Quick Navigation

Report Overview

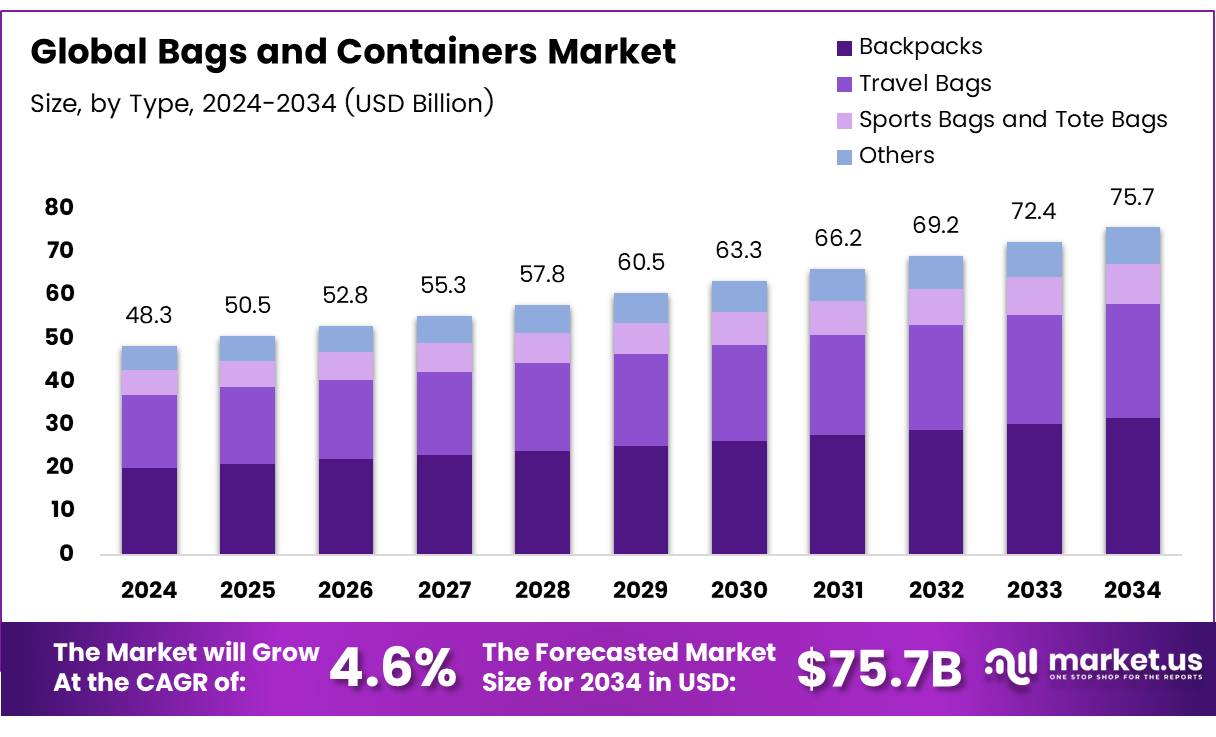

The Global Bags and Containers Market size is expected to be worth around USD 75.7 Billion by 2034, from USD 48.3 Billion in 2024, growing at a CAGR of 4.6% during the forecast period from 2025 to 2034.

The bags and containers market encompasses a wide range of products designed to meet the diverse packaging and carrying needs across various industries. From consumer retail to industrial applications, this market segment includes everything from plastic containers and reusable shopping bags to specialized cargo containers and luxury handbags.

As environmental concerns and consumer preferences evolve, there is a significant shift towards sustainable and versatile packaging solutions, further broadening the market’s scope.

The global market for bags and containers is poised for substantial growth, driven by increasing consumer demand and innovative advancements in materials technology. As the market responds to the dual pressures of consumer convenience and environmental sustainability, companies are investing in research and development to create products that are both user-friendly and eco-conscious.

According to the USDA, Brazil’s MY 2024/25 total coffee production is forecast at 66.4 million bags, slightly up by 0.2 percent from the previous season, indicating a stable demand for coffee bags that could influence material choices and design innovations in this category.

Meanwhile, Recent Study reports that the global revenue in the bags & containers segment is expected to grow by 7.6 billion USD, reaching 53.66 billion USD by 2026—a 16.51% increase, reflecting expanding market opportunities across multiple sectors.

The future growth of the bags and containers market is intrinsically linked to global economic trends, consumer behavior changes, and regulatory landscapes.

Governments worldwide are increasingly investing in recycling infrastructure and imposing regulations that encourage the use of sustainable packaging solutions. These developments not only drive innovation but also open new market segments for eco-friendly products.

Financial Express highlights that 90% of consumers in the Asia-Pacific region are willing to pay more for sustainable products, which emphasizes the potential for premium pricing in eco-conscious segments. Furthermore, Packaging News notes that 64% of respondents aim to reduce single-use packaging usage, a sentiment that can propel demand for reusable and sustainable bag options.

Key Takeaways

- The global bags and containers market is projected to grow from USD 48.3 billion in 2024 to USD 75.7 billion by 2034, at a CAGR of 4.6%.

- Backpacks lead the market by type, holding a 41.2% share in 2024, favored by diverse consumer groups.

- Offline distribution channels dominated in 2024 with a 71.3% market share.

- Plastic is the top material in the market, accounting for a 42.3% share in 2024, valued for its versatility and durability.

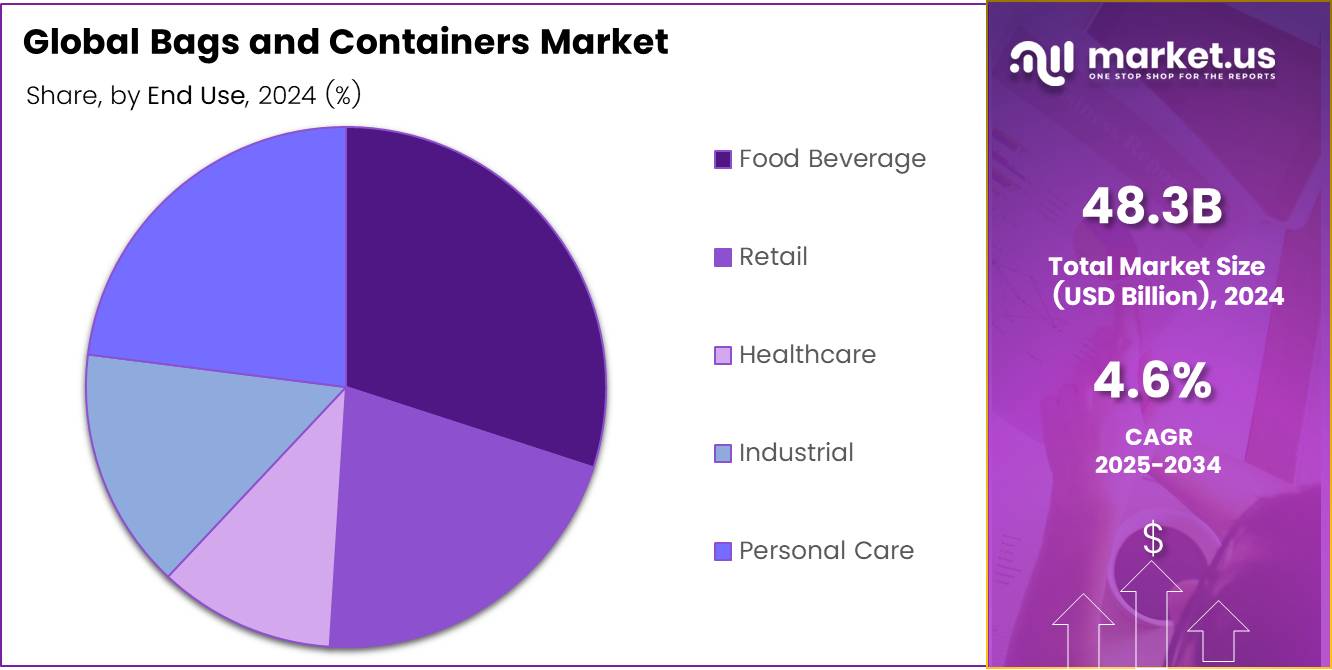

- The Food & Beverage sector leads market demand by end-use, propelled by trends in convenience foods and sustainable packaging.

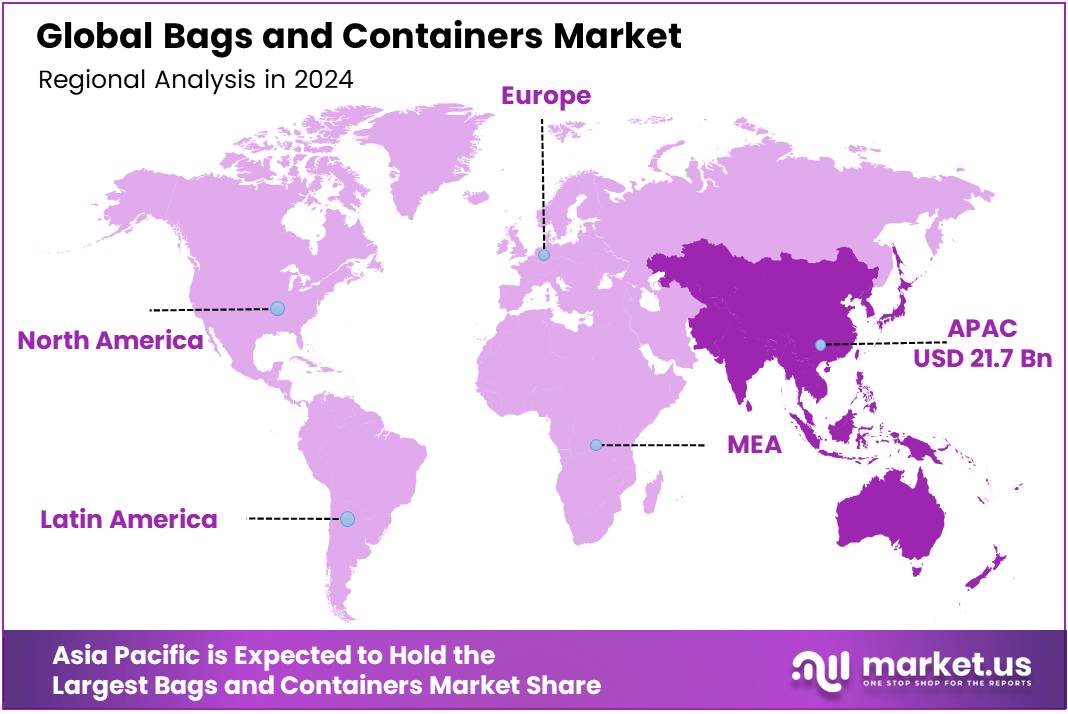

- Asia Pacific is the largest market region, holding a 45.2% share, driven by urbanization and packaging industry growth in China, India, and Japan.

Type Analysis

Backpacks Lead the Way in the Bags and Containers Market with a 41.2% Share

In 2024, the By Type Analysis of the Bags and Containers Market highlighted backpacks as a preeminent category, capturing a substantial 41.2% market share. This segment’s dominance is attributed to the versatile usage of backpacks in various consumer segments, ranging from students to working professionals. The adaptability of backpacks for different settings, such as travel, education, and daily commuting, underscores their continued popularity.

Travel bags, the second most significant category, cater to a growing segment of frequent travelers, reflecting the global expansion in tourism and business travel sectors. These bags are designed to offer durability, security, and efficiency in handling, aligning with the needs of modern travelers.

Sports bags and tote bags also represent significant portions of the market, driven by an increase in health awareness and sports participation. These bags are tailored to meet the specific needs of athletes and fitness enthusiasts, with features designed for convenience and functionality.

The Others category captures specialized bags, including luxury handbags and business cases, which appeal to niche markets looking for premium products. This segment benefits from the rising disposable incomes and the consumer’s willingness to invest in high-quality, durable items.

Overall, the varied demands of a diverse consumer base continue to drive innovation and growth within the Bags and Containers Market.

Distribution Channel Analysis

Offline Dominates Distribution in Bags and Containers Market with 71.3% Share

In 2024, the By Distribution Channel Analysis segment of the Bags and Containers market was prominently led by offline channels, accounting for a substantial 71.3% of the market share.

This significant dominance can be attributed to consumer preferences for tactile purchasing experiences, where physical verification of product quality and instant ownership are highly valued. Traditional retail outlets, including supermarkets, hypermarkets, and specialty stores, continue to be pivotal in driving sales, despite the growth of digital platforms.

Conversely, the online segment, though smaller, is rapidly gaining traction, reflecting a shift in consumer behavior towards digital channels. This segment benefits from the convenience of home shopping, a wider range of products, and often, competitive pricing.

E-commerce platforms and direct-to-consumer strategies by brands are set to reshape the landscape, promising substantial growth potential in the coming years. However, the current market configuration underscores the enduring appeal and strategic importance of offline channels in the Bags and Containers industry.

Material Type Analysis

Plastic Leads in Material Use for Bags and Containers with a 42.3% Market Share

In 2024, Plastic maintained its stronghold in the By Material Type Analysis segment of the Bags and Containers Market, securing a dominant 42.3% share. This prominence can be attributed to plastic’s versatility, affordability, and durability, which make it a preferred choice across various industries including retail, food service, and healthcare.

Moreover, advancements in recycling processes and the development of biodegradable plastics have begun to alleviate environmental concerns, further bolstering its market position.

Following plastic, paper emerged as the second most popular material, favored for its eco-friendly attributes and increasing consumer demand for sustainable products. However, its market share is significantly lower due to limitations in durability and moisture resistance.

Canvas and jute, both known for their durability and sustainable appeal, have carved niche segments within the market. These materials are particularly popular in the personal accessory and premium packaging sectors, where consumers are willing to pay a premium for environmentally friendly options.

Metal, while durable and protective, holds a smaller share due to higher costs and less flexibility in usage compared to other materials. Its use is primarily confined to specialized containers in industries requiring high levels of preservation and protection.

End Use Analysis

Food & Beverage Leads with Commanding Market Share in Bags and Containers Sector

In 2024, the Food & Beverage sector maintained its dominance in the By End Use Analysis segment of the Bags and Containers Market. This sector continues to thrive, driven by increasing consumer demand for convenience foods and sustainable packaging solutions.

Companies in the Food & Beverage industry are increasingly adopting innovative packaging techniques that not only extend shelf life but also appeal to environmentally conscious consumers.

The Retail sector follows, influenced by the surge in e-commerce and the need for durable and secure packaging solutions that ensure product integrity from warehouse to consumer. Retail packaging innovations are focusing on improving customer unboxing experiences and incorporating recycled materials, reflecting broader sustainability trends.

Healthcare, another key segment, has shown robust growth due to stringent regulations requiring high standards for packaging to maintain sterility and integrity of medical products. The rise in global health awareness and pharmaceutical needs further amplifies demand for specialized containers and packaging.

The Industrial segment benefits from globalization and the expansion of manufacturing sectors, necessitating reliable and sturdy packaging for safe materials handling and shipping.

Lastly, the Personal Care segment is evolving with consumer preferences shifting towards premium, aesthetically pleasing, yet functional packaging. Brands are investing in visually striking designs that stand out on shelves and resonate with personal wellness trends.

Key Market Segments

By Type

- Backpacks

- Travel Bags

- Sports Bags and Tote Bags

- Others

By Distribution Channel

- Offline

- Online

By Material Type

- Plastic

- Paper

- Canvas

- Jute

- Metal

By End Use

- Food Beverage

- Retail

- Healthcare

- Industrial

- Personal Care

Drivers

Rising Demand for Convenience Packaging Fuels Growth in the Bags and Containers Market

As consumer preferences evolve toward ease of use and portability, there is a noticeable surge in the demand for bags and containers that offer ready-to-use, convenient packaging solutions. This trend is significantly influenced by the expansion of e-commerce, which necessitates durable, lightweight, and environmentally friendly packaging to protect and transport a wide range of products.

Additionally, growing environmental concerns have propelled the market towards sustainable options, increasing the demand for recyclable and biodegradable packaging. Urbanization, particularly in developing regions, further boosts this demand as more people move to urban centers, requiring reliable and efficient packaging for daily essentials, retail items, and food.

These drivers collectively shape the dynamic landscape of the bags and containers market, emphasizing the need for innovative, practical, and sustainable packaging solutions.

Restraints

High Production Costs Pose Challenges to the Bags and Containers Market

The bags and containers market faces significant challenges due to the high production costs associated with sustainable materials and advanced packaging technologies. These increased costs can restrict market growth, particularly in regions where price sensitivity is a major factor for consumers and businesses.

Additionally, environmental concerns related to the use of non-recyclable and non-biodegradable materials continue to hinder market expansion. As environmental regulations become stricter, the pressure mounts on manufacturers to develop more eco-friendly alternatives.

However, the transition to greener materials often involves higher expenditures, which can be a deterrent for companies looking to innovate while maintaining competitive pricing. These restraints highlight the delicate balance required in the market between sustainability, technological advancement, and cost-efficiency.

Growth Factors

Smart Packaging Innovation Opens New Avenues in Bags and Containers Market

The bags and containers market is ripe for growth, particularly through the adoption of smart packaging technologies. These innovations are not just about keeping products safe; they’re transforming how brands interact with consumers.

Smart packaging allows for real-time product tracking, advanced anti-counterfeit measures, and dynamic consumer engagement. Imagine a world where your bag or container tells you the history of the product inside, or better yet, verifies its authenticity with a tap of your smartphone. This technological leap is opening up new pathways for brands to create trust and enhance user experience.

Additionally, as the world leans towards sustainable solutions, there’s a significant shift towards compostable and biodegradable materials. This not only caters to the growing eco-conscious consumer base but also aligns with global sustainability goals. Meanwhile, the surge in e-commerce has spiked the demand for customized and robust packaging solutions to ensure product safety during transit.

Not to be overlooked, the personal care and cosmetics sector also presents lucrative opportunities for the bags and containers industry to innovate in both design and functionality, making packaging a central element of product appeal. This convergence of technology, sustainability, and consumer demand creates a fertile ground for market expansion and innovation.

Emerging Trends

Automation and AI Revolutionize Bags and Containers Production

In the bags and containers market, a significant trend is the integration of automation and artificial intelligence, streamlining both the production and design processes. This technological shift is not only optimizing manufacturing efficiency but also enhancing the customization capabilities of packaging products, allowing for more precise and faster production cycles.

Furthermore, the rising popularity of flexible packaging solutions, such as stand-up pouches, is reshaping the market landscape. These options offer consumers cost-effective, convenient, and product-preserving alternatives, adding value by extending shelf life and maintaining product integrity.

Additionally, there’s a noticeable surge in consumer preference for reusable containers, driven by increasing environmental awareness. This trend is particularly evident in sectors like grocery and takeout services, where there is a growing demand for durable and sustainable packaging solutions. These factors collectively contribute to a dynamic evolution in the bags and containers industry, where convenience, sustainability, and technology converge to meet modern consumer needs and environmental standards.

Regional Analysis

Asia Pacific Leads Global Bags and Containers Market with 45.2% Share, Valued at USD 21.7 Billion

The global market for bags and containers is segmented into several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each exhibiting distinct market dynamics and growth potentials.

Asia Pacific is the dominant region in the bags and containers market, commanding a 45.2% market share with a valuation of USD 21.7 billion. This region’s leadership is driven by rapid urbanization, expanding retail sectors, and significant investments in packaging industries, particularly in China, India, and Japan. The increasing consumer demand for sustainable and convenient packaging options further fuels market growth.

Regional Mentions:

North America follows, characterized by high consumer spending capability and a strong presence of global players who are innovating in biodegradable and eco-friendly packaging solutions. The U.S. market is particularly strong in advanced packaging technologies, which is critical in driving the North American market’s growth.

In Europe, the market is propelled by stringent regulations regarding packaging waste and sustainability. Countries like Germany, the UK, and France lead in adopting eco-friendly bags and containers, pushing manufacturers to innovate and reduce the environmental impact of their packaging solutions.

The Middle East & Africa region shows promising growth, attributed to the expanding retail sector and urban development, especially in GCC countries. However, the market is still nascent, with significant potential for penetration by both local and international companies looking to establish a foothold.

Latin America presents a dynamic market environment with rising consumer awareness about sustainable packaging. Brazil and Mexico are at the forefront, driven by urban growth and increased standards of living, which influence packaging needs and preferences.

Overall, while Asia Pacific leads the market in size and growth rate, each region presents unique opportunities and challenges that players in the bags and containers market must navigate to optimize their regional strategies and maximize market penetration.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global bags and containers market continues to witness dynamic shifts, influenced largely by changing consumer preferences and the increasing emphasis on sustainability. Among the key players, Samsonite International S.A., LVMH Moët Hennessy Louis Vuitton, and Nike, Inc. remain standout contributors due to their strategic initiatives that focus on innovation and eco-friendly solutions.

Samsonite International S.A. is leading the way with its robust approach to integrating cutting-edge technology into product design. This includes the development of lightweight, durable materials that cater to the growing demand for easy-to-carry and long-lasting luggage. Their continued investment in R&D positions them as pioneers in the market, driving trends that other companies often follow.

LVMH Moët Hennessy Louis Vuitton showcases its strength in the luxury segment, capitalizing on its established brand prestige to expand further into premium bags and accessories. Their strategy revolves around exclusivity and premium pricing, which continues to attract high-end consumers. The company’s focus on artisanal craftsmanship and heritage marketing effectively leverages consumer nostalgia and preference for luxury goods.

Nike, Inc., traditionally known for athletic wear, has successfully penetrated the casual and sports bag market. Their focus on versatile designs that cater to both athletic and everyday use appeals to a broad customer base. Nike’s commitment to sustainability, particularly in using recycled materials across its product lines, resonates well with the environmentally conscious consumer.

Overall, these companies are not just responding to market trends but are actively shaping the industry through innovation, sustainability efforts, and targeted marketing strategies. Their ability to adapt and lead in these areas determines their continued dominance and influence in the global bags and containers market.

Top Key Players in the Market

- Luggage America Inc.

- Samsonite International S.A.

- Ralph Lauren Corp.

- Bric’s Industria Valigeria Fine SPA

- V.F. Corporation

- Delsey S.A

- Tommy Hilfiger

- Antler Ltd.

- VIP Industries Ltd.

- LVMH Moët Hennessy Louis Vuitton

- Nike, Inc.

- Briggs & Riley Travel ware

- Valigeria Roncato

- Ace Co. Ltd.

Recent Developments

- In July 2024, the Cologne-based company Vytal secured €6.2 million in funding to enhance and expand its technology platform dedicated to circular reusable packaging solutions aimed at reducing waste.

- In December 2024, Movopack announced the acquisition of $2.5 million in funding to develop and market its innovative sustainable packaging solutions designed specifically for the e-commerce sector.

- In November 2024, Ukhi successfully raised $1.2 million to escalate the production of sustainable biomaterials for packaging, focusing on eco-friendly alternatives to conventional materials.

- In October 2024, Notpla secured a significant investment of £20 million to advance its development of sustainable packaging materials made from seaweed and plants, promoting environmental sustainability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 48.3 Billion |

| Forecast Revenue (2034) | USD 75.7 Billion |

| CAGR (2025-2034) | 4.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Backpacks, Travel Bags, Sports Bags and Tote Bags, Others), By Distribution Channel (Offline, Online), By Material Type (Plastic, Paper, Canvas, Jute, Metal), By End Use (Food Beverage, Retail, Healthcare, Industrial, Personal Care) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Luggage America Inc., Samsonite International S.A., Ralph Lauren Corp., Bric’s Industria Valigeria Fine SPA, V.F. Corporation, Delsey S.A, Tommy Hilfiger, Antler Ltd., VIP Industries Ltd., LVMH Moët Hennessy Louis Vuitton, Nike, Inc., Briggs & Riley Travel ware, Valigeria Roncato, Ace Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |