Global Allulose Market Size, Share Analysis Report By Type (Powder, Liquid, Crystal), By Application (Food, Beverages, Pharmaceuticals), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Sep 2025

- Report ID: 159295

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

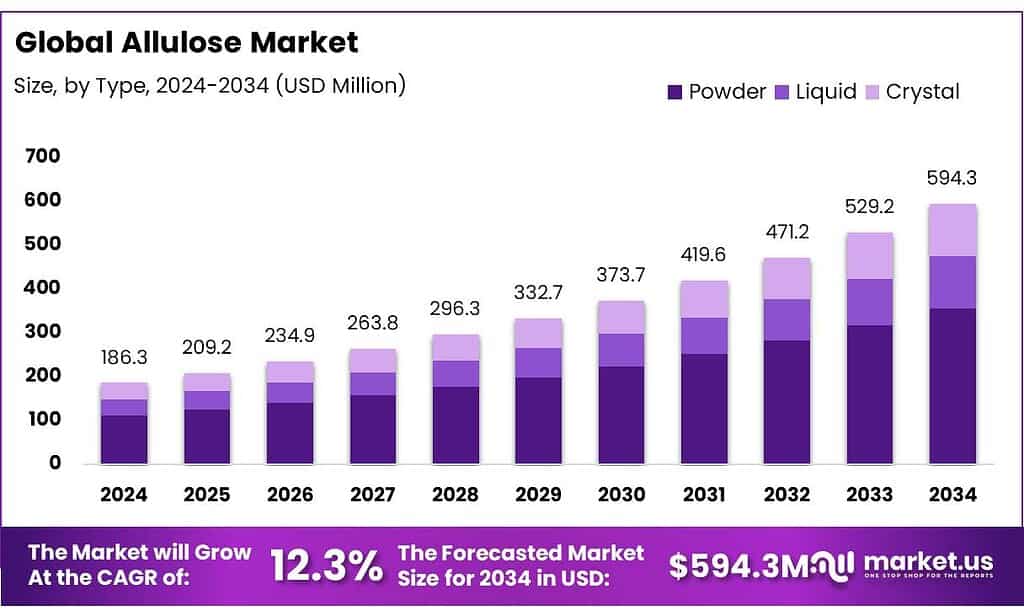

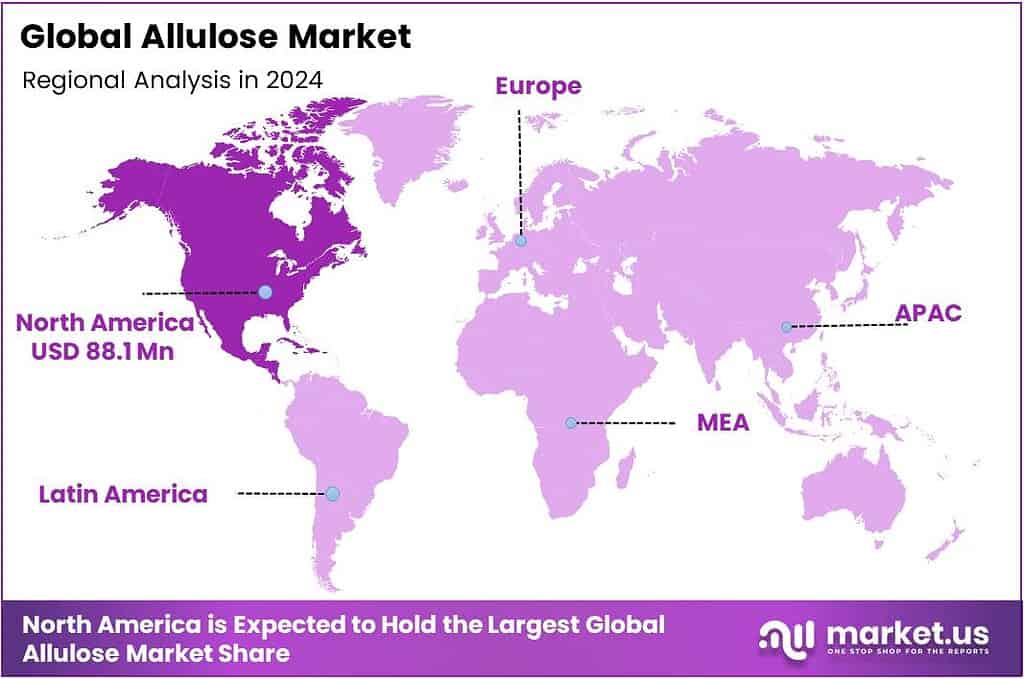

The Global Allulose Market size is expected to be worth around USD 594.3 Million by 2034, from USD 186.3 Million in 2024, growing at a CAGR of 12.3% during the forecast period from 2025 to 2034. In 2024 North America held a dominant market position, capturing more than a 47.3% share, holding USD 88.1 Million in revenue.

Allulose, also known as D-psicose, is a low-calorie monosaccharide that has gained prominence as a sugar substitute due to its minimal caloric content and resemblance to sucrose in taste and texture. Naturally occurring in small quantities in foods like figs, raisins, and maple syrup, allulose is produced commercially through enzymatic conversion of fructose, typically derived from corn or sugar beets. This process involves enzymes such as D-tagatose 3-epimerase to convert fructose into allulose, offering a viable method for large-scale production.

Technological advancements have also played a crucial role in enhancing the production efficiency of allulose. Researchers at the University of California, Davis, in collaboration with Mars, Incorporated, have developed a scalable production technique that achieves over 99% theoretical yield with high purity. This method minimizes the need for expensive separation processes, thereby reducing production costs and making allulose more commercially viable.

The growing prevalence of lifestyle-related health issues such as obesity and diabetes has further fueled the demand for sugar substitutes like allulose. Allulose’s minimal impact on blood glucose levels and its suitability for ketogenic and low-carb diets have contributed to its increasing adoption in food and beverage products. In South Korea, for example, companies like Samyang Corp have significantly expanded their allulose production capacities, with new facilities capable of producing 13,000 tons annually to meet the rising demand.

Policy and public-health goals are the primary driving factors. The World Health Organization recommends cutting free-sugar intake to <10% of total energy, with a conditional target of <5%, creating a sustained global push for sugar reduction across categories. Allulose fits this demand because it provides sugar-like sensory performance with minimal calories, helping brands meet numeric sugar-reduction targets without sacrificing taste.

- In the U.S., FDA’s labeling discretion (exclusion from Added Sugars and use of 0.4 kcal/g) directly improves a product’s on-pack nutrition metrics, which in turn improves eligibility for retailer and school standards tied to sugar thresholds.

Key Takeaways

- Allulose Market size is expected to be worth around USD 594.3 Million by 2034, from USD 186.3 Million in 2024, growing at a CAGR of 12.3%.

- Powder held a dominant market position in the allulose market, capturing more than a 57.2% share.

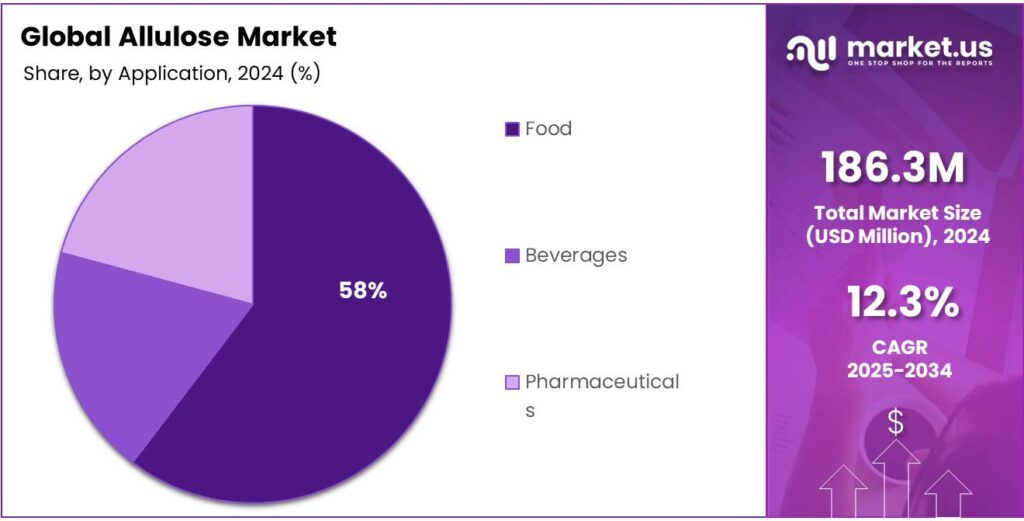

- Food held a dominant market position in the allulose market, capturing more than a 58.8% share.

- North America dominated the global allulose market, accounting for a significant 47.3% share, equivalent to USD 88.1 million.

By Type Analysis

Powder Segment Dominates with 57.2% Market Share in 2024

In 2024, Powder held a dominant market position in the allulose market, capturing more than a 57.2% share. This segment’s leading position can be attributed to its widespread application across various industries, particularly in the food and beverage sector. Powdered allulose is favored due to its ease of use in formulations, as it can be easily incorporated into baked goods, beverages, dairy products, and confectionery. Its versatility and convenience for manufacturers have led to its extensive use in the production of sugar-free and low-calorie products.

The increasing demand for sugar alternatives in processed foods has further bolstered the growth of the powder segment. In addition, its stable shelf life and ability to maintain sweetness during cooking or baking have made it a preferred choice for food manufacturers. Given the rising awareness about health and wellness, powdered allulose is expected to see continued growth in the coming years, with more companies incorporating it into their product offerings to meet consumer demand for healthier sweeteners.

By Application Analysis

Food Segment Leads with 58.8% Share in 2024

In 2024, Food held a dominant market position in the allulose market, capturing more than a 58.8% share. The increasing demand for healthier, low-calorie sweeteners in the food industry has been a key factor behind this growth. Allulose, due to its ability to mimic the sweetness of sugar without the associated calories, is widely used in the production of sugar-free and reduced-calorie products. Its versatility makes it a popular choice for a wide range of food applications, including baked goods, beverages, dairy, and snacks.

The rising health-consciousness among consumers, along with the growing prevalence of diabetes and obesity, has led to a shift in dietary preferences toward products that are low in sugar but high in taste. As a result, food manufacturers are increasingly incorporating allulose into their recipes to cater to this demand. The convenience of allulose in food production, as well as its stability and ability to provide a sugar-like texture, has helped solidify its position in the market.

Key Market Segments

By Type

- Powder

- Liquid

- Crystal

By Application

- Food

- Bakery & Confectionery

- Table-top sweetener

- Dairy & frozen desserts

- Sauces & Dressings

- Ice Creams and Desserts

- Beverages

- Pharmaceuticals

Emerging Trends

Regulatory Approvals and Safety Endorsements

Allulose has garnered significant attention as a low-calorie sweetener, and its growth is propelled by crucial regulatory approvals and safety endorsements from reputable health authorities. In the United States, the Food and Drug Administration (FDA) has recognized allulose as a Generally Recognized As Safe (GRAS) substance. This designation allows manufacturers to use allulose in a wide range of food products without the need for pre-market approval.

Additionally, the FDA permits allulose to be excluded from the total and added sugars count on Nutrition and Supplement Facts labels, provided it is used as an ingredient. This regulatory support has encouraged food companies to incorporate allulose into their products, catering to the growing consumer demand for low-calorie and sugar-free alternatives.

Similarly, in South Korea, allulose has been approved for use in food products. The country’s regulatory framework has facilitated the inclusion of allulose in various food items, aligning with the government’s efforts to promote healthier eating habits among its population. This approval has led to increased production and availability of allulose-containing products in the market.

These regulatory approvals are pivotal in driving the adoption of allulose, as they provide manufacturers with the assurance needed to invest in its incorporation into food products. The support from government agencies not only ensures the safety and efficacy of allulose but also aligns with public health objectives aimed at reducing sugar intake and combating diet-related health issues.

Drivers

Government Initiatives and Regulatory Support

The rising demand for allulose is significantly influenced by government initiatives and regulatory support aimed at promoting healthier dietary choices and reducing sugar consumption. Allulose, a low-calorie sweetener that mimics the taste and texture of sugar, has gained regulatory approvals in various countries, facilitating its adoption in the food and beverage industry.

In the United States, the Food and Drug Administration (FDA) has recognized allulose as a Generally Recognized As Safe (GRAS) substance. This designation allows manufacturers to use allulose in a wide range of food products without the need for pre-market approval. Additionally, the FDA permits allulose to be excluded from the total and added sugars count on Nutrition and Supplement Facts labels, provided it is used as an ingredient. This regulatory support has encouraged food companies to incorporate allulose into their products, catering to the growing consumer demand for low-calorie and sugar-free alternatives

Similarly, in South Korea, allulose has been approved for use in food products. The country’s regulatory framework has facilitated the inclusion of allulose in various food items, aligning with the government’s efforts to promote healthier eating habits among its population

These regulatory approvals are pivotal in driving the adoption of allulose, as they provide manufacturers with the assurance needed to invest in its incorporation into food products. The support from government agencies not only ensures the safety and efficacy of allulose but also aligns with public health objectives aimed at reducing sugar intake and combating diet-related health issues.

Restraints

Limited Consumer Awareness and Acceptance

Despite its potential, allulose faces significant challenges in consumer acceptance, primarily due to limited awareness and concerns over its naturalness. Studies indicate that only about 13% of U.S. consumers have heard of allulose, a figure that has remained relatively unchanged since 2021. This limited recognition hampers its widespread adoption, as consumers often prefer familiar sweeteners over novel alternatives.

Consumer perception plays a crucial role in the acceptance of new ingredients. Research has shown that individuals are more inclined to choose sweeteners labeled as “natural” rather than “artificial.” For instance, stevia and monk fruit sweeteners, which are derived from plants, are perceived as safer and healthier compared to synthetic options like aspartame and sucralose. In contrast, allulose, despite being a naturally occurring sugar found in small quantities in foods like figs and raisins, is often viewed with skepticism due to its unfamiliarity.

This perception issue is not unique to the United States. In Europe, allulose is classified as a “novel food,” requiring extensive safety assessments before approval. Such regulatory hurdles further delay its introduction into the market, limiting its availability and consumer exposure.

Opportunity

Allulose as a Health-Conscious Sweetener

The global allulose market is experiencing significant growth, driven by increasing consumer demand for healthier, low-calorie sweeteners. Allulose, a naturally occurring sugar found in fruits like figs and raisins, offers a sweet taste with approximately 90% fewer calories than sucrose, making it an attractive alternative for those seeking to reduce sugar intake without compromising on taste.

In Asia-Pacific, the allulose market is expanding rapidly, driven by increasing health awareness and the adoption of low-calorie sweeteners in countries like South Korea, Japan, and China. South Korea, in particular, has emerged as a key player in the allulose market. Major companies such as Samyang Corporation have invested significantly in expanding production capacities. In 2024, Samyang opened a new factory with an investment of KRW 140 billion, quadrupling its allulose production to 13,000 tons annually. This expansion is expected to meet the growing domestic and international demand for allulose

Government initiatives and regulatory approvals play a crucial role in the growth of the allulose market. The FDA’s decision to allow allulose to be excluded from total and added sugars on nutrition labels has provided a significant boost to its adoption in food products. However, challenges remain, including the need for further research into the long-term health effects of allulose and its approval in other regions such as the European Union and Canada.

Regional Insights

North America Dominates Allulose Market with 47.3% Share in 2024

In 2024, North America dominated the global allulose market, accounting for a significant 47.3% share, equivalent to USD 88.1 million. The region’s dominance can be attributed to a strong shift in consumer preferences toward healthier, low-calorie alternatives to traditional sugars. North American consumers are increasingly focused on reducing sugar intake due to rising health concerns such as obesity, diabetes, and cardiovascular diseases. This has driven a surge in demand for low-calorie sweeteners like allulose, which offers a similar sweetness to sugar but with significantly fewer calories.

The U.S. leads the North American market, where allulose has gained widespread acceptance following its GRAS (Generally Recognized as Safe) status granted by the FDA in 2019. The FDA approval has boosted consumer confidence and encouraged manufacturers to incorporate allulose into a wide range of food and beverage products. This regulatory backing, combined with a growing preference for clean-label ingredients, has positioned North America as the largest market for allulose globally.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Anderson Advanced Ingredients specializes in innovative ingredient solutions, with a focus on health-conscious products. They offer high-quality allulose as part of their low-calorie sweetener portfolio. Anderson’s allulose is aimed at supporting healthier formulations in food and beverages, particularly targeting reduced sugar content. Their products cater to a growing demand for clean label and low-sugar alternatives, aligning with consumer preferences for healthier, sustainable options in the food industry.

Bonumose LLC is at the forefront of sugar reduction through its proprietary allulose production technology. The company focuses on providing scalable, cost-effective, and high-quality allulose to the food and beverage industry. Bonumose’s innovative production methods ensure a sustainable and efficient process. They cater to manufacturers looking to reduce sugar and calories while maintaining the desired taste and texture in products, driving growth in the low-sugar market.

Apura Ingredients is a leading supplier of natural sweeteners, with a strong emphasis on allulose. They provide clean-label, non-GMO allulose to food and beverage manufacturers seeking sugar alternatives. Apura’s allulose products are widely used in creating low-calorie, sugar-free, and health-focused formulations. Their innovation in ingredient technology ensures high purity and quality, supporting a growing demand for healthier options in consumer food products.

Top Key Players Outlook

- Anderson Advanced Ingredients

- Apura Ingredients

- Bonumose LLC

- CJ Cheil Jedang

- Heartland Food Products Group

- Icon Foods,

- Ingredion Inc

- Matsutani Chemical Industry Co. Ltd.

- Samyang Corporation

- Tate & Lyle

Recent Industry Developments

In 2024, Anderson Advanced Ingredients has further expanded its presence in the U.S. market, capitalizing on the increasing consumer preference for functional foods and sugar reduction. With a focus on sustainability and customer collaboration, the company has invested in research and development to optimize its allulose production, ensuring it remains cost-effective and scalable.

In 2024, Ingredion’s allulose products helped solidify its position as a trusted supplier in the low-calorie sweetener market, catering to the shift toward health-conscious eating and sustainable food production.

Report Scope

Report Features Description Market Value (2024) USD 186.3 Mn Forecast Revenue (2034) USD 594.3 Mn CAGR (2025-2034) 12.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Powder, Liquid, Crystal), By Application (Food, Beverages, Pharmaceuticals) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Anderson Advanced Ingredients, Apura Ingredients, Bonumose LLC, CJ Cheil Jedang, Heartland Food Products Group, Icon Foods,, Ingredion Inc, Matsutani Chemical Industry Co. Ltd., Samyang Corporation, Tate & Lyle Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Anderson Advanced Ingredients

- Apura Ingredients

- Bonumose LLC

- CJ Cheil Jedang

- Heartland Food Products Group

- Icon Foods,

- Ingredion Inc

- Matsutani Chemical Industry Co. Ltd.

- Samyang Corporation

- Tate & Lyle

Our Clients

- 159295

- Sep 2025