Quick Navigation

Report Overview

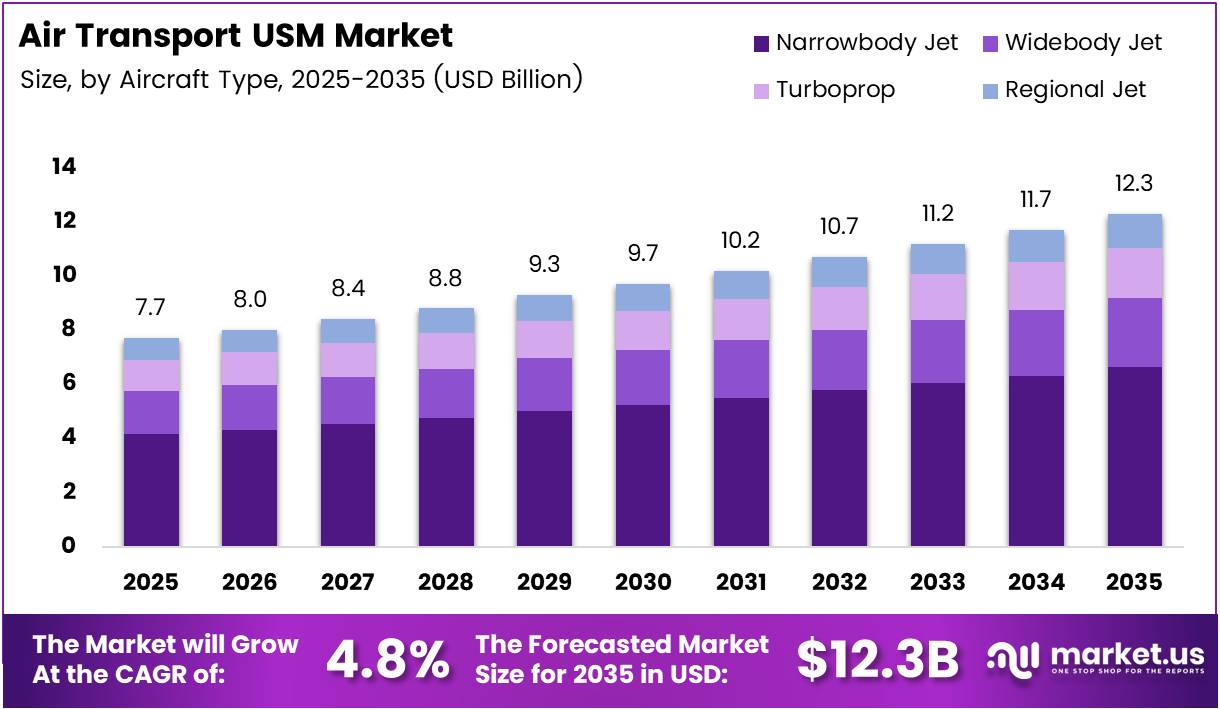

Global Air Transport USM Market size is expected to be worth around USD 12.3 Billion by 2035 from USD 7.7 Billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

The air transport used serviceable material (USM) market covers recertified, airworthy components sourced from retired or part-out aircraft and redistributed through MRO providers, airlines, and specialist distributors. These parts span engines, airframes, and line-replaceable components — all cleared to the same airworthiness standards as new OEM parts, but at a fraction of the procurement cost.

What drives this market is not simply buyer preference for cheaper parts. Structural supply constraints make USM a necessity. New aircraft deliveries remain suppressed, forcing airlines to extend the operational lives of aging fleets well beyond typical retirement thresholds. That extension creates direct, sustained demand for replacement components — demand that OEM production lines cannot meet at current output rates.

The fleet age dynamic reinforces this structural dependency. The global commercial fleet average age reached 15.1 years as of end-2025 — a record high — compared to a long-term historical average of 13.6 years from 1990 to 2024, according to IATA. Older aircraft require more frequent component replacements, and the USM supply chain is the most cost-efficient mechanism for meeting that maintenance load.

OEM supply constraints compound the problem. New part lead times for certain components extended to 200 days or more in 2025–2026, according to Werner Aero CEO Tony Kondo. USM, available immediately upon recertification, eliminates that delay — making it strategically critical for minimizing aircraft-on-ground (AOG) time and keeping airline operations intact.

According to Aerospace Global News, the global order backlog surpassed 17,000 aircraft as of end-2025 — equal to roughly 60% of the active fleet and representing nearly 12 years of output at current production rates. This backlog tells us that new aircraft supply cannot resolve fleet maintenance pressure for the foreseeable future, anchoring USM as a permanent procurement strategy rather than a cyclical stopgap.

According to Oliver Wyman, aircraft production in 2025 was 24% below 2019 levels, while average flight hours per aircraft rose 2% year-over-year. That combination — fewer new planes, more hours on existing ones — means component wear accelerates while replacement supply remains constrained, creating favorable conditions for USM market expansion across all fleet categories and operator types.

Key Takeaways

- The global Air Transport USM Market was valued at USD 7.7 Billion in 2025 and is forecast to reach USD 12.3 Billion by 2035.

- The market grows at a CAGR of 4.8% during the forecast period 2026 to 2035.

- By Provider Type, OEM leads with a market share of 65.9% in 2025.

- By Aircraft Type, Narrowbody Jet holds the dominant share at 53.7% in 2025.

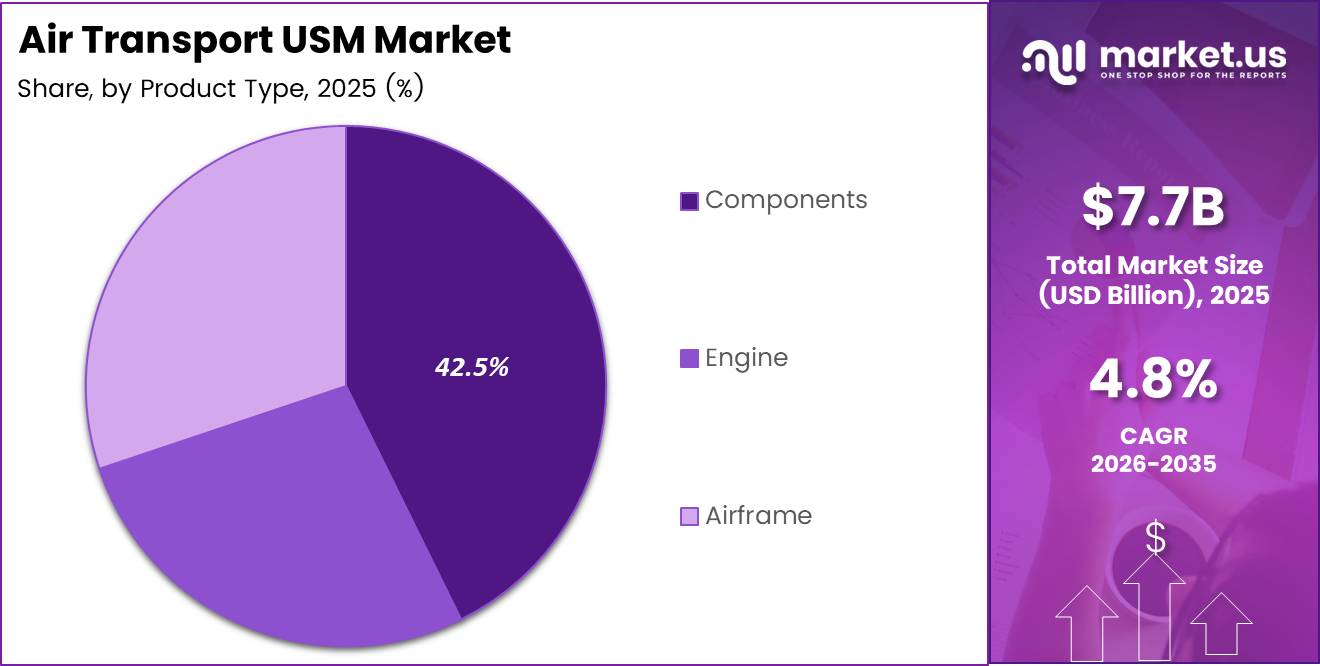

- By Product Type, Components leads the segment with a 42.5% market share in 2025.

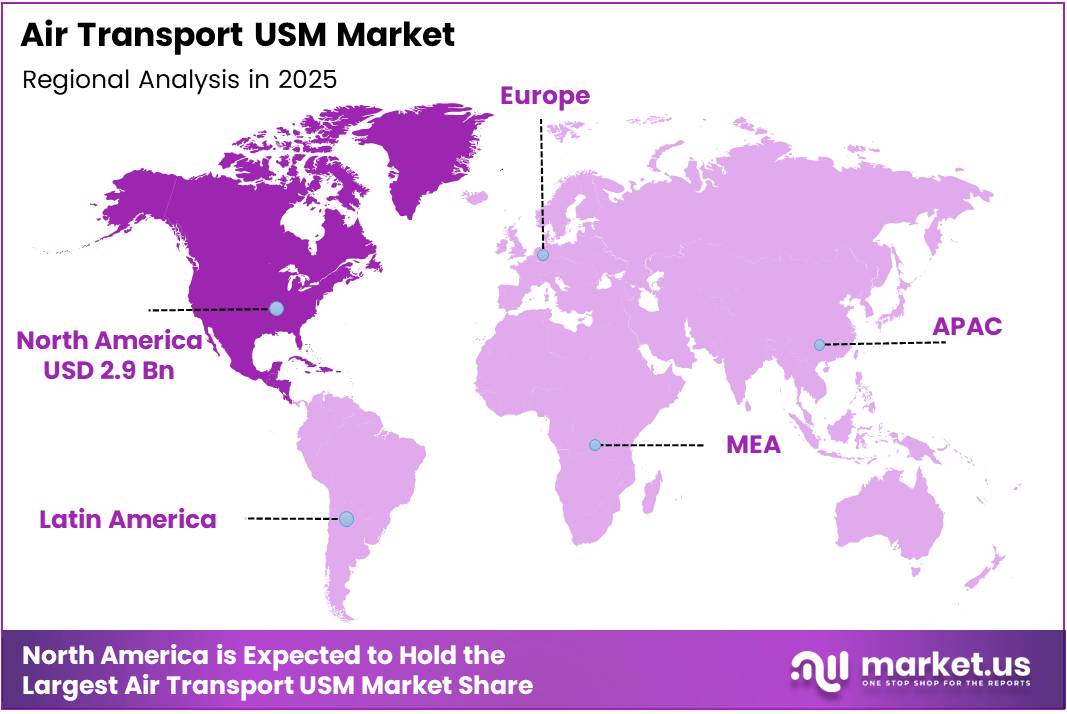

- North America dominates the regional landscape with a 37.90% share, valued at USD 2.9 Billion in 2025.

Product Type Analysis

Components dominates with 42.5% due to broad fleet-wide replacement frequency.

In 2025, Components held a dominant market position in the By Product Type segment of the Air Transport USM Market, with a 42.5% share. This category covers line-replaceable units, avionics, landing gear parts, and structural components — items that cycle through replacement more frequently than engines or full airframes. Their high replacement volume and immediate recertification turnaround make them the most liquid and commercially active segment within the USM ecosystem.

Engine USM carries the highest individual unit value within aviation spare parts procurement. Recertified engines and engine modules command premium pricing relative to components, but they still offer operators significant savings versus new OEM purchases — particularly relevant as engine shop visit turnaround times rose by more than 150% for new-generation engines compared to pre-pandemic levels. Airlines sourcing USM engines bypass both new-part lead times and extended shop queues simultaneously.

Airframe USM serves as the structural feedstock of the part-out economy. Retired aircraft yield structural panels, fuselage sections, and flight control surfaces — all recertifiable under regulatory traceability requirements. Airframe material supply depends directly on retirement rates; with A320-200 retirements declining approximately 10% year-on-year since 2023 according to IBA Insight, airframe USM remains supply-constrained, sustaining elevated pricing across the segment.

Provider Type Analysis

OEM dominates with 65.9% due to established traceability and certification infrastructure.

In 2025, OEM held a dominant market position in the By Provider Type segment of the Air Transport USM Market, with a 65.9% share. OEM-sourced USM carries inherent buyer confidence because the original manufacturer’s documentation, serial traceability, and airworthiness history travel with the part. For airlines operating under strict regulatory oversight, this traceability advantage justifies OEM-sourced USM as the default procurement choice over third-party alternatives.

Non-OEM providers differentiate through speed and pricing flexibility, often serving as the primary channel for operators who need immediate part availability outside standard OEM supply networks. Non-OEM distributors source material from teardowns, airline surplus, and leasing company disposals, processing and recertifying parts through approved maintenance organizations. Their competitive position strengthens when OEM channels face supply bottlenecks — a condition that has been persistent since 2022.

Aircraft Type Analysis

Narrowbody Jet dominates with 53.7% due to highest global fleet count and maintenance frequency.

In 2025, Narrowbody Jet held a dominant market position in the By Aircraft Type segment of the Air Transport USM Market, with a 53.7% share. The global narrowbody fleet — dominated by Boeing 737 and Airbus A320 family variants — represents the largest single aircraft population in commercial aviation. High daily utilization rates and shorter maintenance intervals mean narrowbody operators generate USM demand at a structurally higher frequency than any other category. Consequently, the narrowbody USM segment commands the deepest buyer and seller liquidity.

Widebody Jet USM carries the highest per-transaction value within the aircraft type breakdown. Wide-body engines, landing gear systems, and fuselage sections command premium unit economics when sourced as USM. Moreover, widebody cargo aircraft — with an average fleet age of 19.6 years as of end-2025 — represent the oldest operational category in the commercial fleet, generating disproportionately high component replacement demand relative to fleet size.

Turboprop USM serves regional and commuter operators where new OEM parts often carry delivery timelines incompatible with short-haul network economics. Turboprop fleets typically operate in markets with thinner margins, making USM an essential procurement mechanism rather than a discretionary cost-saving option. Consequently, turboprop USM demand remains structurally stable regardless of broader market cycles.

Regional Jet USM addresses the maintenance needs of operators running Bombardier CRJ and Embraer ERJ fleets, where manufacturer support lifecycles for older variants have diminished. As OEM support contracts expire on legacy regional jets, operators shift procurement entirely to secondary market channels — positioning USM distributors with regional jet expertise in a defensible and growing niche.

Key Market Segments

By Provider Type

- OEM

- Non-OEM

By Aircraft Type

- Narrowbody Jet

- Widebody Jet

- Turboprop

- Regional Jet

By Product Type

- Components

- Engine

- Airframe

Drivers

Aging Global Fleet and OEM Supply Shortfalls Force Structural Dependency on USM Procurement

The global commercial fleet reached an average age of 15.1 years in 2025 — the highest on record — while OEM production remained 24% below 2019 levels. This combination means airlines cannot retire aging aircraft and cannot receive replacements fast enough. Therefore, USM becomes the only operationally viable mechanism for sustaining airworthiness across fleets that now fly more hours than ever before.

According to Oliver Wyman, global MRO demand reached $136 billion in 2025, up 8% from $126 billion in 2024, with engine maintenance alone totaling $62.4 billion. That scale of maintenance activity translates directly into USM procurement volume — airlines managing billions in maintenance spend actively prioritize cost-efficient component sourcing. The USM market captures a growing share of that spend wherever OEM lead times or pricing create procurement gaps.

Supply chain disruptions remain the operational reality of 2025–2026. New OEM part lead times extended to 200 days or more for certain components, while Collins Aerospace launched its Powered by Collins Initiative in February 2025 specifically to accelerate collaboration with supply chain partners on material availability. However, until OEM output normalizes, airlines will continue directing procurement budgets toward USM to prevent AOG events that cost operators revenue daily.

Restraints

Certification Complexity and Regulatory Scrutiny Limit USM Acceptance Across Airline Procurement Functions

Aviation safety regulators — including EASA and the FAA — apply stringent airworthiness standards to all used parts entering the supply chain. Every USM component requires documented traceability back to its last certified operator, a condition that eliminates significant quantities of potentially serviceable material due to incomplete or unverifiable maintenance records. This certification barrier directly limits the volume of USM that qualifies for sale and narrows supplier choice for buyers.

According to an IATA survey published in October 2025, 82% of airline respondents cited part availability as a primary driver of alternative parts adoption — but the same survey reveals that trust and traceability remain active concerns. This statistic highlights a market where demand is structural but uptake is moderated by institutional risk aversion, particularly among full-service carriers operating under strict quality assurance frameworks that require documented part histories.

Limited traceability infrastructure penalizes sellers as much as buyers. USM distributors unable to produce complete maintenance documentation face buyer rejection and depressed pricing regardless of the part’s physical condition. Consequently, the market structurally favors distributors who invest in digital traceability systems — creating a two-tier supplier environment where documentation quality determines market access as much as part availability does.

Growth Factors

Aircraft Teardown Activity and Digital Marketplace Expansion Open New USM Supply and Distribution Channels

According to AviTrader, USM parts offer savings of 60%–80% less than the cost of new OEM parts — a pricing differential that makes USM economically compulsory for airlines managing aging fleets under constrained capital budgets. That cost advantage, sustained by structural OEM supply shortfalls, positions USM not as a compromise procurement option but as the financially rational default for maintenance purchasing decisions across fleet categories.

Aircraft teardown programs directly expand the available USM supply pool. Boeing’s Aircraft Recycling Program — launched in 2025 — recovers material recovery rates of up to 90% for metallic airframes, with a single retired commercial aircraft yielding up to 6,000 reused and recertified parts. Additionally, in March 2025, GE Aerospace announced plans to invest nearly $1 billion in U.S. manufacturing and supply chain capacity, hiring approximately 5,000 workers — signaling that major players are scaling infrastructure to support both OEM and USM part ecosystems simultaneously.

Digital marketplaces for aircraft parts reduce transaction friction across the USM supply chain, enabling buyers to source globally rather than relying on established regional distributor networks. This accessibility widens the potential buyer base, particularly for smaller operators and regional carriers who previously lacked procurement scale to access premier USM distributors. Expanded market access also increases price competition among sellers, benefiting buyers and stimulating overall transaction volume.

Emerging Trends

Blockchain Traceability and AI-Based Inventory Tools Reshape USM Market Infrastructure

According to an IATA survey from October 2025, 74% of 46 surveyed airlines confirmed active use of alternative parts — including USM — within their fleets, with nearly three-quarters of those carriers expanding that use. This level of institutional adoption signals that USM is no longer a marginal procurement strategy. Airlines now treat used serviceable material as a structured supply chain category, which increases demand for technology tools that manage USM inventory and verify part histories at scale.

Blockchain integration for USM parts traceability directly addresses the certification challenge that currently constrains market growth. Distributed ledger records create immutable maintenance histories that travel with each part — eliminating the documentation gaps that exclude viable material from the certified supply pool. Early movers who build blockchain-backed USM platforms gain a verifiable quality advantage that justifies premium pricing and accelerates buyer acceptance among quality-sensitive airline procurement teams.

AI-based inventory management tools allow MRO providers and USM distributors to forecast part demand across fleet types and maintenance cycles, reducing both stockout risk and excess inventory holding costs. Additionally, aircraft leasing companies — which manage large secondary-market part disposals when leases terminate — increasingly partner with USM specialists to optimize the commercial value of recovered material. These partnerships create a more structured and predictable USM supply chain than the historically fragmented part-out market has offered.

Regional Analysis

North America Dominates the Air Transport USM Market with a Market Share of 37.90%, Valued at USD 2.9 Billion

North America leads the global Air Transport USM market with a 37.90% share, valued at USD 2.9 Billion in 2025. The region’s dominance reflects its concentration of major MRO facilities, established USM distribution networks, and the FAA’s mature part traceability framework, which gives North American-certified USM a recognized compliance benchmark that accelerates buyer acceptance both domestically and in export markets.

Europe Air Transport USM Market Trends

Europe holds the second-largest share, driven by EASA’s harmonized airworthiness certification framework and a high density of legacy carrier fleets requiring sustained component replacement. European MRO hubs in Germany, France, and the UK actively source USM to manage maintenance costs on aging narrowbody and widebody fleets. The region’s regulatory alignment with North America also facilitates bilateral USM trade across the Atlantic.

Asia Pacific Air Transport USM Market Trends

Asia Pacific represents the highest-growth regional opportunity within the USM market. Rapid expansion of low-cost carrier fleets across Southeast Asia, India, and China has created large maintenance backlogs that OEM supply chains cannot address at current capacity. Regional MRO operators in Singapore, China, and India are actively building USM procurement capabilities to serve fast-growing but cost-sensitive airline operators across the region.

Middle East and Africa Air Transport USM Market Trends

The Middle East functions as a strategic transshipment hub for USM distribution between Europe, Asia, and Africa. Gulf-based MRO operators serve as regional aggregators of certified parts, leveraging free zone trade infrastructure to streamline USM import and re-export. Africa’s aviation market, constrained by capital access, relies heavily on secondary market parts to keep aging regional fleets operational across thin-margin routes.

Latin America Air Transport USM Market Trends

Latin America’s USM demand concentrates in Brazil and Mexico, where established MRO infrastructure and growing LCC fleets create consistent component replacement requirements. Currency volatility and import duty structures make new OEM parts financially prohibitive for many regional operators, reinforcing USM as the default procurement channel. Brazil’s ANAC regulatory framework increasingly aligns with FAA standards, improving the acceptability of internationally certified USM within the domestic market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AJ Walter Aviation Limited positions itself as a full-spectrum USM and component services provider, covering both OEM and non-OEM material across narrowbody and widebody platforms. Its strategic advantage lies in proprietary inventory depth and long-term airline customer agreements, which generate recurring demand rather than transactional spot purchases. In May 2025, AJW Group launched the LARA initiative — a structured program balancing new and serviceable material procurement — directly addressing the supply chain gaps that define this market.

AAR Corp. operates across MRO services, parts supply, and government aviation support, giving it a diversified revenue structure that insulates it from single-segment pricing cycles. Its acquisition of Triumph Group’s Product Support business in March 2024 for $725 million expanded its component capabilities significantly, while the subsequent sale of its Landing Gear Overhaul division to GA Telesis in April 2025 for $51 million sharpens its strategic focus on higher-margin USM and parts trading activities.

AerSale Inc. centers its competitive positioning on aircraft teardown-to-USM conversion, capturing value at the feedstock stage of the supply chain rather than relying solely on secondary market trading. This vertical integration — from acquiring end-of-life aircraft through recertification to sale — gives AerSale greater margin control and more predictable inventory supply than pure-play distributors. Its focus on narrowbody platforms aligns directly with the segment commanding the largest USM demand share.

Boeing Company entered the USM supply chain as a strategic participant through its Aircraft Recycling Program, launched in 2025, which recovers material recovery rates of up to 90% for metallic airframes and yields up to 6,000 recertified parts per retired aircraft. Boeing’s participation signals OEM recognition that the USM market is a permanent structural feature of aviation supply chains — and that controlling USM feedstock protects OEM revenue relationships with airline customers during periods of new-aircraft supply constraint.

Key Players

- AJ Walter Aviation Limited

- AAR Corp.

- AerSale Inc.

- Boeing Company

- Delta TechOps

- GA Telesis, LLC

- General Electric

- HEICO Corporation

- Liebherr Group

Recent Developments

- March 2024 — AAR Corporation completed the acquisition of Triumph Group’s Product Support business for $725 million. This transaction, announced in December 2023 and closed on March 1, 2024, expanded AAR’s component MRO capabilities and strengthened its position in the aviation aftermarket parts supply chain.

- April 2025 — AAR Corporation completed the sale of its Landing Gear Overhaul business to GA Telesis for $51 million. Announced in December 2024 and closed in April 2025, this divestiture refocused AAR’s operational strategy on higher-margin USM trading and parts supply activities.

- May 2025 — AJW Group launched the LARA (Lifecycle Asset Reuse and Availability) initiative to systematically balance new and serviceable material procurement. This program directly targets the supply chain fragmentation challenges that constrain USM market efficiency and buyer confidence across airline and MRO procurement functions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.7 Billion |

| Forecast Revenue (2035) | USD 12.3 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Provider Type (OEM, Non-OEM), By Aircraft Type (Narrowbody Jet, Widebody Jet, Turboprop, Regional Jet), By Product Type (Components, Engine, Airframe) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AJ Walter Aviation Limited, AAR Corp., AerSale Inc., Boeing Company, Delta TechOps, GA Telesis LLC, General Electric, HEICO Corporation, Liebherr Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |