Bearings Market By Product Type (Roller bearing, Ball bearing, Plain bearing), By Machine type (ICE Vehicles, Electric vehicles, Industrial machinery, Aerospace machinery), By Distribution channel (Online, Offline), By Application, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

- Published date: Feb 2024

- Report ID: 17634

- Number of Pages: 289

- Format:

- keyboard_arrow_up

Quick Navigation

Report Overview

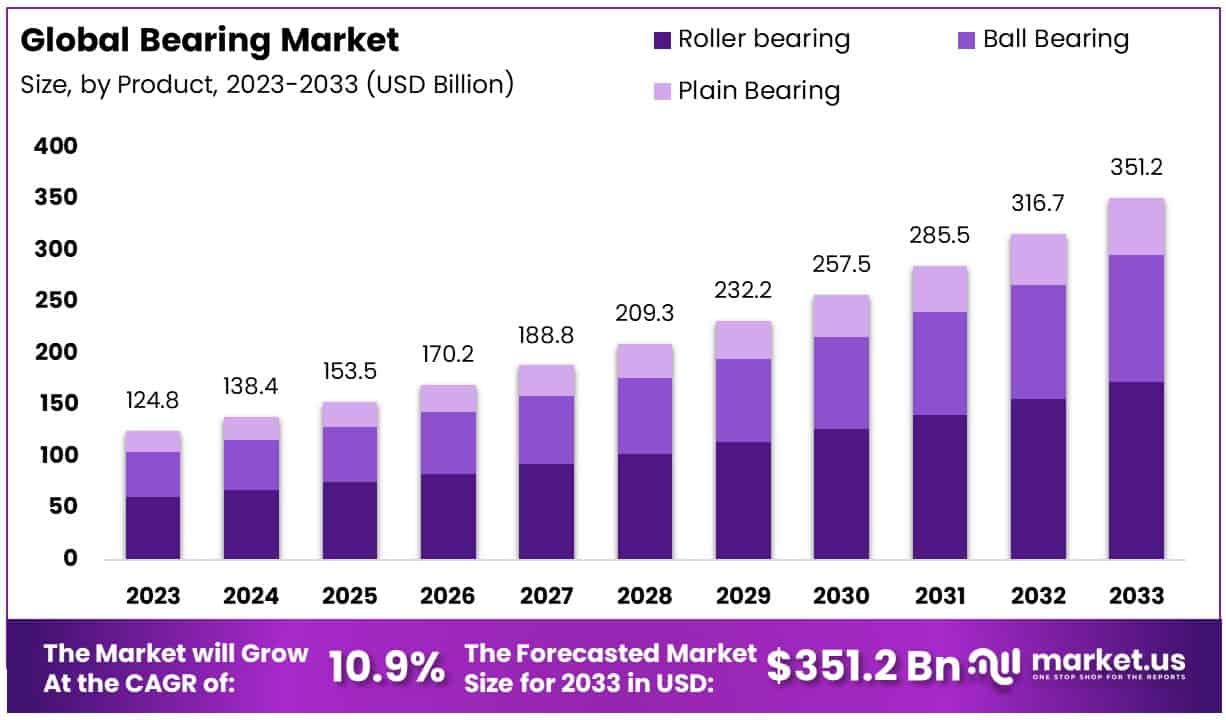

The Global Bearings Market size is expected to be worth around USD 351.2 Billion by 2033, from USD 124.8 Billion in 2023, growing at a CAGR of 10.90% during the forecast period from 2024 to 2033.

The Bearings Market represents a crucial segment within the mechanical component industry, essential for reducing friction between moving parts in machinery. This market encompasses a broad range of product types, including ball bearings, roller bearings, and plain bearings, tailored for diverse applications across automotive, aerospace, industrial, and consumer goods sectors. Its growth is driven by the demand for enhanced efficiency, reliability, and lifespan of machinery and vehicles.

Within the dynamic landscape of the Bearings Market, robust growth is anticipated, fueled by increasing demands across pivotal sectors such as automotive, aerospace, and industrial machinery. The strategic integration of advanced materials alongside precision engineering emerges as a cornerstone in propelling the market forward, significantly enhancing the bearing’s performance and longevity.

Key Takeaways

- Market Value and Growth Projection: The Bearings Market is projected to reach approximately USD 351.2 Billion by 2033, showing a robust CAGR of 10.90% during the forecast period from 2024 to 2033.

- Product Type Analysis: Roller Bearings held the dominant market position in 2023, with over a 49.2% share, renowned for their ability to handle heavy loads and facilitate high-speed operations.

- Machine Type Analysis: Industrial Machinery held a dominant market position, capturing over 60.1% share in 2023. They are indispensable for operational efficiency and reliability in manufacturing, processing, and other industrial operations.

- Distribution Channel Type Analysis: Online Distribution Channel dominated the market in 2023, with over 72.4% share, reflecting the digital transformation in supply chain and procurement processes.

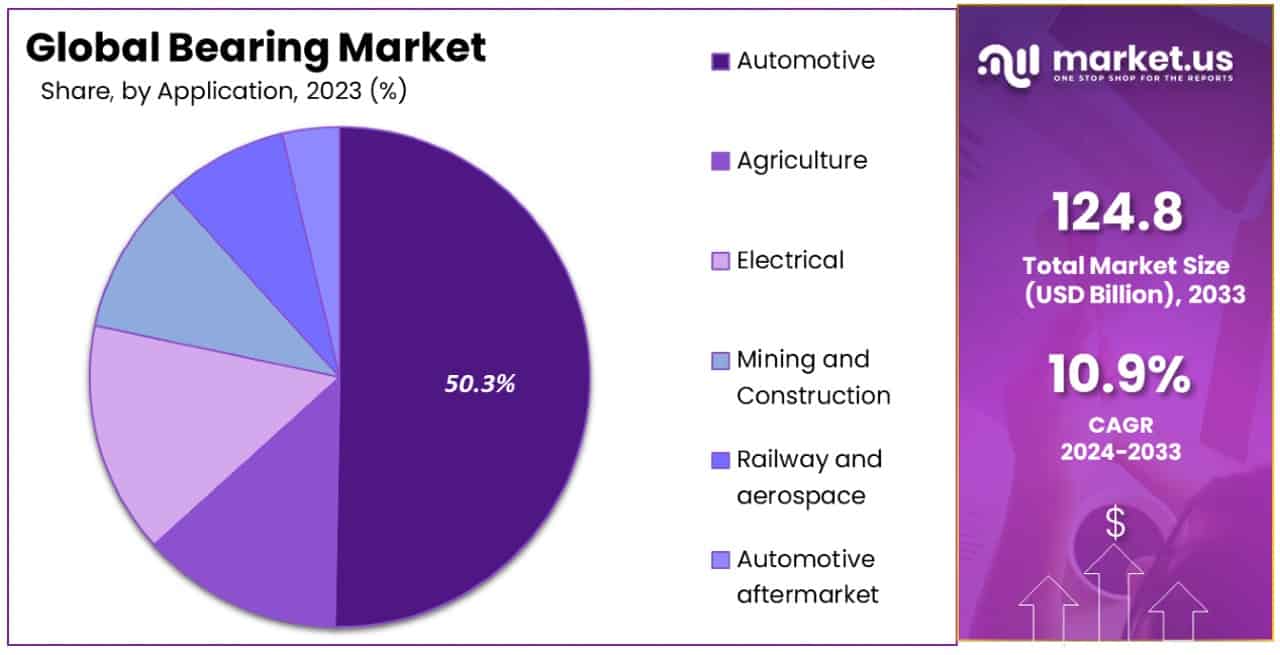

- Application Type Analysis: Automotive held the dominant market position, with over 50.3% share in 2023, emphasizing the critical role bearings play in ensuring the smooth operation of vehicles.

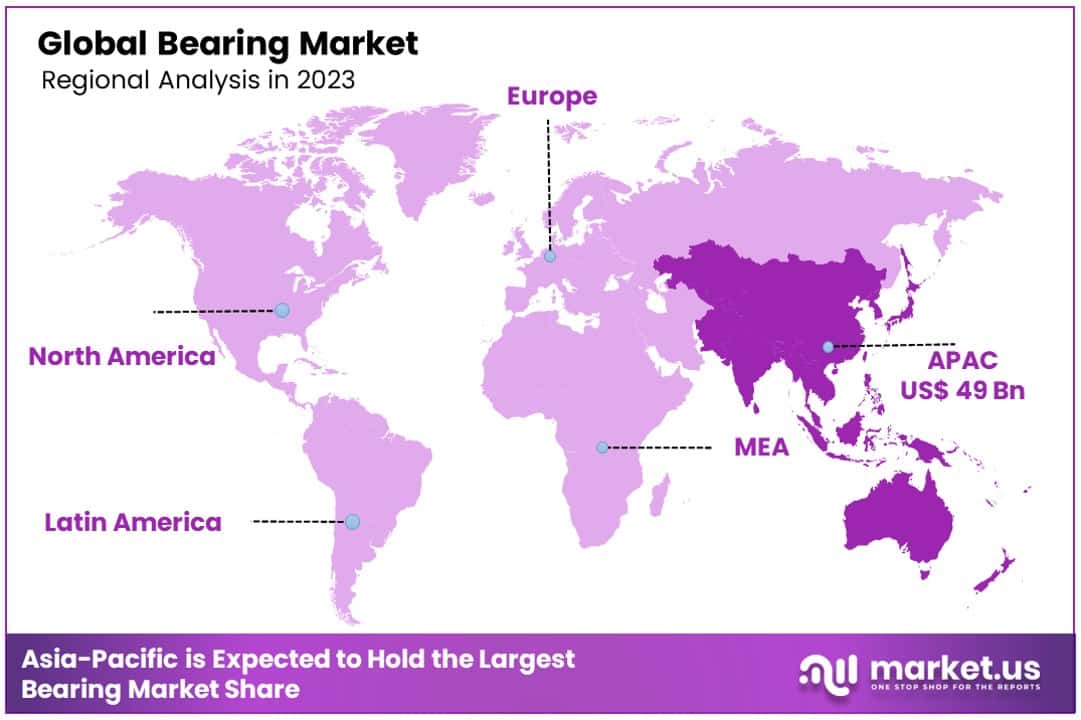

- Regional Analysis: Asia-Pacific dominates the global market with a substantial 39.3% share, driven by robust manufacturing activities, especially in China, Japan, and India.

Additionally, the emergence of smart bearings, embedded with sensors for the real-time monitoring of operational statuses, heralds a shift towards predictive maintenance strategies. This shift is critically aligned with the principles of Industry 4.0, emphasizing the paramount importance of operational efficiency and reliability.

Particularly, the automotive industry stands as a primary driver of market growth, where the advent of electric vehicles (EVs) introduces both novel opportunities and challenges for bearing manufacturers. The transition towards EVs necessitates bearings that are capable of enduring high speeds and elevated temperatures, thereby highlighting the imperative for continued research and development investments.

Concurrently, the surge in demand for renewable energy sources catalyzes growth within the wind turbine sector, emphasizing the essential role of specialized bearings in augmenting energy efficiency and extending turbine lifespan.

A notable milestone has been achieved, with over a million wind turbine bearings manufactured and delivered in compliance with the Wind Power Standard, which enforces the highest product and process quality standards. Established for over a decade, this standard addresses the increasing reliability demands placed upon wind turbines and their components, showcasing the industry’s dedication to excellence and sustainable practices.

Nevertheless, the Bearings Market encounters challenges, such as the fluctuation in raw material costs and the enforcement of rigorous environmental regulations. These obstacles mandate a commitment to sustainable manufacturing practices. Firms adept at navigating these complexities, investing in technological advancements, and adhering to sustainability trends are poised to secure leadership positions in the market.

This analysis underscores the strategic imperatives for stakeholders within the Bearings Market, emphasizing innovation, quality, and sustainability as key drivers of competitive advantage and market leadership.

Driving Factors

Increasing Demand for Precision Bearings to Drive Market Development

The Bearings Market is experiencing a significant upswing, largely fueled by the escalating demand for precision bearings. These specialized bearings are essential for applications requiring high accuracy and reliability, such as in the aerospace, automotive, and manufacturing sectors. Precision bearings enhance the performance and efficiency of machinery by minimizing friction and wear, leading to extended equipment life and reduced maintenance costs.

The demand for precision in these critical applications cannot be overstated, as even the slightest deviation can lead to significant operational disruptions. This heightened demand reflects the broader industrial shift towards automation and precision engineering, emphasizing the critical role of precision bearings in facilitating technological advancement and operational excellence.

Rising Energy Production and Distribution Activities Worldwide

The global increase in energy production and distribution activities serves as a catalyst for the Bearings Market’s growth. With the world’s energy needs expanding, the deployment of bearings in energy infrastructure—from wind turbines to traditional power plants—has become more prevalent.

As countries continue to invest in both renewable and conventional energy sources to meet growing demand, the need for high-quality bearings essential for the construction and maintenance of these facilities is expected to surge, driving further market expansion.

Expansion of Mining and Construction Activities Worldwide

The global expansion of mining and construction activities represents another pivotal growth driver for the Bearings Market. As these sectors experience resurgence and growth, the demand for heavy machinery and equipment, which relies extensively on bearings, escalates. Bearings play a vital role in the operational efficiency and longevity of construction and mining machinery, with their quality and performance directly impacting project timelines and costs.

This increased activity is estimated to push sales significantly, as the development of infrastructure, extraction of minerals, and construction of buildings and roads in emerging economies and developed nations alike require robust machinery equipped with durable bearings. The synergistic effect of this expansion, coupled with the push for energy production and the demand for precision bearings, creates a comprehensive landscape of growth opportunities for the Bearings Market.

Restraining Factors

High Price of Raw Materials

A significant restraint facing the Bearings Market is the high price of raw materials, which directly impacts the cost of production for bearings manufacturers. Materials such as steel, aluminum, and titanium, essential for manufacturing various types of bearings, have experienced volatility in prices due to factors like global demand fluctuations, trade policies, and geopolitical tensions.

This volatility not only increases operational costs for manufacturers but also reduces profit margins, potentially leading to higher prices for end-users. In a market where cost efficiency and competitive pricing are key to securing contracts and maintaining market share, the high cost of raw materials poses a substantial challenge.

Limited Raw Material Supply and Dependency

Another restraint is the limited supply and dependency on specific raw materials crucial for bearing production. The Bearings Market relies heavily on the availability of high-quality raw materials, which are concentrated in specific geographic regions.

This dependency exposes manufacturers to risks associated with supply chain disruptions, such as natural disasters, labor strikes, or political instability in these regions. Additionally, the growing demand for these materials in other industries competes for the same resources, exacerbating the issue of supply and leading to increased prices.

By Product Type Analysis

In 2023, Roller Bearing held a dominant market position in the Product type segment of the Bearings Market, capturing more than a 49.2% share. This substantial market share reflects the critical role roller bearings play in a myriad of industrial applications, emphasizing their efficiency in handling heavy loads and facilitating high-speed operations.

Roller bearings, distinguished by their design which involves cylindrical rollers to distribute the load over a larger area, are integral to the operational efficiency and durability of machinery across sectors such as automotive, industrial machinery, and heavy equipment.

Ball Bearings emerged as the second prominent segment, valued for their versatility and broad applicability across diverse industries, including automotive, aerospace, and electronics. These bearings are adept at managing both radial and thrust loads, making them indispensable for a multitude of applications. The design and engineering of ball bearings focus on minimizing friction and supporting smooth operation of machinery, thereby contributing significantly to the Bearings Market’s growth.

Plain Bearings, although capturing a smaller portion of the market compared to roller and ball bearings, play a vital role in applications that demand low maintenance and where sliding motion is prevalent. They are particularly favored in scenarios that involve high-load but low-speed operations, finding relevance in construction, mining, agriculture, and several other sectors.

By Machine Type Analysis

In 2023, Industrial Machinery held a dominant market position in the Machine type segment of the Bearings Market, capturing more than a 60.1% share. This commanding presence underscores the indispensable role of bearings in the industrial sector, where they are crucial for the operational efficiency and reliability of a wide array of machinery and equipment.

Bearings in industrial applications are pivotal in minimizing friction and wear, thereby enhancing productivity and extending the service life of machinery used in manufacturing, processing, and other industrial operations.

ICE (Internal Combustion Engine) Vehicles and Electric Vehicles represent significant segments within the Bearings Market as well, reflecting the automotive industry’s extensive demand for bearings. Bearings in ICE vehicles are critical for the smooth operation of engines, transmissions, and wheel hubs, among other components. As the automotive industry gradually shifts towards electric mobility, the demand for bearings in Electric Vehicles has seen a noticeable uptick, driven by the need for high-performance bearings in electric motors, powertrains, and other EV-specific applications.

Aerospace Machinery, though a smaller segment compared to Industrial Machinery and automotive applications, demands highly specialized bearings that can withstand extreme conditions of temperature, pressure, and loading. Bearings used in aerospace applications are designed for high precision, reliability, and durability, catering to the unique requirements of aircraft engines, landing gear, and control systems.

By Distribution Channel Type

In 2023, Online distribution channels held a dominant market position in the Distribution channel type segment of the Bearings Market, capturing more than a 72.4% share. This overwhelming preference for online channels underscores the digital transformation within the supply chain and procurement processes across industries. The rise of e-commerce platforms and digital marketplaces has significantly facilitated the accessibility, comparison, and purchasing of bearings, offering a broad spectrum of products ranging from high-precision bearings for industrial machinery to automotive and aerospace applications.

The convenience of online shopping, coupled with the ability to access detailed product specifications, customer reviews, and competitive pricing, has propelled the shift towards digital procurement.

Offline distribution channels, while still relevant, have seen a reduced market share in the face of the burgeoning online segment. Traditional brick-and-mortar stores, along with direct sales from manufacturers, continue to serve a segment of customers who prefer in-person transactions or have specific needs that benefit from direct interaction with sales personnel. However, the trend indicates a growing preference for the convenience, efficiency, and broader access provided by online channels.

Application Type Analysis

In 2023, Automotive held a dominant market position in the Application type segment of the Bearings Market, capturing more than a 50.3% share. This substantial market share emphasizes the critical role bearings play in the automotive industry, where they are integral to the operation of virtually every moving part.

From engines and transmissions to wheel hubs and steering systems, bearings ensure the smooth, efficient, and safe operation of vehicles. The demand in this segment is driven by both the production of new vehicles and the need for replacement bearings in vehicle maintenance and repair, underscoring the automotive sector’s vast and continuous need for high-quality bearings.

The Agriculture sector highlighted the need for bearings capable of withstanding extreme conditions to ensure the efficiency and longevity of farming machinery. Concurrently, the Electrical segment experienced a surge in demand for electrically insulated bearings, driven by the global shift towards electrification and renewable energy sources.

In the realms of Mining and Construction, the demand for durable bearings capable of enduring heavy loads and harsh environmental conditions was critical for the productivity of equipment used in these industries.

Similarly, Railway and Aerospace applications required bearings that adhered to stringent standards of precision, reliability, and durability, catering to the high-performance expectations in these safety-critical sectors.

The Automotive Aftermarket segment saw growth, fueled by an increasing need for maintenance and repair services, emphasizing the importance of bearings in vehicle performance and longevity.

Key Market Segments

By Products

- Roller bearing

- Ball bearing

- Plain bearing

By Machine type

- ICE Vehicles

- Electric vehicles

- Industrial machinery

- Aerospace machinery

By Distribution channel

- Online

- Offline

By Application

- Automotive

- Agriculture

- Electrical

- Mining and Construction

- Railway and aerospace

- Automotive aftermarket

Growth Opportunities

Aerospace Investment Sparks Bearings Demand

The global Bearings Market in 2023 is positioned to capitalize on unprecedented opportunities arising from significant investments in aerospace and aviation technologies.

As governments and private entities pour resources into defense, space exploration, and the development of more efficient commercial aircraft, the demand for specialized bearings that ensure the reliability and efficiency of these high-stakes applications is expected to surge. This sector’s growth necessitates innovation in bearing design and manufacturing, highlighting the importance of precision, performance, and quality in aerospace applications.

Technological Advancements Propel Market Forward and Unveil Growth Opportunities

The landscape of technological advancements presents another avenue for growth in the Bearings Market. The integration of Industry 4.0 technologies, such as the Internet of Things (IoT) and artificial intelligence (AI), into bearing products introduces smart bearings capable of real-time performance monitoring and predictive maintenance. This technological leap not only enhances machinery efficiency but also opens new markets for bearings, emphasizing the importance of continuous innovation and adaptation.

Trending Factors

- Adoption of Smart Technologies: The Bearings Market is witnessing a significant shift towards the integration of Industry 4.0 technologies. Smart bearings, equipped with IoT and AI capabilities for real-time monitoring and predictive maintenance, are revolutionizing machinery efficiency and extending operational lifespans.

- Sustainability and Environmental Responsibility: Manufacturers are increasingly focusing on producing energy-efficient bearings and employing sustainable materials and processes. This trend is driven by regulatory demands and consumer expectations for eco-friendly products, encouraging innovations in green manufacturing techniques.

- Material Science Innovations: Advancements in materials science are enabling the creation of bearings that are lighter, more durable, and capable of operating in extreme conditions. This innovation is crucial for industries such as aerospace, where performance and reliability are paramount.

- Global Supply Chain Resilience: In response to recent disruptions, there’s an increasing emphasis on building more resilient global supply chains. The Bearings Market is adapting through diversified sourcing, localized manufacturing, and digital supply chain solutions to ensure stability and responsiveness.

Regional Analysis

In the global landscape, the Bearings Market exhibits significant regional disparities, shaped by industrial trends, technological adoption, and economic factors. Dominating the market with a substantial 39.3% share, Asia-Pacific stands out as the forefront of growth, driven by robust manufacturing activities, particularly in China, Japan, and India. This region benefits from extensive industrialization, a booming automotive sector, and increasing investments in infrastructure and renewable energy projects, which collectively fuel the demand for bearings.

North America, with its advanced manufacturing base and technological leadership, especially in aerospace and automotive industries, remains a key player in the Bearings Market. The region’s focus on innovation and the integration of smart technologies into manufacturing processes are pivotal in driving the demand for high-performance and precision bearings. The United States, as the largest market in this region, emphasizes renewable energy and electric vehicle production, further bolstering the market’s expansion.

Europe’s Bearings Market is characterized by its stringent environmental regulations and high standards for product quality and sustainability. The region’s automotive and industrial machinery sectors, particularly in Germany, Italy, and France, are significant consumers of bearings. Europe’s push towards electrification and sustainable manufacturing practices presents new opportunities for bearing manufacturers to innovate and adapt to evolving market needs.

The Middle East & Africa, though a smaller market, is witnessing growth in construction and mining activities, driving the demand for heavy-duty bearings. Investments in infrastructure development and renewable energy, especially in Gulf Cooperation Council (GCC) countries, are expected to propel the market forward.

Latin America, with its growing automotive production in countries such as Brazil and Mexico, presents opportunities for the Bearings Market. The region’s focus on improving industrial machinery and infrastructure development contributes to the demand for various types of bearings.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2023, the global Bearings Market continues to be highly competitive, with key players such as Brammer Plc, HKT Bearing Ltd, JTEKT Corporation, NBI Bearing Europe, NSK Global, NTN Corporation, RBC Bearings Inc, Rexnord Corporation, RHP Bearing, Schaeffler Group, SKF Corporation, and Harbin Bearing Manufacturing Co., Ltd., leading the charge. These companies are at the forefront of innovation, leveraging advanced manufacturing techniques, and engaging in strategic partnerships to expand their market footprint and product offerings.

SKF Corporation and Schaeffler Group, in particular, stand out for their significant contributions to technological advancements within the industry. Their focus on R&D has led to the development of smart bearing solutions integrated with IoT technologies, catering to the growing demand for predictive maintenance and operational efficiency. Similarly, JTEKT Corporation’s expertise in the automotive sector, especially in producing bearings for electric vehicles, positions it well amidst the global shift towards electrification.

NTN Corporation and NSK Global are also pivotal, with their expansive product portfolios covering various applications, from industrial machinery to aerospace. Their global presence and commitment to quality have ensured strong customer loyalty and a competitive edge in the market.

Emerging players like Harbin Bearing Manufacturing Co., Ltd., are gaining recognition for their cost-effective solutions, particularly in developing markets, challenging established players by offering comparable quality at lower prices.

In terms of strategic moves, RBC Bearings Inc and Rexnord Corporation have focused on acquisitions to broaden their product lines and enter new markets, demonstrating the industry’s dynamic nature and the continuous pursuit of growth opportunities.

Market Key Players

- Brammer Plc

- HKT Bearing ltd

- JTEKT Corporation

- NBI Bearing Europe

- NSK Global

- NTN Corporation

- RBC Bearing Inc

- Rexnord Corporation

- RHP Bearing

- Schaeffler Group

- SKF Corporation

- Harbin Bearing Manufacturing Co, ltd

Recent Developments

- JUL 23: NBC Bearings plans to introduce over 500 new bearing sizes to the market.

- JUL 23: Gemini completed an investment in Alpine Bearing Company, a value-added distributor of high-precision ball bearings.

- OCT 23: A large Chinese company manufacturing roller bearings and components is looking for two distributors in USA and Europe to support its export markets growth. The ideal targets are strong in serving cylindrical, taper and spherical roller bearings to heavy industries like steel mills, mining, paper mills and oil & gas industries.

Report Scope

Report Features Description Market Value (2023) USD 124.8 Billion Forecast Revenue (2033) USD 351.2 Billion CAGR (2024-2033) 10.90% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Roller bearing, Ball bearing, Plain bearing), By Machine type (ICE Vehicles, Electric vehicles, Industrial machinery, Aerospace machinery), By Distribution channel (Online, Offline), By Application Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Brammer Plc, HKT Bearing ltd, JTEKT Corporation, NBI Bearing Europe, NSK Global, NTN Corporation, RBC Bearing Inc, Rexnord Corporation, RHP Bearing, Schaeffler Group, SKF Corporation, Harbin Bearing Manufacturing Co, ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) Frequently Asked Questions (FAQ)

What is the projected size of the Bearings Market?The Bearings Market is expected to reach approximately USD 351.2 Billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 10.90% during the forecast period from 2024 to 2033.

What region dominates the global Bearings Market?Asia-Pacific dominates the global market with a substantial 39.3% share. This dominance is driven by robust manufacturing activities, particularly in countries such as China, Japan, and India.

What growth opportunities are highlighted in the report?Investments in aerospace and aviation technologies create demand for specialized bearings, emphasizing reliability and efficiency in critical applications.

Which segments are covered in the report?The report segments the market by product type (roller bearing, ball bearing, plain bearing), machine type (ICE vehicles, electric vehicles, industrial machinery, aerospace machinery), distribution channel (online, offline), and application. This comprehensive segmentation provides a detailed understanding of various aspects of the bearing market and its diverse applications across industries.

- Brammer Plc

- HKT Bearing ltd

- JTEKT Corporation

- NBI Bearing Europe

- NSK Global

- NTN Corporation

- RBC Bearing Inc

- Rexnord Corporation

- RHP Bearing

- Schaeffler Group

- SKF Corporation

- Harbin Bearing Manufacturing Co, ltd

- Nestlé S.A Company Profile

- settingsSettings

Our Clients

- 17634

- Feb 2024

| Single User $4,599 $3,499 USD / per unit save 24% | Multi User $5,999 $4,299 USD / per unit save 28% | Corporate User $7,299 $4,999 USD / per unit save 32% | |

|---|---|---|---|

| e-Access | |||

| Report Library Access | |||

| Data Set (Excel) | |||

| Company Profile Library Access | |||

| Interactive Dashboard | |||

| Free Custumization | No | up to 10 hrs work | up to 30 hrs work |

| Accessibility | 1 User | 2-5 User | Unlimited |

| Analyst Support | up to 20 hrs | up to 40 hrs | up to 50 hrs |

| Benefit | Up to 20% off on next purchase | Up to 25% off on next purchase | Up to 30% off on next purchase |

| Buy Now ($ 3,499) | Buy Now ($ 4,299) | Buy Now ($ 4,999) |