Global Alternative Protein Ingredients Market Size, Share Analysis Report By Product (Plant Proteins, Roots, Ancient Grains, Nuts And Seeds, Microbe-based Protein, Insect Protein), By Application (Instant Nutritional Drinks, Ready to Drink Nutritional Drinks, Meat Analogues (Texture), Meat and Sausages (Binder), Ice Cream, Yogurts, Others, Bakery Products, High Protein Bars/ Cereals, Mayonnaise And Salad Dressings, Sauces and Gravies, Animal Feed, Milk, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182201

- Number of Pages: 199

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

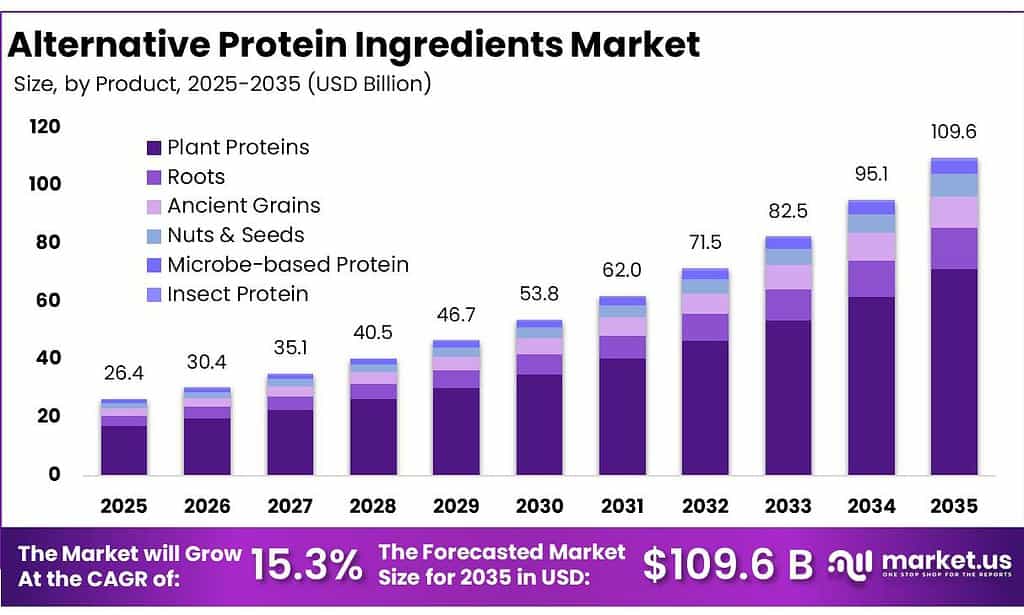

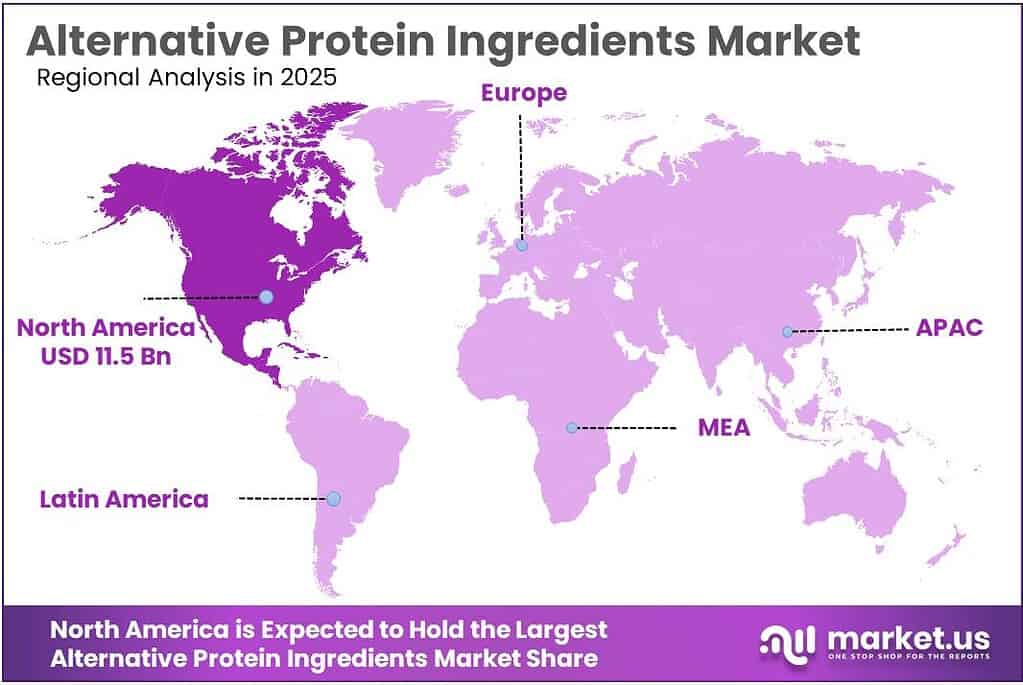

The Global Alternative Protein Ingredients Market size is expected to be worth around USD 109.6 Billion by 2035, from USD 26.4 Billion in 2025, growing at a CAGR of 15.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 43.6% share, holding USD 11.5 Billion revenue.

Alternative protein ingredients represent a strategic ingredient class built around plant proteins, fermentation-derived proteins, algal inputs, fungal biomass, and functional blends that can replace or extend animal-based protein systems in foods, beverages, and nutrition products.

The backdrop is structurally supportive: FAO-led reporting showed that 673 million people experienced hunger in 2024, while 2.6 billion people could not afford a healthy diet in the same year, underscoring the need for scalable, nutrient-dense, and cost-efficient protein formats.

According to GFI’s 2024 State of Alternative Proteins report, global retail sales of plant-based meat, seafood, milk, yogurt, ice cream, and cheese reached US$28.6 billion in 2024, up 5% year on year, while the U.S. plant-based retail market stood at US$8.1 billion. The same report noted that at least 46 alternative-protein facilities were launched, expanded, or announced in 2024, including 26 plant-based, 16 fermentation, and 4 cultivated-meat facilities.

The key demand drivers are affordability pressure, protein diversification, and resource efficiency. OECD-FAO’s 2025–2034 Outlook states that global food and agricultural trade reached US$1.9 trillion in 2023, and projects that 22% of all calories will cross international borders over the next decade, increasing the strategic value of locally processable protein ingredients.

At the same time, FAO reports that agrifood systems account for about one-third of total anthropogenic greenhouse gas emissions, which keeps low-input protein ingredients commercially relevant for food manufacturers under sustainability mandates. GFI’s 2024 ISO-certified study further reported that plant-based meat has an 89% lower environmental impact than animal meat overall, including 91% lower than beef, 88% lower than pork, and 71% lower than chicken.

Policy support is also strengthening the outlook. The European Commission’s 2025 Horizon topic on scaling nutritional proteins from alternative sources explicitly targets food ingredients with at least 50% protein content by weight, reflecting growing institutional support for extraction, purification, and downstream ingredient innovation.

Key Takeaways

- Alternative Protein Ingredients Market size is expected to be worth around USD 109.6 Billion by 2035, from USD 26.4 Billion in 2025, growing at a CAGR of 15.3%.

- Plant Proteins held a dominant market position, capturing more than a 65.1% share.

- Meat Analogues (Texture) held a dominant market position, capturing more than a 19.2% share.

- North America continues to lead the Alternative Protein Ingredients market, holding a dominant share of 43.6% valued at USD 11.5 billion.

By Product Analysis

Plant Proteins lead strongly with 65.1% share driven by wide usage and affordability

In 2025, Plant Proteins held a dominant market position, capturing more than a 65.1% share. This leadership is mainly supported by their strong presence across everyday food and beverage products such as dairy alternatives, protein powders, bakery items, and ready-to-drink nutrition.

Ingredients like soy, pea, and wheat protein continue to remain the most widely used due to their easy availability, cost efficiency, and well-established supply chains. Food manufacturers are also increasingly choosing plant proteins because they offer flexibility in formulation and align well with clean-label trends, which are becoming more important for consumers.

