabetes Federation (IDF) continue to recommend it as the preferred initial therapy.

Segment growth is further accelerated by expanding off-label therapeutic applications. The WHO estimates that 10–13% of women of reproductive age are affected by polycystic ovary syndrome (PCOS), with global cases rising 89.6% from 36.65 million in 1990 to 69.47 million in 2021. Due to its insulin-sensitizing properties, metformin has become widely adopted in PCOS management, securing a vastly expanding patient base that will sustain its dominant market position throughout the forecast period.

Application Analysis

Global Biguanide Market Growth Continues to Be Led by Type 2 Diabetes Applications.

Type 2 diabetes accounted for 80.1% of the global biguanides market revenue in 2025, primarily due to its large patient population and the widespread use of metformin as the standard first-line treatment. The segment’s dominance closely reflects the global diabetes burden, as the IDF Diabetes Atlas 2025 estimates that more than 90% of the world’s 589 million diabetes patients are affected by type 2 diabetes. This creates a substantial and sustained demand base for biguanide therapies.

The growing prevalence of the disease further strengthens market demand. According to a 2024 Lancet study conducted by the NCD Risk Factor Collaboration (NCD-RisC) and the WHO, adult diabetes prevalence doubled from 7% in 1990 to 14% in 2022, resulting in more than a four-fold increase in total diabetes cases worldwide. Much of this growth has been driven by rising type 2 diabetes rates in low- and middle-income countries. The WHO also identifies elevated blood glucose as one of the leading metabolic risk factors contributing to non-communicable disease (NCD) deaths globally.

Clinical guidelines continue to support long-term demand for biguanides. Both the American Diabetes Association (ADA) Standards of Care 2024 and IDF clinical guidelines recommend metformin as the preferred first-line medication for newly diagnosed type 2 diabetes patients without contraindications. In addition, nearly 75% of people living with diabetes reside in low- and middle-income countries, where affordable oral medications remain the most practical treatment option. As a result, type 2 diabetes is expected to remain the primary driver of biguanide consumption throughout the forecast period.

Meanwhile, PCOS/endocrine and metabolic off-label treatments, weight management, and developing R&D applications all offer substantial market opportunities. Metformin is increasingly used to treat polycystic ovarian syndrome (PCOS), insulin resistance, and other metabolic disorders because of its ability to enhance insulin sensitivity and metabolic outcomes.

Biguanides’ therapeutic scope is being expanded further by growing research interest in obesity management, healthy aging, cardiovascular health, and possible oncology uses. As healthcare providers prioritize preventative metabolic care and researchers continue to investigate new therapeutic applications, these categories are likely to contribute steadily to market expansion during the forecast period.

Distribution Channel Analysis

Retail Pharmacies held a major share of the market.

Retail pharmacies held a dominant 40.3% share of the global biguanides market in 2025, supported by the long-term treatment requirements of type 2 diabetes and the extensive reach of community pharmacy networks worldwide. Biguanides, particularly metformin, are used as daily medications and require continuous prescription refills, making retail pharmacies the primary distribution channel for patients managing chronic diabetes.

The strength of this segment is supported by the scale of the global pharmacy infrastructure. According to the International Pharmaceutical Federation (FIP) 2025 Global Pharmacy Workforce Report, more than 5.57 million pharmacists are licensed across 83 countries, with over 77% working in community and retail pharmacy settings. This makes retail pharmacies the most accessible healthcare touchpoint for millions of patients.

The importance of these networks is further highlighted by estimates from the WHO and the Access to Medicine Foundation, which indicate that nearly 2 billion people, or about one-third of the global population, still lack regular access to essential medicines. As a result, many governments continue to expand community pharmacy networks to improve medicine availability.

Retail pharmacies are especially important in major diabetes markets such as China, with approximately 148 million diabetes patients, and India, with around 89.8 million patients. Their broad geographic presence, affordable dispensing services, and easy access to generic metformin support high sales volumes.

In addition, prescription medicines account for approximately 54% of total retail pharmacy revenue globally, while chronic disease treatments represent the largest repeat-purchase category. These factors continue to strengthen the leading position of retail pharmacies in the global biguanides market.

Online and mail-order pharmacies are anticipated to witness the fastest growth during the forecast period, driven by the increasing adoption of digital healthcare platforms, growing internet penetration, and rising consumer preference for convenient medication purchasing options. These channels offer benefits such as home delivery services, easy prescription management, competitive pricing, and improved accessibility for patients in remote locations.

Meanwhile, hospital and institutional pharmacies continue to play a critical role in treatment initiation, inpatient care, and management of patients with complex metabolic conditions. Other healthcare settings, including specialty clinics and integrated care centers, also contribute to market growth by expanding patient access to diabetes treatment and supporting comprehensive disease management programs.

Key Market Segments

By Dosage Form

- Immediate‑release tablets

- Extended‑release tablets

- Fixed‑dose combinations (FDCs)

- Oral solutions / others

By Type

- Metformin

- Other biguanides

By Application

- Type 2 diabetes

- PCOS / endocrine & metabolic off‑label

- Weight management

- Emerging, R&D and other

By Channel

- Retail pharmacies

- Hospital / institutional

- Online / mail‑order

- Other care settings.

Driver

Prediabetes Screening Expanding Early Metformin Use

Improved screening and prevention pathways are converting prediabetes from a passive risk state into an actively managed segment, particularly in the U.S. The National Institute of Diabetes and Digestive and Kidney Diseases estimates that 97.6 million U.S. adults had prediabetes in 2021, creating a large pool for early intervention.

Policy support is also strengthening: Centers for Medicare & Medicaid Services expanded the Medicare Diabetes Prevention Program in 2026 by removing the once in a lifetime participation limit, enabling eligible beneficiaries to re-enter structured prevention services.While lifestyle modification remains first line, many high risk or persistently dysglycemic patients are now managed more proactively, opening a wider role for low cost, well established metformin as an early pharmacologic option to delay progression to type 2 diabetes.

Commercially, this shifts metformin demand upstream, from maintenance therapy in diagnosed diabetes toward prevention linked prescribing, supporting higher prescription volumes across primary care, endocrinology, and population health programs rather than relying solely on later stage diabetes treatment.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetes burden expansion lifting first-line biguanide volumes | +2.2% | North America core, EU, China, India, MENA urban clusters | Medium term (2-4 years) |

| Prediabetes screening and prevention pathways widening early metformin use | +1.4% | U.S. core, OECD markets, urban APAC spill-over | Short term (≤ 2 years) |

| CKD-compatible treatment positioning preserving metformin in combination regimens | +1.6% | U.S., EU5, Japan, South Korea, China tertiary care corridors | Medium term (2-4 years) |

| Essential-medicine status and low-cost access supporting public-sector procurement | +1.3% | LMICs, South Asia, Sub-Saharan Africa, Latin America public systems | Long term (≥ 4 years) |

| Quality-control tightening after nitrosamine scrutiny improving supply normalization | +0.9% | U.S., EU, India API/export hubs, global generic channels | Short term (≤ 2 years) |

| Long-term safety monitoring increasing clinical persistence through managed surveillance | +0.8% | North America, EU, Australia, advanced hospital systems in APAC | Medium term (2-4 years) |

Challenge

NDMA Quality Control Burden in Metformin Manufacturing

Ongoing concerns around NDMA impurities have shifted metformin manufacturing from routine compliance to a higher cost, higher friction quality control environment. Since late 2010s monitoring campaigns, a portion of tested batches have shown NDMA levels above conservative thresholds, leading to targeted recalls and intensified regulatory scrutiny rather than broad market withdrawal.

For large scale generic producers, this has increased analytical and validation requirements, including GC MS/MS and LC MS/MS testing, stability studies, and batch revalidation, raising direct manufacturing costs by roughly 1 to 2 % per unit. Release timelines can also extend by 5 to 10 days per batch, reducing effective inventory flexibility and increasing reliance on larger safety stocks.These constraints are compounded by process redesign needs to minimize nitrosamine formation, including changes to synthesis routes, solvent systems, and reactor controls.

Together, this creates additional CAPEX pressure and operational inefficiency, contributing to an estimated 0.7 % point drag on potential CAGR.In response, manufacturers are increasingly adopting multi site testing, dual sourcing of intermediates, and process analytical technologies PAT to stabilize impurity control over a 2 to 4 year horizon, rather than relying on reactive batch level interventions.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| NDMA quality-control burden | -0.7% | US, EU, Australia, regulated APAC | Medium term (2-4 years) |

| Safety–monitoring and lactic acidosis risk | -0.5% | Global hospital & primary care systems | Long term (≥ 4 years) |

| GI intolerance and adherence erosion | -0.9% | Global, high-volume T2D populations | Long term (≥ 4 years) |

| Competitive pressure from GLP-1 and combos | -1.3% | US, EU, urban EMs | Long term (≥ 4 years) |

| Off-label expansion complexity | -0.6% | US, EU, select Asia & LATAM | Medium term (2-4 years) |

| Manufacturing cost and supply chain volatility | -0.8% | India, China, global generic hubs | Medium term (2-4 years) |

Restraints

NDMA Quality Control Burden in Metformin Manufacturing

Ongoing concerns around NDMA impurities have shifted metformin manufacturing from routine compliance to a higher cost, higher friction quality control environment. Since late 2010s monitoring campaigns, a portion of tested batches have shown NDMA levels above conservative thresholds, leading to targeted recalls and intensified regulatory scrutiny rather than broad market withdrawal.

For large scale generic producers, this has increased analytical and validation requirements, including GC MS/MS and LC MS/MS testing, stability studies, and batch revalidation, raising direct manufacturing costs by roughly 1 to 2 % per unit. Release timelines can also extend by 5 to 10 days per batch, reducing effective inventory flexibility and increasing reliance on larger safety stocks.These constraints are compounded by process redesign needs to minimize nitrosamine formation, including changes to synthesis routes, solvent systems, and reactor controls.

Together, this creates additional CAPEX pressure and operational inefficiency, contributing to an estimated 0.7 % point drag on potential CAGR.In response, manufacturers are increasingly adopting multi site testing, dual sourcing of intermediates, and process analytical technologies PAT to stabilize impurity control over a 2 to 4 year horizon, rather than relying on reactive batch level interventions.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NDMA-linked metformin recalls & testing burden | -1.4% | North America core, EU, India export hubs | Medium term (2–4 years) |

| API concentration risk in India & China | -1.2% | APAC corridors, Latin America, Africa | Medium term (2–4 years) |

| Tightening diabetes therapy guidelines & pricing controls | -0.9% | EU, UK, Canada, select APAC | Long term (≥ 4 years) |

| cGMP compliance gaps and FDA/EMA enforcement | -1.1% | Emerging manufacturing bases, global exporters | Short to medium term (≤ 4 years) |

| Logistics disruption and cold-chain prioritization | -0.8% | Global, with higher impact in low-income markets | Short term (≤ 2 years) |

Opportunity

Metformin Cardiometabolic Bundling for Outcome Based Risk Management

Cardiometabolic bundling reframes metformin and related biguanides as anchor therapies within integrated diabetes, cardiovascular, and kidney risk management packages rather than standalone glucose lowering drugs.

This aligns with the growing burden of multimorbidity as global diabetes prevalence is projected to rise from approximately 463 million to around 700 million adults by 2045, alongside rising healthcare spend already exceeding USD 1 trillion annually.In bundled models, payers shift focus from per prescription reimbursement to outcomes based contracts that reward reductions in cardiovascular events, hospitalizations, and renal decline.

Metformin’s established associations with lower mortality in high risk cardiometabolic populations make it a cost efficient backbone therapy for such programs.If bundled care models capture even 10 to 15 % of current fee for service spending, and deliver modest outcome improvements such as 5 to 8 % fewer hospital readmissions and 10 to 15 % mortality reduction in selected cohorts, payers could justify incremental per patient spending while reducing downstream costs.

This creates an estimated USD 8 to 18 billion in additional annual value globally across eligible populations.For manufacturers and health systems, this shift depends on adoption of composite endpoints, multi year risk sharing contracts, and integrated care pathways. While still early stage, successful execution could expand margins by 300 to 500 basis points by linking low cost drugs to high value outcome improvements rather than unit volume.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Cardiometabolic risk bundle integration | +2.5% | North America, EU, urban APAC | Short–Medium term (≤ 4 years) |

| Pre-diabetes and obesity therapeutic expansion | +3.2% | APAC emerging, Latin America, Middle East | Medium term (2–4 years) |

| Fixed-dose combos with SGLT2/GLP-1 | +2.0% | North America core, EU, Japan | Medium–Long term (≥ 3 years) |

| Long-acting and novel delivery formats | +1.8% | Global, with LMIC focus | Long term (≥ 4 years) |

| Value-based chronic care contracts | +2.2% | US, UK, Nordics, select APAC | Short–Medium term (≤ 4 years) |

| LMIC formulary and distribution optimization | +2.8% | Africa, South Asia, Southeast Asia | Medium–Long term (3–6 years) |

Geopolitical Impact Analysis

Geopolitical developments are creating significant challenges for the biguanides market due to the heavy concentration of Active Pharmaceutical Ingredient (API) production in China. Metformin hydrochloride, the most widely used biguanide drug, depends on dimethylamine and other key raw materials that are largely supplied by China. The country accounts for approximately 40% of global API production by volume, with API exports reaching US$43.0 billion in 2024, reflecting 5.1% year-over-year growth. This concentration increases supply chain risk, particularly for India, which sources around 60–80% of its API raw material requirements from China despite being one of the world’s largest pharmaceutical exporters.

Trade tensions have further intensified these risks. A 54.9% China-specific tariff on pharmaceutical APIs could increase U.S. generic drug prices by an average of 11.3%, while a 100% global API tariff could raise prescription costs by approximately 30%. In October 2025, the U.S. introduced a 100% tariff on imported patented pharmaceuticals from certain countries, while products from the EU, Japan, and South Korea became subject to tariffs of around 15%, increasing pressure on pharmaceutical manufacturers to diversify sourcing and invest in domestic production.

Logistics disruptions have added further cost pressure across the biguanides supply chain. According to the IMF, Red Sea disruptions in early 2024 reduced Suez Canal traffic by approximately 50%, forcing vessels to reroute around the Cape of Good Hope. This increased shipping distances by nearly 40% and extended transit times by 10 days or more. In response, India expanded its Bulk Drug Production Linked Incentive (PLI) Scheme, attracting investments of more than ₹40,890 crore (about US$4.9 billion) by September 2025 and generating domestic API sales of ₹26,123 crore.

At the global level, the WHO’s 3rd World Local Production Forum in April 2025 brought together 4,077 participants from 141 countries, highlighting pharmaceutical supply chain localization as a strategic priority. These developments are increasing production costs and narrowing margins for generic metformin manufacturers, making supply chain diversification and dual-sourcing essential for long-term stability.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Biguanides Market.

In 2025, Asia Pacific led the worldwide biguanides market in 2025, accounting for 40.1% of total sales. The region’s leadership is mostly due to the fast expanding burden of type 2 diabetes, rising obesity rates, and the increasing incidence of other metabolic illnesses. China and India have some of the world’s largest diabetic populations, resulting in significant and persistent demand for cost-effective antidiabetic medicines like metformin.

Government activities aimed at diabetes awareness, early diagnosis, and disease management are accelerating treatment acceptance throughout the region. Furthermore, strengthening healthcare infrastructure, boosting health insurance coverage, and increasing access to important drugs all improve patient access to diabetic care. The broad availability of affordable metformin products, as well as the significant presence of generic pharmaceutical makers, continue to market growth.

North America and Europe are large markets for biguanides, thanks to modern healthcare systems, high diabetes awareness, advantageous reimbursement structures, and widespread acceptance of evidence-based treatment guidelines. The growing emphasis on preventive healthcare, chronic illness management, and combination medicines continues to drive demand in both regions.

Latin America is experiencing steady expansion as diabetes prevalence rises, healthcare access improves, and government-led disease management initiatives increase. Meanwhile, the Middle East and Africa are expected to experience the fastest growth during the forecast period, owing to rising obesity and diabetes rates, improved healthcare infrastructure, expanded access to essential medicines, and increased investments in chronic disease prevention and treatment programs.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global biguanides market is characterized by moderate consolidation, bringing together a diverse mix of multinational pharmaceutical companies and generic drug manufacturers that compete primarily on the basis of product availability, competitive pricing, formulation innovation, and distribution reach.

Given that metformin is a well-established and mature therapy, competitive dynamics are largely shaped by the development and supply of high-quality generic formulations, extended-release products, and fixed-dose combination therapies specifically designed to enhance patient adherence and support more effective glycemic control.

Leading players continue to strengthen their positions in the diabetes space through strategic product approvals, collaborative partnerships, and focused efforts to broaden access across key healthcare markets worldwide.

Prominent multinational pharmaceutical companies, including Merck & Co., Inc., AstraZeneca plc, and Boehringer Ingelheim International GmbH, maintain an active presence in the market through a range of metformin-containing combination products, while generic manufacturers continue to play an indispensable role in ensuring the widespread availability of affordable biguanide therapies on a global scale.

As the global demand for cost-effective and accessible diabetes management solutions continues to intensify, competitive activity is expected to remain firmly centered on improving product accessibility, advancing formulation technologies, securing regulatory approvals, and capitalizing on expansion opportunities within high-growth emerging healthcare markets.

Top Key Players

- Pfizer Inc.

- Sanofi (Sanofi‑Aventis LLC)

- Merck & Co., Inc.

- Novartis AG

- AstraZeneca plc

- GlaxoSmithKline plc (GSK)

- Takeda Pharmaceutical Company Limited

- Novo Nordisk A/S

- Boehringer Ingelheim International GmbH

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc. (incl. legacy Mylan)

- Aurobindo Pharma Ltd.

- Cipla Ltd.

- Reddy’s Laboratories Ltd.

- Lupin Limited

- Others

Key Developments

- In March 2025, DongKoo Bio & Pharma received approval in South Korea for Sitaflozinmet, a metformin-based triple-combination therapy combining dapagliflozin and sitagliptin, highlighting growing demand for advanced diabetes treatment combinations.

- In January 2025, Zydus Lifesciences expanded access to its metformin-based therapies after Zituvimet and Zituvimet XR were added to the CVS Caremark formulary in the U.S., strengthening its presence in the diabetes treatment market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 5.4 Billion |

| Forecast Revenue (2035) | US$ 7.3 Billion |

| CAGR (2026-2035) | 3.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Dosage Form (Immediate-release Tablets, Extended-release Tablets, Fixed-dose Combinations (FDCs), and Oral Solutions/Others), By Type (Metformin and Other Biguanides), By Application (Type 2 Diabetes, PCOS/Endocrine & Metabolic Off-label, Weight Management, and Emerging R&D and Other), By Distribution Channel (Retail Pharmacies, Hospital/Institutional, Online/Mail-order, and Other Care Settings). |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., Sanofi (Sanofi-Aventis LLC), Merck & Co., Inc., Novartis AG, AstraZeneca plc, GlaxoSmithKline plc (GSK), Takeda Pharmaceutical Company Limited, Novo Nordisk A/S, Boehringer Ingelheim International GmbH, Teva Pharmaceutical Industries Ltd., Viatris Inc. (including legacy Mylan), Aurobindo Pharma Ltd., Cipla Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, and Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |