Quick Navigation

- Report Overview

- Key Insight Summary

- Analysts’ Viewpoint

- North America Industry Revenue

- Growth Factors

- Emerging Trends

- Component Analysis

- Deployment Analysis

- Technology Analysis

- Application Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity Analysis

- Challenge Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

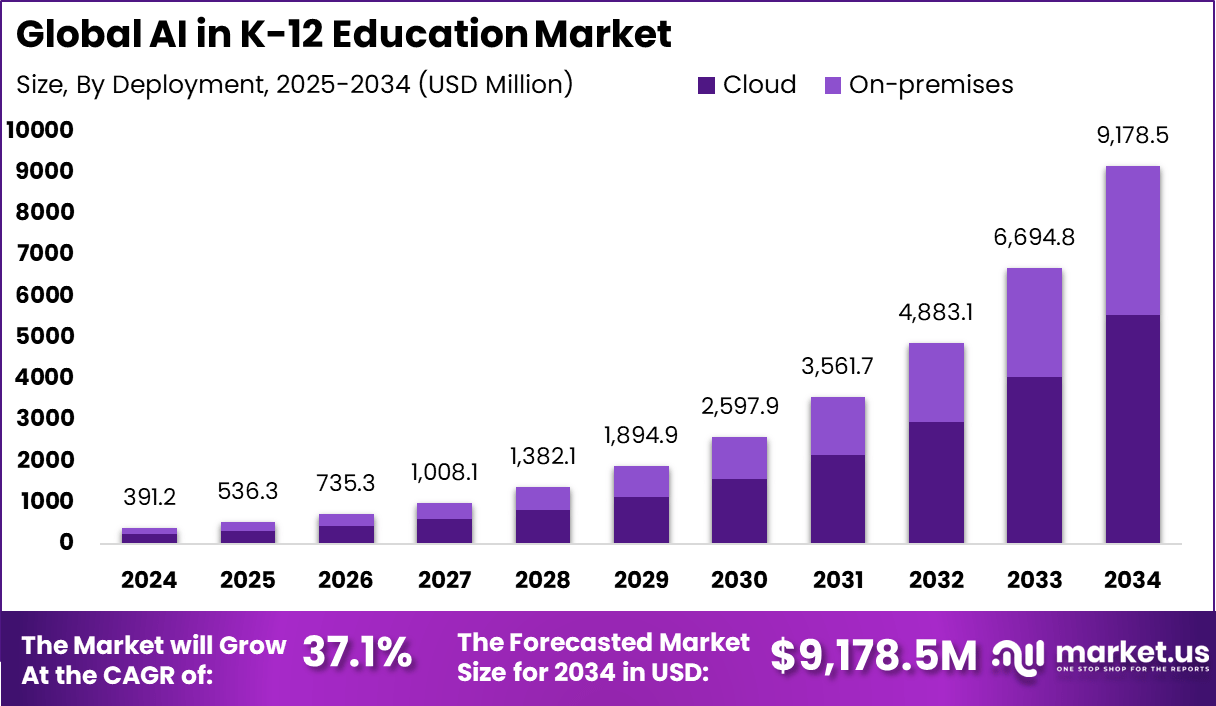

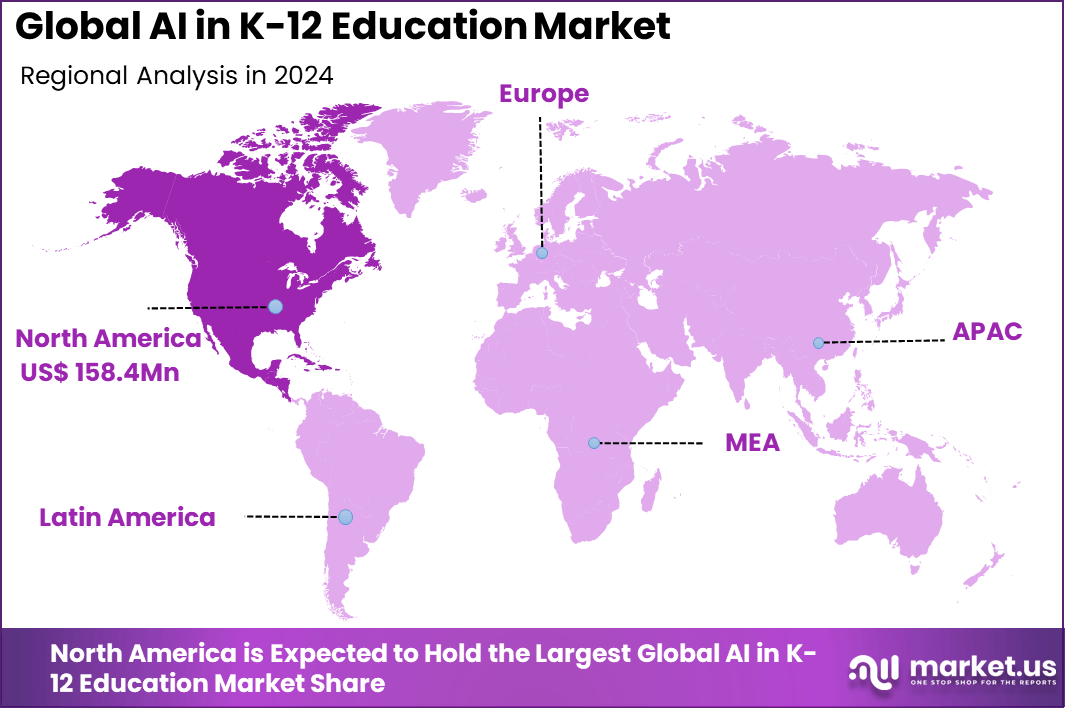

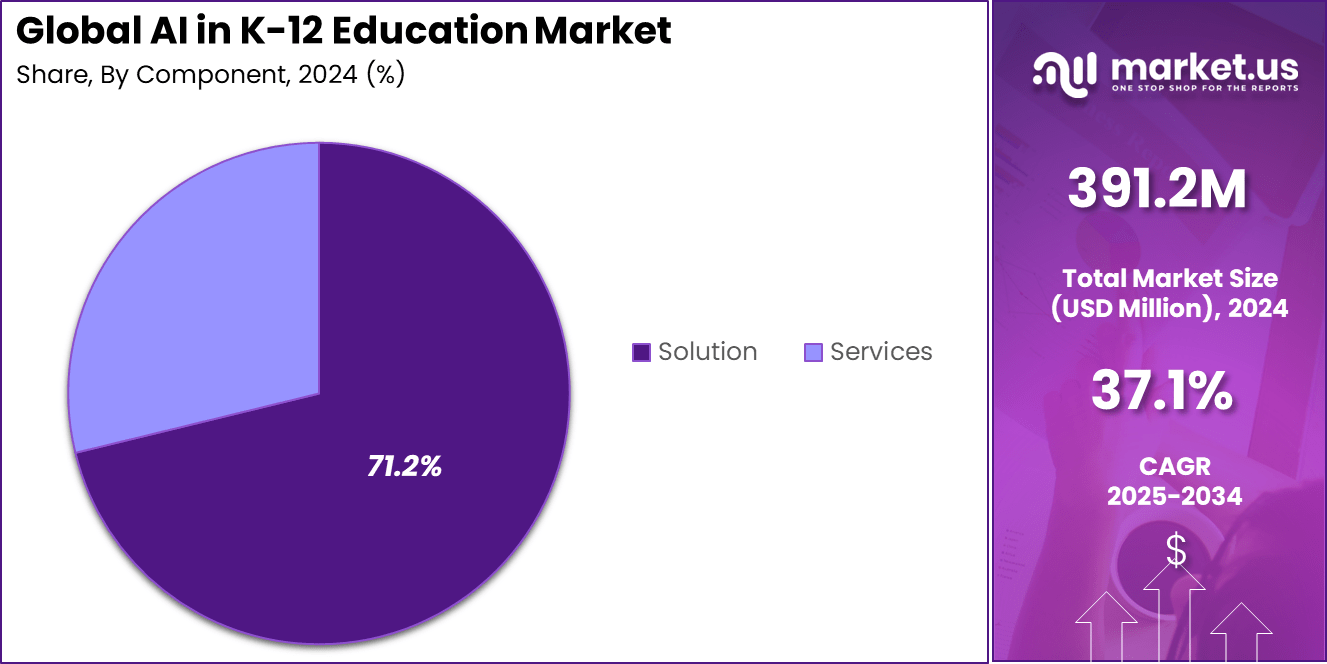

The Global AI in K-12 Education Market size is expected to be worth around USD 9,178.5 Million By 2034, from USD 391.2 Million in 2024, growing at a CAGR of 37.1% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40.5% share, holding USD 158.4 Million revenue.

The AI in K‑12 education market can be described as the integration of machine learning, natural language processing, intelligent tutoring systems, automated grading, and adaptive learning platforms into primary and secondary schooling environments. It is characterized by the deployment of software tools that personalize instruction, automate administrative tasks, and support educators with real‑time analytics.

According to Market.us reports that the Global K-12 EdTech Market is projected to grow from USD 78.2 billion in 2023 to USD 253.9 billion by 2033, registering a CAGR of 12.5% during the forecast period. This growth aligns with increasing investment in AI-driven tools and platforms aimed at transforming classroom instruction and administrative efficiency.

The principal drivers include the rising demand for personalized learning experiences that adapt to each student’s pace and capability, and the need for scalable solutions to manage increasing classroom complexity. Technological advancement in AI algorithms, combined with institutional investments in digital infrastructure and teacher training, further fuels momentum.

Market Size and Growth

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 391.2 Mn |

| Forecast Revenue (2034) | USD 9,178.5 Mn |

| CAGR(2025-2034) | 37.1% |

| Leading Segment | Solution: 71.2% |

| Largest Market | North America [40.5% Market Share] |

According to Engageli, 60% of teachers have already embedded AI into their teaching practices, with 44% time savings observed in tasks like lesson planning and content creation. Additionally, 89% of students admit to using ChatGPT for homework, and 86% of education organizations have adopted generative AI, making education the leading industry in AI adoption.

Personalized AI-driven learning has shown to improve student outcomes by up to 30%, highlighting its transformative potential. Data from AISTATISTICS further reveals that 51% of teachers now prefer AI-powered educational games over other tools. Around 3 in 5 educators are actively using AI in their classrooms.

However, 65% of teachers cite plagiarism as a top concern, especially with essay assignments. Public opinion remains divided, with 33% of U.S. adults believing AI has had a negative impact on education, while 32% see it positively. Still, 60% of teachers expect AI to become even more widespread in the coming decade.

Key Insight Summary

- The market is projected to expand from USD 391.2 million in 2024 to approximately USD 9,178.5 million by 2034, growing at a strong CAGR of 37.1%.

- North America led the global market in 2024 with a 40.5% share, generating around USD 158.4 million in revenue, supported by early adoption of EdTech solutions.

- Solutions dominated the component segment, capturing 71.2%, driven by the demand for AI-enabled learning tools and personalized content delivery.

- The cloud deployment model accounted for 60.5%, due to its scalability, cost-efficiency, and ease of integration across schools.

- Machine Learning was the top-used technology, holding 65.2%, as it powers adaptive learning, performance tracking, and predictive student analytics.

- The leading application was Learning Platforms & Virtual Facilitators, reflecting the shift toward interactive, AI-guided, and self-paced digital learning environments.

Analysts’ Viewpoint

Opportunities for investment exist in professional development platforms that train educators on AI, development of responsible AI tools aligned with policy frameworks, and scalable cloud‑based solutions for underserved schools. Additionally, partnerships between public sector bodies and private stakeholders are creating spaces for joint innovation in AI literacy and curriculum design.

Benefits to educational institutions include greater operational efficiency through automated attendance, grading, and feedback; better student outcomes via tailored learning paths; and improved teacher satisfaction as time is freed for direct interaction. Implementation of analytics supports timely interventions for struggling learners.

Policy guidance is evolving rapidly. In the United States, federal education bodies now endorse AI tools in schools, offer grants for AI technology adoption, and promote initiatives to train educators in AI use. Ethical guidelines, privacy protections, and responsibility frameworks are being emphasized to ensure transparency and trust.

North America Industry Revenue

In 2024, North America held a dominant market position, capturing more than a 40.5% share, holding USD 158.4 million in revenue in the AI in K-12 Education Market. This leadership can be attributed to the region’s robust digital infrastructure and high investment in EdTech innovations.

The United States, in particular, has seen widespread deployment of AI-powered tools such as personalized learning platforms, automated grading systems, and intelligent tutoring programs in public and private school systems. Strong partnerships between schools, government agencies, and AI companies have further accelerated the adoption rate.

The region’s early integration of one-to-one device programs and cloud-based learning management systems has laid a strong foundation for AI applications. Federal and state-level funding programs aimed at advancing digital equity and personalized learning have ensured that even rural and underserved districts gain access to AI-driven educational tools.

Moreover, North American schools benefit from a high level of teacher training in AI-enabled platforms, allowing smoother implementation across grade levels. These conditions collectively position North America as the frontrunner in leveraging artificial intelligence to enhance K-12 learning outcomes.

Growth Factors

| Key Factor | Description |

|---|---|

| Personalized Learning | AI customizes instruction to fit individual student needs, improving engagement and outcomes. |

| Digital Learning Expansion | Increased adoption of digital platforms enables flexible, remote, and inclusive AI-driven education. |

| Administrative Efficiency | Automates grading, attendance, and reporting, freeing up teacher time for instruction and support. |

| Data-driven Insights | Real-time analytics allow educators to identify and address student learning gaps efficiently. |

| Equity and Accessibility | AI tools support diverse needs with features for language, disability, and culturally relevant content. |

Emerging Trends

| Emerging Trend | Description |

|---|---|

| Generative AI Content | AI creates lesson plans, assignments, and materials, reducing workload and enabling curriculum updates. |

| Adaptive Learning Platforms | Platforms such as Squirrel AI and DreamBox tailor lessons in real time based on student performance. |

| AI-powered Tutoring | Chatbots and virtual tutors provide on-demand, personalized support and feedback to students. |

| Immersive & Gamified Learning | AI integrates with AR/VR and gamification for engaging, participatory learning experiences. |

| Focus on Data Security | Emphasis on responsible AI use and student data privacy shapes adoption and tool development. |

Component Analysis

In 2024, the solution segment dominated the AI in K-12 education market, accounting for approximately 71 % of global revenue share in 2024. This dominance reflects significant institutional investment in AI-driven platforms, applications, and systems that enable personalized learning, real‑time analytics, automated assessment, and adaptive content delivery.

Institutions have prioritized software over professional services in order to integrate scalable AI capabilities directly into classrooms and administrative functions. The robust share held by solutions underscores the centrality of packaged, technology‑led offerings in driving market expansion.

Strong demand for learning management systems, intelligent tutoring systems, and virtual classroom platforms has elevated the role of solutions. These offerings allow educators to tailor instructional paths, automate grading, and track student performance with enhanced efficiency. As such, the solution component continues to serve as the foundational pillar of AI market growth within K-12 education.

Deployment Analysis

Cloud deployment led AI adoption in K‑12 education with around 60 % of market share in 2024, offering the greatest flexibility, accessibility, and scalability to educational stakeholders . The cloud model enables anytime‑anywhere access to AI tools, supporting hybrid and remote learning models and easing integration across diverse devices and learning contexts.

Institutions favoring cloud infrastructure benefit from rapid onboarding, lower maintenance overhead, and the ability to scale resources in response to fluctuating student and user demand. The cloud ecosystem also facilitates seamless updates and deployment of new AI capabilities, positioning it as the preferred deployment choice in the K‑12 segment.

Technology Analysis

Machine Learning (ML) holds the largest technology share in the AI K‑12 education market – approximately 65 % in 2024 – driven by its role in powering adaptive learning platforms, predictive analytics, and behavior analytics systems. ML algorithms enable customized learning paths by analyzing students’ performance, engagement patterns, and learning styles, thereby enhancing instructional responsiveness.

The dominance of ML is attributed to its proven capabilities in creating dynamic and personalized learning environments. While NLP and deep learning segments are growing rapidly, ML retains the majority share due to widespread deployment in existing systems that support real‑time adaptation and personalized feedback mechanisms.

Application Analysis

The learning platform & virtual facilitators segment accounted for the largest revenue share in application terms in 2024 – estimated at 47 % of the AI in education market. These platforms integrate AI‑based tutoring agents, content management systems, assessment tools, and interactive interfaces into unified ecosystems that enhance teaching and learning.

AI-powered virtual facilitators support real‑time question answering, guide customized learning pathways, and provide automated feedback to students. Learning platforms consolidate assignments, assessment, and collaboration tools into accessible environments across devices, improving student engagement and retention

Key Market Segments

By Component

- Solution

- Services

By Deployment

- Cloud

- On-premises

By Technology

- Natural Language Processing (NLP)

- Machine Learning

By Application

- Learning Platform & Virtual Facilitators

- Intelligent Tutoring System (ITS)

- Smart Content

- Fraud and Risk Management

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Demand for Personalized Learning and Efficiency

The growth of personalized learning demand is fueling adoption of AI tools that can deliver tailored instruction and adaptive assessments. Educators and administrators are drawn to AI’s ability to reduce time spent on routine tasks, reduce administrative burden, and improve learning performance through data-informed interventions.

In addition, the broader digital transformation of education systems is enabling more scalable and flexible platforms. Institutions are moving toward cloud‑based systems that support remote access and data analytics, which in turn reinforce the drive toward AI deployment to optimize content delivery and institutional oversight.

Restraint

Equity and Privacy Concerns

Significant digital access disparities continue to limit equitable deployment of AI in many K‑12 settings, particularly in rural and low‑income communities. Availability of reliable internet connectivity and sufficient hardware remains inconsistent, leading to unequal access to AI‑based platforms .

Further, data privacy and algorithmic fairness concerns present substantial obstacles. Many AI tools collect sensitive student information and lack transparent mechanisms for auditing. Regulatory uncertainty and uneven compliance across regions have prompted delayed or suspended AI implementations in multiple jurisdictions.

Opportunity Analysis

Teacher Support and Professional Learning

AI systems that assist educators with lesson planning, grading, and administration are increasing operational efficiency and freeing time for instructional engagement. Surveys show that a majority of K‑12 teachers using AI tools report substantial weekly time savings and more focus on direct student interaction.

In response, professional learning communities and teacher training initiatives are being launched to support responsible AI integration. Federal, state and union‑led programs now emphasize guidance on ethical use, AI literacy, and inclusive curriculum design, which creates opportunities for scaling AI as a teacher support tool rather than technology that replaces human agency.

Challenge Analysis

Ethical Bias and Critical Thinking Impact

AI tools such as automated graders and generative language models carry risks of bias and reduction in human judgement. Evidence shows that some AI‑supported assessment platforms have misclassified responses from non‑native English speakers or marginalized students, raising fairness concerns in evaluation and feedback processes.

Moreover, over‑reliance on AI for explanations or solutions may diminish opportunities for critical thinking development. Critics argue that constant use of generative AI may shift student focus toward shortcuts rather than deeper inquiry, unless curricular strategies explicitly cultivate analytical reasoning and digital literacy.

Key Player Analysis

In the AI in K-12 education space, major technology players like IBM Corporation, Amazon Web Services, Inc., and Google LLC have taken early leadership positions. Their advanced AI infrastructure and cloud platforms are enabling personalized learning, real-time data analytics, and intelligent tutoring systems across classrooms. These companies are focused on integrating speech recognition, predictive analytics, and adaptive content delivery.

Key education-focused firms such as Pearson Plc, Cognizant, and Graham Holdings Company are also actively shaping this sector. Pearson is leveraging AI to enhance its digital textbooks and assessment tools, helping students progress at their own pace. Cognizant contributes with AI-driven consulting services that optimize digital learning strategies for schools.

Established educational publishers like McGraw Hill, Nuance Communications, Inc., and Houghton Mifflin Harcourt are modernizing their offerings by embedding AI in learning management systems and content platforms. McGraw Hill emphasizes adaptive learning solutions powered by data science. Nuance contributes through voice-driven applications that assist in language development and accessibility.

Top Key Players in the Market

- IBM Corporation

- Amazon Web Services, Inc.

- Google LLC

- Pearson Plc

- Cognizant

- Graham Holdings Company

- McGraw Hill

- Nuance Communications, Inc.

- Houghton Mifflin Harcourt

Recent Developments

- June 2025: Pearson and Google Cloud announced a major strategic partnership to co-develop AI-driven educational tools specifically for the K-12 segment. This collaboration will see advanced AI infrastructures (Vertex AI) integrated into Pearson’s virtual school ecosystem to build personalized learning platforms and data-driven tools for teachers and students

- Also in June 2025, Michigan Virtual University collaborated with the AI Education Project (aiEDU) to promote AI literacy and readiness across Michigan’s K-12 system. This partnership aims to enhance teacher support and leverage the state’s existing instructional tech networks to accelerate AI integration in classrooms.

- September 2024: AWS entered a pivotal partnership with Magic EdTech, designed to empower K-12 education with advanced AI-powered digital learning. This collaboration brings together AWS’s robust cloud infrastructure and Magic EdTech’s learning expertise to streamline content creation and deliver highly personalized digital experiences for schools.

Report Scope

| Report Features | Description |

|---|---|

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | Component (Solution, Services), By Deployment (Cloud, On-premises), By Technology(Natural Language Processing (NLP), Machine Learning), By Application (Learning Platform & Virtual Facilitators, Intelligent Tutoring System (ITS), Smart Content, Fraud and Risk Management, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amazon Web Services, Inc., IBM Corporation, Google LLC, Pearson Plc, Cognizant, Graham Holdings Company, McGraw Hill, Nuance Communications, Inc., Houghton Mifflin Harcourt |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |