Quick Navigation

- Report Overview

- Key Takeaways

- U.S. AI Accelerator Market

- Type Analysis

- Technology Analysis

- End-Use Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

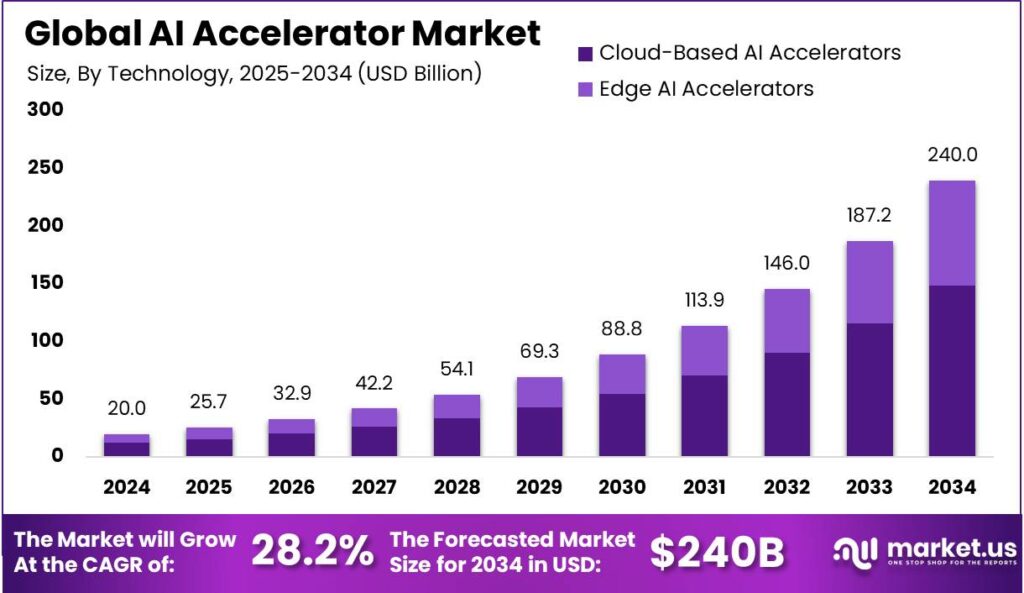

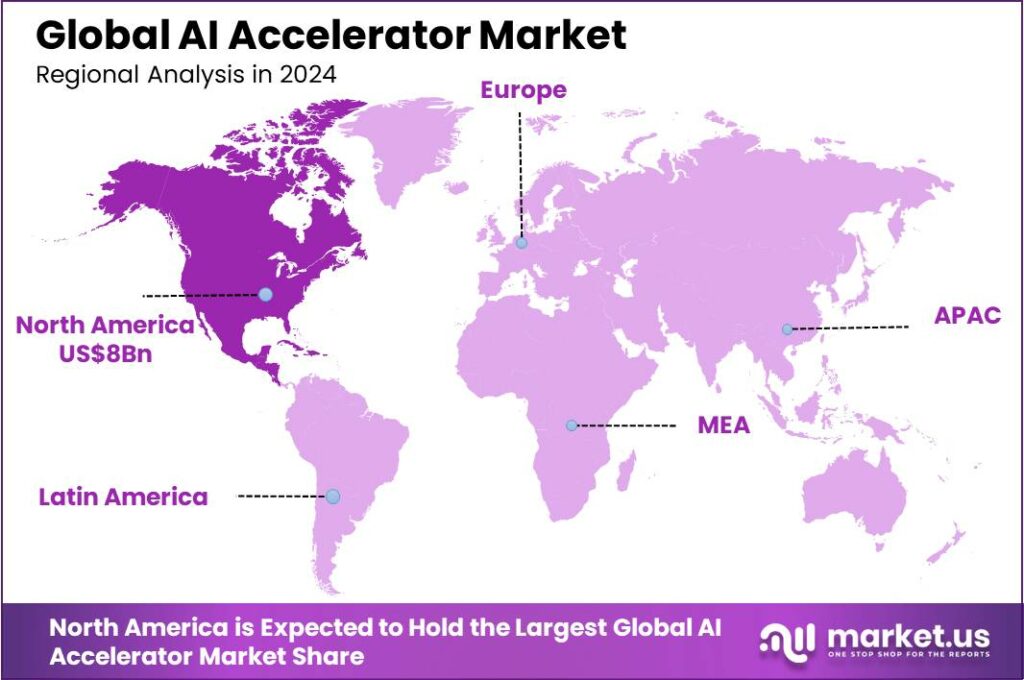

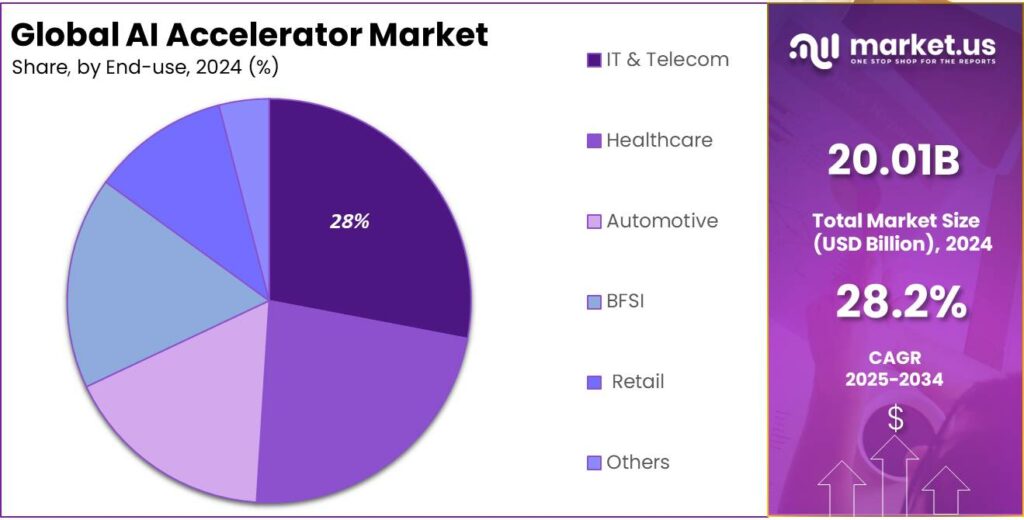

The Global AI Accelerator Market size is expected to be worth around USD 240 Billion By 2034, from USD 20.01 Billion in 2024, growing at a CAGR of 28.20% during the forecast period from 2025 to 2034. In 2024, North America led the global AI Accelerator Market with a 40% market share and USD 8 billion in revenue.

An AI accelerator is a specialized hardware component or software-based system designed to speed up artificial intelligence (AI) applications, particularly those involving deep learning and machine learning. These accelerators are designed to handle complex computations at high speeds, efficiently processing large volumes of data, which is crucial for training and deploying AI models.

The AI accelerator market encompasses the global industry focused on producing and distributing technologies like GPUs, ASICs, FPGAs, and TPUs. These accelerators are integrated into a wide range of devices across sectors such as automotive, healthcare, finance, and telecommunications.

The growth of the AI accelerator market is driven by the rising demand for AI technologies across industries like automotive, healthcare, and consumer electronics, which require powerful computational resources for machine learning tasks. Additionally, the increasing volumes of data from various sources demand more efficient processing capabilities to manage complex algorithms and real-time analytics.

Advancements in AI and machine learning algorithms, along with increased demand for specialized hardware, are driving AI accelerator market growth. Government and private sector support through investments and policies for AI R&D further fuel market expansion, enhancing AI capabilities and accessibility globally.

AI accelerators are becoming more popular for their ability to speed up data processing and analysis. Their adoption is driven by the increasing integration of AI and machine learning in applications like voice recognition and algorithmic trading. The rise of cloud services and IoT devices also boosts the demand for AI accelerators, enhancing the performance and responsiveness of these technologies.

The market offers opportunities for innovation, particularly in developing energy-efficient, high-performance accelerators for mobile devices and edge computing. As AI applications expand in emerging markets, there is significant potential for deploying advanced AI accelerators, driving growth and investment.

Market expansion in the AI accelerator sector is set to expand rapidly, driven by advancements in AI algorithms and the rise of AI applications across industries. Emerging markets offer significant potential, fueled by digital transformation. Collaborations between manufacturers and tech companies will also spur innovations, enhancing AI capabilities and accessibility, further boosting market growth.

Key Takeaways

- The Global AI Accelerator Market is projected to grow significantly, reaching an estimated value of USD 240 Billion by 2034, up from USD 20.01 Billion in 2024, with a CAGR of 28.20% during the forecast period from 2025 to 2034.

- In 2024, the Graphics Processing Units (GPUs) segment dominated the market, capturing over 59.6% of the total share in the AI accelerator market.

- The cloud-based AI accelerators segment also held a dominant position in 2024, commanding over 62% of the market share.

- The IT & Telecom sector held the largest share in the AI Accelerator Market in 2024, accounting for more than 28% of the total market.

- North America led the global AI Accelerator Market in 2024, with a market share of over 40%, and the region’s revenue was valued at approximately USD 8 billion.

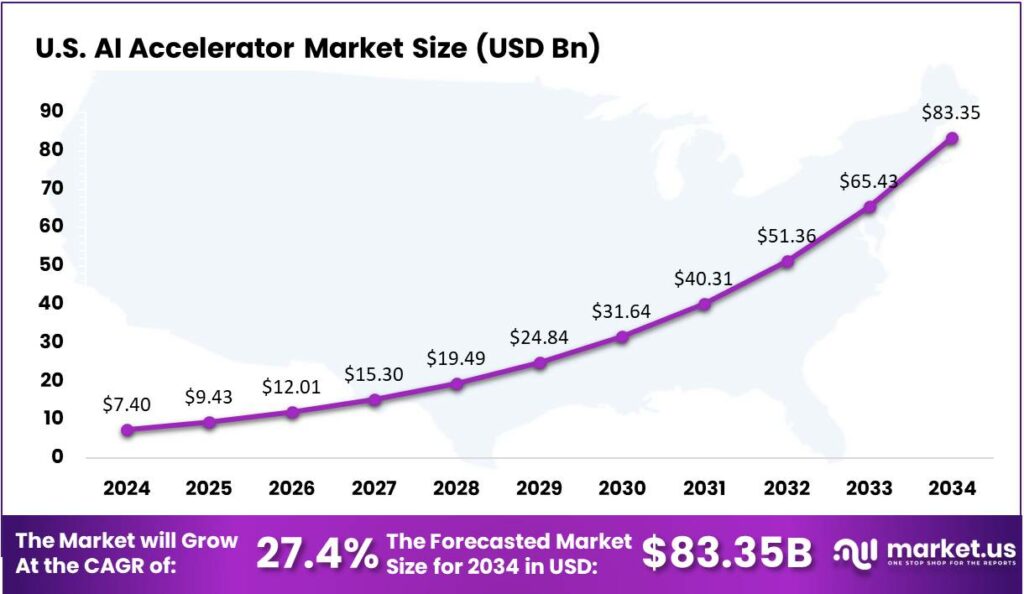

- The U.S. AI Accelerator Market was estimated at USD 7.4 billion in 2024, with a projected CAGR of 27.4% during the forecast period.

U.S. AI Accelerator Market

In 2024, the U.S. AI Accelerator Market was estimated to be valued at USD 7.4 billion. This market is projected to expand at a compound annual growth rate (CAGR) of 27.4% over the forecast period. The significant growth can be attributed to the increasing adoption of AI technologies across various sectors including healthcare, automotive, finance, and retail.

The growing demand for AI accelerators stems from the need for faster data processing and quicker AI operations. Industries are adopting these accelerators to improve decision-making and operational efficiency. In healthcare, they play a key role in drug discovery and patient diagnostics, cutting down both time and costs.

Moreover, the integration of AI accelerators into consumer electronics and the rising trend of automation in the automotive and manufacturing sectors are expected to further boost the market growth. The development of more advanced and cost-effective AI accelerator models by leading market players also suggests a promising expansion trajectory for this market in the coming years.

In 2024, North America held a dominant market position in the global AI Accelerator Market, capturing more than a 40% share, with revenue amounting to USD 8 billion. This leadership can primarily be attributed to the region’s robust technological infrastructure and the early adoption of advanced technologies.

North America is home to leading AI technology developers and houses significant investments in AI research and development. The presence of major tech giants, such as Google, IBM, and Microsoft, who are continuously innovating and investing in AI technologies, plays a crucial role in driving the market forward.

The region’s market dominance is further bolstered by supportive government policies aimed at enhancing AI capabilities across various sectors, including healthcare, automotive, and manufacturing. For example, initiatives promoting the use of AI in healthcare for diagnostics and personalized treatment options have led to increased demand for AI accelerators.

Furthermore, the high penetration of cloud-based services in North American enterprises contributes significantly to the expansion of the AI Accelerator Market. Cloud platforms equipped with AI accelerators offer enhanced processing power and faster data analytics, essential for businesses looking to leverage big data for strategic decision-making.

Type Analysis

In 2024, the Graphics Processing Units (GPUs) segment held a dominant market position, capturing more than a 59.6% share of the AI accelerator market. This substantial market share can be attributed to the versatility and efficiency of GPUs in handling complex mathematical computations required for training deep learning models.

The dominance of the GPU segment is strengthened by ongoing innovations from key players like NVIDIA and AMD, who are focused on improving processing power and energy efficiency. These advancements have made GPUs essential for high-performance computing, particularly in AI workloads, driving their widespread adoption across various industries.

The compatibility of GPUs with popular AI frameworks like TensorFlow and PyTorch has made them a preferred choice for AI researchers and developers. This seamless integration into existing development environments helps reduce deployment complexity and time, driving their widespread adoption for AI acceleration.

Furthermore, the economic scale of GPU production has led to more cost-effective solutions, making them accessible to a broader range of users, from large enterprises to individual developers. As AI technologies become more democratized, the demand for GPUs continues to grow, maintaining their leadership in the AI accelerator market.

Technology Analysis

In 2024, the cloud-based AI accelerators segment held a dominant market position, capturing more than a 62% share. This segment’s leadership is primarily due to its critical role in supporting cloud computing environments where massive data sets require rapid processing for AI applications.

The superiority of cloud-based AI accelerators stems from their ability to provide substantial computational power without the need for on-premise hardware installations. This attribute is particularly appealing to small and medium-sized enterprises that may not have the capital to invest in expensive hardware.

Cloud-based AI accelerators play a crucial role in deploying deep learning models and complex algorithms that need significant computational power. They drive innovation across sectors like finance, healthcare, and automotive, supporting tasks such as fraud detection, advanced diagnostics, and autonomous driving technologies.

The cloud-based AI accelerators segment remains dominant due to ongoing advancements in cloud infrastructure, which enhance the efficiency and capabilities of these accelerators. As cloud providers expand their global infrastructure and optimize data center technologies, performance improvements will continue to drive growth and segment’s leadership.

End-Use Analysis

In 2024, the IT & Telecom segment held a dominant market position in the AI Accelerator Market, capturing more than a 28% share. This prominence is primarily due to the critical need for AI accelerators in managing the vast data traffic and improving the efficiency of telecommunications operations.

The deployment of AI accelerators in IT & Telecom also facilitates the implementation of more sophisticated machine learning models that can predict equipment failures, optimize network quality, and enhance customer service. By accelerating data processing times and improving the accuracy of outputs, these accelerators enable telecom companies to deliver higher quality service while managing costs more effectively.

Moreover, the increasing reliance on virtualized network functions and the rollout of IoT devices further drives the need for robust AI accelerators in this sector. As telecom operators continue to expand their infrastructure to support a growing array of smart devices and services, the integration of AI technologies becomes indispensable.

The competitive landscape in IT & Telecom drives companies to innovate, with AI accelerators giving telecom operators an edge. They enable services like smart home tech, enhanced mobile broadband, and low-latency communications, helping maintain a competitive edge, ensure customer satisfaction, and fuel growth in the AI Accelerator Market.

Key Market Segments

By Type

- Graphics Processing Units (GPUs)

- Tensor Processing Units (TPUs)

- Application-Specific Integrated Circuits (ASICs)

- Central Processing Units (CPUs)

- Field-Programmable Gate Arrays (FPGAs)

By Technology

- Cloud-Based AI Accelerators

- Edge AI Accelerators

By End-use

- IT & Telecom

- Healthcare

- Automotive

- BFSI

- Retail

- Others

Driver

Proliferation of AI Applications

The rapid expansion of artificial intelligence (AI) applications across various industries is a significant driver for the AI accelerator market. Sectors such as healthcare, finance, automotive, and consumer electronics increasingly rely on AI to enhance efficiency and innovation. For instance, in healthcare, AI accelerators enable advanced diagnostic tools and personalized treatment plans.

In finance, they facilitate real-time data analysis for improved decision-making. The automotive industry leverages AI accelerators for autonomous driving technologies, while consumer electronics benefit from enhanced functionalities in devices like smartphones and smart home systems. This widespread adoption underscores the critical role of AI accelerators in meeting the computational demands of modern applications.

Restraint

High Initial Investment and Implementation Costs

Despite the promising growth, the AI accelerator market faces challenges due to substantial initial investments and implementation costs. Developing or procuring AI accelerator hardware, establishing the necessary infrastructure, and integrating these systems into existing workflows require significant financial resources.

Another important point is the lack of clear ROI (Return on Investment) metrics. Many SMEs struggle to quantify the long-term benefits of AI adoption, making it difficult to justify the initial investment. Without concrete data or success stories tailored to their industry, decision-makers may remain hesitant to invest in AI technologies, further contributing to the slow adoption rate and hindering market expansion.

Opportunity

Advancements in Generative AI

Advancements in generative AI present a substantial opportunity for the AI accelerator market. Technologies such as GPT-4 and DALL-E have revolutionized content creation by enabling machines to generate high-quality text, images, and videos.

This innovation is transforming industries like marketing, entertainment, and media, where demand for AI-generated content is surging. The ability of AI accelerators to efficiently handle the complex computations required for generative AI models positions them as essential components in this evolving landscape. As generative AI continues to gain traction, the demand for robust AI accelerators is expected to rise correspondingly.

Challenge

Competition and Market Dynamics

The AI accelerator market is experiencing intensified competition as new players enter the field and existing companies expand their offerings. Notably, firms like Broadcom and Marvell are emerging as significant competitors to established leaders such as NVIDIA.

These companies are developing custom application-specific integrated circuits (ASICs) tailored for AI workloads, offering more specialized and efficient solutions. This shift indicates a potential change in market dynamics, with customers exploring alternatives to traditional GPU-based accelerators. The evolving competitive landscape presents challenges for companies to differentiate their products and maintain market share in an increasingly crowded marketplace.

Emerging Trends

One significant trend is the integration of AI accelerators into everyday devices. Companies like Hailo have introduced AI-centric vision processors, such as the Hailo-15, which bring powerful AI capabilities directly to cameras used in smart cities, factories, and retail locations.

Another notable development is the collaboration between major tech companies to advance AI hardware. For instance, Amazon and Databricks have entered a five-year agreement wherein Databricks will utilize Amazon’s Trainium AI chips.

Additionally, the AI chip market is witnessing increased competition. Companies like Broadcom and Marvell are emerging as significant competitors to established players by focusing on building specialized chips tailored for AI applications. This competition is driving innovation and offering businesses more options for their AI hardware needs.

Business Benefits

AI accelerators enhance processing speed and efficiency by offloading complex tasks from general-purpose CPUs to specialized hardware. This enables faster data analysis and machine learning, allowing businesses to handle large datasets in real-time for quicker decision-making and improved market responsiveness.

Integrating AI accelerators can result in cost savings. For instance, Amazon’s partnership with Databricks, using Amazon’s Trainium AI chips, helps lower AI development costs. This affordable alternative to traditional hardware allows businesses to allocate resources more efficiently, investing in other key growth areas.

Moreover, AI accelerators enhance the capability to deploy advanced AI applications. With improved hardware, businesses can implement sophisticated models for predictive analytics, customer personalization, and automation. This advancement leads to improved customer experiences, streamlined operations, and a competitive edge in the market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

- NVIDIA is a global leader in AI acceleration, known for its Graphics Processing Units (GPUs) that are widely used in AI tasks. The company’s GPU architecture, particularly its A100 Tensor Core, is designed for high-performance computing and deep learning applications. NVIDIA has strategically positioned itself at the forefront of AI by offering a range of solutions that power everything from self-driving cars to cloud data centers.

- Intel Corporation has been a prominent player in the semiconductor industry and has increasingly invested in AI accelerators. With its line of processors, like the Xeon CPUs and specialized hardware like the Intel Nervana and Habana Labs AI chips, Intel is aiming to provide solutions that cater to various AI workloads.

- Google (Alphabet Inc.), through its parent company Alphabet Inc., has revolutionized AI acceleration with its custom-built Tensor Processing Units (TPUs). TPUs are highly optimized for machine learning tasks and are integral to Google’s AI services, including Google Cloud and products like Google Search and Google Translate.

Top Key Players in the Market

- NVIDIA Corporation

- Intel Corporation

- Google (Alphabet Inc.)

- AMD (Advanced Micro Devices)

- Qualcomm Technologies, Inc.

- ARM Holdings

- Graphcore

- MediaTek

- Synopsys

- Huawei Technologies Co., Ltd.

- Baidu, Inc.

- IBM Corporation

- Other Key Players

Top Opportunities Awaiting for Players

- Sustainability and Energy Efficiency Initiatives: Companies are increasingly focusing on sustainability within AI applications, which offers a significant opportunity for AI accelerator technologies that can enhance energy efficiency. This is particularly relevant as environmental concerns become pivotal in technology deployment strategies.

- Enhanced Digital Workflows: The integration of AI into digital workflows is revolutionizing productivity and efficiency across businesses. AI accelerators can play a crucial role in automating tasks and optimizing operations, which in turn can improve organizational efficiency and reduce operational costs.

- Expansion into Healthcare and Automotive Sectors: AI accelerators are finding new applications in healthcare for diagnostics and treatment planning, and in the automotive industry for enhancing vehicle automation and safety systems. These sectors are expected to demand more sophisticated AI capabilities, which accelerators can provide.

- Agentic AI and Autonomous Decision-Making: There is growing interest in agentic AI, which involves systems capable of making autonomous decisions. This trend is particularly influential in fields such as customer service, logistics, and finance, where AI can independently manage and optimize complex processes.

- Private and Hybrid Cloud Deployments: As organizations continue to seek control over their data and AI infrastructure, there is a significant shift towards private and hybrid cloud environments. AI accelerators that can operate effectively in these environments are likely to see increased demand due to their ability to reduce latency and protect intellectual property while offering scalability.

Recent Developments

- In April 2024, Graphcore revealed the Bowmore IPU, a new AI accelerator designed for edge computing. The Bowmore IPU enhances AI inference acceleration at the edge, delivering faster performance, lower latency, and greater power efficiency compared to traditional AI accelerators.

- In June 2024, Google announced a partnership with NVIDIA to integrate NVIDIA’s AI tools into Google Cloud services. This collaboration aims to enhance the capabilities of AI applications hosted on Google’s infrastructure.

- In December 2024, NVIDIA completed its acquisition of Israeli startup Run:ai, which specializes in AI infrastructure management. The software will be open-sourced to enhance its use across various hardware platforms beyond NVIDIA’s own systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 20.01 Bn |

| Forecast Revenue (2034) | USD 240 Bn |

| CAGR (2025-2034) | 28.20% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), Application-Specific Integrated Circuits (ASICs), Central Processing Units (CPUs), Field-Programmable Gate Arrays (FPGAs)), By Technology (Cloud-Based AI Accelerators, Edge AI Accelerators), By End-use (IT & Telecom, Healthcare, Automotive, BFSI, Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NVIDIA Corporation, Intel Corporation, Google (Alphabet Inc.), AMD (Advanced Micro Devices), Qualcomm Technologies, Inc., ARM Holdings, Graphcore, MediaTek, Synopsys, Huawei Technologies Co., Ltd., Baidu, Inc., IBM Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |