Global Advanced Vehicle Diagnostics and Remote Services Market Size, Share, Growth Analysis By Offerings (Predictive and Condition-Based Diagnostics, Remote Vehicle Health Monitoring and Fault Diagnostics, Over-the-Air (OTA) Software and Firmware Management, Remote Control Calibration and Feature Activation, Cybersecurity, Compliance and System Integrity Services), By Vehicle Type (SUV, LCV, HCV, Hatchback/Sedan), By End User (Fleet Operators, Individual Vehicle Owners, Automotive OEMs and Tier-1 Suppliers, Workshops and Service Networks), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179750

- Number of Pages: 382

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

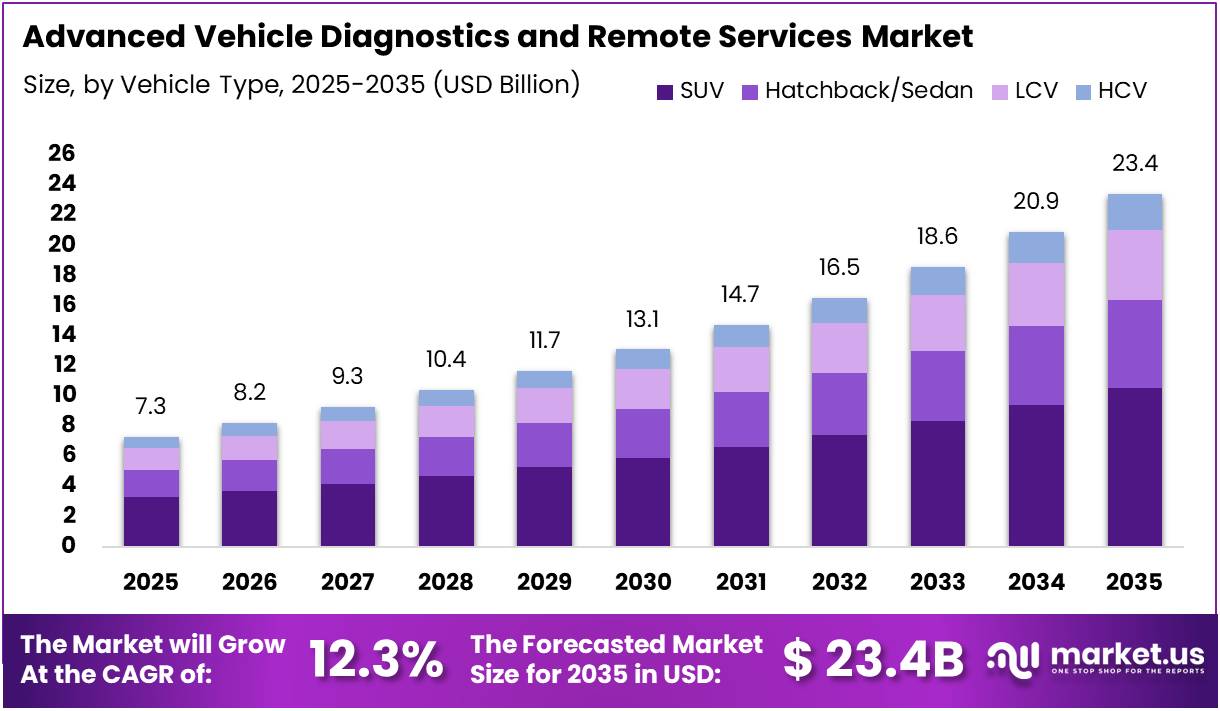

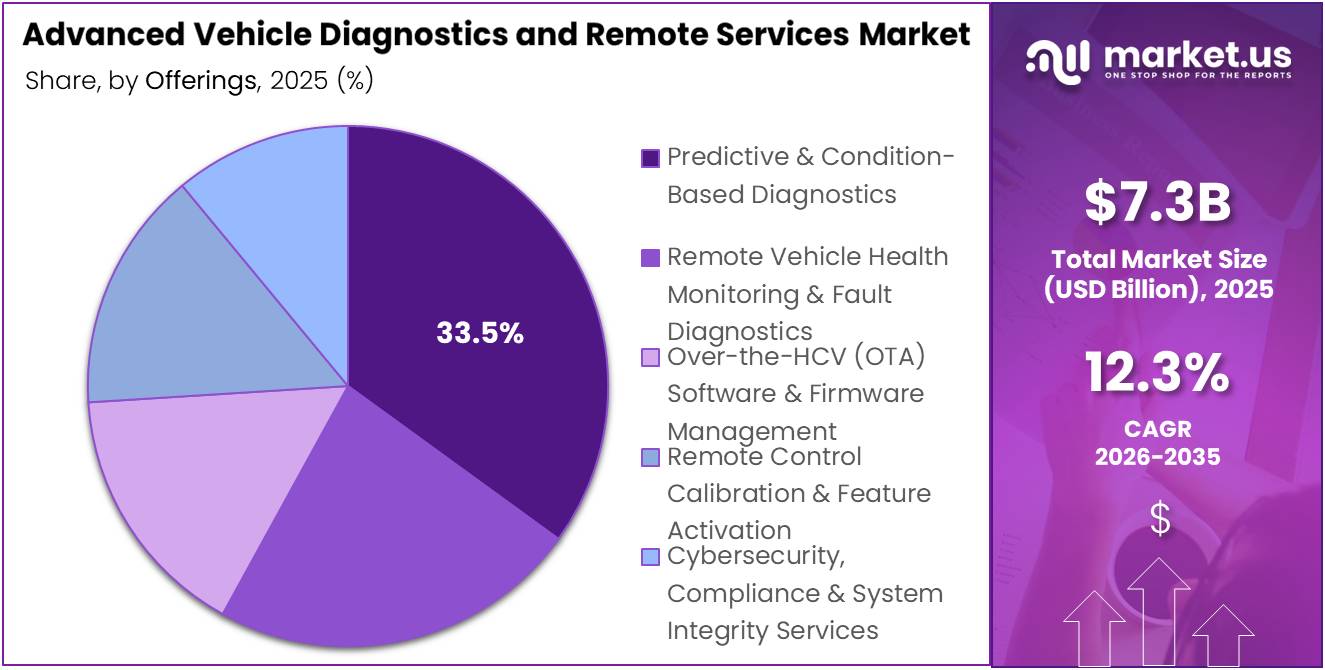

The Global Advanced Vehicle Diagnostics and Remote Services Market size is expected to be worth around USD 23.4 Billion by 2035 from USD 7.3 Billion in 2025, growing at a CAGR of 12.3% during the forecast period 2026 to 2035.

Advanced vehicle diagnostics and remote services refer to technologies that enable real-time monitoring, fault detection, and remote management of vehicle systems. These platforms use connected telematics, onboard diagnostics, and cloud-based tools to deliver actionable vehicle health data. The market serves passenger cars, commercial vehicles, and fleet operators across global automotive ecosystems.

The market is growing rapidly due to increasing adoption of connected vehicle platforms, telematics control units, and predictive maintenance solutions. Moreover, automakers are integrating remote diagnostics into new vehicle designs to reduce service downtime and improve customer satisfaction. This trend is further supported by growing demand for over-the-air software updates and real-time fault monitoring capabilities.

Government mandates for on-board diagnostics compliance and emission monitoring are accelerating market adoption across regions. Additionally, regulators in North America, Europe, and Asia Pacific are enforcing stricter vehicle health and safety standards. These regulations are creating strong demand for advanced diagnostic tools and remote service platforms across both passenger and commercial segments.

The shift toward electric and hybrid vehicles is opening significant new opportunities for remote diagnostics providers. Consequently, OEMs and technology suppliers are developing AI-driven platforms to support EV battery health monitoring and software-defined vehicle architectures. Subscription-based remote monitoring models are also gaining traction as a recurring revenue stream for service providers and dealers alike.

According to JETIR, a 2025 engineering implementation of DoIP with CAN-to-Ethernet achieved a packet transmission success rate of 98.5%, significantly improving reliability for remote diagnostics data exchange. The same implementation reduced diagnostic latency by 40% compared with traditional CAN-only solutions. Additionally, according to WJARR, commercial vehicles with telematics demonstrated maintenance cost reductions of up to 25% through predictive diagnostics.

According to dialzara, AI-powered scan tools reduced diagnostic time by up to 90% compared to traditional methods. Furthermore, about 60% of collision repair shops in the US now use some form of digital diagnostics. According to ResearchGate, a remote diagnostic device via mobile application achieved response times of 0.4 to 0.6 seconds under stable internet conditions.

Key Takeaways

- The global Advanced Vehicle Diagnostics and Remote Services Market was valued at USD 7.3 Billion in 2025 and is projected to reach USD 23.4 Billion by 2035.

- The market is expected to grow at a CAGR of 12.3% during the forecast period 2026 to 2035.

- By Offerings, Predictive and Condition-Based Diagnostics dominated with a 33.5% market share in 2025.

- By Vehicle Type, SUVs held the leading position with a 41.3% share in 2025.

- By End User, Fleet Operators accounted for the largest share at 36.8% in 2025.

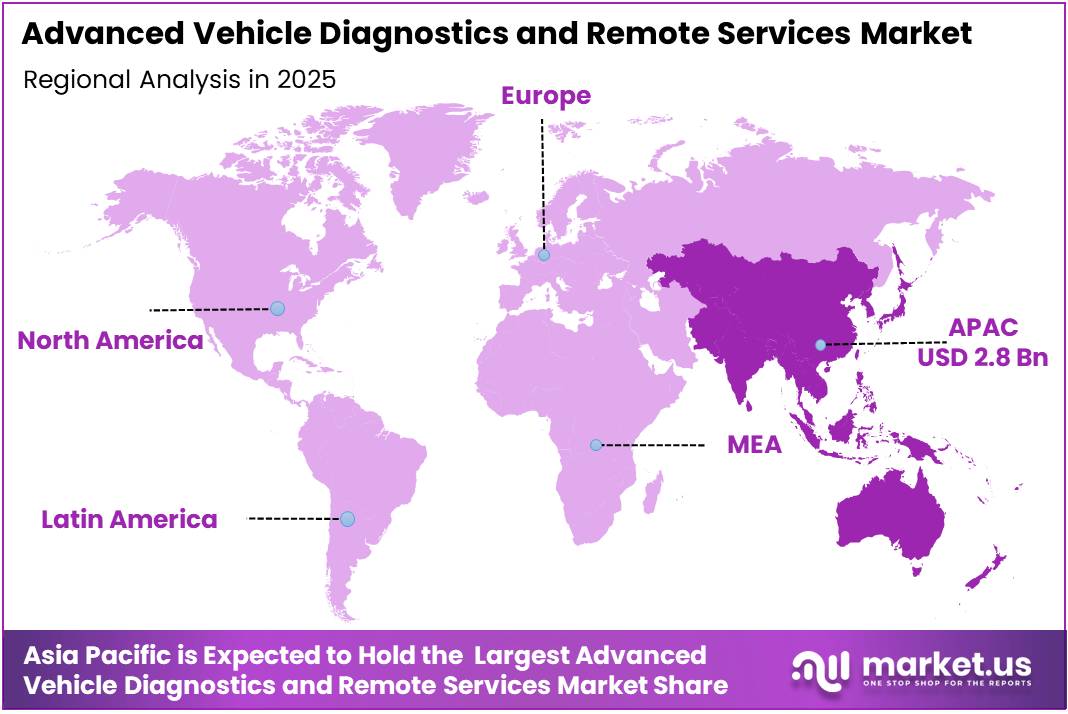

- Asia Pacific dominated the regional landscape with a 38.50% share, valued at USD 2.8 Billion in 2025.

By Offerings Analysis

Predictive and Condition-Based Diagnostics dominates with 33.5% due to strong demand for proactive vehicle health management and reduced maintenance costs.

In 2025, Predictive and Condition-Based Diagnostics held a dominant market position in the By Offerings segment of the Advanced Vehicle Diagnostics and Remote Services Market, with a 33.5% share. This segment leads due to its ability to detect faults before failure, reducing unplanned downtime and operational costs for fleet operators and OEMs globally.

Remote Vehicle Health Monitoring and Fault Diagnostics is gaining strong momentum across commercial and passenger vehicle segments. This offering enables continuous vehicle status tracking and real-time alerts for system anomalies. Moreover, growing fleet management needs and increasing vehicle connectivity are driving its adoption among logistics operators and automotive service networks worldwide.

Over-the-Air (OTA) Software and Firmware Management is becoming a core capability for modern connected vehicles. It allows manufacturers to remotely deploy software updates and bug fixes without requiring physical service visits. Consequently, OEMs are prioritizing OTA capabilities as a standard feature in new vehicle architectures, particularly in electric vehicle platforms.

Remote Control Calibration and Feature Activation enables technicians to configure and calibrate vehicle systems remotely, reducing workshop visits. This service is particularly valuable for ADAS recalibration and feature unlocking after software updates. Additionally, it supports faster turnaround for service centers managing large volumes of connected vehicles across distributed geographies.

Cybersecurity, Compliance and System Integrity Services are becoming essential as remote vehicle access expands. With increasing connectivity, vehicles face elevated risks of unauthorized access and data breaches. Therefore, automotive stakeholders are investing in compliance-driven cybersecurity frameworks to protect diagnostic communication channels and ensure regulatory adherence across global markets.

By Vehicle Type Analysis

SUVs dominate with 41.3% due to high vehicle connectivity features and premium diagnostics integration in the segment.

In 2025, SUV held a dominant market position in the By Vehicle Type segment of the Advanced Vehicle Diagnostics and Remote Services Market, with a 41.3% share. SUVs are equipped with advanced telematics and connectivity systems as standard, making them the primary segment for remote diagnostics and over-the-air service adoption globally.

Light Commercial Vehicles (LCV) represent a high-growth category within the remote diagnostics market. Fleet operators managing large LCV pools increasingly rely on telematics-based health monitoring to reduce maintenance costs and improve route efficiency. Moreover, rising e-commerce activity is expanding the LCV fleet base, further boosting demand for remote service platforms.

Heavy Commercial Vehicles (HCV) are a critical segment for predictive diagnostics given their high operational value and maintenance complexity. Unplanned breakdowns in HCV fleets generate significant financial losses. Consequently, logistics and transport companies are adopting remote fault detection and condition-based maintenance solutions to minimize downtime and ensure regulatory compliance.

Hatchback and Sedan vehicles represent the broader consumer base for connected diagnostics services. While historically underserved compared to SUVs, increasing connectivity features in entry-level models are expanding adoption. Additionally, growing individual vehicle owner awareness of remote health monitoring tools is driving demand for affordable diagnostic solutions in this segment.

By End User Analysis

Fleet Operators dominate with 36.8% due to high vehicle volumes and operational need for continuous remote health monitoring.

In 2025, Fleet Operators held a dominant market position in the By End User segment of the Advanced Vehicle Diagnostics and Remote Services Market, with a 36.8% share. Fleet operators benefit most from remote diagnostics by reducing unplanned downtime, optimizing maintenance schedules, and lowering total operating costs across large multi-vehicle operations.

Individual Vehicle Owners are an emerging and rapidly growing end user group for remote diagnostics services. Rising consumer awareness about vehicle health, coupled with affordable mobile-based diagnostic applications, is driving adoption. Moreover, automakers and aftermarket providers are launching subscription-based tools tailored to individual users seeking real-time vehicle condition insights.

Automotive OEMs and Tier-1 Suppliers are integrating remote diagnostics capabilities directly into new vehicle platforms and supply chain processes. These stakeholders use diagnostic data to improve product quality, monitor warranty performance, and enable over-the-air service delivery. Consequently, remote diagnostics is becoming a core element of connected vehicle strategies for leading manufacturers.

Workshops and Service Networks are leveraging advanced diagnostic tools to improve service accuracy and technician efficiency. Remote diagnostics allows service centers to pre-diagnose vehicles before physical arrival, reducing repair time significantly. Additionally, multi-brand diagnostic platforms are enabling independent workshops to service a broader range of connected vehicles competitively.

Key Market Segments

By Offerings

- Predictive and Condition-Based Diagnostics

- Remote Vehicle Health Monitoring and Fault Diagnostics

- Over-the-Air (OTA) Software and Firmware Management

- Remote Control Calibration and Feature Activation

- Cybersecurity, Compliance and System Integrity Services

By Vehicle Type

- SUV

- LCV

- HCV

- Hatchback/Sedan

By End User

- Fleet Operators

- Individual Vehicle Owners

- Automotive OEMs and Tier-1 Suppliers

- Workshops and Service Networks

Drivers

Rising Connected Vehicle Adoption and Regulatory Compliance Requirements Drive Advanced Diagnostics Market Growth

The rapid integration of connected vehicle platforms and telematics control units across passenger and commercial fleets is a primary market driver. Automakers are embedding real-time data communication systems into new vehicle architectures, enabling continuous remote monitoring. This connectivity infrastructure forms the foundation for advanced diagnostics and remote service delivery at scale.

Increasing regulatory mandates for on-board diagnostics compliance and emission monitoring systems are further accelerating adoption. Governments across North America, Europe, and Asia Pacific require vehicles to meet strict diagnostic and environmental standards. Consequently, automakers and service providers must invest in capable diagnostics platforms to ensure compliance and avoid regulatory penalties.

Growing demand for predictive maintenance solutions is also a significant market driver. Fleet operators and vehicle owners are prioritizing proactive fault detection to reduce unplanned downtime and operational disruptions. Moreover, predictive diagnostics reduces long-term maintenance costs, making it an economically compelling investment for commercial vehicle operators and OEM service networks.

Restraints

Diagnostic Standardization Complexity and Cybersecurity Risks Restrain Market Adoption

One of the key restraining factors is the high complexity of multi-brand diagnostic standardization across diverse vehicle electronics ecosystems. Modern vehicles use a wide range of proprietary communication protocols and electronic control units. Consequently, developing universal diagnostic platforms that operate seamlessly across different manufacturers remains a significant technical and commercial challenge.

Escalating cybersecurity risks associated with remote access to vehicle control systems pose a serious concern for market stakeholders. As vehicles become increasingly connected, they also become more vulnerable to unauthorized intrusion and data breaches. Therefore, ensuring robust cybersecurity across remote diagnostic communication channels requires continuous investment in encryption, authentication, and compliance frameworks.

The combination of standardization complexity and cybersecurity obligations increases development costs and extends time-to-market for diagnostic solution providers. Smaller vendors in particular face resource constraints in meeting these requirements simultaneously. Additionally, the absence of globally harmonized cybersecurity and diagnostics standards creates fragmented regulatory landscapes that further complicate product development and deployment strategies.

Growth Factors

AI-Driven Analytics, EV Ecosystem Expansion, and Subscription Models Accelerate Market Growth

The development of AI-driven fault detection and real-time vehicle health analytics platforms represents a major growth opportunity. AI enables faster, more accurate identification of vehicle system anomalies compared to traditional rule-based diagnostics. Moreover, machine learning models continue to improve in accuracy as they process larger volumes of real-world vehicle data, enhancing diagnostic precision.

The rapid expansion of electric vehicle and hybrid vehicle ecosystems is creating new demand for specialized remote diagnostics solutions. EV platforms require continuous monitoring of battery health, thermal management systems, and software-defined components. Consequently, diagnostics providers are developing EV-specific tools and analytics capabilities to serve this fast-growing segment of the automotive industry.

The emergence of subscription-based remote vehicle monitoring and service models is also a strong growth enabler. These models provide recurring revenue streams for service providers while offering vehicle owners affordable access to continuous diagnostics. Additionally, subscription platforms increase customer retention for OEMs and dealership networks by embedding diagnostics into long-term service relationships.

Emerging Trends

Edge Computing, Digital Twins, and 5G Connectivity Are Reshaping the Vehicle Diagnostics Landscape

The adoption of edge computing for in-vehicle data processing is a transformative trend in advanced diagnostics. By processing data closer to the source, edge architectures reduce latency and enable faster real-time decision support within the vehicle. Moreover, this approach reduces dependency on cloud connectivity, improving diagnostic performance in areas with limited network availability.

The increasing use of digital twins for remote vehicle performance simulation and diagnostics is gaining industry attention. Digital twin platforms create virtual replicas of physical vehicle systems, enabling engineers to test fault scenarios and predict component behavior remotely. Consequently, OEMs and Tier-1 suppliers are investing in digital twin capabilities to improve diagnostic accuracy and reduce physical testing costs.

The deployment of 5G-enabled real-time vehicle-to-cloud communication infrastructure is accelerating the capabilities of remote diagnostics platforms. High-speed, low-latency 5G connectivity enables near-instantaneous transmission of complex vehicle health data to cloud analytics systems. Additionally, 5G supports a higher density of connected vehicles, making it a critical enabler for large-scale fleet diagnostics and remote service delivery.

Regional Analysis

Asia Pacific Dominates the Advanced Vehicle Diagnostics and Remote Services Market with a Market Share of 38.50%, Valued at USD 2.8 Billion

Asia Pacific holds the dominant position in the global Advanced Vehicle Diagnostics and Remote Services Market, accounting for a 38.50% share valued at USD 2.8 Billion in 2025. The region benefits from a large and rapidly growing vehicle production base, strong government support for connected mobility, and increasing OEM investment in telematics-enabled vehicle platforms across China, Japan, South Korea, and India.

North America Advanced Vehicle Diagnostics and Remote Services Market Trends

North America represents a mature and high-value market for advanced vehicle diagnostics, driven by strict OBD compliance mandates and widespread fleet telematics adoption. The United States leads regional demand, supported by a large commercial vehicle base and strong aftermarket diagnostics infrastructure. Moreover, growing investment in AI-driven diagnostics and EV health monitoring is sustaining market expansion in the region.

Europe Advanced Vehicle Diagnostics and Remote Services Market Trends

Europe is a significant market shaped by stringent vehicle emission regulations and strong automotive manufacturing heritage. Germany, France, and the UK are key contributors, with OEMs actively integrating remote diagnostics into new vehicle platforms. Additionally, the European Union’s focus on connected and automated mobility is encouraging investment in advanced diagnostic solutions across passenger and commercial vehicle segments.

Latin America Advanced Vehicle Diagnostics and Remote Services Market Trends

Latin America is an emerging market with growing demand for remote diagnostics driven by fleet expansion and rising vehicle connectivity. Brazil and Mexico represent the primary growth markets in the region, supported by increasing commercial vehicle deployments and improving telecommunications infrastructure. However, economic variability and limited standardized regulatory frameworks continue to moderate the pace of market adoption.

Middle East and Africa Advanced Vehicle Diagnostics and Remote Services Market Trends

The Middle East and Africa market is in early development but shows steady growth potential, driven by fleet modernization programs and increasing adoption of connected vehicle technologies. GCC nations are investing in smart mobility infrastructure, creating demand for remote diagnostics platforms. Furthermore, growing logistics and transportation activity across the region is supporting incremental adoption of telematics-based diagnostic services.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Robert Bosch GmbH is a global leader in automotive diagnostics, offering a comprehensive portfolio of connected vehicle health monitoring and remote service solutions. The company has made significant investments in AI-powered fault detection, OTA software management, and cybersecurity-integrated diagnostics platforms. Bosch’s strong OEM relationships and global service network give it a commanding presence across both passenger and commercial vehicle diagnostics markets.

Continental AG is a major player in advanced vehicle diagnostics, leveraging its expertise in automotive electronics, telematics, and software-defined vehicle systems. The company offers integrated remote diagnostics and predictive maintenance platforms that serve fleet operators, OEMs, and service networks. Moreover, Continental’s focus on connected mobility and electric vehicle system diagnostics positions it strongly for sustained growth in evolving automotive markets.

ZF Friedrichshafen AG brings deep capabilities in vehicle system integration and remote diagnostics, particularly for commercial vehicles and advanced driver assistance systems. The company is expanding its diagnostics portfolio to include real-time fault monitoring and over-the-air calibration services. Additionally, ZF’s investments in digital twin technologies and AI-based analytics are strengthening its position in the next-generation vehicle diagnostics space.

Aptiv PLC specializes in advanced vehicle connectivity and diagnostics software, providing solutions that bridge hardware systems and cloud-based analytics platforms. Aptiv’s portfolio includes vehicle health management, remote fault diagnostics, and cybersecurity services tailored for both passenger cars and commercial fleets. Furthermore, its focus on software-defined vehicle architectures and scalable diagnostic platforms makes it a key enabler of connected automotive service ecosystems.

Key Players

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Aptiv PLC

- HARMAN International

- Denso Corporation

- Valeo SA

- Hyundai Mobis

- Visteon Corporation

- Panasonic Automotive Systems

Recent Developments

- February 2025 – Rotunda Capital Partners announced the acquisition of AirPro Diagnostics, a provider of remote and cloud-based automotive diagnostics solutions. This strategic move strengthens Rotunda’s portfolio in the connected vehicle services space and expands AirPro’s capacity to scale its remote diagnostics offerings across North American markets.

- June 2025 – Greybull Stewardship announced the acquisition of VSSTA, Inc., a company specializing in vehicle systems diagnostics and remote service technologies. This transaction reflects growing investor interest in the advanced vehicle diagnostics sector and is expected to accelerate VSSTA’s product development and market expansion efforts.

- November 2025 – Repairify and Opus IVS announced their intent to combine their diagnostics businesses to advance the future of automotive diagnostics. The proposed merger aims to create a stronger platform for remote diagnostics, calibration, and connected vehicle services, consolidating expertise and customer reach across the North American automotive repair and service network.

Report Scope

Report Features Description Market Value (2025) USD 7.3 Billion Forecast Revenue (2035) USD 23.4 Billion CAGR (2026-2035) 12.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Offerings (Predictive and Condition-Based Diagnostics, Remote Vehicle Health Monitoring and Fault Diagnostics, Over-the-Air (OTA) Software and Firmware Management, Remote Control Calibration and Feature Activation, Cybersecurity, Compliance and System Integrity Services), By Vehicle Type (SUV, LCV, HCV, Hatchback/Sedan), By End User (Fleet Operators, Individual Vehicle Owners, Automotive OEMs and Tier-1 Suppliers, Workshops and Service Networks) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Aptiv PLC, HARMAN International, Denso Corporation, Valeo SA, Hyundai Mobis, Visteon Corporation, Panasonic Automotive Systems Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Advanced Vehicle Diagnostics and Remote Services MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Advanced Vehicle Diagnostics and Remote Services MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Aptiv PLC

- HARMAN International

- Denso Corporation

- Valeo SA

- Hyundai Mobis

- Visteon Corporation

- Panasonic Automotive Systems

Our Clients

- 179750

- Feb 2026