Quick Navigation

Report Overview

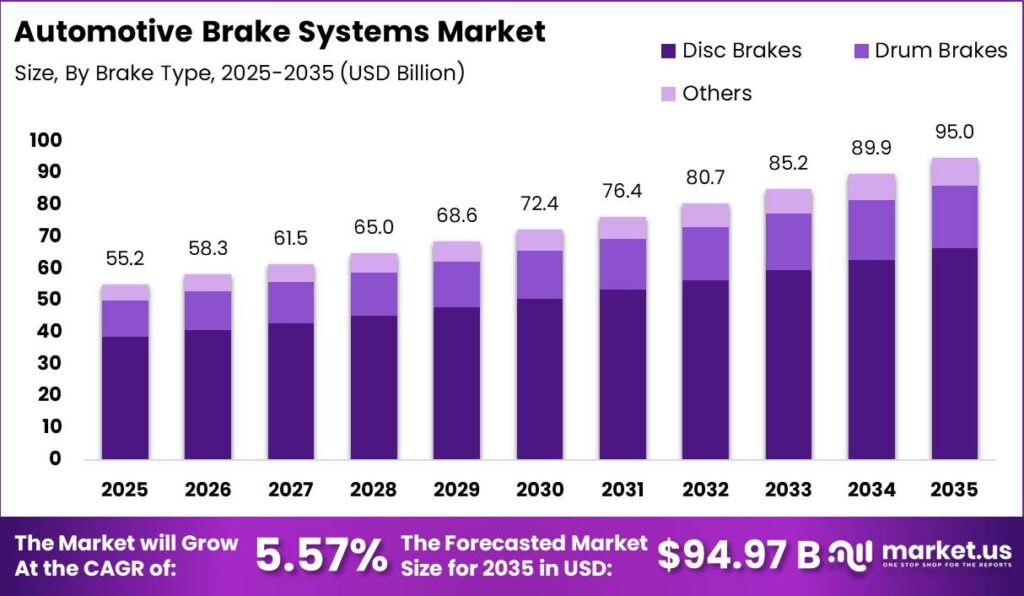

Global Automotive Brake Systems Market size is expected to be worth around USD 94.97 Billion by 2035 from USD 55.24 Billion in 2025, growing at a CAGR of 5.57% during the forecast period 2026 to 2035.

The automotive brake systems market encompasses all friction-based, hydraulic, pneumatic, and electromechanical components that generate controlled deceleration in passenger cars, commercial vehicles, and electric platforms. Core product categories include disc brake assemblies, drum brake systems, anti-lock braking modules, electronic stability control units, and regenerative braking systems sold through OEM supply chains and independent aftermarkets.

Key Takeaways

- Market size in 2025: USD 55.24 Billion

- Market size in 2035: USD 94.97 Billion

- CAGR (2026–2035): 5.57%

- Dominant brake type: Disc Brakes with 69.90% share

- Dominant technology: Anti-Lock Braking System (ABS) with 35.20% share

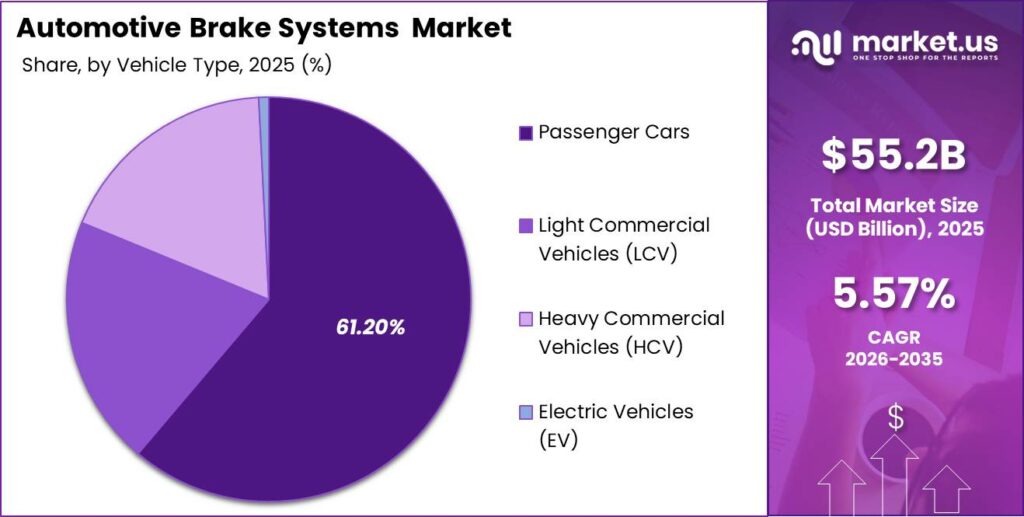

- Dominant vehicle type: Passenger Cars with 61.20% share

- Dominant sales channel: OEM with 71.80% share

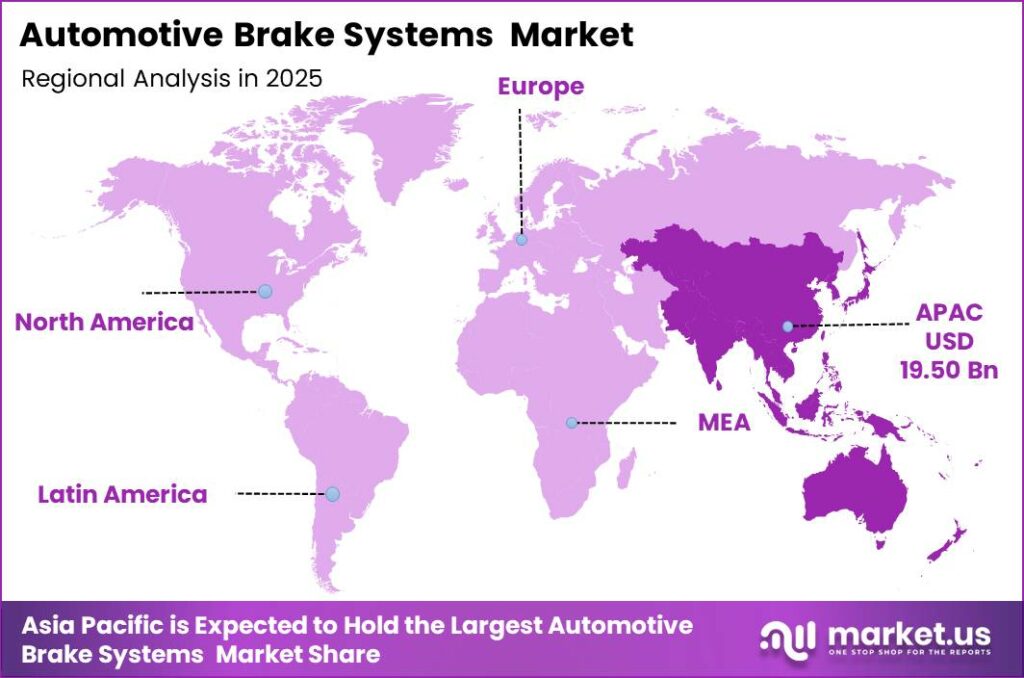

- Dominant region: Asia Pacific with 35.30% share, valued at USD 19.50 Billion

Regulatory mandates are reshaping brake system specifications at the OEM level. The NHTSA finalized FMVSS No. 127 in April 2024, requiring Automatic Emergency Braking (AEB) and Pedestrian AEB systems on all new light vehicles, with compliance beginning September 1, 2029. This mandate directly expands electronic brake control content per vehicle and creates a defined commercial ramp for brake system suppliers serving U.S. OEM programs.

International regulatory alignment is reinforcing this demand structure beyond North America. In March 2026, UNECE adopted the first global standard establishing test methods and emission limits for brake particle emissions from light-duty vehicles. This regulatory convergence signals that advanced friction materials and brake dust management systems will become mandatory content across all major vehicle markets within this forecast period.

Brake Type Analysis

Disc Brakes dominate with 69.90% due to superior thermal management and OEM fitment rates.

In 2025, Disc Brakes held a dominant market position in the By Brake Type segment of the Automotive Brake Systems Market, with a 69.90% share. Disc brakes dissipate heat more efficiently than drum alternatives, reducing brake fade during repeated hard stops. According to the European Automobile Manufacturers’ Association (ACEA), front disc brake fitment reached 100% across all new M1 passenger cars sold in Europe by 2024, confirming near-total OEM standardization in mature markets. Suppliers with strong disc brake caliper programs hold the most defensible volume positions in this segment.

Drum Brakes retain a structural role in rear-axle applications for entry-level passenger vehicles and light commercial platforms across price-sensitive markets. The International Organization of Motor Vehicle Manufacturers (OICA) reported global light vehicle production of approximately 92 million units in 2024, with drum rear axle fitment remaining above 40% in markets such as India and Southeast Asia where cost-per-vehicle economics constrain disc brake adoption at rear positions. This persistent fitment share creates sustained volume demand for drum brake components in high-production emerging market assembly programs.

Technology Analysis

Anti-Lock Braking System (ABS) dominates with 35.20% due to global mandatory fitment across all vehicle classes.

In 2025, Anti-Lock Braking System (ABS) held a dominant market position in the By Technology segment of the Automotive Brake Systems Market, with a 35.20% share. Antilock Braking System fitment is legally mandated across all new passenger cars in the EU, United States, Japan, South Korea, India, and China, covering markets that collectively produce more than 70 million vehicles annually per OICA data. This regulatory universality makes ABS the highest-volume electronic brake control technology by unit count and secures its dominant technology share through the forecast period.

Electronic Stability Control (ESC) systems build on ABS hardware by adding yaw-rate sensors and individual wheel torque modulation, raising the per-vehicle brake electronics content value. The UNECE estimates that ESC reduces fatal single-vehicle crashes by up to 49% in cars and 59% in SUVs based on its in-depth accident analysis reports, a safety case that has driven mandatory ESC fitment laws across more than 40 countries. Brake suppliers delivering integrated ABS and ESC modules secure higher unit revenue than standalone ABS suppliers.

Traction Control System (TCS), Electronic Brake Force Distribution (EBD), and Automotive Regenerative Braking System technologies complete the technology mix by addressing wheel slip during acceleration, rear-axle load balancing, and energy recovery in electrified platforms respectively. The IEA reported global electric car sales exceeding 17 million units in 2024, representing 20% of all new car sales globally. This EV volume expansion directly scales regenerative braking system fitment rates and creates a structural content upgrade opportunity for suppliers with validated blended braking control architectures.

Vehicle Type Analysis

Passenger Cars dominate with 61.20% due to highest global production volume and mandatory safety content.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Brake Systems Market, with a 61.20% share. Passenger car production volume drives brake system demand more than any other vehicle category. OICA data confirms global passenger car output of approximately 67 million units in 2024, and each unit requires a complete front and rear brake assembly, ABS module, and increasingly an ESC and AEB-compatible control unit. OEM brake suppliers with established passenger car platform programs hold the highest revenue concentration in this segment.

Light Commercial Vehicles (LCV) represent the second-largest vehicle type by brake system content value, serving last-mile delivery, utility, and small fleet applications where brake wear rates exceed passenger car norms due to load cycling and stop frequency. The World Bank reported that urban freight transport volumes grew by approximately 6% annually between 2020 and 2024 across developing economies, directly supporting LCV fleet expansion and aftermarket brake replacement demand in high-density urban markets. Brake suppliers with LCV-specific disc and drum programs capture both OEM and high-frequency aftermarket replacement revenue.

Heavy Commercial Vehicles (HCV) and Electric Vehicles (EV) complete the vehicle type structure. The IEA confirmed that global electric car stock surpassed 40 million units by end-2023, with the EV segment requiring fundamentally different brake specifications including regenerative blending control and reduced thermal load management given the lower mechanical braking frequency compared to ICE equivalents. Brake suppliers who qualify electro-hydraulic and brake-by-wire architectures for EV platforms gain access to the highest-growth vehicle sub-segment in the forecast period.

Sales Channel Analysis

OEM dominates with 71.80% due to platform-locked supply agreements and mandatory content fitment.

In 2025, OEM held a dominant market position in the By Sales Channel segment of the Automotive Brake Systems Market, with a 71.80% share. OEM supply agreements lock brake system suppliers into multi-year platform contracts tied to vehicle production programs, generating predictable volume and design-in advantage that aftermarket competitors cannot replicate. The OICA reported that global vehicle production exceeded 93 million units in 2023, and each unit requires full OEM-sourced brake system fitment at assembly, making the OEM channel structurally dominant by unit volume and revenue concentration.

The Aftermarket channel holds the remaining share and is structurally driven by vehicle fleet age and brake wear replacement cycles. The U.S. Bureau of Transportation Statistics reported that the average age of registered light vehicles in the United States reached 12.6 years in 2024, extending replacement part demand across a large base of aging vehicles. Brake pads and rotors on average require replacement every 50,000 to 70,000 kilometers depending on driving conditions, generating recurring aftermarket volume that grows as the global registered fleet expands beyond 1.4 billion vehicles.

Key Market Segments

By Brake Type

- Disc Brakes

- Drum Brakes

- Others

By Technology

- Anti-Lock Braking System (ABS)

- Electronic Stability Control (ESC)

- Traction Control System (TCS)

- Electronic Brake Force Distribution (EBD)

- Regenerative Braking System

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EV)

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Brake Systems Market with a Market Share of 35.30%, Valued at USD 19.50 Billion

Asia Pacific holds the largest regional share of the automotive brake systems market, underpinned by the highest vehicle production concentration globally. China, Japan, South Korea, and India collectively account for the majority of Asia Pacific output, with China alone producing over 30 million vehicles annually per OICA data. This manufacturing density makes Asia Pacific the primary OEM brake system procurement hub and secures its dominant 35.30% revenue share through the forecast period.

India represents the fastest-growing country within Asia Pacific and ranks among the highest-growth markets globally for automotive brake systems. India’s vehicle production crossed 5.8 million units in 2024 per SIAM data, and Bharat NCAP safety ratings are accelerating disc brake adoption across entry-level passenger cars that previously used rear drum configurations. This regulatory-driven content upgrade creates a direct revenue per vehicle uplift for brake suppliers qualifying disc brake programs for Indian OEM platforms.

North America and Europe collectively represent the second and third largest regional revenue pools, supported by high brake system content per vehicle driven by mandatory AEB, ESC, and ADAS integration requirements. Latin America and Middle East & Africa contribute smaller revenue shares but benefit from expanding vehicle fleets and rising aftermarket replacement demand as vehicle parc age increases across both regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Regulatory mandates and electrification gaps create entry points across brake technology tiers

The OEM sales channel holds a 71.80% revenue share but concentrates value among a small group of platform-qualified Tier-1 suppliers. This concentration leaves the aftermarket channel structurally underserved by advanced brake technologies, as most electronic brake upgrades remain OEM-fitment-only. Aftermarket-focused suppliers who develop retrofit ABS and ESC kits validated for aging vehicle fleets in India, Southeast Asia, and Sub-Saharan Africa can capture recurring replacement revenue outside the locked OEM program structure.

The Regenerative Braking System sub-segment within the Technology segment remains the lowest-penetration technology category in the market despite the IEA confirming global EV sales exceeded 17 million units in 2024. Most current regenerative braking architectures are OEM-integrated and not available as aftermarket upgrades. Suppliers who develop standardized regenerative blending retrofit modules for hybrid commercial vehicle fleets in China, the EU, and the United States gain a first-mover position in a segment with no established competitive base.

The Heavy Commercial Vehicle sub-segment is growing in India, China, and Sub-Saharan Africa but remains under-penetrated by air disc brake technology relative to mature Western markets. The World Bank’s urban freight growth data confirms expanding HCV fleet size in developing economies, yet brake system content per HCV in these markets remains weighted toward lower-value drum and basic hydraulic systems. Tier-1 air disc brake suppliers who localize manufacturing costs for emerging market HCV programs capture both OEM fitment and high-frequency aftermarket replacement revenue from operators running high-mileage fleets.

Asia Pacific holds a 35.30% market share valued at USD 19.50 Billion but contains significant intra-regional disparity. Established markets such as Japan and South Korea are fully penetrated by advanced brake electronics, while emerging Southeast Asian markets including Vietnam, Indonesia, and Thailand remain at early disc brake and ABS adoption stages. New entrants who target ASEAN OEM supplier qualification programs gain access to rapidly expanding vehicle production volumes with lower incumbent competition than China or Japan present.

Technology and Innovation Landscape - Brake-by-wire, AI diagnostics, and modular architectures define the next competitive cycle

Brake-by-wire control units are becoming the defining technology transition across next-generation vehicle platforms. ZF Friedrichshafen AG secured a contract to equip nearly 5 million vehicles with its hybrid Brake-by-Wire system, demonstrating that partial electrohydraulic architectures are reaching commercial scale ahead of full EMB deployment. Suppliers who achieve ISO 26262 ASIL-D validation for brake-by-wire platforms before 2028 will lock in platform design-in positions that competitors without certified architectures cannot contest.

AI-powered brake wear prediction is expanding through real-time sensor fusion and vehicle diagnostics integration. OEMs are embedding brake pad wear sensors, wheel speed data, and thermal load signals into vehicle diagnostics platforms that feed predictive maintenance algorithms. This data layer creates a recurring connected brake SaaS revenue stream for suppliers and fleet operators, converting a hardware replacement cycle into a subscription analytics business with gross margins substantially above physical brake component economics.

OEMs are adopting modular braking architectures that integrate ABS, ESC, and regenerative braking control into unified electronic control units. This consolidation reduces per-vehicle brake electronics BOM count, lowers weight, and simplifies software validation. Suppliers who deliver a single integrated control unit covering all three functions command higher per-unit revenue than those supplying discrete ABS, ESC, and regenerative modules separately, and reduce the OEM’s system integration cost, creating a dual commercial incentive for OEM program selection.

Over-the-air software updates are enabling continuous optimization of braking performance in software-defined vehicles, decoupling brake system performance from the hardware replacement cycle for the first time. This capability is particularly valuable for AEB calibration updates as pedestrian detection algorithms improve and regulatory test requirements expand, as confirmed by NHTSA’s May 2026 NCAP proposal adding Rear Automatic Braking with pedestrian detection. Brake system suppliers who own the software stack rather than only the hardware gain the ability to generate post-sale revenue and differentiate on continuous performance improvement.

Drivers

Mandatory Advanced Driver Assistance Systems and AEB regulations are the primary structural force expanding OEM brake system content per vehicle. NHTSA’s finalized FMVSS No. 127 rule requires AEB and Pedestrian AEB on all new U.S. light vehicles by September 2029, and UNECE’s expanded heavy-vehicle AEBS regulations are making electronically integrated braking architectures standard across commercial platforms. Each compliance mandate directly increases the electronic brake control module, sensor, and actuator content value per vehicle, benefiting Tier-1 brake suppliers with qualified integrated system programs.

EV platform growth compounds this demand by requiring regenerative-compatible hydraulic brake systems that blend friction and motor braking seamlessly. ADAS deployment is simultaneously driving demand for high-response brake control modules integrated with ESC. Heavy commercial vehicle safety regulations are accelerating upgrades to high-performance air disc braking systems across fleet operators in regulated markets. These converging demand vectors create layered content expansion across all vehicle types and both OEM and aftermarket sales channels.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro 7 Brake Particulate Emission Limits Mandating Low-Dust & Advanced Friction Material Upgrades | +1.9% | EU (all M1/N1 type approvals from November 29, 2026) | Short term (≤ 2 years) |

| EV & Hybrid Platform Growth Driving Regenerative Braking & Integrated Brake-By-Wire Demand | +1.6% | China, Europe, United States, South Korea, Japan | Short term (≤ 2 years) |

| Mandatory ADAS & AEB Fitment Increasing Electrohydraulic & Blended Braking System Content | +1.2% | EU, United States, India, Japan, South Korea, ASEAN | Short term (≤ 2 years) |

| Expanding Global Vehicle Fleet & Rising Aftermarket Brake Replacement Demand | +0.9% | Global, led by India, China, Southeast Asia, Middle East & Africa | Short term (≤ 2 years) |

| Bharat NCAP & Upgraded Safety Standards Requiring Disc Brake Adoption in Indian Market | +0.6% | India | Medium term (2–4 years) |

| Rising Commercial Vehicle Production in Asia-Pacific & Africa Boosting Heavy-Duty Brake Demand | +0.5% | India, China, Southeast Asia, Sub-Saharan Africa | Medium term (2–4 years) |

Restraints

Brake-by-wire platforms require costly ISO 26262 functional safety validation and calibration, creating a high barrier to commercialization that delays adoption timelines for suppliers without dedicated safety engineering programs. Volatile steel, cast iron, and semiconductor supply chains are simultaneously raising brake system manufacturing costs across all tiers. The U.S. Section 232 tariff escalation on steel and aluminum directly inflates raw material input costs for caliper bodies, rotors, and bracket assemblies that constitute over half of a typical disc brake assembly bill of materials.

The U.S. 25% auto parts tariff compounds input cost pressure by disrupting established global brake system supply chains connecting Mexico, Canada, South Korea, and Germany to U.S. OEM assembly programs. EV regenerative braking reduces conventional brake wear rates in high-EV markets, suppressing aftermarket replacement frequency in China, Europe, and the United States over the medium term. These restraints collectively compress margin and complicate investment planning for brake system suppliers dependent on U.S. market volumes or globally integrated supply chains.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. 50% Steel & Aluminum Tariffs Inflating Brake Component Raw Material Costs | -2.0% | United States; cascading to globally sourced Tier-1 brake suppliers serving U.S. OEMs | Short term (≤ 2 years) |

| U.S. 25% Auto Parts Tariff Disrupting Global Brake System Supply Chains | -1.4% | United States, Mexico, Canada, South Korea, Germany | Short term (≤ 2 years) |

| Global Passenger Vehicle Production Slowdown Suppressing OEM Brake System Volumes | -1.0% | Europe, North America, China | Short term (≤ 2 years) |

| EV Regenerative Braking Reducing Conventional Brake Wear & Aftermarket Replacement Frequency | -0.7% | China, Europe, United States — primary EV-dense markets | Medium term (2–4 years) |

| High Capital Investment Requirement for Euro 7-Compliant Friction Material R&D & Tooling | -0.5% | EU, UK — friction material SMEs with limited R&D budgets | Short term (≤ 2 years) |

Challenges

Counterfeit and substandard brake components remain the most structurally entrenched challenge suppressing legitimate market value across price-sensitive emerging markets. In India, Southeast Asia, Sub-Saharan Africa, and Latin America, informal vehicle repair ecosystems handle an estimated 60–75% of total aftermarket brake component volume. Counterfeit pads sold at 30–50% below genuine part prices force brand-owning manufacturers to compress entry-tier pricing by 20–35%, reducing blended gross margin by an estimated 6–12 percentage points versus counterfeit-free market scenarios.

Brake-by-wire validation and safety certification lag creates a secondary challenge by delaying high-value electromechanical system commercialization globally. Friction material reformulation cost and process complexity penalizes EU and UK Tier-2 suppliers with limited R&D budgets as Euro 7 compliance deadlines approach. Thermal management challenges in heavy EV and PHEV platforms and a skilled brake system NVH and dynamics engineering shortage in North America, Germany, and Japan complete the challenge landscape, each requiring multi-year mitigation timelines that compress near-term growth potential for affected market participants.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Counterfeit & Substandard Aftermarket Proliferation | -1.5% | India, Southeast Asia, Sub-Saharan Africa, Latin America, China | Long term (≥ 4 years) |

| Brake-By-Wire Validation & Safety Certification Lag | -1.2% | Global — constraining EV-platform high-value brake-by-wire adoption | Long term (≥ 4 years) |

| Friction Material Reformulation Cost & Process Complexity | -0.9% | EU, UK — SME and Tier-2 friction material suppliers | Medium term (2–4 years) |

| Thermal Management Challenges in Heavy EV & PHEV Platforms | -0.7% | Global, particularly large-format EV SUV & truck platforms | Medium term (2–4 years) |

| Skilled Brake System NVH & Dynamics Engineering Shortage | -0.5% | Global, most acute in North America, Germany, Japan engineering hubs | Long term (≥ 4 years) |

Opportunities

Electro-mechanical brake-by-wire commercialization represents the highest-value uncaptured opportunity in the automotive brake systems market. Software-defined and autonomous vehicles are creating structural demand for EMB systems that eliminate hydraulic circuits entirely, while aging commercial vehicle fleets across North America, Europe, and Asia Pacific are expanding retrofit opportunities for intelligent electronic braking systems. Connected brake health monitoring is enabling predictive maintenance and fleet analytics solutions that generate recurring software revenue beyond one-time hardware sales.

Carbon-ceramic and lightweight composite rotor adoption is accelerating across premium EV and performance vehicle segments in Europe, the United States, Japan, and China, where vehicle weight reduction directly extends battery range. NHTSA estimates that mandatory AEB implementation will save at least 360 lives and prevent approximately 24,000 injuries annually once fully deployed, reinforcing the policy case for continued electronic brake content expansion. Suppliers who commercialize Sensify-class software-defined braking platforms, EMB actuators, and low-emission friction systems early will capture the highest-margin positions across the next brake technology cycle.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Electro-Mechanical Brake-By-Wire (EMB) Commercialization for EV & Autonomous Platforms | +2.2% | China, Europe, United States, South Korea, Japan | Long term (≥ 4 years) |

| Brake Dust Capture Filter & Low-Emission System Aftermarket Retrofit in EU | +1.5% | EU, UK, Norway — Euro 7-aligned vehicle fleets | Medium term (2–4 years) |

| Disc Brake Conversion & Upgrade Aftermarket in Indian Passenger Car & Two-Wheeler Segments | +1.1% | India | Medium term (2–4 years) |

| Predictive Brake Wear Monitoring & Connected Brake SaaS for Fleet Management | +0.9% | United States, EU, GCC, India — commercial fleet & shared mobility operators | Medium term (2–4 years) |

| Carbon Ceramic & Composite Rotor Premiumization in EV & Performance Vehicle Segments | +0.6% | Europe, United States, Japan, China (premium EV segment) | Long term (≥ 4 years) |

Key Company Insights

Robert Bosch GmbH holds the broadest integrated brake system portfolio in the global market, combining ABS, ESC, AEB control modules, and electrohydraulic brake actuators across passenger car, commercial vehicle, and EV platforms. This systems integration depth creates a design-in advantage that single-component competitors cannot match at the OEM program level. However, Bosch’s high exposure to ICE vehicle platforms creates a medium-term revenue transition risk as electrification compresses conventional brake booster and vacuum system volumes.

Brembo S.p.A. is executing an aggressive pivot from premium friction hardware to software-defined braking, with its Sensify intelligent Brake-by-Wire platform entering large-scale series production for a leading global vehicle manufacturer in May 2026. Brembo simultaneously signed additional Sensify contracts with new customers, targeting hundreds of thousands of units per year. This volume commitment positions Brembo as the first friction specialist to commercialize brake-by-wire at scale, creating a structural gross margin upgrade as software and electronics content replaces commodity caliper revenue.

Key Players

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Brembo S.p.A.

- Akebono Brake Industry Co., Ltd.

- Aisin Corporation

- Hyundai Mobis Co., Ltd.

- Hitachi Astemo, Ltd.

- Haldex AB

- Advics Co., Ltd.

- Knorr-Bremse AG

- Brakes India Private Limited

Recent Developments

- January 2025: ZF Friedrichshafen AG secured a major global OEM contract to supply its hybrid Brake-by-Wire technology, with the agreement expected to equip nearly 5 million vehicles over the life of the contract.

- January 2025: ADVIK completed the acquisition of Germany-based Powersports MTG GmbH, a manufacturer of mechanical and hydraulic motorcycle braking and clutch systems, gaining access to more than 60 patents in hydraulic braking technology and expanding its R&D capabilities in Germany.

- March 2026: UNECE adopted the world’s first international regulation establishing standardized test methods and emission limits for brake particle emissions from light-duty vehicles, creating a binding global compliance framework for brake friction material suppliers.

- May 2026: NHTSA proposed updating its New Car Assessment Program (NCAP) by adding Rear Automatic Braking (RAB) with pedestrian detection as a recommended advanced safety technology for passenger vehicles.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 55.24 Billion |

| Forecast Revenue (2035) | USD 94.97 Billion |

| CAGR (2026-2035) | 5.57% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Brake Type (Disc Brakes, Drum Brakes, Others), By Technology (Anti-Lock Braking System (ABS), Electronic Stability Control (ESC), Traction Control System (TCS), Electronic Brake Force Distribution (EBD), Regenerative Braking System), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EV)), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Brembo S.p.A., Akebono Brake Industry Co., Ltd., Aisin Corporation, Hyundai Mobis Co., Ltd., Hitachi Astemo, Ltd., Haldex AB, Advics Co., Ltd., Knorr-Bremse AG, Brakes India Private Limited |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |