Global Bakery Contract Manufacturing Market By Product Type (Bread And Rolls, Cookies And Biscuits, Cakes And Pastries, Pizza Crusts, Others), By Service Type ( Manufacturing, Custom Formulation, Packaging And Labelling, Full-Service), By End User (Food And Beverage Companies, Retail Chains And Supermarkets, Catering Services, Quick-Service Restaurants (QSRs)), By Distribution Channel (Offline Sales, Online Sales)

- Published date: Mar 2026

- Report ID: 181685

- Number of Pages: 247

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

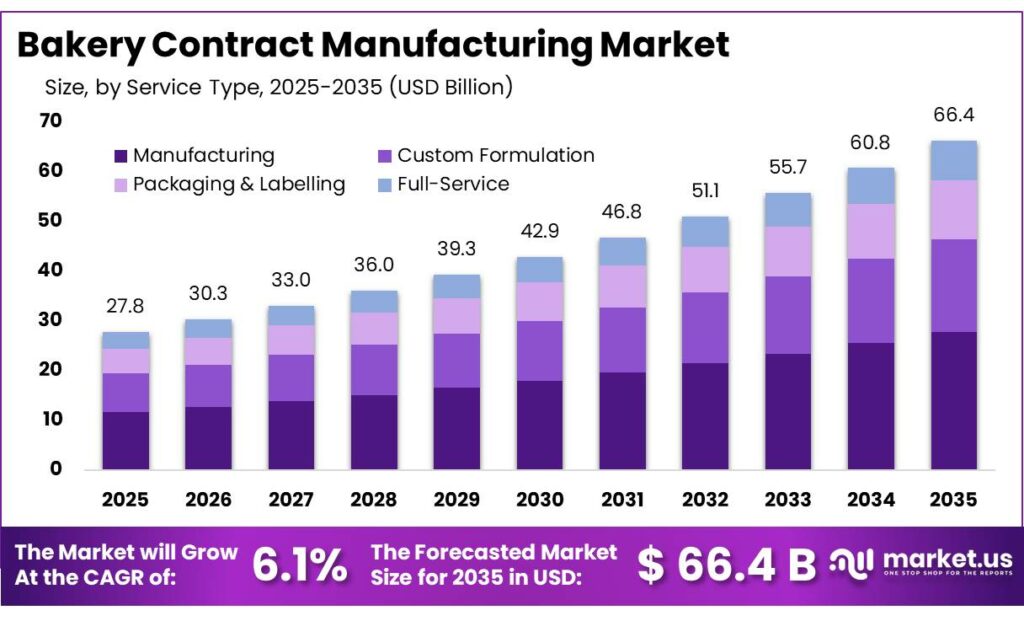

The Global Bakery Contract Manufacturing Market size is expected to be worth around USD 66.4 Billion by 2035, from USD 27.8 Billion in 2025, growing at a CAGR of 9.1% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 34.1% share, holding USD 9.4 billion revenue.

Bakery contract manufacturing has become an increasingly strategic operating model for branded food companies that want scale without carrying the full burden of fixed plant investment, labor intensity, and compliance complexity. The industrial backdrop is substantial: the American Bakers Association states that the U.S. baking industry employs almost 800,000 people, generates more than $42 billion in direct wages, and creates more than $186 billion in overall economic impact.

In Europe, FoodDrinkEurope reports that the wider food and drink industry generated €1,196 billion in turnover, €249 billion in value added, and €45 billion in investment in 2021, underscoring the manufacturing depth from which outsourced bakery production can be sourced.

FoodDrinkEurope also reports 304,120 food and drink companies in the EU and notes that about 16% of manufacturing employees work in this sector, indicating a broad production ecosystem that supports flexible capacity allocation. On the trade side, USDA data show U.S. baked goods exports at $4.27 billion and 1.44 million metric tons in 2025, confirming that bakery products remain globally traded and operationally scalable. This environment favors specialist manufacturers able to deliver consistent formulations, packaging formats, and export-ready documentation.

In the European Union, food and drink generated €1,523 billion in turnover in 2023, employed 4.8 million people and included 309,000 companies, while bakery and farinaceous products alone represented 19% of total food-and-drink turnover, 17% of value added and 32% of sector employment. In Canada, bakeries and tortilla manufacturing reported C$17.7 billion in shipments, C$9.0 billion in value added and C$2.4 billion in net revenue in 2023. This indicates that bakery contract manufacturing is operating in a large, labor-intensive, repeat-purchase category with strong industrial relevance across developed food markets.

The main driving factors are input availability, price management, labor economics, portfolio diversification and retailer demand for efficient private-label supply. On the agricultural side, USDA forecast global wheat production at a record 837.8 million metric tons in 2025/26, which supports a deeper raw-material base for industrial bakers and co-manufacturers.

The U.S. Bureau of Labor Statistics noted that the Producer Price Index for bakery products increased in 35 of 36 months from January 2021 through the end of 2023, showing why brand owners increasingly seek outsourced manufacturing partners that can optimize procurement, throughput and pack formats. Scale is also visible in labor: bakeries and tortilla producers represented 14.7% of U.S. food-and-beverage manufacturing employment in 2021.

Key Takeaways

- Bakery Contract Manufacturing Market size is expected to be worth around USD 66.4 Billion by 2035, from USD 27.8 Billion in 2025, growing at a CAGR of 9.1%.

- Bread & Rolls held a dominant market position, capturing more than a 34.7% share.

- Manufacturing held a dominant market position, capturing more than a 42.3% share.

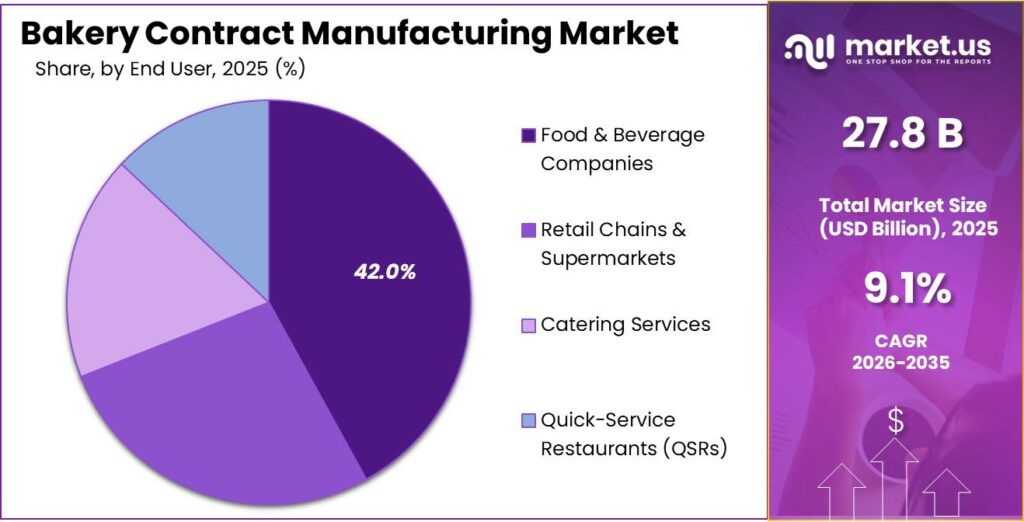

- Food & Beverage Companies held a dominant market position, capturing more than a 42.8% share.

- Offline Sales held a dominant market position, capturing more than a 82.5% share.

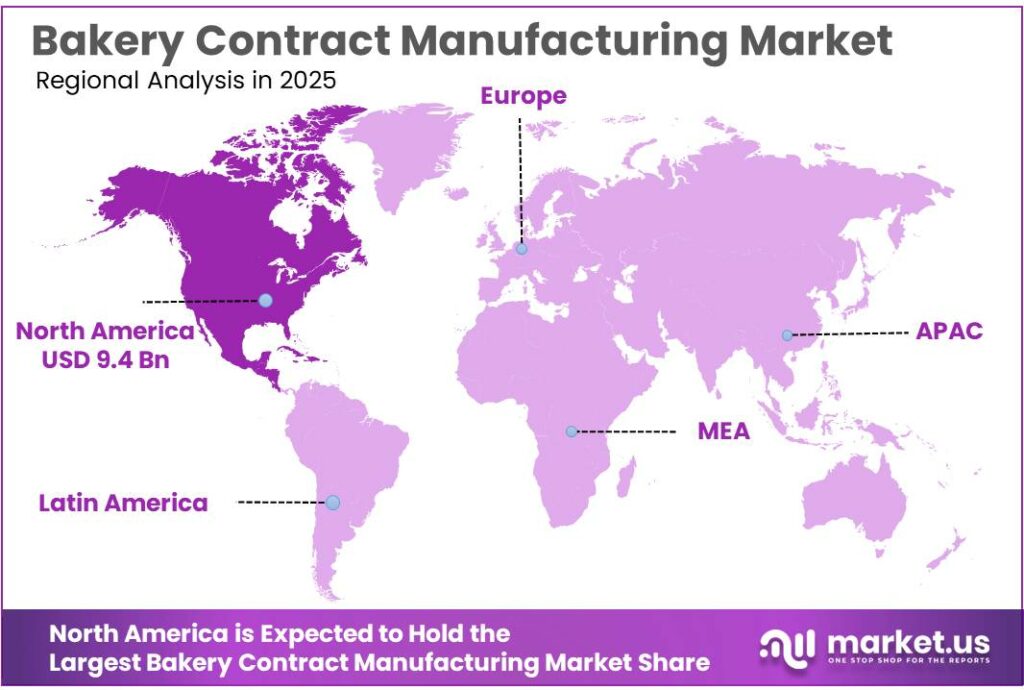

- North America held a dominant position in the bakery contract manufacturing market, accounting for 34.1% share with a market value of USD 9.4 billion.

By Product Type Analysis

Bread & Rolls dominate with 34.7% due to everyday consumption and large-scale production demand

In 2025, Bread & Rolls held a dominant market position, capturing more than a 34.7% share. This segment continues to lead because bread is a daily staple across multiple regions, making it a high-volume and consistent demand category for contract manufacturers. Large retail chains and foodservice providers rely heavily on outsourced production to maintain steady supply, especially for sliced bread, buns, and dinner rolls. In 2026, the segment remained strong as manufacturers focused on improving shelf life, texture consistency, and cost efficiency through automation and standardized recipes. The growing popularity of packaged sandwiches and quick-service meals has also supported demand for burger buns and sandwich rolls.

By Service Type Analysis

Manufacturing dominates with 42.3% driven by high-volume outsourcing and efficiency needs

In 2025, Manufacturing held a dominant market position, capturing more than a 42.3% share. This segment leads because many bakery brands prefer to outsource production instead of investing in their own large facilities. Contract manufacturers provide ready infrastructure, skilled labor, and standardized processes, which helps brands scale quickly without heavy capital spending. In 2026, the demand for manufacturing services remained strong as companies focused more on cost control and faster product turnaround. Large-scale production of bread, cakes, and frozen bakery items is easier to manage through specialized partners who can handle bulk orders with consistent quality.

By End User Analysis

Food & Beverage Companies dominate with 42.8% as outsourcing supports scale and faster product launches

In 2025, Food & Beverage Companies held a dominant market position, capturing more than a 42.8% share. This segment leads because large food brands depend on contract manufacturers to meet growing demand without expanding their own production facilities. Outsourcing allows these companies to focus on branding, distribution, and new product development while leaving production to experienced partners. In 2026, this trend continued as companies increased their use of contract manufacturing to handle seasonal demand spikes and manage costs more effectively.

By Distribution Channel Analysis

Offline Sales dominate with 82.5% as traditional retail and bulk buying remain strong

In 2025, Offline Sales held a dominant market position, capturing more than a 82.5% share. This segment continues to lead because bakery products are widely sold through supermarkets, convenience stores, and foodservice outlets where consumers prefer to buy fresh and packaged items directly. Physical stores offer better product visibility, immediate availability, and trust in quality, which keeps demand strong in offline channels. In 2026, the dominance of offline sales remained steady as bulk purchasing by hotels, restaurants, and catering businesses continued to rely on direct supply from contract manufacturers.

Key Market Segments

By Product Type

- Bread & Rolls

- Cookies & Biscuits

- Cakes & Pastries

- Pizza Crusts

- Others

By Service Type

- Manufacturing

- Custom Formulation

- Packaging & Labelling

- Full-Service

By End User

- Food & Beverage Companies

- Retail Chains & Supermarkets

- Catering Services

- Quick-Service Restaurants (QSRs)

By Distribution Channel

- Offline Sales

- Online Sales

Emerging Trends

Automation is becoming the most important trend in bakery contract manufacturing

A clear latest trend in bakery contract manufacturing is the move toward automation-led production. In 2025, this became more visible as bakery producers looked for faster output, better consistency, and lower waste across large-volume product lines. The wider food industry already shows the scale behind this shift. In the European Union, the food and drink industry generated €1,523 billion in turnover in 2023, employed 4.8 million people, and accounted for around 16% of manufacturing employment, which highlights how much room there is for productivity gains through automated systems.

Bakery is especially important inside that base, with bakery and farinaceous products representing 19% of total food and drink turnover in the EU. In 2025, IBIE’s industry awards and innovation showcase put strong focus on automation, robotics, and production efficiency, showing where investment attention is moving. For contract manufacturers, this trend matters because customers want large runs, fixed quality, and quicker turnaround without building their own plants. Automation helps deliver that in a practical way.

Digital traceability is growing alongside automation and shaping new contracts

The same trend is now expanding beyond machines into digital traceability and compliance-ready production. In 2025, the U.S. FDA proposed extending the Food Traceability Rule compliance date by 30 months, from January 20, 2026 to July 20, 2028. That move showed two things at once: traceability rules are becoming more important, and many food businesses still need more time to upgrade systems. At the same time, the European Commission allocated €132 million for 2025 to promote sustainable and high-quality agri-food products, which supports better documented, higher-standard food supply chains.

For bakery contract manufacturers, this creates a real opportunity to stand out by combining automated production with stronger batch tracking, ingredient records, and audit readiness. Buyers are no longer looking only for low-cost output. They also want proof of consistency, safety, and supply chain control. That is why the latest trend is not just more equipment on the factory floor, but smarter and more transparent production. In simple terms, the factories that can produce fast and prove every step are becoming the preferred partners in 2025 and 2026.

Drivers

Rising Global Demand for Bread and Everyday Bakery Consumption

One of the biggest driving factors for bakery contract manufacturing is the strong and consistent global demand for bread and daily bakery products. Bread is not just a snack, it is a basic food item consumed across the world every day. According to the Food and Agriculture Organization (FAO), bread is considered “an important source of dietary energy” and plays a key role in daily nutrition. At the same time, global consumption remains very high, with average bread intake ranging between 59 to 70 kg per person annually in many regions.

In 2025 and 2026, this steady demand directly supports contract manufacturing because brands need continuous large-scale production without interruption. Data also shows that more than 40 countries consume over 1 million tons of bread each year, while global bread demand exceeds 65 million tons annually. This kind of volume cannot always be handled by in-house facilities, so companies prefer outsourcing production. Contract manufacturers help maintain supply, reduce operational pressure, and ensure consistent product quality. As consumption continues to stay stable and frequent, the need for reliable production partners keeps growing, making demand a strong long-term driver for this market.

Strong Wheat Supply and Government-Backed Food Stability

Another major driving factor is the stable and growing supply of wheat, which is the main raw material for bakery products. Governments and global organizations are actively working to ensure food security and stable grain availability. According to FAO’s 2025 outlook, global wheat inventories are expected to increase by 3.6% by 2026, reaching one of the highest levels recorded. This kind of supply stability is important because it supports large-scale baking operations and reduces the risk of raw material shortages.

Wheat is also one of the most widely consumed cereals globally, with an average consumption of 65.6 kg per person per year across 173 countries. This shows how important wheat-based products like bread are in global diets. Governments and food bodies continue to support wheat production through agricultural policies and food security programs, which indirectly benefits the bakery industry.

Restraints

Raw Material Price Swings make planning harder for bakery manufacturers

One major restraining factor for bakery contract manufacturing is raw material price volatility, especially in wheat and other grain-based inputs. Bakery producers work on tight margins, so even small changes in flour or cereal prices can disturb production budgets and contract pricing. In 2025, the FAO reported that international wheat prices moved up at different points of the year because of tighter seasonal supplies, Black Sea trade uncertainty, and weather risks in key producing countries.

FAO also noted that its Cereal Price Index averaged 107.9 points in 2025, while in February 2026 the index stood at 108.6 points and world wheat prices rose 1.8% month on month. That kind of movement creates uncertainty for contract manufacturers that promise fixed production terms to brand owners. Even when supply is available, unstable input pricing affects procurement timing, recipe costs, and profit visibility. For outsourced bakery production, this becomes a real restraint because customers expect stable pricing, but raw material markets do not always cooperate.

Compliance and operating cost pressure add another layer of strain

The second part of the same restraint is the rising cost of running a compliant food manufacturing operation. Bakery contract manufacturers are not only dealing with flour, sugar, oils, and packaging costs, they are also expected to invest in traceability, documentation, and quality systems. In the United States, the FDA said in 2025 that it intended to extend the Food Traceability Rule compliance date by 30 months, moving it from January 20, 2026 to July 20, 2028, which shows how demanding implementation has been for food businesses.

At the same time, broader cost pressure has not disappeared. The U.S. Bureau of Labor Statistics reported that the consumer index for cereals and bakery products increased 2.7% over the 12 months ending in February 2026. For manufacturers, that reflects an environment where food costs remain sensitive even when output continues. This makes contract manufacturing harder because clients want lower costs, faster delivery, and full compliance at the same time.

Opportunity

Expansion of Packaged and Industrial Bakery Products Creates Strong Growth Opportunity

One of the biggest growth opportunities for bakery contract manufacturing is the rapid expansion of packaged and industrial bakery products. Consumers are increasingly shifting toward ready-to-eat and convenient food, especially bread, buns, and packaged snacks that fit into busy daily routines. According to industry data, global bread demand alone exceeds 65 million tons annually, and more than 80% of households consume bread every week, showing how large and stable this category is.

In 2025 and 2026, this shift has created a strong opportunity for contract manufacturers, as brands increasingly outsource production of packaged bakery items to meet volume demand. Governments and food bodies also support food processing and shelf-stable products as part of food security and supply chain resilience strategies. The FAO highlights that bakery products are a key source of dietary energy globally, reinforcing their importance in everyday consumption.

Growth in Wheat-Based Food Systems and Stable Supply Supports Expansion

Another strong opportunity comes from the expanding wheat-based food ecosystem, which supports continuous bakery production at scale. Wheat remains one of the most important food crops globally, consumed in over 170 countries with an average intake of 65.6 kg per person annually, showing its deep integration into daily diets. In addition, wheat-based foods contribute around 20% of global dietary energy supply, making them essential for both nutrition and food security.

From a supply perspective, FAO reported that global cereal production reached 3.1 billion tonnes by 2024, reflecting strong agricultural output and improved yields. This growing supply base supports large-scale baking operations and allows contract manufacturers to secure raw materials more efficiently. In 2025–2026, governments and international organizations continue to focus on strengthening food supply chains and grain availability, which directly benefits industrial baking.

Regional Insights

North America dominates with 34.1% share valued at USD 9.4 Bn driven by strong industrial baking base

In 2025, North America held a dominant position in the bakery contract manufacturing market, accounting for 34.1% share with a market value of USD 9.4 billion. The region’s leadership is mainly supported by its well-established industrial baking infrastructure and strong demand for packaged and convenience bakery products.

The United States plays a central role, where the baking industry alone contributes over $186 billion annually to the economy and employs nearly 800,000 workers, showing the scale and maturity of the sector. This large production base makes it easier for brands to outsource manufacturing to specialized partners who can handle high-volume orders with consistent quality.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

HACO Holding AG is a Switzerland-based food group known for private label and contract food production, including bakery-related products. The company operates multiple production units across Europe and focuses on customized food solutions for retail and foodservice clients. HACO is part of a broader food ecosystem with operations spanning sauces, beverages, and bakery mixes. While exact revenue figures are not publicly disclosed, the company operates within the European food industry valued at over €1,523 billion turnover in 2023, highlighting its presence in a large-scale manufacturing environment.

Hearthside Food Solutions LLC is one of the largest contract manufacturers in the food industry and a leading player in bakery outsourcing. The company operates over 30 production facilities and employs thousands of workers across the U.S. It generates estimated annual revenue of around $1.6 billion and has approximately 4,260 employees, highlighting its large-scale operations.

Cibus Nexum is a Europe-based contract manufacturing and food innovation company focused on connecting food production capabilities with brand requirements. The company works across bakery and processed food categories, offering formulation, sourcing, and manufacturing services. It operates within a rapidly growing outsourcing environment, where the global bakery contract manufacturing market is expected to grow from $27.58 billion in 2025 to $30.27 billion in 2026, reflecting increasing reliance on third-party production partners.

Top Key Players Outlook

- HACO Holding AG

- PacMoore Products, Inc.

- Blackfriars Bakery

- Cibus Nexum

- Hearthside Food Solutions LLC

- Perfection Foods

- Richmond Baking

- Oakhouse Bakery

- Adventure Bakery LLC

- Michel’s Bakery, Inc.

- Stephano Group Ltd.

- Tradition Fine Foods Ltd.

Recent Industry Developments

In 2025, Hearthside Food Solutions also completed a major financial restructuring, eliminating close to $2 billion in debt to stabilize operations and support long-term growth.

Report Scope

Report Features Description Market Value (2025) USD 27.8 Bn Forecast Revenue (2035) USD 66.4 Bn CAGR (2026-2035) 9.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Bread And Rolls, Cookies And Biscuits, Cakes And Pastries, Pizza Crusts, Others), By Service Type ( Manufacturing, Custom Formulation, Packaging And Labelling, Full-Service), By End User (Food And Beverage Companies, Retail Chains And Supermarkets, Catering Services, Quick-Service Restaurants (QSRs)), By Distribution Channel (Offline Sales, Online Sales) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape HACO Holding AG, PacMoore Products, Inc., Blackfriars Bakery, Cibus Nexum, Hearthside Food Solutions LLC, Perfection Foods, Richmond Baking, Oakhouse Bakery, Adventure Bakery LLC, Michel’s Bakery, Inc., Stephano Group Ltd., Tradition Fine Foods Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Bakery Contract Manufacturing MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Bakery Contract Manufacturing MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- HACO Holding AG

- PacMoore Products, Inc.

- Blackfriars Bakery

- Cibus Nexum

- Hearthside Food Solutions LLC

- Perfection Foods

- Richmond Baking

- Oakhouse Bakery

- Adventure Bakery LLC

- Michel’s Bakery, Inc.

- Stephano Group Ltd.

- Tradition Fine Foods Ltd.

Our Clients

- 181685

- Mar 2026