By Application Analysis

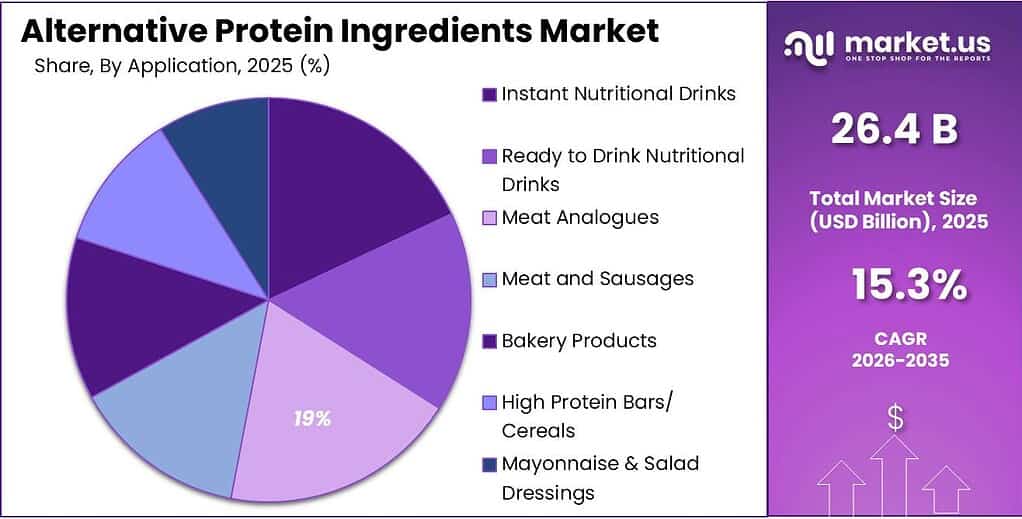

Meat Analogues (Texture) holds 19.2% as demand for realistic plant-based meat grows

In 2025, Meat Analogues (Texture) held a dominant market position, capturing more than a 19.2% share. This segment is mainly driven by the rising demand for plant-based meat products that closely match the texture and bite of conventional meat. Consumers today are not just looking for alternatives, but for products that feel similar in taste and mouthfeel, which has pushed manufacturers to focus heavily on texture-enhancing protein ingredients such as textured vegetable protein and extrusion-based formulations.

Key Market Segments

By Product

- Plant Proteins

- Cereals

- Legumes

- Lupine

- Chickpea

- Others

- Roots

- Potato

- Maca

- Others

- Ancient Grains

- Hemp

- Quinoa

- Sorghum

- Amaranth

- Chia

- Millet

- Others

- Nuts & Seeds

- Canola

- Almonds

- Flaxseeds

- Others

- Microbe-based Protein

- Algae

- Bacteria

- Yeast

- Fungi

- Precision Fermentation Protein

- Insect Protein

- Coleoptera

- Lepidoptera

- Hymenoptera

- Orthoptera

- Hemiptera

- Diptera

- Others

By Application

- Instant Nutritional Drinks

- Ready to Drink Nutritional Drinks

- Meat Analogues (Texture)

- Meat and Sausages (Binder)

- Ice Cream

- Yogurts

- Others

- Bakery Products

- High Protein Bars/ Cereals

- Mayonnaise & Salad Dressings

- Sauces and Gravies

- Animal Feed

- Milk

- Others

Emerging Trends

Precision fermentation and technology-driven proteins are shaping the next phase

One of the most important latest trends in the alternative protein ingredients market is the rapid rise of precision fermentation and technology-led innovation. This trend is changing how proteins are produced, moving away from traditional agriculture toward controlled and efficient systems. According to the Good Food Institute, global fermentation-related patents for alternative proteins have increased by over 6500% in the last 10 years, reaching more than 2,400 unique filings.

In 2025 and moving into 2026, fermentation is gaining strong attention because it allows companies to create specific protein ingredients such as dairy proteins without using animals. It also helps improve functionality, taste, and consistency in final products. Governments are also supporting this shift. Public investment in fermentation technologies reached around $203 million in 2024, which was higher than investments in plant-based protein research.

Shift toward better taste, functionality, and mainstream food integration

Another major trend is the strong shift toward improving taste, texture, and everyday usability of alternative protein ingredients. Earlier, products were mainly focused on replacing meat, but now the focus has moved toward making proteins suitable for daily food consumption across multiple categories. According to industry insights, 63% of consumers say taste and nutrition are equally important when choosing protein-rich foods.

In 2025 and 2026, companies are working on improving sensory performance through better processing methods and ingredient blending. New developments include sunflower protein, which can contain up to 50% protein along with fiber and vitamins, making it suitable for beverages and dairy alternatives

Drivers

Rising Global Protein Demand is pushing shift toward alternative ingredients

One of the strongest driving factors for alternative protein ingredients is the steady rise in global protein demand combined with changing dietary patterns. Across the world, protein consumption has been increasing consistently over the past few decades. According to FAO-based data, global per capita protein supply has increased by around one-third over time, showing a clear upward demand trend across regions.

At the same time, there is a structural shift in where this protein comes from. Scientific studies indicate that around 80% of global protein intake is currently derived from plant-based sources, while only about 20% comes from animal-based foods. This clearly highlights the foundational role of plant proteins in the global diet and explains why industries are increasingly focusing on improving plant-based and alternative protein ingredients.

Government policies and sustainability concerns accelerating adoption

Another major factor supporting the growth of alternative protein ingredients is the increasing focus on sustainability and policy support from governments and global organizations. Food systems today are under pressure to deliver more nutrition with fewer environmental resources. According to FAO insights, there are more than 7,000 edible plant species, yet global diets rely heavily on a limited number of crops, which highlights the need to diversify protein sources for long-term food security

Additionally, global institutions and national governments are actively working on improving protein quality databases, food safety frameworks, and nutritional standards for alternative proteins. FAO has emphasized the inclusion of both traditional and novel protein sources in future food composition systems, supporting broader adoption across countries. In parallel, many developed regions are promoting a “protein transition,” where dietary patterns shift toward higher plant-based consumption, with some countries targeting ratios such as 50:50 or even 40:60 between animal and plant proteins

Restraints

High Production Cost and Price Sensitivity remain a key challenge

One of the biggest restraining factors for alternative protein ingredients is the high production cost, which directly affects final product pricing and consumer adoption. Compared to conventional protein sources, many alternative proteins—especially newer ones like fermentation-based or highly processed plant proteins—require advanced processing technologies, specialized infrastructure, and controlled manufacturing environments.

According to Food and Agriculture Organization (FAO), affordability remains a major concern in global nutrition systems, as more than 3.1 billion people were unable to afford a healthy diet in 2021.

From an industry point of view, companies often struggle to match the price of traditional protein products such as meat, eggs, or dairy. Even when production volumes increase, the cost of raw materials, processing, and formulation remains relatively high. This creates a barrier for large-scale adoption, particularly in price-conscious markets like India, Southeast Asia, and Africa.

Government initiatives such as India’s ₹10,900 crore Production Linked Incentive Scheme for Food Processing Industry (PLISFPI) are trying to improve manufacturing efficiency, but cost parity is still a work in progress.

Limited consumer acceptance due to taste and familiarity

Another important restraint is consumer hesitation, mainly linked to taste, texture, and familiarity. While awareness of plant-based and alternative proteins is growing, many consumers still prefer traditional protein sources because they are familiar, widely available, and culturally accepted.

According to the Good Food Institute, plant-based food sales reached US$8.1 billion in the U.S. in 2024, but still accounted for only about 1.1% of total food and beverage sales.

Taste and texture remain key issues, especially in meat analogue products where consumers expect a very close match to real meat. If the product does not meet expectations, repeat purchases tend to drop.

Opportunity

Expanding global food demand is creating strong opportunity for alternative protein ingredients

One of the biggest growth opportunities for alternative protein ingredients comes from the rapid increase in global food and protein demand. As populations grow and incomes rise, the pressure on food systems is becoming more visible. According to data linked with the Food and Agriculture Organization, global food demand is expected to grow by around 60% by 2050, showing how much additional production will be required in the coming decades. At the same time, global protein demand is projected to increase by up to 20% by 2025, reflecting immediate pressure on supply systems

This situation is opening a clear opportunity for alternative protein ingredients, especially those that can be produced efficiently and at scale. Traditional animal protein systems require large amounts of land, water, and feed, while studies indicate that agriculture already uses around 50% of global land and contributes to about 30% of greenhouse gas emissions. This creates a strong need for protein sources that can deliver similar nutrition with fewer resources. Alternative protein ingredients such as plant-based, fermentation-derived, and blended proteins are well positioned to fill this gap.

Sustainability transition and policy support opening new market pathways

Another major growth opportunity lies in the global shift toward sustainable diets and supportive policy frameworks. Many countries are now focusing on reducing environmental impact while ensuring nutritional security. According to FAO insights, there are over 1,000 manufacturers and 500 ingredient suppliers already active in the alternative protein space globally, showing how quickly the ecosystem is expanding

In addition, policymakers are encouraging diversification of protein sources to strengthen food systems. FAO has highlighted the importance of expanding beyond conventional crops and animal sources to include novel and underutilized protein ingredients. This is especially important as global diets currently depend on a limited number of crops, increasing supply risks. Governments are also investing in food processing and innovation programs, which indirectly support alternative protein ingredient production and adoption.

Regional Insights

North America dominates with 43.6% share driven by strong consumer adoption and innovation base

North America continues to lead the Alternative Protein Ingredients market, holding a dominant share of 43.6% valued at USD 11.5 billion, supported by strong consumer awareness, advanced food technology infrastructure, and high adoption of plant-based and functional nutrition products. The region, especially the United States, plays a central role due to its well-established ecosystem of food innovation, investment funding, and retail penetration of alternative protein products.

According to industry data, North America accounted for a significant portion of global demand and generated over USD 14.2 billion in 2024, reflecting its strong base for further expansion.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ADM plays a major role in alternative protein ingredients through its strong plant protein portfolio. The company operates in more than 200 countries and reported over USD 93 billion revenue in 2023, showing its large-scale global reach. ADM has invested heavily in plant protein facilities, including innovation centers and processing units to expand soy and pea protein production. It continues to strengthen its alternative protein capacity through partnerships and product development, aiming to meet rising demand across food, beverage, and nutrition segments.

Impossible Foods Inc. is a leading food-tech company known for developing plant-based meat using innovative ingredients like heme. The company has raised over USD 2 billion in funding since its founding and expanded into 20,000+ retail and foodservice locations globally. Its products are designed to replicate real meat taste and texture using advanced food science. Impossible Foods continues to invest in R&D and international expansion, focusing on improving product affordability and accessibility across key global markets.

Lightlife Foods, Inc., a subsidiary of Maple Leaf Foods, focuses on plant-based protein products such as tempeh, sausages, and burgers. Maple Leaf Foods reported around CAD 4.9 billion revenue in 2023, supporting Lightlife’s operations. The brand has been active for over 40 years, making it one of the early entrants in plant-based proteins. It emphasizes simple ingredients and clean-label formulations, targeting consumers looking for healthier alternatives. Lightlife continues expanding its presence in North America through retail and foodservice channels.

Top Key Players Outlook

- ADM

- Cargill Inc.

- Lightlife Foods, Inc.

- Impossible Foods Inc.

- International Flavors & Fragrances, Inc.

- Ingredion Inc.

- Kerry Group

- Glanbia plc

- Bunge Limited

- Axiom Foods Inc.

Recent Industry Developments

As of 2025, ADM (Archer Daniels Midland) continues to expand its human nutrition segment, which includes alternative proteins, reporting net earnings of USD 1.1 billion and operating cash flow of USD 5.5 billion, showing stable financial strength to support innovation.

As of 2025, Cargill continues to leverage its global scale, operating in 70+ countries with a workforce of around 160,000 employees, allowing it to maintain a strong supply chain for protein ingredients worldwide.

Report Scope

Report Features Description Market Value (2025) USD 26.4 Bn Forecast Revenue (2035) USD 109.6 Bn CAGR (2026-2035) 15.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Plant Proteins, Roots, Ancient Grains, Nuts And Seeds, Microbe-based Protein, Insect Protein), By Application (Instant Nutritional Drinks, Ready to Drink Nutritional Drinks, Meat Analogues (Texture), Meat and Sausages (Binder), Ice Cream, Yogurts, Others, Bakery Products, High Protein Bars/ Cereals, Mayonnaise And Salad Dressings, Sauces and Gravies, Animal Feed, Milk, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ADM, Cargill Inc., Lightlife Foods, Inc., Impossible Foods Inc., International Flavors & Fragrances, Inc., Ingredion Inc., Kerry Group, Glanbia plc, Bunge Limited, Axiom Foods Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Alternative Protein Ingredients MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Alternative Protein Ingredients MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ADM

- Cargill Inc.

- Lightlife Foods, Inc.

- Impossible Foods Inc.

- International Flavors & Fragrances, Inc.

- Ingredion Inc.

- Kerry Group

- Glanbia plc

- Bunge Limited

- Axiom Foods Inc.

Our Clients

- 182201

- Mar 2026