Quick Navigation

Report Overview

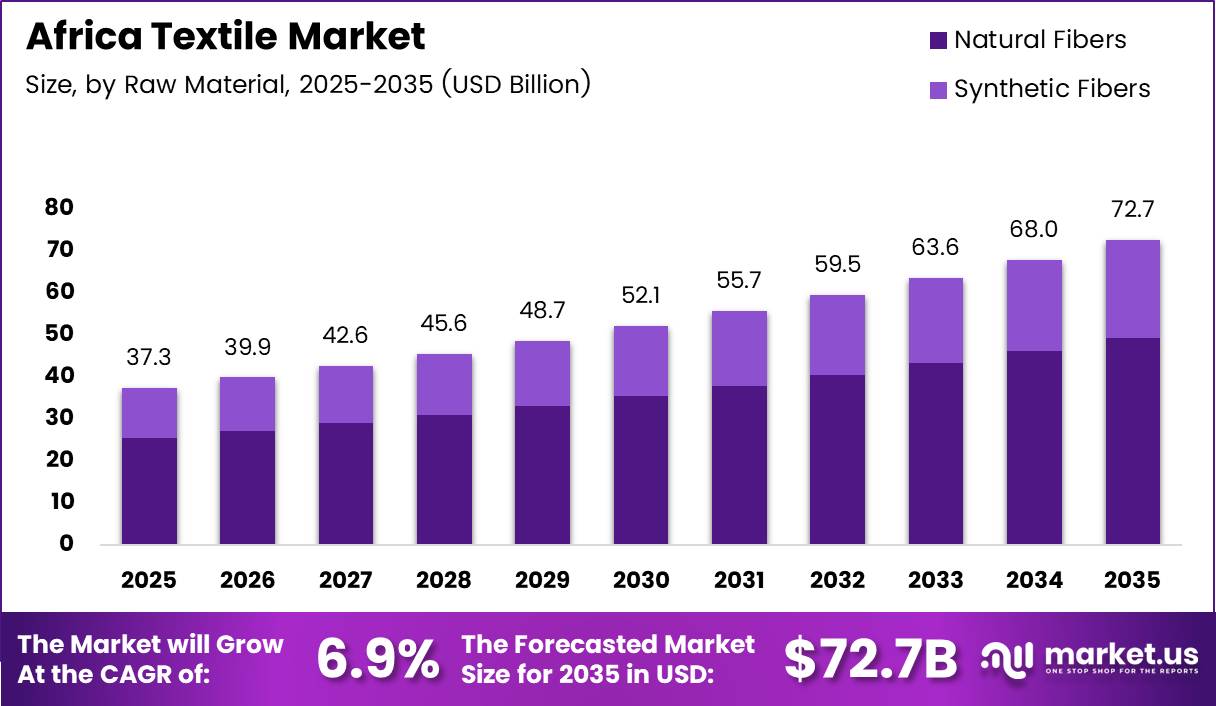

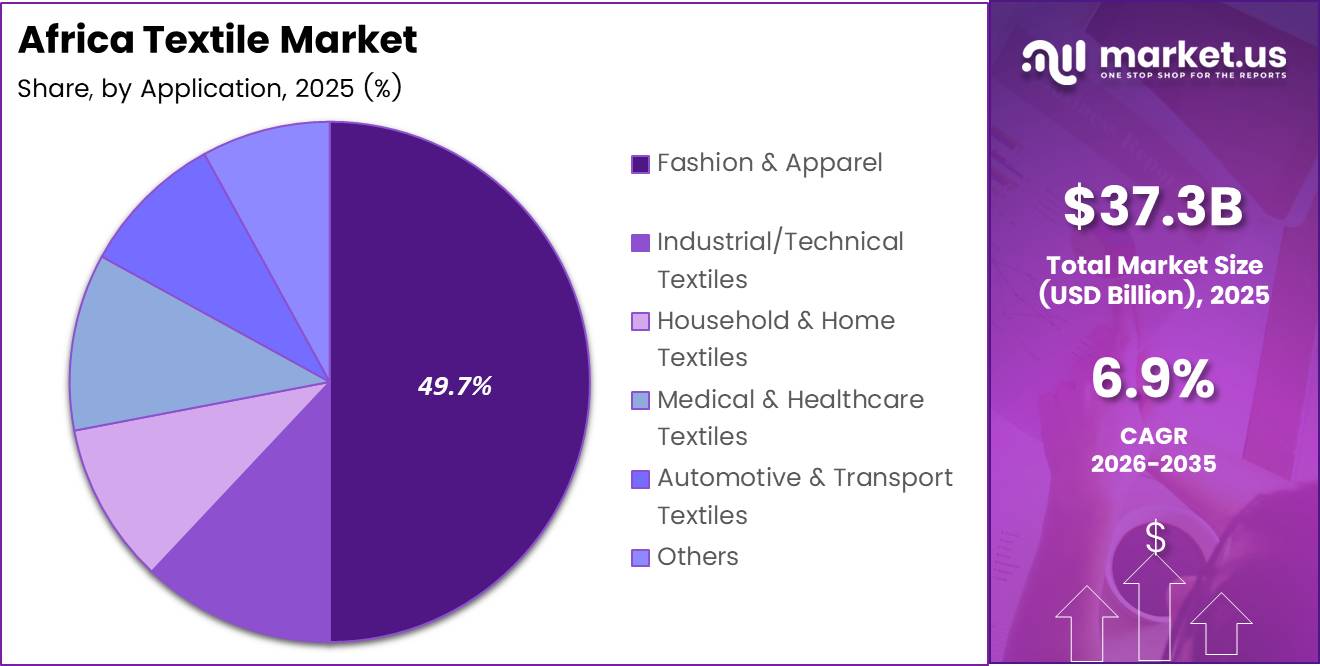

Africa Textile Market size is expected to be worth around USD 72.7 Billion by 2035 from USD 37.3 Billion in 2025, growing at a CAGR of 6.9% during the forecast period 2026 to 2035.

Africa’s textile sector spans the full production chain, from raw fiber cultivation and yarn spinning to fabric weaving, garment manufacturing, and retail distribution. The market serves both domestic consumers and global export buyers. Natural fibers, particularly cotton, form the productive base across East, West, and Southern African economies.

Urbanization is reshaping consumer behavior across the continent. Cities in Nigeria, Ethiopia, Kenya, and South Africa are producing a new generation of apparel buyers who favor branded and fashion-forward products. This urban consumer shift directly expands the addressable market for domestic textile producers and retail chains.

Regional trade frameworks structure much of Africa’s textile export activity. The African Continental Free Trade Area (AfCFTA) creates intra-continental sourcing incentives. Programs like AGOA have historically provided preferential access to the US market. These policy structures directly influence where manufacturers invest and which production segments scale fastest.

Government-led industrialization programs are directing capital toward integrated textile zones. Ethiopia’s Hawassa Industrial Park and similar special economic zones in Senegal, Côte d’Ivoire, and Tanzania attract both domestic and foreign manufacturers. These facilities lower entry costs for garment exporters and help governments reduce unemployment in labor-intensive segments.

Sustainability is emerging as a procurement condition, not a marketing claim. According to Textile Exchange, the 2025 Sustainable Cotton Challenge targets raising sustainable cotton use from 30% to 50% industry-wide. This benchmark signals that export buyers in Europe and North America are tightening sourcing requirements, and African producers who meet them gain a measurable competitive edge.

According toTextile Press, South Africa’s textile imports declined by 17% to $580.15 million in the first two months of 2026. This contraction reflects both import substitution pressure and currency-driven cost sensitivity. It creates a direct opening for local manufacturers to capture share previously held by Asian suppliers in the South African retail market.

According to Ecotextile, Cotton made in Africa (CmiA) reached a record 700 partners and suppliers across 25 countries as of February 2026. This network expansion signals that traceability and certified sustainable sourcing are becoming infrastructure-level requirements for African cotton supply chains, not optional certifications.

Key Takeaways

- The Africa Textile Market was valued at USD 37.3 Billion in 2025 and is forecast to reach USD 72.7 Billion by 2035.

- The market grows at a CAGR of 6.9% from 2026 to 2035.

- By Raw Material, Natural Fibers dominate with a 67.8% market share in 2025.

- By Process/Technology, Woven holds the leading position with a 48.2% share in 2025.

- By Application, Fashion & Apparel commands the largest share at 49.7% in 2025.

- South Africa’s textile imports fell by 17% to $580.15 million in early 2026, signaling import substitution pressure.

- CmiA reached 700 partners across 25 countries as of February 2026.

- ARISE IIP secured a USD 450 million credit facility in March 2025 to expand industrial textile zones.

- AGOA was reauthorized until December 31, 2026, maintaining duty-free access for over 1,800 products.

- In November 2024, Rieter and ARISE IIP agreed to develop 500,000 metric tons of cotton transformation capacity backed by USD 5 billion in project financing.

Raw Material Analysis

Natural Fibers dominates with 67.8% due to cotton availability and export demand.

In 2025, Natural Fibers held a dominant market position in the By Raw Material segment of the Africa Textile Market, with a 67.8% share. Africa’s cotton belt stretches across Mali, Burkina Faso, Tanzania, and Uganda, giving producers cost-advantaged access to raw materials. This geographic supply base makes natural fiber textiles the default input for both domestic apparel and export-grade fabric.

Synthetic Fibers represent the counterbalancing segment to natural fiber dominance. Rising polyester use in affordable garment manufacturing is expanding synthetic fiber demand in urban African markets. However, most synthetic fiber feedstock is imported, which creates cost exposure when global petrochemical prices shift.

Process/Technology Analysis

Woven dominates with 48.2% due to broad apparel and home textile applications.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the Africa Textile Market, with a 48.2% share. Woven fabrics form the structural basis of formal apparel, traditional garments, and household textiles across all African sub-regions. The technology’s versatility across cotton, synthetic, and blended yarns makes it the default process for the widest range of end-use categories.

Knitted fabric production serves the fast-growing sportswear, casualwear, and intimate apparel segments. South African and Kenyan knitting mills supply both domestic retail chains and export buyers requiring stretch-woven performance fabrics. The segment benefits from lower capital requirements compared to weaving, making it accessible to small and mid-scale manufacturers.

Non-woven fabrics represent the fastest-expanding process category, driven by medical textile, hygiene product, and agricultural fabric demand. Non-woven production requires specialized machinery and technical expertise, which concentrates manufacturing in industrial zones with reliable power infrastructure. This segment’s growth is structurally linked to healthcare investment and agricultural modernization programs.

3-D Weaving & Spacer Fabrics represent the premium technology frontier in African textile manufacturing. These fabrics serve aerospace, automotive, and advanced medical applications and require significant technical capability. Current African production is minimal, but technology transfer agreements linked to industrial park development may introduce this capability over the forecast period.

Application Analysis

Fashion & Apparel dominates with 49.7% due to urban population growth and rising retail consumption.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the Africa Textile Market, with a 49.7% share. Urban population growth across sub-Saharan Africa is the structural engine behind this dominance. As city populations expand, per-capita apparel spending rises, and both domestic brands and international fast-fashion retailers compete for this consumer base.

Industrial/Technical Textiles serve construction, agriculture, filtration, and protective equipment markets. This segment represents a high-value diversification path for textile manufacturers moving beyond commodity fabric production. Infrastructure investment programs funded by the African Development Bank and bilateral donors create sustained procurement demand for geotextiles and construction fabrics.

Household & Home Textiles cover bedding, towels, curtains, and upholstery fabrics serving both retail consumers and hospitality procurement. South Africa and Egypt are the largest home textile producers on the continent. The hospitality sector’s recovery and expansion across tourism-dependent economies like Kenya, Morocco, and Tanzania drives commercial procurement in this segment.

Medical & Healthcare Textiles include surgical drapes, wound care materials, and personal protective equipment. Healthcare infrastructure expansion and post-pandemic procurement programs are the primary demand drivers. This segment requires higher technical standards than apparel and currently relies heavily on imports, creating a measurable opportunity for domestic producers that meet certification requirements.

Automotive & Transport Textiles supply seat fabrics, headliners, carpets, and filtration components to vehicle assembly operations. South Africa hosts the continent’s most developed automotive manufacturing base, making it the primary market for this segment. Vehicle production growth in Morocco and Egypt adds secondary demand nodes for automotive textile suppliers.

Key Market Segments

By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Urbanization and Middle-Class Expansion Are Structurally Enlarging Africa’s Textile Consumer Base

Africa’s urban population is expanding faster than any other continent. Cities in Nigeria, Ethiopia, Kenya, and South Africa are generating new cohorts of wage-earning consumers who allocate more income to branded apparel and home textiles. This demographic shift is not cyclical. It is a structural expansion of the addressable market that persists regardless of commodity price volatility.

Government industrialization policies are reinforcing the consumer demand signal with supply-side investment. Ethiopia, Senegal, and Tanzania have designated textile and apparel manufacturing as priority sectors in national development plans. These policies direct infrastructure, tax incentives, and foreign investment facilitation toward sectors where domestic job creation and export earnings align, and textiles sit at that intersection.

Trade policy frameworks create a direct incentive structure for textile investment. According to UNCTAD, Kenya’s trade-weighted average US tariff on exports would nearly triple from 10% to 28% if AGOA expires without replacement. However, the AGOA regional apparel program was reauthorized until December 31, 2026, extending duty-free access to over 1,800 products. This extension preserves the export economics that justify current manufacturing capacity in East African garment hubs.

Restraints

Import Dependency and Energy Costs Are Compressing Margins Across African Textile Production

African textile manufacturers face a structural cost problem at both ends of production. Most synthetic fiber feedstocks are imported, and unreliable power infrastructure in sub-Saharan Africa forces mills to operate backup generators at significant additional cost. These twin pressures reduce the cost competitiveness of African-made textiles against Asian suppliers who operate with cheaper energy and vertically integrated raw material supply.

According to IDOS Research, Madagascar’s apparel exports would face a weighted average tariff of over 13% under US MFN tariff rates if AGOA expires. This figure illustrates how much of Africa’s textile export economics depend on preferential trade access rather than underlying cost competitiveness. When that access is uncertain, investment decisions stall and expansion plans get deferred.

Power infrastructure gaps create particular problems for capital-intensive segments like synthetic fabric weaving, dyeing, and finishing. Textile processing requires consistent, high-voltage power supply. Load-shedding events in South Africa, grid instability in Nigeria, and infrastructure limitations in landlocked manufacturing economies all translate directly into production downtime, quality defects, and higher per-unit costs that erode export margins.

Growth Factors

Sustainable Textile Production and FDI Into Integrated Manufacturing Clusters Are Creating New Revenue Streams

Sustainable and organic textile production represents a direct revenue differentiation opportunity for African producers. European and North American buyers are shifting sourcing criteria toward certified origin, traceability, and reduced-chemical processing. African cotton’s geographic separation from mass-production industrial systems gives it credible provenance claims that Asian commodity cotton cannot easily replicate.

Foreign direct investment into integrated textile and garment clusters is validating Africa’s manufacturing potential at scale. In November 2024, Rieter signed a framework agreement with ARISE IIP and Afreximbank under the Africa Textile Renaissance Plan to develop 500,000 metric tons of cotton transformation capacity across Africa, supported by USD 5 billion in project financing. This commitment signals that global machinery and finance partners view Africa’s textile industrialization as commercially viable, not speculative.

According to Trading Economics, South African manufacturing activity increased 0.9% year-on-year in March 2026, following a 2.3% fall in February. This recovery indicates that domestic production is stabilizing after a period of contraction. For textile manufacturers, recovering industrial output suggests that input supply chains, energy availability, and consumer demand are aligning in ways that support capacity utilization and margin recovery.

Emerging Trends

Circular Textile Practices and Digital Manufacturing Technologies Are Redefining Competitive Standards in Africa

Eco-friendly fabric production is transitioning from export-market preference to commercial requirement. According to Textile Exchange, the 2025 Sustainable Cotton Challenge targets raising sustainable cotton use from 30% to 50% industry-wide. African producers who achieve certified sustainable status before this target normalizes will command premium pricing and preferred supplier status with global fashion brands.

The ESA-backed GreenerCotton project concluded its Final Review in July 2025, supporting CmiA sustainability standards in Tanzania. This completion demonstrates that donor-backed sustainability infrastructure is generating verifiable outcomes, not just pilot programs. Producers in Tanzania and neighboring countries now have a certified supply chain framework they can use to access premium sustainable cotton markets.

Digital textile printing and smart manufacturing automation are beginning to enter African production facilities. These technologies reduce minimum order quantities, shorten lead times, and enable customized fabric production for domestic fashion brands. African designers and fashion labels are creating a pull-through demand for shorter, more flexible production runs that conventional weaving mills are not optimized to serve.

Key Company Insights

CIEL Textile Ltd operates as one of Africa’s most vertically integrated textile producers, with manufacturing assets spanning Mauritius, Madagascar, and India. Its integration across spinning, fabric production, and garment assembly allows it to serve fast-fashion buyers who require short lead times and consistent quality. This vertical model insulates CIEL from single-tier margin compression but requires continuous capital investment to stay competitive.

Mediterranean Textile Company SAE operates within Egypt’s export-oriented textile manufacturing ecosystem, serving European and US buyers with woven and knitted fabrics. Egypt’s free trade agreements provide Mediterranean Textile with structural tariff advantages that competitors in sub-Saharan Africa cannot access through the same channels. Its positioning within Egypt’s industrial textile zones further reduces logistics and energy costs relative to standalone facilities.

Almeda Textile Factory Plc operates inside Ethiopia’s industrial park framework, benefiting from subsidized infrastructure, preferential energy pricing, and streamlined export logistics. Ethiopia’s positioning as a low-cost garment export hub gives Almeda a labor cost advantage over Southern African competitors. However, trade policy uncertainty around AGOA renewal represents a material risk to the export economics that underpin its business model.

Truworths International Ltd operates primarily as a fashion retail and sourcing business rather than a manufacturer, giving it a different risk and reward profile from production-focused players. Its strength lies in brand positioning, consumer credit financing, and retail network depth across Southern Africa. Truworths translates consumer demand data directly into sourcing decisions, making it a market signal for suppliers rather than a competitor to them.

Key Players

- CIEL Textile Ltd

- Mediterranean Textile Company SAE

- Almeda Textile Factory Plc

- Truworths International Ltd

- Rivatex East Africa Ltd

- Saygin-Dima Textile SC

- Woolworths Holdings Ltd

- Edcon Ltd

- Gelvenor Textiles

- Thika Cloth Mills Ltd

- United Textile Industry (K) Ltd

- Spin Knit Kenya Ltd

- Sunflag Group (Kenya/Nigeria)

- Bhupco Textile Mills

- Oriental Mills Ltd

Recent Developments

- March 2025 – ARISE IIP secured a USD 450 million credit facility from African Export-Import Bank (Afreximbank) to accelerate development of industrial parks and special economic zones supporting textile and apparel manufacturing across multiple African countries.

- February 2026 – Cotton made in Africa (CmiA) reached a record 700 partners and suppliers across 25 countries, establishing the largest certified sustainable cotton network in Africa’s history.

- January to February 2026 – South Africa’s textile imports declined by 17% to $580.15 million in the first two months of 2026, reflecting a measurable shift toward domestic sourcing and import cost sensitivity among South African retailers.

- March 2026 – South African manufacturing activity increased 0.9% year-on-year, recovering from a 2.3% fall in February, signaling stabilization in industrial output conditions that affect textile and apparel production capacity.

- 2025 – The 2025 Sustainable Cotton Challenge set an industry target to increase sustainable cotton sourcing from 30% to 50%, establishing a global benchmark that directly affects procurement requirements for African cotton exporters.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 37.3 Billion |

| Forecast Revenue (2035) | USD 72.7 Billion |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Natural Fibers, Synthetic Fibers), By Process/Technology (Woven, Knitted, Non-woven, 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | CIEL Textile Ltd, Mediterranean Textile Company SAE, Almeda Textile Factory Plc, Truworths International Ltd, Rivatex East Africa Ltd, Saygin-Dima Textile SC, Woolworths Holdings Ltd, Edcon Ltd, Gelvenor Textiles, Thika Cloth Mills Ltd, United Textile Industry (K) Ltd, Spin Knit Kenya Ltd, Sunflag Group (Kenya/Nigeria), Bhupco Textile Mills, Oriental Mills Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |