Quick Navigation

Report Overview

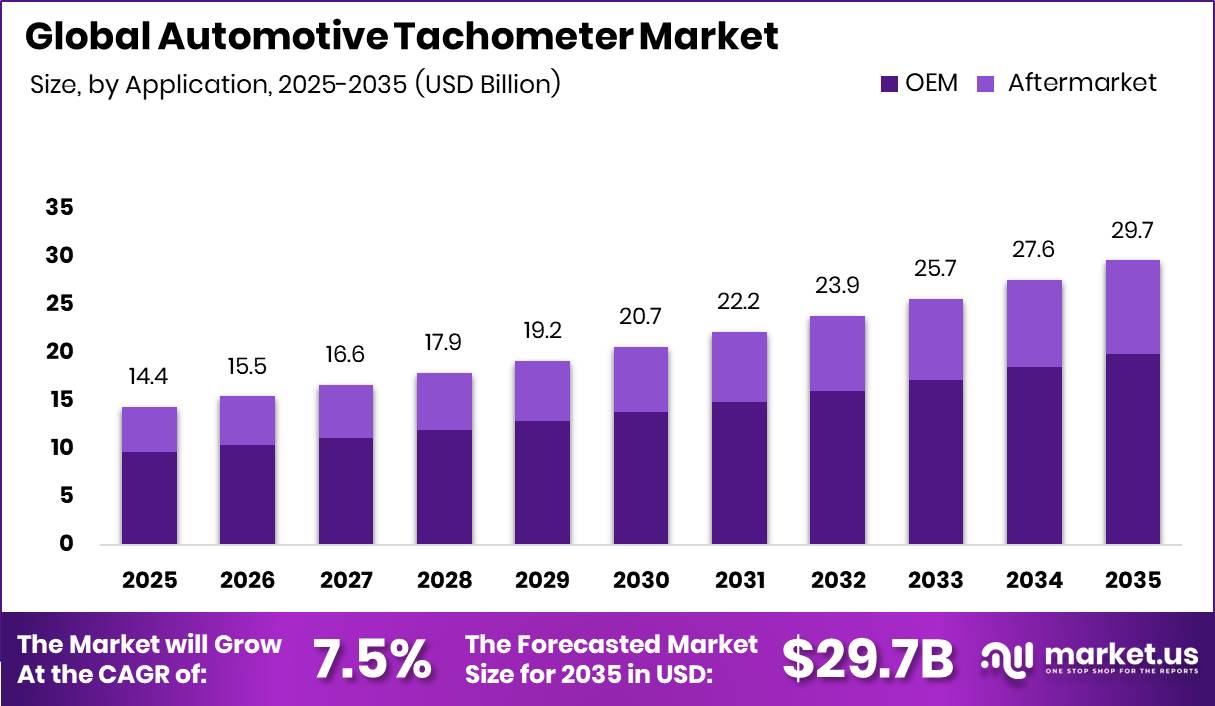

Global Automotive Tachometer Market size is expected to be worth around USD 29.7 Billion by 2035 from USD 14.4 Billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035. This trajectory reflects a market more than doubling in value over a decade. Suppliers and investors entering now face a structurally expanding revenue base with rising content value per vehicle.

The automotive tachometer market covers instruments that measure and display engine rotational speed in revolutions per minute across passenger cars, commercial vehicles, two-wheelers, and off-highway vehicles. The market spans original equipment manufacturer supply channels and the aftermarket replacement segment. Products range from traditional analog dials to advanced digital and hybrid display systems integrated into modern instrument clusters.

Key Takeaways

- Global Automotive Tachometer Market was valued at USD 14.4 Billion in 2025 and is forecast to reach USD 29.7 Billion by 2035.

- The market is projected to grow at a CAGR of 7.5% from 2026 to 2035.

- By Display Type, LED Display dominates with a 34.5% share.

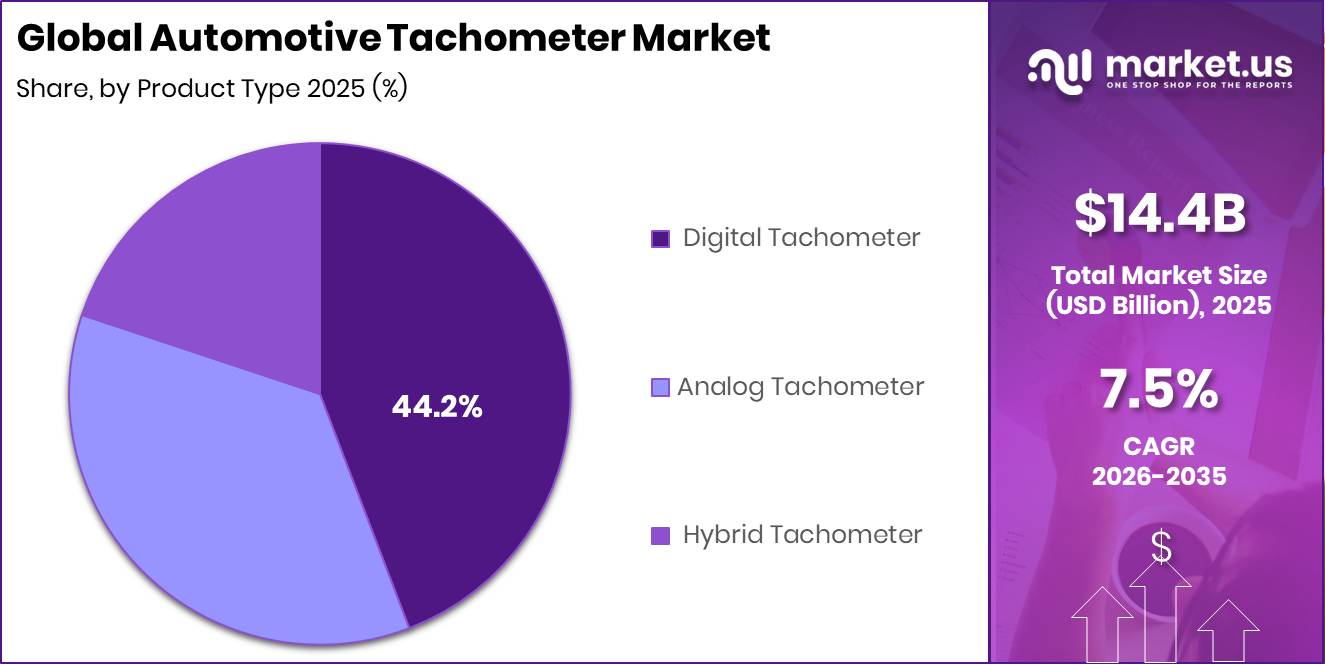

- By Product Type, Digital Tachometer holds the largest share at 44.2%.

- By Technology, Solid-State Tachometer leads with 47.4% share.

- By Vehicle Type, Passenger Cars account for 49.9% of the market.

- By Application, OEM holds a dominant share of 67.1%.

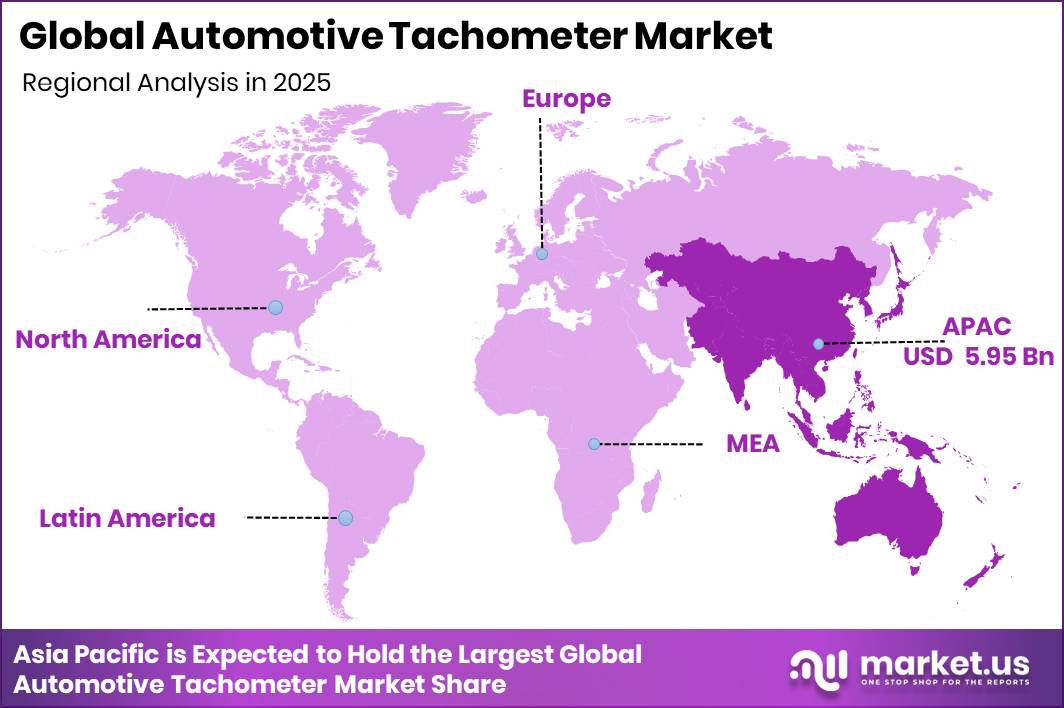

- Asia-Pacific is the dominant region with a 41.3% market share, valued at USD 5.95 Billion.

Government regulations now shape tachometer product architecture directly. In the United States, FMVSS No. 101 governs display identification requirements for speedometers and odometers, while in Europe, UNECE R155 applied to new vehicle type approvals from July 2022 and extended to all existing vehicle types by July 2024. These mandates force cluster redesigns and raise compliance costs, giving technically capable suppliers a structural pricing advantage over commodity producers.

According to IEA data, 630 battery electric vehicle models were available globally in 2025, compared with fewer than 200 models in 2018. This model proliferation accelerates the shift away from engine-RPM tachometers in new vehicle programs. As reported by ACEA data, battery-electric vehicles accounted for 13.6% of all new EU passenger car registrations in 2024, which means the addressable market for conventional tachometers in Europe is narrowing faster than overall vehicle sales figures suggest.

However, the total market continues to expand because hybrid powertrains preserve RPM display requirements and because Asia-Pacific production growth more than offsets European BEV penetration. Tachometer content per vehicle is also rising as digital cluster adoption spreads into mid-range and mass-market segments, increasing average unit values even where traditional volume channels face pressure.

Display Type Analysis

LED Display dominates with 34.5% due to low cost and wide vehicle compatibility.

In 2025, LED Display held a dominant market position in the By Display Type segment of the Automotive Tachometer Market, with a 34.5% share. LED technology delivers proven brightness, long operational life, and manufacturing cost advantages that make it the preferred choice for volume-segment passenger cars and commercial vehicles. OEM procurement teams selecting LED clusters retain margin flexibility without sacrificing regulatory display compliance.

LCD Display holds the second-largest position in this segment. LCD technology supports higher-resolution graphics and configurable layouts, making it the preferred upgrade path in mid-range and premium vehicles shifting to fully digital instrument clusters. As cockpit integration deepens, LCD-based clusters command higher per-unit values and stronger supplier margins than LED alternatives.

Analog Dial retains a share of the display type segment driven by cost-sensitive vehicle programs in emerging markets and specialty applications. Analog dials face structural decline as digital adoption spreads downmarket, but they remain relevant in two-wheeler, off-highway, and entry-level passenger car segments where simplicity and repairability are prioritized over display versatility.

Product Type Analysis

Digital Tachometer dominates with 44.2% due to integration with digital cockpit architectures.

In 2025, Digital Tachometer held a dominant market position in the By Product Type segment of the Automotive Tachometer Market, with a 44.2% share. Digital units integrate directly with CAN bus systems and ECU-managed instrument clusters, making them the standard choice for new vehicle programs prioritizing real-time data visualization. This integration position gives digital tachometer suppliers stronger platform nomination leverage with OEM procurement teams.

Analog Tachometer holds a 36% share and remains commercially relevant in markets where mechanical reliability, calibration simplicity, and lower unit cost outweigh the benefits of digital integration. In November 2025, Genesis introduced the 2026 G70 Prestige Graphite with a new 12.3-inch fully digital instrument cluster replacing its previous analog configuration, illustrating the directional shift away from analog units in premium segments.

Hybrid Tachometer accounts for 20% of the product type segment. Hybrid units combine analog needle mechanisms with digital overlays, allowing automakers to retain familiar driver interfaces while embedding digital data feeds. This format suits mid-market vehicle programs managing consumer preference risk during the transition from traditional gauges to fully digital displays.

Technology Analysis

Solid-State Tachometer dominates with 47.4% due to durability and semiconductor integration advantages.

In 2025, Solid-State Tachometer held a dominant market position in the By Technology segment of the Automotive Tachometer Market, with a 47.4% share. Solid-state designs eliminate moving parts, reducing failure rates and warranty costs for OEMs. This reliability profile makes solid-state units the preferred technology for passenger car and light commercial vehicle programs where long service intervals and low field-return rates are procurement priorities.

Electromechanical Tachometer holds a 36% share and serves applications where established mechanical performance standards take precedence over digital upgrade paths. Figures from ACEA show hybrid-electric vehicle registrations in the EU increased by 33.1% year-over-year in December 2024, exceeding petrol vehicle registrations for the fourth consecutive month. This HEV growth sustains electromechanical tachometer demand because hybrid powertrains retain engine-RPM monitoring requirements that pure BEV platforms eliminate.

Digital Signal Processing Tachometer holds a 17% share and targets precision-critical applications such as high-performance vehicles and motorsport programs. DSP-based units process RPM signals with higher accuracy and faster refresh rates than electromechanical alternatives. As reported by ACEA, hybrid-electric vehicles accounted for 30.9% of all new EU passenger car registrations in 2024, reinforcing the hybrid segment as a sustained demand channel for precision RPM instrumentation.

Vehicle Type Analysis

Passenger Cars dominate with 49.9% due to global production volume and cluster upgrade rates.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Tachometer Market, with a 49.9% share. Passenger cars drive the highest absolute unit volumes and generate the broadest range of tachometer product specifications, from entry-level analog dials to fully integrated digital cluster systems. OEM program wins in passenger cars deliver the most scalable revenue base available to tachometer suppliers.

Light Commercial Vehicles account for 23% of vehicle type demand. Fleet operators and logistics companies specify tachometer systems that support engine efficiency monitoring and regulatory compliance for driver hours and fuel consumption reporting. This application base creates sustained replacement demand independent of consumer vehicle sales cycles, providing suppliers a more stable revenue channel than the passenger car segment alone.

Heavy Commercial Vehicles represent 19% of the vehicle type segment. Heavy vehicle programs require durable, vibration-resistant tachometer units capable of operating across extended duty cycles. Fleet monitoring systems increasingly integrate tachometer data with telematics platforms for predictive maintenance, which raises the functional specification and unit value of tachometers deployed in heavy commercial applications.

Application Analysis

OEM dominates with 67.1% due to platform integration and volume production contracts.

In 2025, OEM held a dominant market position in the By Application segment of the Automotive Tachometer Market, with a 67.1% share. OEM supply channels deliver guaranteed volume tied to vehicle production programs, creating predictable revenue streams for nominated suppliers. Platform nominations lock tachometer suppliers into multi-year contracts, creating switching cost advantages that make OEM relationships structurally more defensible than aftermarket positions.

Aftermarket accounts for 32.9% of application demand. The aftermarket channel serves replacement needs across the global installed vehicle base, including aging ICE vehicles, performance tuning applications, and fleet maintenance programs. Data from the Challenges section indicates that traditional tachometer-specific aftermarket volumes in Europe, North America, and Japan face an estimated erosion of 10% to 18% over a five-year horizon as integrated digital clusters reduce individual component replacement cycles.

This erosion risk creates a bifurcation within the aftermarket channel. Suppliers offering plug-and-play digital retrofit kits targeting enthusiast, restoration, and off-road segments are positioned to capture margin-accretive volume that conventional replacement part distributors cannot address. The aftermarket digital retrofit opportunity carries estimated gross margins of 30 to 40% on hardware and 45% or more on vehicle-specific harness accessories.

Key Market Segments

By Display Type

- LED Display

- LCD Display

- Analog Dial

- OLED Display

By Product Type

- Analog Tachometer

- Digital Tachometer

- Hybrid Tachometer

By Technology

- Electromechanical Tachometer

- Solid-State Tachometer

- Digital Signal Processing Tachometer

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Two Wheelers

- Off-Highway Vehicles

By Application

- OEM

- Aftermarket

Drivers

Regulatory requirements now act as a direct catalyst for tachometer and instrument cluster redesigns. In the United States, FMVSS No. 101 governs display identification requirements, while digital clusters must meet broader visibility, telltale, and illumination standards. These compliance requirements force OEM suppliers to upgrade cluster architecture on each new program, raising per-unit content value and creating a sustained engineering spend cycle that benefits technically capable suppliers.

In Europe and the UK, UNECE R155 applied to new vehicle type approvals from July 2022 and extended to all existing vehicle types by July 2024, with additional compliance milestones extending into 2026. These regulations require cybersecurity management systems, secure software update mechanisms, and lifecycle risk management for cluster control units. Suppliers with established software validation and cybersecurity integration capabilities gain a structural pricing advantage as compliance complexity raises barriers for commodity competitors.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital cluster adoption in mass-market vehicles | +1.6% | China core, EU, India, North America | Short term |

| EV and hybrid powertrain mix expansion | +1.4% | China core, EU core, North America, India spill-over | Medium term |

| Premiumization of cockpit electronics in SUVs and upper trims | +1.1% | India, China, North America, GCC, ASEAN urban markets | Short term |

| Compliance-led redesign under display, telltale and cyber rules | +0.9% | EU, UK, North America, Japan, Korea | Medium term |

| Rising global vehicle output with Asia-led manufacturing concentration | +1.3% | China core, India core, ASEAN, Mexico, Morocco spill-over | Short term |

| Software-defined cockpit upgrades and OTA-enabled feature refresh | +0.8% | EU, China, North America, Korea premium OEM base | Long term |

Restraints

Aftermarket replacement demand for standalone tachometer components faces structural erosion in developed markets. As software-managed digital clusters proliferate, independent repairability declines and replacement cycles stretch. This dynamic reduces traditional tachometer-specific aftermarket volumes by an estimated 10% to 18% over a five-year horizon in Europe, North America, and Japan, weakening the annuity revenue stream that specialist component vendors and distributors rely on to offset OEM program cyclicality.

The commercial consequence extends beyond volume loss. Distributors face lower channel velocity, and component vendors lose the cushioning that aftermarket revenue historically provided against primary market downturns. Whole-cluster swap logic replacing individual tachometer servicing also concentrates repair revenue at dealerships and integrated cluster suppliers, structurally excluding independent aftermarket distributors from a growing share of the service-part value chain.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital cockpit substitution | -1.2% | EU, North America, Japan, Korea, China urban OEM hubs | Medium term |

| Semiconductor lead-time risk | -1.0% | Global, APAC supply corridors, EU assembly belts | Short term |

| Cybersecurity compliance burden | -0.9% | EU, UK, Japan, Korea, Australia | Medium term |

| Tariff-led electronics inflation | -0.8% | North America core, China-linked supply chains, EU exporters | Short term |

| Vehicle production mix imbalance | -0.7% | Europe core, mature North America, premium OEM clusters | Medium term |

| Aftermarket replacement erosion | -0.6% | EU, North America, Japan | Long term |

Challenges

Cybersecurity validation now imposes a recurring engineering cost on tachometer and cluster suppliers operating in UNECE-regulated markets. UNECE R155 and R156 require cybersecurity management, secure software updating, risk monitoring, incident response, and protected OTA processes for type approval. Even where the tachometer display itself is relatively simple, the embedded software chain, authentication layers, code-signing, and hardware security integration add months of validation activity before start of production.

The commercial effect compounds across multi-region programs. Development calendars can stretch by 8 to 16 weeks, and cybersecurity assurance can consume low-to-mid single-digit percentages of electronics development budgets. Smaller suppliers that previously competed on electromechanical competence now require sustained software compliance teams, secure update infrastructure, and cross-functional documentation discipline to remain nominated on global vehicle platforms, raising minimum viable scale for market participation.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Mature-node chip tightness | -1.1% | APAC fabs; EU plants; North America OEM base | Medium term (2-4 years) |

| Cockpit architecture migration | -0.9% | North America premium; EU regulatory hubs; China, Japan, Korea | Medium term (2-4 years) |

| Cybersecurity validation burden | -0.7% | EU core; UK; UNECE-aligned export programs | Medium term (2-4 years) |

| Regional production instability | -0.8% | Europe core; Americas assembly belts; APAC export corridors | Short term (≤ 2 years) |

| Engineering talent bottlenecks | -0.6% | EU industrial clusters; U.S. manufacturing belt; advanced APAC hubs | Long term (≥ 4 years) |

| Aftermarket calibration complexity | -0.4% | Latin America; Southeast Asia; Middle East and Africa; aging-vehicle markets | Long term (≥ 4 years) |

Opportunities

The global installed base of older vehicles with analog or semi-digital instrument clusters represents a commercially underserved segment for suppliers capable of delivering plug-and-play digital tachometer retrofit kits. These kits integrate digital displays, CAN translators, mobile calibration applications, and compliance-ready warning indicators, targeting enthusiast, restoration, off-road, and light-commercial applications outside the conventional OEM replacement cycle.

The retrofit business model generates hardware gross margins of 30 to 40% and vehicle-specific harness accessory margins of 45% or more. Unlike traditional OEM supply volumes, retrofit demand is not tied to new vehicle production programs. Advances in digital display technology now allow a single core platform to support dozens of vehicle models, creating a scalable pathway for suppliers to extract value from the installed vehicle base without new program nomination requirements.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Software-defined tachometer UX | +1.4% | North America, EU, China, Japan, Korea | Short term |

| Aftermarket digital retrofit kits | +2.1% | North America core, EU, India, ASEAN, LATAM | Short term |

| 2W / powersports adjacency | +1.8% | India, China, ASEAN, Latin America | Medium term |

| Fleet tachometer telemetry bundles | +1.2% | North America, EU, GCC, APAC logistics hubs | Medium term |

| EV performance and energy gauges | +1.6% | China, EU, North America, premium APAC | Medium term |

| Cockpit platform roll-up M&A | +2.4% | Global, with APAC manufacturing base | Long term |

Regional Analysis

Asia-Pacific Dominates the Automotive Tachometer Market with a Market Share of 41.3%, Valued at USD 5.95 Billion

Asia-Pacific leads the global automotive tachometer market through concentrated vehicle manufacturing in China, Japan, South Korea, India, and ASEAN production corridors. The region’s 41.3% share reflects its position as the world’s largest vehicle production base. China alone drives demand for both mass-market digital clusters and premium cockpit electronics, while India’s rising vehicle output adds sustained volume to the regional supply chain.

North America holds the second-largest regional position, supported by high-volume passenger car and light truck production and strong aftermarket activity across the United States and Canada. FMVSS No. 101 compliance requirements drive cluster redesign spending among OEM suppliers serving North American programs. In March 2026, Marelli announced more than 20 new automotive technologies for Auto China 2026, including next-generation cockpit electronics relevant to instrument cluster applications, reflecting supplier focus on multi-region platform strategies.

Europe sustains tachometer demand through its premium vehicle manufacturing base in Germany, France, the UK, Spain, and Italy. Data from ACEA shows new EU passenger car registrations reached approximately 10.6 million units in 2024. UNECE R155 and R156 compliance obligations across this production volume force cluster architecture upgrades, directly increasing tachometer module content value and benefiting suppliers with established cybersecurity and software validation capabilities.

Latin America and the Middle East and Africa remain smaller regional markets but contribute incremental demand through commercial vehicle fleet growth and aftermarket replacement activity. These regions rely heavily on ICE powertrains, which sustains conventional tachometer demand over a longer horizon than mature markets transitioning to electrified vehicles. Aftermarket retrofit opportunities in these regions are particularly relevant given their large installed base of aging vehicles.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

Robert Bosch GmbH maintains a broad competitive position across multiple automotive electronics segments, including instrument cluster systems and tachometer modules. Bosch’s integration of functional safety, cybersecurity compliance, and software-defined cockpit capabilities positions it to meet UNECE R155 and FMVSS requirements simultaneously. This cross-market compliance infrastructure raises the supplier’s value to OEMs managing multi-region vehicle programs and reduces platform re-nomination risk. Figures from ACEA show electrified vehicles represented 57.7% of December 2024 EU passenger vehicle registrations, reinforcing demand for cluster systems that display both RPM and energy management data.

Continental AG competes through its integrated cockpit electronics platform, combining display hardware, software stacks, and sensor systems within unified cluster architectures. In January 2025, Garmin launched Unified Cabin 2025, expanding its digital cockpit platform with support for up to six integrated screens, illustrating the competitive pressure tier-one suppliers like Continental face from electronics-focused challengers entering the instrument cluster space. Continental’s scale in display manufacturing and its OEM program depth across Europe, China, and North America provide structural resilience, but the Garmin move signals that software-native players are targeting the same cockpit real estate.

Key Players

- Robert Bosch GmbH

- Continental AG

- Nippon Seiki Co. Ltd.

- DENSO Corporation

- Aptiv PLC

- Honeywell International Inc.

- Magneti Marelli S.p.A.

- Yazaki Corporation

- Garmin Ltd.

- Stoneridge, Inc.

- Maxi Display Technologies

- Mitsuba Corporation

- Kienzle Automotive Systeme GmbH

- Lucas Automotive

Recent Developments

- January 2026 – Visteon showcased its next-generation SmartCore HPC cockpit domain controller at CES 2026, delivering up to 700 TOPS of computing performance for digital instrument clusters and multi-display cockpit systems.

- May 2026 – Visteon and Smart Eye launched an LCD instrument cluster with integrated driver-monitoring technology, embedding eye-tracking and driver-attention analytics directly into the cluster display.

- May 2026 – Mercedes-Benz initiated a recall affecting more than 144,000 vehicles due to software faults that could cause digital instrument clusters to temporarily go blank, highlighting the importance of software-defined tachometer and gauge system validation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.4 Billion |

| Forecast Revenue (2035) | USD 29.7 Billion |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Display Type (LED Display, LCD Display, Analog Dial, OLED Display), By Product Type (Analog Tachometer, Digital Tachometer, Hybrid Tachometer), By Technology (Electromechanical Tachometer, Solid-State Tachometer, Digital Signal Processing Tachometer), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two Wheelers, Off-Highway Vehicles), By Application (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Robert Bosch GmbH, Continental AG, Nippon Seiki Co. Ltd., DENSO Corporation, Aptiv PLC, Honeywell International Inc., Magneti Marelli S.p.A., Yazaki Corporation, Garmin Ltd., Stoneridge, Inc., Maxi Display Technologies, Mitsuba Corporation, Kienzle Automotive Systeme GmbH, Lucas Automotive |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |