Global Automotive Ignition System Market Size, Share, Growth Analysis By Type (Distributor Ignition System, Distributor-less ignition System, Coil-on-Plug Ignition System, Magneto Ignition System), By Component (Ignition Switch, Spark Plug, Glow Plug, Ignition Coil, Others), By Fuel Type (Gasoline, Diesel, Natural Gas, Ethanol), By Technology (Electronic Ignition System, Conventional Ignition System, Smart ignition System, Advanced Ignition System), By Vehicle Type (Passenger Car, Commercial Vehicle, Two-Wheeler, Heavy-Duty Vehicle), By Application (Spark Ignition, Compression Ignition, Gas Ignition, Dual Fuel Ignition), By Sales Channel (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Jan 2026

- Report ID: 174646

- Number of Pages: 299

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Type Analysis

- Component Analysis

- Fuel Type Analysis

- Technology Analysis

- Vehicle Type Analysis

- Application Analysis

- Sales Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Automotive Ignition System Company Insights

- Key Companies

- Recent Developments

- Report Scope

Report Overview

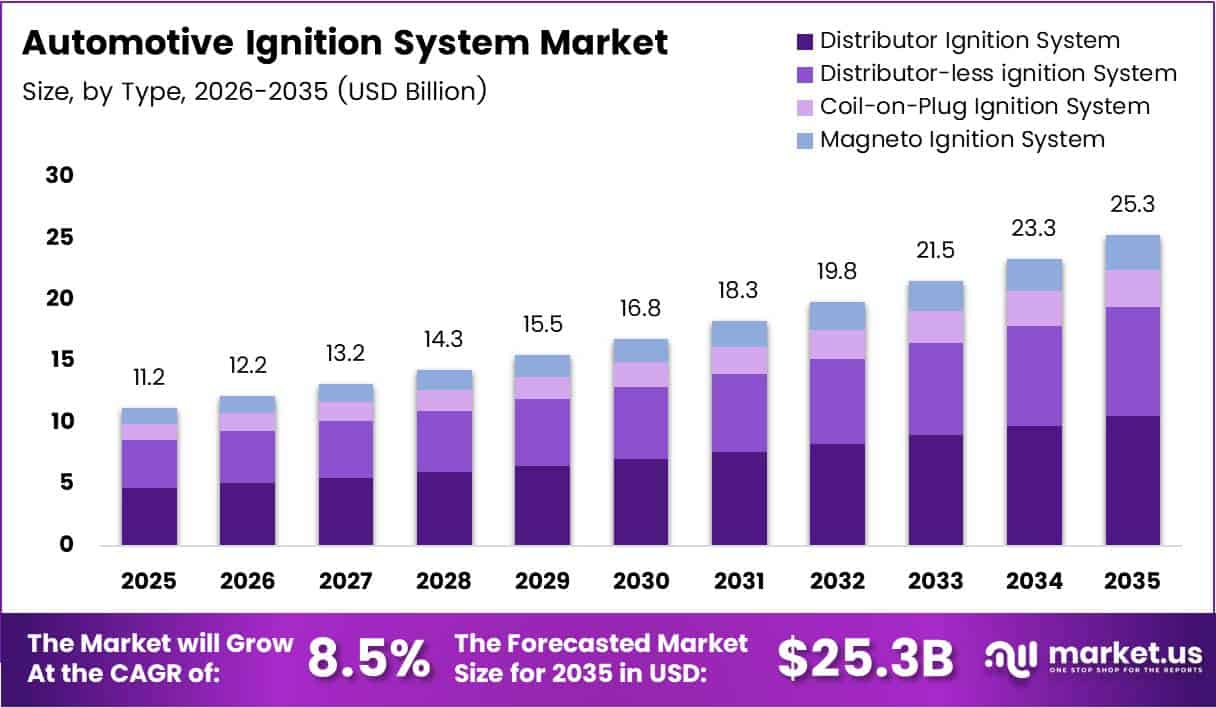

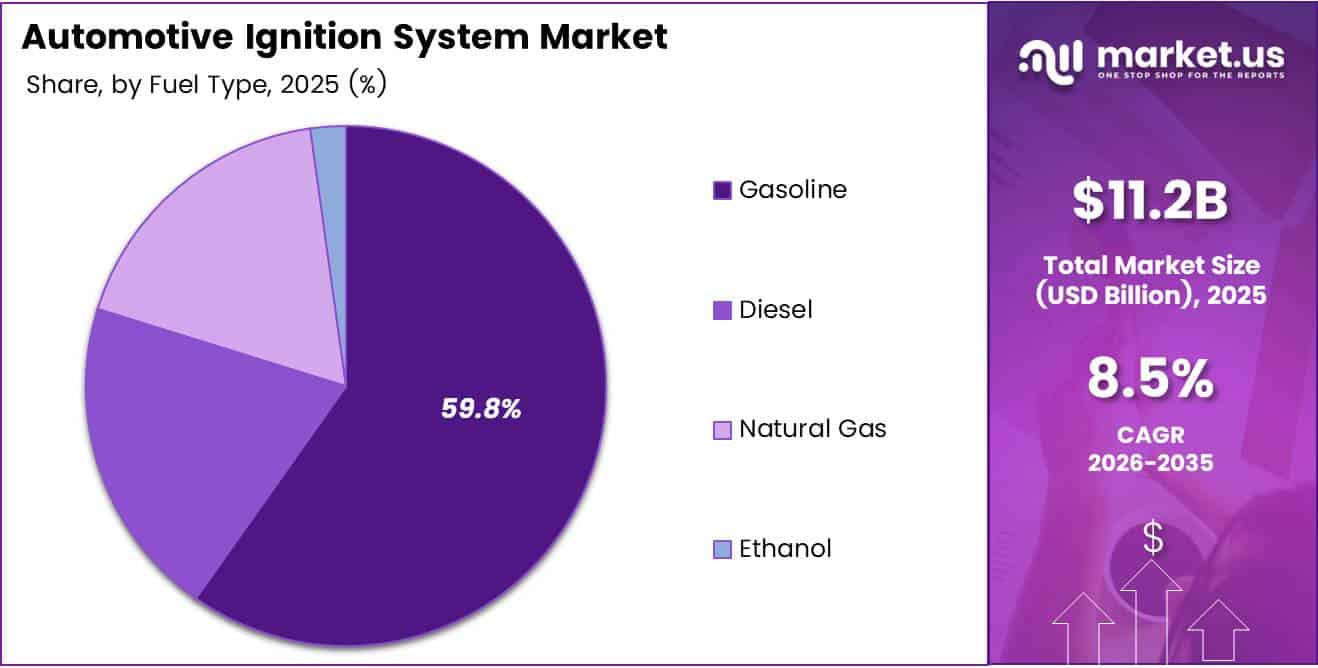

Global Automotive Ignition System Market size is expected to be worth around USD 25.3 Billion by 2035 from USD 11.2 Billion in 2025, growing at a CAGR of 8.5% during the forecast period 2026 to 2035.

Automotive ignition systems are critical components that initiate combustion in internal combustion engines. These systems generate high-voltage electrical sparks to ignite the air-fuel mixture, enabling engine operation. Moreover, they encompass various technologies including distributor-based, distributor-less, and coil-on-plug configurations.

The automotive ignition system market serves as the backbone of conventional vehicle powertrains. Consequently, it supports millions of gasoline, diesel, and alternative fuel vehicles globally. Additionally, the market includes both original equipment manufacturer channels and robust aftermarket services for maintenance and replacement needs.

Market growth is driven by rising global production of gasoline-powered passenger vehicles. Furthermore, increasing demand for fuel-efficient and high-performance engines accelerates innovation. However, the rapid shift toward battery electric vehicles presents notable challenges for traditional ignition system manufacturers seeking sustainable growth trajectories.

Advanced electronic ignition technologies are gaining widespread adoption across vehicle segments. Therefore, manufacturers are investing heavily in research and development initiatives. Additionally, integration with engine management systems and IoT platforms enhances diagnostic capabilities and operational efficiency significantly.

Government regulations emphasizing emission control and fuel efficiency standards boost market expansion. Consequently, automakers prioritize advanced ignition technologies to meet stringent compliance requirements. Moreover, emerging economies demonstrate substantial growth potential due to expanding vehicle ownership and increasing urbanization rates across developing regions.

According to MDPI research, spark plug replacement intervals for latest ignition systems have extended from 20,000 km to 120,000 km. This technological advancement significantly reduces maintenance costs and enhances consumer value proposition. Additionally, it reflects continuous innovation in materials science and component durability within the automotive ignition system industry.

Key Takeaways

- Global Automotive Ignition System Market valued at USD 11.2 Billion in 2025, projected to reach USD 25.3 Billion by 2035 at 8.5% CAGR

- Asia Pacific dominates with 37.3% market share, valued at USD 4.1 Billion

- Distributor Ignition System leads Type segment with 39.4% market share

- Spark Plug dominates Component segment holding 31.2% share

- Gasoline Fuel Type commands largest share at 59.8%

- Electronic Ignition System captures 43.1% of Technology segment

- Passenger Car leads Vehicle Type segment with 49.9% share

- Spark Ignition dominates Application segment at 56.60%

- OEM Sales Channel holds dominant position with 69.3% market share

Type Analysis

Distributor Ignition System dominates with 39.4% due to its widespread adoption in conventional vehicles.

In 2025, Distributor Ignition System held a dominant market position in the By Type Analysis segment of Automotive Ignition System Market, with a 39.4% share. This traditional system remains prevalent in older vehicle models and cost-sensitive markets. Moreover, its simplicity and ease of maintenance contribute to sustained demand across developing economies globally.

Distributor-less Ignition System represents advanced technology eliminating mechanical distribution components. This configuration enhances reliability by reducing moving parts prone to wear. Additionally, it improves ignition timing precision and engine performance. Consequently, modern vehicles increasingly adopt this technology for superior fuel efficiency and reduced emissions compliance.

Coil-on-Plug Ignition System delivers direct spark energy to individual cylinders. This design maximizes combustion efficiency while minimizing energy loss during transmission. Furthermore, it enables precise cylinder-specific ignition control. Therefore, premium and performance vehicles extensively utilize this technology for optimal power delivery and enhanced engine responsiveness characteristics.

Magneto Ignition System operates independently without battery power requirements. This self-contained configuration proves ideal for small engines and aviation applications. Moreover, it demonstrates exceptional reliability in remote or extreme operating conditions. Consequently, specialized vehicle segments and industrial equipment continue valuing this proven ignition technology solution.

Component Analysis

Spark Plug dominates with 31.2% owing to universal application across gasoline engines.

In 2025, Spark Plug held a dominant market position in the By Component Analysis segment of Automotive Ignition System Market, with a 31.2% share. These components generate critical sparks for fuel ignition in combustion chambers. Additionally, frequent replacement requirements ensure consistent aftermarket demand. Therefore, spark plugs represent the highest-volume component within automotive ignition systems globally.

Ignition Switch serves as the primary control interface for engine starting operations. This component enables electrical circuit activation and vehicle security functions. Moreover, modern switches integrate advanced features including keyless entry and push-button start. Consequently, technological evolution drives continuous product development and replacement cycles within this component category.

Glow Plug facilitates cold-start operations specifically in diesel engine applications. This heating element preheats combustion chambers enabling reliable ignition. Furthermore, cold climate regions demonstrate particularly high demand for quality glow plugs. Therefore, seasonal replacement patterns and durability requirements significantly influence this specialized component market segment.

Ignition Coil transforms battery voltage into high-voltage electrical energy for spark generation. This electromagnetic device proves critical for consistent ignition performance. Additionally, advanced coil designs enhance energy efficiency and component longevity. Consequently, premium vehicle segments increasingly adopt sophisticated ignition coil technologies for superior engine management capabilities.

Others category encompasses auxiliary components including wiring harnesses and control modules. These supporting elements ensure system integration and operational reliability. Moreover, diagnostic sensors and electronic control units enhance modern ignition system functionality. Therefore, this segment reflects growing complexity in contemporary automotive electrical architectures.

Fuel Type Analysis

Gasoline dominates with 59.8% reflecting global preference for petrol-powered vehicles.

In 2025, Gasoline held a dominant market position in the By Fuel Type Analysis segment of Automotive Ignition System Market, with a 59.8% share. Gasoline engines require spark ignition systems for combustion initiation processes. Moreover, widespread availability and established infrastructure support continued gasoline vehicle production. Consequently, this fuel type maintains the largest ignition system market share globally.

Diesel fuel type utilizes compression ignition requiring specialized glow plug systems. These engines dominate commercial vehicle and heavy-duty applications worldwide. Additionally, diesel powertrains offer superior fuel economy for long-distance transportation. Therefore, this segment maintains steady demand despite increasing electrification trends in passenger vehicle categories.

Natural Gas represents an environmentally friendly alternative fuel gaining adoption. These vehicles require specialized ignition components for gaseous fuel combustion. Furthermore, government incentives promote natural gas vehicle deployment in urban areas. Consequently, this segment demonstrates promising growth potential in regions prioritizing emission reduction and air quality improvement.

Ethanol-blended fuels require ignition systems compatible with corrosive fuel characteristics. This renewable fuel option reduces petroleum dependence and carbon emissions. Moreover, agricultural economies actively promote ethanol production and consumption. Therefore, flex-fuel capable ignition systems address growing demand for sustainable transportation solutions.

Technology Analysis

Electronic Ignition System dominates with 43.1% due to superior performance and reliability.

In 2025, Electronic Ignition System held a dominant market position in the By Technology Analysis segment of Automotive Ignition System Market, with a 43.1% share. Electronic control enables precise ignition timing optimization across operating conditions. Additionally, solid-state components eliminate mechanical wear and maintenance requirements. Consequently, modern vehicles predominantly feature electronic ignition technologies for enhanced efficiency and durability.

Conventional Ignition System relies on mechanical breaker points for timing control. This traditional technology remains present in older vehicles and classic car applications. Moreover, its simplicity enables cost-effective repairs in resource-limited markets. Therefore, vintage vehicle restoration and developing economy segments sustain demand for conventional ignition system components.

Smart Ignition System integrates advanced diagnostics and adaptive control algorithms. These intelligent systems optimize combustion parameters based on real-time sensor data. Furthermore, connectivity features enable remote monitoring and predictive maintenance capabilities. Consequently, premium vehicle manufacturers increasingly adopt smart ignition technologies for differentiated customer experiences.

Advanced Ignition System incorporates cutting-edge technologies including plasma and laser ignition. These innovative approaches enhance combustion efficiency beyond conventional spark ignition limits. Moreover, they enable ultra-lean fuel mixtures for superior emission performance. Therefore, research and development investments focus on commercializing advanced ignition solutions for future powertrains.

Vehicle Type Analysis

Passenger Car dominates with 49.9% reflecting largest vehicle production volumes globally.

In 2025, Passenger Car held a dominant market position in the By Vehicle Type Analysis segment of Automotive Ignition System Market, with a 49.9% share. Personal transportation vehicles constitute the majority of global automobile production. Additionally, diverse model variants require extensive ignition system applications. Consequently, passenger cars represent the primary demand driver for automotive ignition system manufacturers worldwide.

Commercial Vehicle segment includes light and medium-duty trucks for business applications. These vehicles require robust ignition systems for demanding operational conditions. Moreover, fleet replacement cycles ensure consistent aftermarket component demand. Therefore, commercial vehicle applications provide stable revenue streams for ignition system suppliers across regional markets.

Two-Wheeler category encompasses motorcycles and scooters with compact ignition requirements. These vehicles dominate personal mobility in densely populated Asian markets. Furthermore, cost-sensitive consumers prioritize affordable and reliable ignition components. Consequently, two-wheeler ignition systems emphasize durability and value proposition in emerging economy segments.

Heavy-Duty Vehicle applications demand industrial-grade ignition components for extreme conditions. These vehicles operate in construction, mining, and long-haul transportation sectors. Additionally, extended maintenance intervals require premium component quality and longevity. Therefore, heavy-duty ignition systems command higher margins despite lower volume compared to passenger vehicle applications.

Application Analysis

Spark Ignition dominates with 56.60% serving majority of gasoline engine applications.

In 2025, Spark Ignition held a dominant market position in the By Application Analysis segment of Automotive Ignition System Market, with a 56.60% share. This combustion method powers most passenger vehicles and light-duty applications globally. Moreover, continuous technological improvements enhance spark ignition efficiency and emission performance. Consequently, this application maintains leadership position despite emerging alternative powertrain technologies.

Compression Ignition application serves diesel engine vehicles through glow plug systems. This method provides superior thermal efficiency for heavy-duty and commercial applications. Additionally, compression ignition engines deliver exceptional torque characteristics for load-carrying operations. Therefore, this application remains critical for transportation and industrial vehicle segments worldwide.

Gas Ignition systems enable natural gas and LPG-powered vehicle operation. These applications reduce greenhouse gas emissions compared to conventional liquid fuels. Furthermore, government policies increasingly favor gaseous fuel adoption in urban areas. Consequently, gas ignition systems demonstrate accelerating growth in environmentally conscious markets and fleet operations.

Dual Fuel Ignition technology enables flexible operation across multiple fuel types. This innovative application maximizes operational versatility and energy security. Moreover, it allows optimization based on fuel availability and cost considerations. Therefore, dual fuel capable ignition systems attract interest from commercial operators seeking operational flexibility.

Sales Channel Analysis

OEM dominates with 69.3% driven by new vehicle production requirements.

In 2025, OEM held a dominant market position in the By Sales Channel Analysis segment of Automotive Ignition System Market, with a 69.3% share. Original equipment manufacturers integrate ignition systems during initial vehicle assembly processes. Additionally, automaker specifications drive innovation and quality standards across the industry. Consequently, OEM channel represents the primary revenue source for tier-one ignition system suppliers globally.

Aftermarket sales channel serves replacement and maintenance demand for existing vehicle populations. This segment provides essential components for aging vehicles requiring ignition system repairs. Moreover, independent repair facilities and vehicle owners rely on aftermarket availability. Therefore, aftermarket distribution networks ensure continued vehicle operability and generate recurring revenue streams for component manufacturers.

Key Market Segments

By Type

- Distributor Ignition System

- Distributor-less ignition System

- Coil-on-Plug Ignition System

- Magneto Ignition System

By Component

- Ignition Switch

- Spark Plug

- Glow Plug

- Ignition Coil

- Others

By Fuel Type

- Gasoline

- Diesel

- Natural Gas

- Ethanol

By Technology

- Electronic Ignition System

- Conventional Ignition System

- Smart ignition System

- Advanced Ignition System

By Vehicle Type

- Passenger Car

- Commercial Vehicle

- Two-Wheeler

- Heavy-Duty Vehicle

By Application

- Spark Ignition

- Compression Ignition

- Gas Ignition

- Dual Fuel Ignition

By Sales Channel

- OEM

- Aftermarket

Drivers

Rising Global Production of Gasoline-Powered Passenger Vehicles Drives Market Growth

Global automotive manufacturing continues expanding with increasing consumer demand for personal transportation. Consequently, gasoline-powered vehicles require sophisticated ignition systems for optimal engine performance. Moreover, emerging markets demonstrate accelerating vehicle adoption rates. Therefore, production volume growth directly translates to heightened ignition system demand across all component categories and technology segments.

Developing economies witness rapid urbanization and rising middle-class populations. Additionally, infrastructure improvements enable greater vehicle ownership accessibility. Furthermore, affordable gasoline vehicle models attract first-time buyers. Consequently, manufacturers scale production capacity to meet regional demand, creating sustained ignition system market expansion opportunities.

Fuel-efficient and high-performance engines necessitate advanced ignition technologies. Moreover, stringent emission regulations compel automakers to optimize combustion processes. Additionally, consumer expectations for reliability and durability increase continuously. Therefore, electronic ignition systems with precise timing control become standard equipment across modern vehicle platforms globally.

Advanced electronic ignition technologies enhance engine efficiency and reduce harmful emissions. Furthermore, integration with engine management systems enables real-time optimization. Additionally, diagnostic capabilities improve maintenance scheduling and component longevity. Consequently, OEM adoption of sophisticated ignition technologies accelerates, driving premium product segment growth and innovation investment.

Restraints

Rapid Shift Toward Battery Electric Vehicles Challenges Traditional Ignition System Demand

Electric vehicle adoption accelerates globally, eliminating ignition system requirements entirely. Consequently, long-term market growth faces significant structural challenges. Moreover, government incentives and environmental regulations favor battery electric powertrains. Therefore, traditional ignition system manufacturers must adapt strategies to address declining addressable market size in passenger vehicle segments.

Automakers commit substantial investments toward electric vehicle development and production capacity. Additionally, charging infrastructure expansion reduces range anxiety barriers. Furthermore, battery technology improvements enhance electric vehicle competitiveness. Consequently, gasoline vehicle production growth rates decelerate in developed markets, constraining ignition system demand expansion potential significantly.

Advanced ignition components incorporate sophisticated materials and electronic controls. Moreover, precision manufacturing requirements increase production costs substantially. Additionally, integration complexity demands extensive testing and validation processes. Therefore, price-sensitive market segments resist premium ignition system adoption, limiting penetration of innovative technologies in cost-competitive vehicle categories.

Research and development expenditures for advanced ignition technologies require substantial capital investment. Furthermore, component suppliers face margin pressures from competitive pricing dynamics. Additionally, system integration demands collaboration across multiple engineering disciplines. Consequently, smaller manufacturers struggle to maintain technology leadership, resulting in market consolidation and reduced innovation diversity.

Growth Factors

Development of Smart Ignition Coils with Integrated Diagnostics Creates New Market Opportunities

Smart ignition technologies incorporate sensors and microprocessors for real-time performance monitoring. Consequently, predictive maintenance capabilities reduce unexpected vehicle failures. Moreover, diagnostic data enables optimized service scheduling and component replacement. Therefore, connected vehicle platforms increasingly integrate smart ignition systems, creating premium product segment growth opportunities for technology leaders.

Hybrid vehicles combine electric and combustion powertrains requiring specialized ignition solutions. Additionally, these vehicles demand seamless transitions between power sources. Furthermore, efficiency optimization across operating modes proves critical for consumer acceptance. Consequently, hybrid ignition system development represents significant growth opportunity as manufacturers expand electrified vehicle portfolios globally.

Emerging economies demonstrate rapidly expanding vehicle populations requiring maintenance services. Moreover, aging vehicle fleets necessitate frequent ignition component replacement. Additionally, growing service networks improve aftermarket product accessibility. Therefore, replacement demand in developing markets provides sustained revenue growth opportunities independent of new vehicle production cycles.

Modern vehicles integrate ignition systems with comprehensive engine management platforms. Additionally, IoT connectivity enables remote diagnostics and software updates. Furthermore, data analytics optimize combustion parameters for efficiency improvements. Consequently, integrated ignition solutions command premium pricing while enhancing overall vehicle performance, creating differentiated value propositions for technology-forward manufacturers.

Emerging Trends

Adoption of Distributor-Less Ignition Systems Transforms Industry Standards

Distributor-less ignition systems eliminate mechanical components prone to wear and failure. Consequently, reliability improvements reduce maintenance requirements and ownership costs. Moreover, electronic control enables superior ignition timing precision across operating conditions. Therefore, modern vehicle platforms universally adopt distributor-less configurations, rendering traditional distributor systems obsolete in new production.

Laser-based and plasma ignition technologies represent cutting-edge combustion initiation methods. Additionally, these advanced approaches enable ultra-lean fuel mixtures for emission reduction. Furthermore, they demonstrate superior performance in challenging operating environments. Consequently, research initiatives focus on commercialization pathways despite current cost and complexity barriers limiting widespread adoption.

Component manufacturers prioritize weight reduction and compact packaging for improved vehicle efficiency. Moreover, advanced materials enable smaller form factors without performance compromise. Additionally, miniaturization supports engine downsizing trends across automotive industry. Therefore, next-generation ignition components deliver equivalent or superior performance in significantly reduced physical footprints and weights.

Long-life spark plugs utilize precious metal electrodes and advanced ceramic insulators. Additionally, these components extend replacement intervals beyond 100,000 km in modern applications. Furthermore, durability improvements reduce total ownership costs and environmental impact. Consequently, premium long-life ignition components gain market share despite higher initial costs, reflecting consumer preference for reduced maintenance frequency.

Regional Analysis

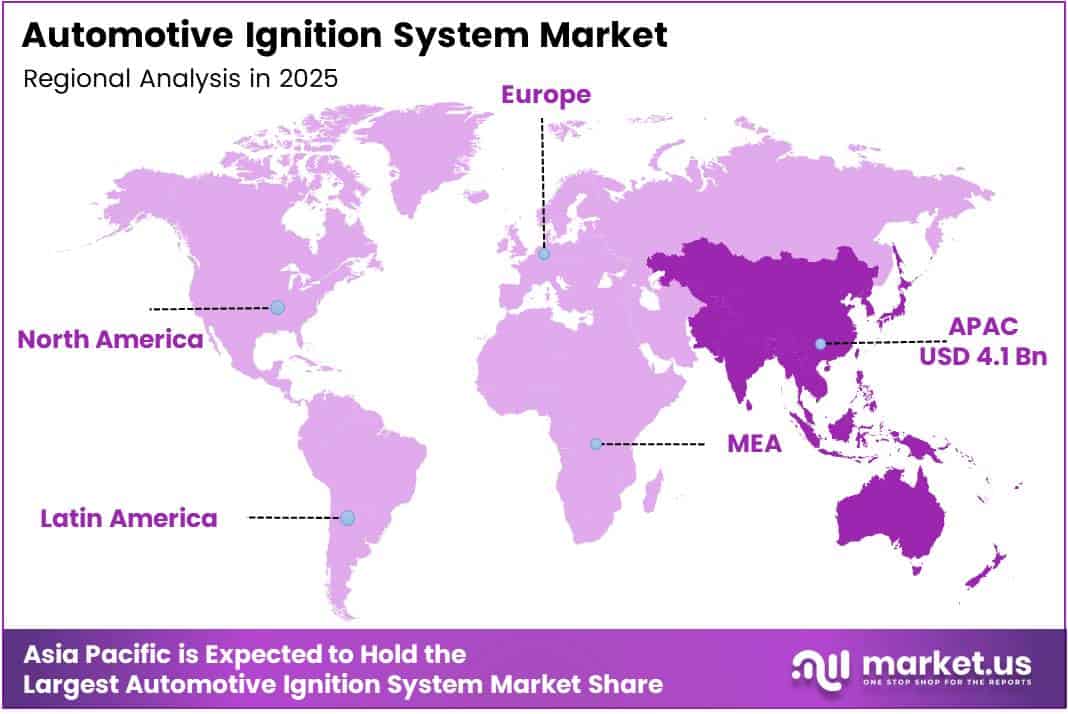

Asia Pacific Dominates the Automotive Ignition System Market with a Market Share of 37.3%, Valued at USD 4.1 Billion

Asia Pacific commands the largest automotive ignition system market share at 37.3%, valued at USD 4.1 Billion. This regional dominance reflects massive vehicle production concentrated in China, Japan, South Korea, and India. Moreover, rapid economic development drives accelerating vehicle ownership rates. Additionally, established automotive manufacturing ecosystems support comprehensive supply chain capabilities. Consequently, Asia Pacific remains the primary growth engine for global ignition system demand.

North America Automotive Ignition System Market Trends

North America represents a mature market characterized by advanced technology adoption and premium vehicle preferences. Moreover, stringent emission regulations drive continuous innovation in ignition system performance. Additionally, extensive aftermarket networks support robust replacement component demand. Therefore, the region maintains significant market value despite lower growth rates compared to emerging economies.

Europe Automotive Ignition System Market Trends

Europe demonstrates strong demand for fuel-efficient powertrains and environmental compliance technologies. Additionally, premium automotive manufacturers concentrate in Germany, France, and Italy. Furthermore, diesel engine applications maintain substantial market presence in commercial segments. Consequently, European ignition system markets emphasize quality, performance, and regulatory compliance over volume growth.

Middle East and Africa Automotive Ignition System Market Trends

Middle East and Africa exhibit growing vehicle markets driven by infrastructure development and urbanization. Moreover, harsh operating conditions necessitate durable ignition components. Additionally, expanding dealer and service networks improve product accessibility. Therefore, the region presents emerging growth opportunities despite current smaller market size compared to established regions.

Latin America Automotive Ignition System Market Trends

Latin America experiences steady automotive market growth concentrated in Brazil and Mexico. Additionally, cost-sensitive consumers prioritize value and reliability. Furthermore, local manufacturing capabilities support regional supply chains. Consequently, Latin American markets favor proven ignition technologies over premium advanced solutions, emphasizing affordability and serviceability.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Automotive Ignition System Company Insights

Robert Bosch GmbH maintains global leadership in automotive ignition system technologies through comprehensive product portfolios. The company delivers advanced electronic ignition solutions across passenger and commercial vehicle segments. Moreover, extensive research and development capabilities drive continuous innovation in efficiency and emission reduction. Additionally, established OEM relationships ensure consistent market presence. Consequently, Bosch remains the primary technology benchmark for ignition system performance standards worldwide.

Denso Corporation represents a major Japanese tier-one supplier with strong presence in Asian markets. The company specializes in high-quality spark plugs, ignition coils, and integrated systems. Furthermore, precision manufacturing capabilities deliver exceptional component reliability and longevity. Additionally, strategic partnerships with leading automakers secure stable production volumes. Therefore, Denso maintains competitive positioning through quality differentiation and operational excellence in cost-effective manufacturing.

NGK Spark Plug Co. Ltd. dominates global spark plug markets through specialized expertise and manufacturing scale. The company produces premium ceramic insulators and precious metal electrode technologies. Moreover, extensive aftermarket distribution networks ensure worldwide product availability. Additionally, continuous material science innovations extend component replacement intervals significantly. Consequently, NGK establishes strong brand recognition among consumers and professional technicians across all vehicle segments.

BorgWarner Inc. provides advanced ignition technologies emphasizing performance and efficiency optimization. The company focuses on electronic control systems and integrated powertrain solutions. Furthermore, acquisitions and partnerships expand technological capabilities and market reach. Additionally, hybrid and alternative fuel vehicle applications represent strategic growth priorities. Therefore, BorgWarner positions itself for evolving automotive market dynamics through diversified product offerings and innovation investment.

Key Companies

- BorgWarner Inc.

- Schaeffler Group

- Denso Corporation

- Diamond Electric Mfg. Co. Ltd.

- Tenneco Inc.

- Hitachi Ltd.

- Mitsubishi Electric Corporation

- NGK Spark Plug Co. Ltd.

- Robert Bosch Gmbh

- Valeo

Recent Developments

- In August 2025, PHINIA completed strategic acquisition of SEM, expanding its ignition system component portfolio. This transaction strengthens PHINIA’s market position in aftermarket distribution channels. Moreover, the acquisition provides access to complementary technologies and customer relationships. Consequently, combined operations enhance competitive capabilities across North American and European markets.

- In September 2025, Vertech acquired Corso Systems’ SCADA conversion tools, enhancing industrial automation capabilities. This strategic move supports integration of advanced diagnostic systems with ignition technologies. Additionally, it enables improved manufacturing process control and quality assurance. Therefore, the acquisition positions Vertech for expanded industrial and automotive applications.

- In September 2025, NGK Spark Plug Co. completed new acquisition expanding its technological capabilities. This strategic investment strengthens the company’s research and development resources. Moreover, it provides access to emerging ignition technologies and intellectual property. Consequently, NGK enhances its competitive positioning for next-generation automotive applications and alternative fuel systems.

Report Scope

Report Features Description Market Value (2025) USD 11.2 Billion Forecast Revenue (2035) USD 25.3 Billion CAGR (2026-2035) 8.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Distributor Ignition System, Distributor-less ignition System, Coil-on-Plug Ignition System, Magneto Ignition System), By Component (Ignition Switch, Spark Plug, Glow Plug, Ignition Coil, Others), By Fuel Type (Gasoline, Diesel, Natural Gas, Ethanol), By Technology (Electronic Ignition System, Conventional Ignition System, Smart ignition System, Advanced Ignition System), By Vehicle Type (Passenger Car, Commercial Vehicle, Two-Wheeler, Heavy-Duty Vehicle), By Application (Spark Ignition, Compression Ignition, Gas Ignition, Dual Fuel Ignition), By Sales Channel (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BorgWarner Inc., Schaeffler Group, Denso Corporation, Diamond Electric Mfg. Co. Ltd., Tenneco Inc., Hitachi Ltd., Mitsubishi Electric Corporation, NGK Spark Plug Co. Ltd., Robert Bosch Gmbh, Valeo Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automotive Ignition System MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample

Automotive Ignition System MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BorgWarner Inc.

- Schaeffler Group

- Denso Corporation

- Diamond Electric Mfg. Co. Ltd.

- Tenneco Inc.

- Hitachi Ltd.

- Mitsubishi Electric Corporation

- NGK Spark Plug Co. Ltd.

- Robert Bosch Gmbh

- Valeo

Our Clients

- 174646

- Jan 2026