Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Ingredient Analysis

- Nature and Formulation Analysis

- Distribution Channel Analysis

- Price Range and Tier Analysis

- End User Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

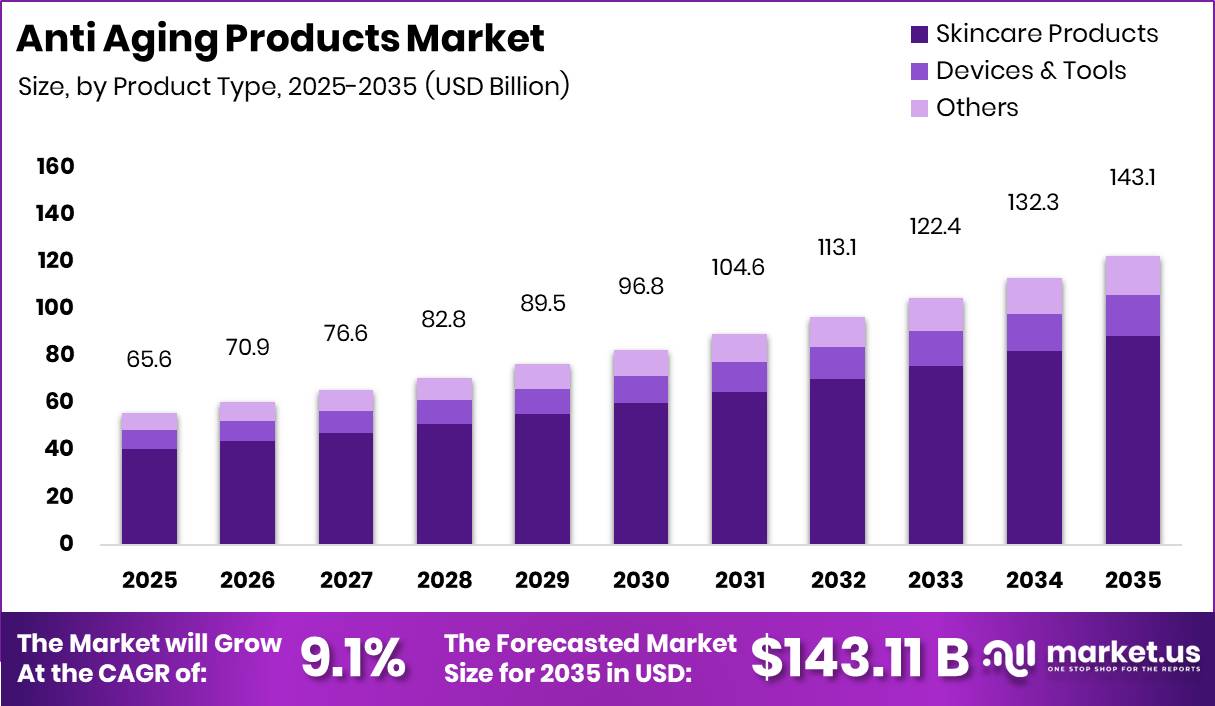

Global Anti Aging Products Market size is expected to be worth around USD 143.11 Billion by 2035 from USD 65.57 Billion in 2025, growing at a CAGR of 9.1% during the forecast period 2026 to 2035. This trajectory signals sustained consumer investment in dermatology backed skincare routines worldwide.

Therefore, the anti aging products market spans skincare, hair care, body care, devices, and tools designed to reduce visible signs of aging. The category combines topical formulations, ingestible products, injectable treatments, and device based solutions sold through offline and online retail networks. This structure lets brands serve multiple price tiers and care needs simultaneously.

Key Takeaways

- The Anti Aging Products Market is valued at USD 65.57 Billion in 2025 and is projected to reach USD 143.11 Billion by 2035.

- The market is set to expand at a CAGR of 9.1% between 2026 and 2035.

- Skincare Products dominate the By Product Type segment with a 62.00% share.

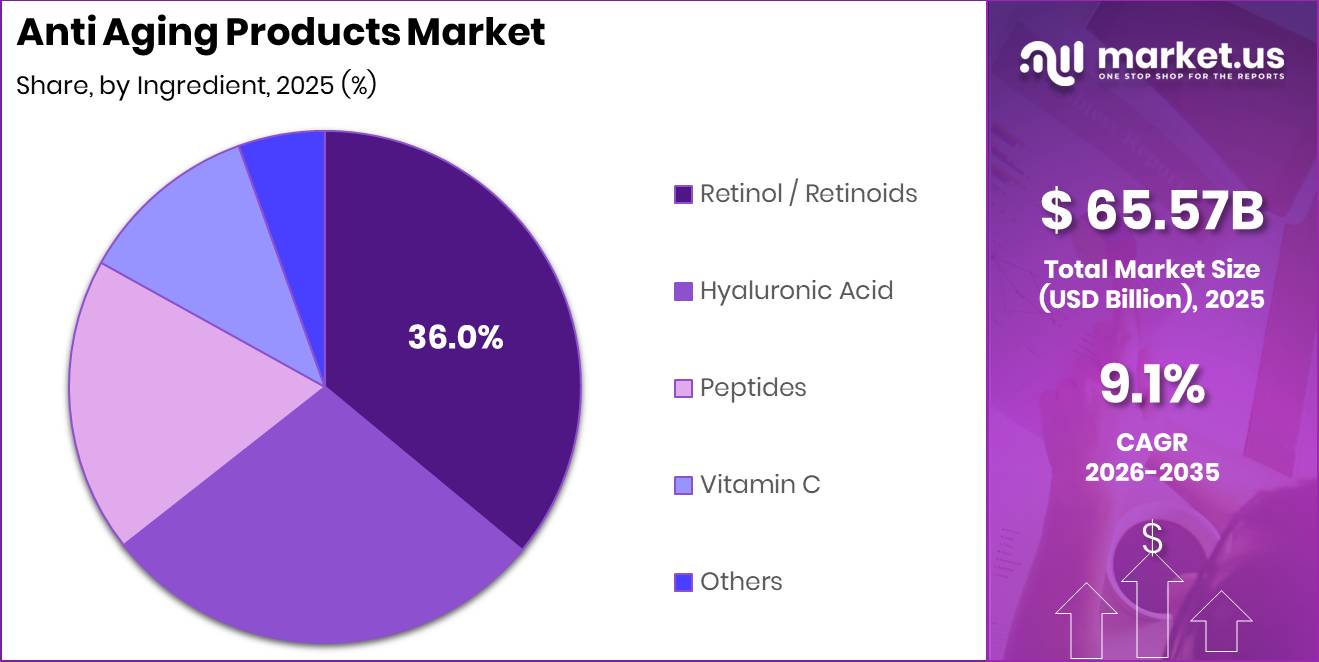

- Retinol and Retinoids lead the By Ingredient segment with a 36.00% share.

- Conventional and Synthetic formulations hold 76.88% of the By Nature and Formulation segment.

- Offline channels account for 68.00% of the By Distribution Channel segment.

- Mass and Drug Store priced products under USD 20 capture 70.82% of the By Price Range segment.

- Individual Consumers and Retail buyers represent 55.80% of the By End User segment.

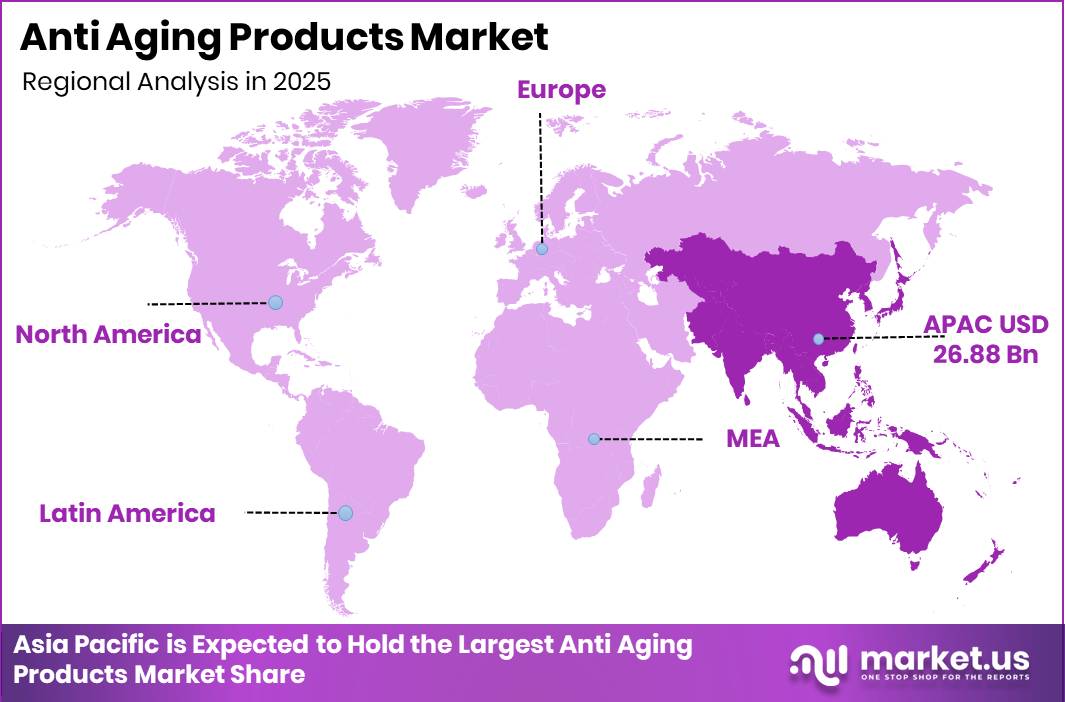

- Asia Pacific dominates the global market with a 41.00% share, valued at USD 26.88 Billion.

This reflects a category increasingly shaped by ingredient transparency expectations rather than packaging claims alone. Regulators in North America and Europe continue raising safety substantiation and labeling standards for cosmetic products. Brands that document ingredient sourcing and efficacy data early secure stronger retail shelf access and consumer loyalty.

According to NSF, 74% of U.S. consumers consider organic ingredients important when purchasing personal care products. This preference pushes manufacturers toward clean label formulations and transparent sourcing claims. As reported by Revance, 91% of surveyed aesthetics consumers report being more ingredient aware than ever before, raising disclosure pressure across the category.

This signals consolidation among brands with credible dermatological positioning. In June 2025, L’Oréal agreed to acquire a majority stake in British skincare brand Medik8, known for vitamin A based anti aging products. This move strengthens L’Oréal’s dermatological credibility and shows large players prioritizing science backed acquisitions over trend driven launches.

Product Type Analysis

Skincare Products dominates with 62.00% due to broad daily routine adoption.

In 2025, Skincare Products held a dominant market position in the By Product Type segment of Anti Aging Products Market, with a 62.00% share. This segment includes anti-wrinkle creams, serums, masks, and sunscreens used in daily routines. Consequently, brands prioritize multi-step skincare lines over single-purpose launches to maximize basket size.

Devices and Tools hold a 12.00% share as consumers pair at-home gadgets with topical products. This segment includes microcurrent tools, LED masks, and cleansing devices marketed for visible firming results. As a result, device makers increasingly bundle subscriptions with refill products to lock in recurring revenue.

Others within Product Type captures 11.50% share, covering niche anti-aging formats outside core categories. Hair Care Products hold 10.00% share, led by anti-gray treatments and regrowth formulas targeting visible aging beyond skin. Body Care Products hold the remaining 4.50% share collectively.

Ingredient Analysis

Retinol and Retinoids dominates with 36.00% due to proven clinical wrinkle reduction.

In 2025, Retinol and Retinoids held a dominant market position in the By Ingredient segment of Anti Aging Products Market, with a 36.00% share. Hyaluronic Acid, Peptides, Vitamin C, and Others make up the remaining share collectively without individually disclosed figures. This reflects strong reliance on a single clinically validated active across global formulations.

As per our research, 73% of U.S. adults use products or procedures to prevent premature skin aging. This behavior sustains steady retinol demand as consumers seek preventive rather than corrective regimens. Therefore, formulators continue investing in retinol stabilization technology to reduce irritation while preserving efficacy claims.

Nature and Formulation Analysis

Conventional and Synthetic dominates with 76.88% due to established efficacy and lower cost.

In 2025, Conventional and Synthetic formulations held a dominant market position in the By Nature and Formulation segment of Anti Aging Products Market, with a 76.88% share. Natural and Organic formulations hold the remaining share. This reflects consumer trust in proven actives over emerging botanical alternatives at scale.

Distribution Channel Analysis

Offline dominates with 68.00% due to trusted in-store dermatology guidance.

In 2025, Offline channels held a dominant market position in the By Distribution Channel segment of Anti Aging Products Market, with a 68.00% share. This channel spans specialty beauty stores, pharmacies, department stores, and dermatology clinics where consumers seek guided purchases. Online channels hold the remaining share through direct to consumer and marketplace formats.

Data from Euromonitor shows 22% of global consumers define beauty as embracing aging, while 18% associate beauty with rejuvenation. This split shapes in-store consultation scripts differently across regions. Consequently, retailers train staff to position products around either acceptance or active correction depending on local consumer attitudes.

Price Range and Tier Analysis

Mass and Drug Store dominates with 70.82% due to accessible everyday pricing.

In 2025, Mass and Drug Store priced products below USD 20 held a dominant market position in the By Price Range segment of Anti Aging Products Market, with a 70.82% share. Mid-Range, Prestige, Luxury, and Ultra-Luxury tiers hold the remaining share collectively. This reflects broad price sensitivity even within a clinically positioned category.

As per our research, 56% of U.S. adults use sunscreen regularly as part of anti-aging prevention efforts. This habit sustains mass tier sunscreen volume across supermarkets and pharmacies. As a result, mass brands compete primarily on reapplication convenience rather than premium ingredient storytelling.

End User Analysis

Individual Consumers and Retail dominates with 55.80% due to self-directed skincare routines.

In 2025, Individual Consumers and Retail buyers held a dominant market position in the By End User segment of Anti Aging Products Market, with a 55.80% share. Dermatology Clinics, Beauty Salons, Hospitals, and Professional Makeup Artists hold the remaining share collectively. This signals continued growth in self-administered routines over clinic-led treatment.

Key Market Segments

By Product Type

- Skincare Products

- Anti-wrinkle creams and moisturizers

- Serums and face oils

- Masks and sheet masks

- Sunscreens and UV protection

- Others

- Hair Care Products

- Anti-gray and hair color products

- Hair thickening and regrowth treatments

- Others

- Body Care Products

- Anti-aging body lotions and creams

- Firming and lifting body treatments

- Hand and nail anti-aging creams

- Devices and Tools

- Others

By Ingredient

- Retinol and Retinoids

- Hyaluronic Acid

- Peptides

- Vitamin C

- Others

By Nature and Formulation

- Conventional and Synthetic

- Natural and Organic

By Application

- Topical Application

- Oral and Ingestible

- Injectable and Clinical

- Device-Based

By Distribution Channel

- Offline

- Specialty beauty stores

- Department stores and luxury retail

- Pharmacies and drugstores

- Supermarkets and hypermarkets

- Dermatology clinics and medical spas

- Salon and spa professional channels

- Online

- Brand-owned D2C websites

- E-commerce marketplaces

- Social commerce

- Subscription beauty boxes

- Telemedicine and prescription platforms

By Price Range and Tier

- Mass and Drug Store (Below USD 20)

- Mid-Range and Masstige (USD 20 to 80)

- Prestige and Premium (USD 80 to 300)

- Luxury (USD 300 to 1,000)

- Ultra-Luxury and Clinical (Above USD 1,000)

By End User

- Individual Consumers and Retail

- Dermatology Clinics and Aesthetic Centers

- Beauty Salons and Spas

- Hospitals and Healthcare Facilities

- Professional and Celebrity Makeup Artists

Regional Analysis

Asia Pacific Dominates the Anti Aging Products Market with a Market Share of 41.00%, Valued at USD 26.88 Billion

Asia Pacific leads the global market through dense urban populations across China, Japan, South Korea, and India seeking visible skin renewal. Local beauty culture treats skincare as a daily routine rather than an occasional purchase. In December 2025, Beiersdorf expanded its Eucerin HARI FILLER anti-aging range into Japan, reinforcing regional brand depth.

North America builds on dermatology clinic density and strong pharmacy distribution across the US and Canada. Consumers in this region favor clinically validated actives sold through trusted retail pharmacy chains. This structure supports premium positioning while keeping mass tier sunscreen and moisturizer products widely accessible nationwide.

Europe spans Germany, France, the UK, Spain, and Italy, where regulatory scrutiny shapes ingredient and labeling standards. This regulatory environment favors brands with strong safety documentation and clinical substantiation. Consequently, European retailers prioritize listing partners who can demonstrate compliant, well-documented product claims consistently.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Anti-aging demand increasingly favors dermocosmetic brands that pair cosmetic retail with medical credibility. L’Oréal reported 2025 group sales of 44.0 Billion euros, with its Dermatological Beauty division growing 5.5% for the year and 11.5% in Q4. This acceleration shows medically positioned skincare outpacing efficacy-led segments overall.

This shift moves the business model from trend-led launches to repeatable routines built around serums, SPF, and retinoid-alternative regimens. These routines carry higher retention and lower promotional dependency than seasonal product drops. Therefore, clinical skincare supports premium pricing and improves gross margin mix without entering regulated drug pathways in most markets.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population expansion | +1.4% | North America, EU, Japan, South Korea, China urban, India metro | Long term |

| Clinical dermocosmetics adoption | +1.2% | North America core, EU, Brazil, Gulf, APAC tier-1 cities | Medium term |

| Biotech personalization tools | +0.9% | U.S., France, South Korea, Japan, China premium corridors | Medium term |

| Beauty e-commerce acceleration | +1.0% | U.S., China, UK, Gulf, Southeast Asia | Short term |

| APAC premium anti-aging spend | +1.1% | China, South Korea, Japan, Singapore, India upper-income urban | Medium term |

| Retinol compliance and reformulation cycle | +0.6% | EU core, UK spill-over, global exporters to Europe | Short term |

Restraints

Cross-border compliance creates a major restraint as anti-aging portfolios face heavier administrative load under MoCRA in the US alongside stricter European dossier and labeling standards. Each marketed cosmetic product must be listed with the FDA annually, and serious adverse events must be reported within 15 business days. This raises overhead and slows SKU onboarding industry wide.

This restraint hits anti-aging harder than basic personal care because the category is innovation-led and claim-heavy. A 3 to 6 month launch delay on a hero serum can erase a seasonal merchandising window. Consequently, working capital can rise roughly 8% to 12%, depressing forecast CAGR by about 0.9 percentage points in North America and Europe.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-region compliance burden | -0.9% | North America core, EU, UK | Short term (≤ 2 years) |

| Ingredient restriction reformulation | -0.8% | EU core, UK aligned, premium APAC imports | Medium term (2-4 years) |

| Tariff and input-cost inflation | -0.7% | U.S. imports, China-linked supply chains, EU/APAC corridors | Short term (≤ 2 years) |

| Efficacy skepticism and claims scrutiny | -0.6% | North America, EU, urban APAC | Medium term (2-4 years) |

| Consumer downtrading in prestige skincare | -0.5% | U.S., China, North Asia, Western Europe | Short term (≤ 2 years) |

| Testing, traceability, recall readiness | -0.4% | North America core, EU, global exporters | Medium term (2-4 years) |

Challenges

Anti-aging brands now face a heavier burden generating technical substantiation for wrinkle, firmness, microbiome, and longevity claims across jurisdictions. US MoCRA rules require facility registration, annual product listing, and adverse event reporting within 15 business days. EU anti-greenwashing rules taking effect through September 2026 raise proof requirements for environmental messaging further.

This pressure modeled extends time-to-market by 4 to 9 months for higher-claim launches and raises pre-launch testing spend by 15% to 30%. As a result, weaker claims get pruned before launch, slowing premium innovation throughput. Shared regulatory data rooms and modular testing protocols offer the clearest path to controlling this cost.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Active ingredient volatility | -1.1% | EU sourcing hubs, North America core, APAC manufacturing corridors | Medium term (2-4 years) |

| Claims substantiation burden | -0.9% | EU regulatory hubs, U.S. compliance markets, developed APAC | Medium term (2-4 years) |

| Sustainable packaging transition | -0.8% | EU first wave, North America premium brands, Japan-Korea urban markets | Long term (≥ 4 years) |

| Formulation talent bottlenecks | -0.7% | U.S. innovation clusters, EU labs, India-Korea contract R&D bases | Long term (≥ 4 years) |

| Omnichannel demand distortion | -1.0% | North America digital channels, China social commerce, EU multichannel retail | Short term (≤ 2 years) |

| Personalization scale economics | -0.6% | North America premium skincare, EU dermocosmetics, advanced APAC markets | Long term (≥ 4 years) |

Opportunities

Senior-care channels remain an untapped go-to-market path as assisted living, senior communities, and home-care networks rarely receive formal anti-aging distribution. One in five Americans is projected to be over 65 by 2030, creating a large underserved demand pool. This gap favors simplified, high-trust regimen products over complex beauty assortments.

This channel design could reduce customer acquisition cost by 20% to 35% versus open-market beauty retail while supporting stable reorder cycles. Caregiver education, easy-open packaging, and reimbursement-adjacent partnerships strengthen this case. Consequently, this opportunity could add around 0.9 percentage points of incremental CAGR across the US, Western Europe, and Japan.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Longevity ingestibles adjacency | +1.6% | North America core, EU, Japan, South Korea, urban China | Short term |

| Diagnostic personalization platforms | +1.3% | APAC premium, North America, GCC | Short term |

| Menopause and 45+ hormonal skin | +1.1% | North America, EU, Australia, Japan | Medium term |

| Dermatology-medspa hybrid bundles | +1.5% | North America core, Brazil, South Korea, UAE | Medium term |

| Senior-care channel expansion | +0.9% | U.S., Western Europe, Japan | Medium term |

| Regulatory-grade M&A roll-up | +1.2% | U.S., EU, selective APAC | Long term |

Key Company Insights

L’Oréal strengthens its anti-aging portfolio through targeted acquisitions rather than organic product development alone. In June 2026, L’Oréal acquired a majority stake in Indian skincare company Innovist, adding science-led brands Bare Anatomy and Chemist at Play. This buy-and-build approach gives L’Oréal faster access to regional formulation expertise and distribution networks across APAC.

Beiersdorf AG pairs mass-market scale with emerging science platforms to defend its dermocosmetic position. In August 2025, Beiersdorf launched the NIVEA Cellular Epigenetics Rejuvenating Serum featuring EPICELLINE, its first mass-market epigenetic anti-aging serum. This positions Beiersdorf as a bridge between accessible pricing and clinically advanced anti-aging science.

Key Players

- L’Oréal

- Beiersdorf AG

- Shiseido

- Niagen Bioscience

- Pulmatrix

- Eos SENOLYTIX

- Dior Beauty

- Revance

- Kenvue

Recent Developments

- January 2025 – Shiseido unveiled a reformulated ULTIMUNE serum powered by its new patented Power Fermented Camellia Plus technology, targeting skin regeneration and age related skin concerns.

- August 2025 – Beiersdorf AG launched the NIVEA Cellular Epigenetics Rejuvenating Serum featuring EPICELLINE, its first mass market epigenetic anti aging serum designed to reverse visible skin aging.

- March 2026 – Niagen Bioscience launched the Niagen Skincare Innovation Lab and introduced Niagen NanoCloud, a dermatologist tested topical anti aging product based on NAD+ science.

- March 2026 – Pulmatrix and Eos SENOLYTIX announced a merger agreement alongside 19 million dollars in financing to accelerate development of therapies targeting aging related conditions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 65.57 Billion |

| Forecast Revenue (2035) | USD 143.11 Billion |

| CAGR (2026-2035) | 9.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Skincare Products, Hair Care Products, Body Care Products, Devices and Tools, Others), By Ingredient (Retinol and Retinoids, Hyaluronic Acid, Peptides, Vitamin C, Others), By Nature and Formulation (Conventional and Synthetic, Natural and Organic), By Application (Topical, Oral and Ingestible, Injectable and Clinical, Device-Based), By Distribution Channel (Offline, Online), By Price Range (Mass, Mid-Range, Prestige, Luxury, Ultra-Luxury), By End User (Individual Consumers, Dermatology Clinics, Beauty Salons, Hospitals, Professional Makeup Artists) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | L’Oréal, Beiersdorf AG, Shiseido, Niagen Bioscience, Pulmatrix, Eos SENOLYTIX, Dior Beauty, Revance, Kenvue |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |