Global Activated Carbon For Pharma And Healthcare Market Size, Share, And Industry Analysis Report By Form (Powdered, Granular, Bead Carbon, Impregnated Carbon, Activated Fiber, Others), By Application (API Production, Finished Drug Production, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179453

- Number of Pages: 352

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

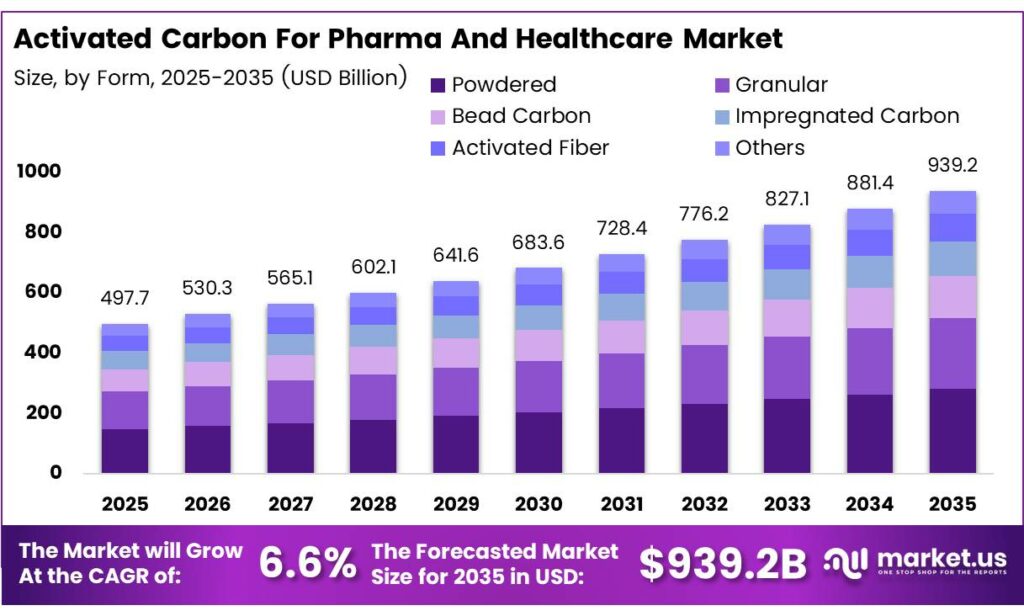

The Global Activated Carbon For Pharma And Healthcare Market size is expected to be worth around USD 939.2 billion by 2035 from USD 497.7 billion in 2025, growing at a CAGR of 6.6% during the forecast period 2026 to 2035.

Activated carbon for pharma and healthcare refers to a highly porous carbon material used to purify, decolorize, and filter substances in drug manufacturing and medical applications. Pharmaceutical producers rely on this material to remove impurities, toxins, and residual solvents during active pharmaceutical ingredient (API) production. Its high adsorption capacity makes it essential across formulation and purification stages.

The market covers multiple product forms, including powdered activated carbon, granular carbon, bead carbon, impregnated carbon, and activated fiber. Each form serves a specific function in manufacturing workflows. Powdered variants dominate in batch purification, while granular types support continuous processing systems commonly adopted by large-scale drug producers.

- Global trade data reflects the scale of this market. According to the World Integrated Trade Solution (WITS), global exports of activated carbon reached approximately USD 2.21 billion for 673,000 tons traded, signaling strong cross-border demand for purification-grade carbon across healthcare supply chains. This trade volume demonstrates how deeply activated carbon is embedded in global pharmaceutical production networks.

Government agencies worldwide continue to reinforce stringent quality standards for pharmaceutical manufacturing. The FDA and EMA require manufacturers to demonstrate effective impurity removal during drug production. Consequently, pharmaceutical companies invest heavily in high-purity activated carbon to meet compliance requirements and maintain product safety across their supply chains.

- Additionally, India’s exports of activated carbon (HS 3802) reached USD 242,172.54 thousand, corresponding to 141,861,000 kilograms shipped globally. This highlights India’s growing role as a major supplier to pharmaceutical and healthcare purification markets worldwide, reinforcing the country’s strategic importance in the global activated carbon supply chain.

Asia Pacific leads investment in generic drug manufacturing infrastructure, creating strong regional demand for pharmaceutical-grade activated carbon. Countries like India and China scale up production capacity to serve both domestic and export markets. This expansion directly increases the consumption of filtration and purification media across regional pharmaceutical clusters.

Key Takeaways

- The Global Activated Carbon For Pharma And Healthcare Market, valued at USD 497.7 billion in 2025, is expected to reach USD 939.2 billion by 2035, at a CAGR of 6.6%.

- The Powdered segment dominates with a 58.2% market share in 2025.

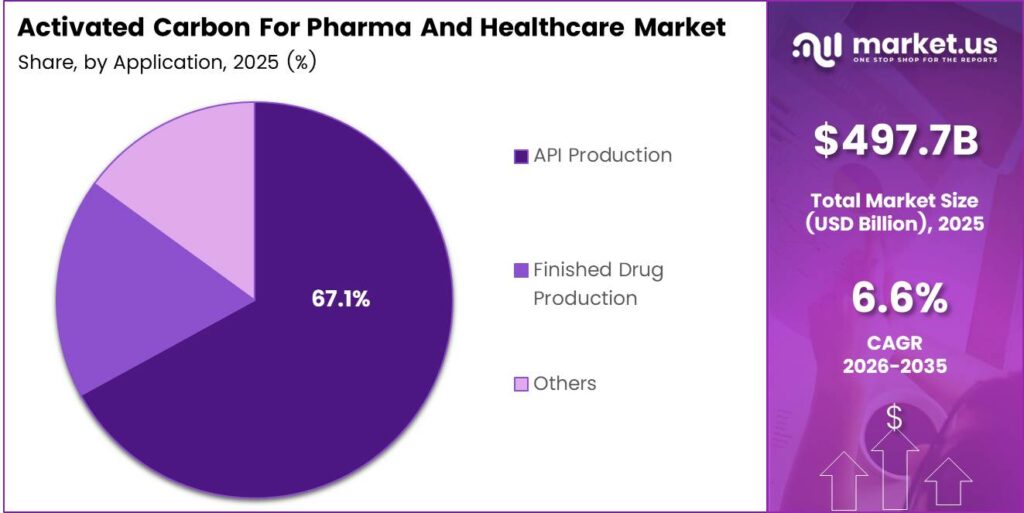

- The API Production segment holds the largest share at 67.1% in 2025.

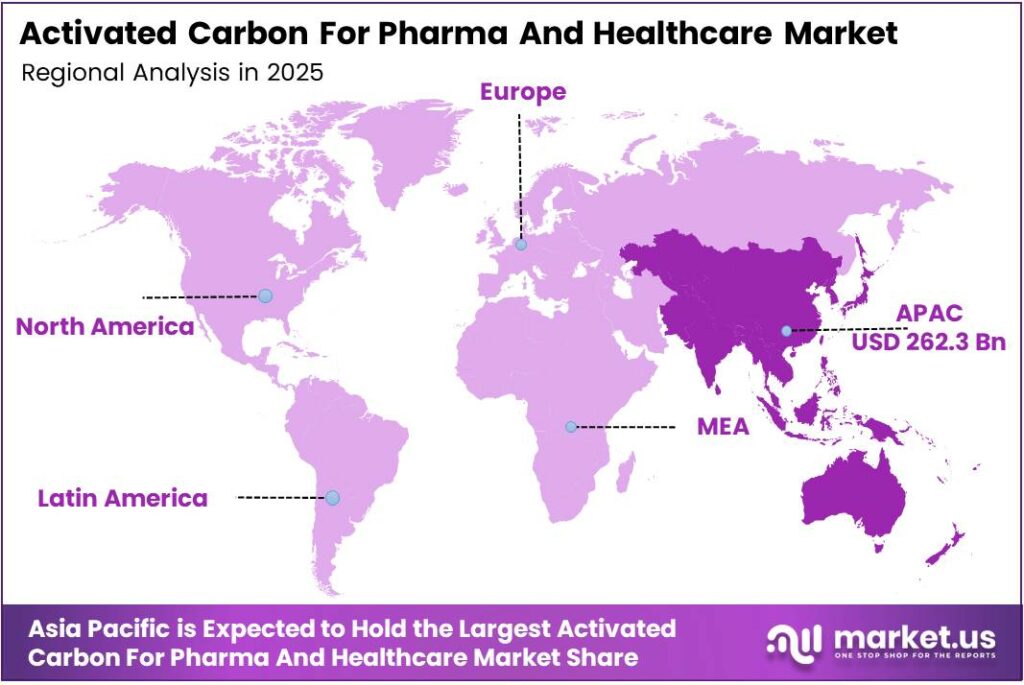

- Asia Pacific leads regionally with a 52.7% market share, valued at USD 262.3 billion.

By Form Analysis

Powdered Activated Carbon dominates with 58.2% due to its superior batch purification efficiency and wide compatibility across pharmaceutical manufacturing stages.

In 2025, Powdered Activated Carbon held a dominant market position in the By Form segment of the Activated Carbon for Pharma and Healthcare Market, with a 58.2% share. Pharmaceutical manufacturers prefer powdered forms for batch decolorization, impurity removal, and API refinement. Moreover, powdered carbon delivers rapid adsorption rates and integrates easily into existing liquid-phase purification workflows used across drug production facilities.

Granular Activated Carbon serves a growing role in continuous manufacturing processes adopted by large pharmaceutical plants. Its structural durability supports repeated use and easy handling in fixed-bed filtration columns. Additionally, granular carbon suits applications requiring precise flow control and extended contact time with process fluids in both API and finished drug production environments.

Bead Carbon offers uniform particle size and low dust generation, making it suitable for specialized pharmaceutical filtration systems. Its spherical structure improves flow distribution and reduces pressure drop in packed-bed columns. Consequently, bead carbon finds growing adoption in high-precision purification stages where consistent performance and minimal product contamination are critical manufacturing requirements.

Impregnated Carbon and Activated Fiber address niche pharmaceutical applications requiring targeted adsorption of specific chemical compounds. Impregnated variants remove acid gases and specialized contaminants in cleanroom air systems. Activated fiber, with its high surface area-to-mass ratio, supports thin-layer filtration solutions. Both forms complement the broader portfolio of carbon products used across healthcare manufacturing settings.

By Application Analysis

API Production dominates with 67.1% due to stringent purity requirements and high-volume activated carbon consumption during active pharmaceutical ingredient synthesis.

In 2025, API Production held a dominant market position in the By Application segment of the Activated Carbon For Pharma And Healthcare Market, with a 67.1% share. Drug manufacturers use activated carbon extensively during API synthesis to remove color bodies, metal impurities, and organic contaminants. Furthermore, global growth in generic drug output directly amplifies demand for high-performance purification carbon in active ingredient processing stages.

Finished Drug Production represents another key application area where activated carbon supports final formulation quality. Manufacturers apply carbon treatment to remove residual solvents, colorants, and pyrogens before drug packaging. Therefore, finished drug facilities maintain steady consumption of pharmaceutical-grade activated carbon as regulatory agencies increase scrutiny on final product purity and patient safety standards.

The Others application segment covers healthcare uses such as overdose treatment, hemoperfusion systems, and medical device sterilization filtration. Hospitals and clinical facilities consume activated carbon through emergency medical applications and blood purification cartridges. Additionally, medical-grade carbon serves air and water filtration systems within healthcare infrastructure, supporting infection control and environmental safety programs across treatment facilities.

Key Market Segments

By Form

- Powdered

- Granular

- Bead Carbon

- Impregnated Carbon

- Activated Fiber

- Others

By Application

- API Production

- Finished Drug Production

- Others

Emerging Trends

Sustainable and Specialty Carbon Forms Reshape Pharmaceutical Filtration Practices

Pharmaceutical manufacturers increasingly shift toward reactivatable granular forms that support continuous manufacturing processes. These formats reduce carbon consumption, lower waste generation, and improve handling efficiency across large-scale drug production facilities. Kuraray Co., Ltd.’s functional Materials segment recorded segment sales of approximately USD 1.315 billion in 2024, reflecting growing commercial investment in advanced activated carbon solutions for pharmaceutical and medical applications.

Bio-based and coconut-derived activated carbon variants gain traction among pharmaceutical producers prioritizing eco-friendly procurement. Buyers increasingly prefer renewable raw materials that align with corporate sustainability goals and green chemistry principles. Consequently, coconut shell-derived carbon commands premium positioning in healthcare procurement channels, driving suppliers to expand sustainable sourcing partnerships and certification programs across their supply networks.

Specialty grades optimized for selective toxin adsorption in vaccine and biologic production emerge as a high-growth niche. Manufacturers targeting biologics require carbon products engineered for precise molecular adsorption without compromising product yield. Additionally, powdered activated carbon sees growing adoption for targeted residual drug removal in pharmaceutical wastewater streams, supporting environmental compliance programs within healthcare and bioprocessing manufacturing campuses.

Drivers

Escalating API Purification Demand and Regulatory Mandates Accelerate Market Growth

Global pharmaceutical production growth directly increases demand for high-purity activated carbon used in API purification processes. Drug manufacturers across emerging and developed markets expand output to address the rising chronic disease burden and generic drug demand. The United States exported activated carbon worth USD 362 million, equal to 16.3% of global export value, confirming its central role in high-specification pharmaceutical carbon supply chains.

Stringent FDA and EMA regulatory mandates require pharmaceutical manufacturers to demonstrate effective impurity removal throughout production. Therefore, compliance-driven procurement sustains consistent carbon demand across drug manufacturers seeking reliable, validated purification solutions that satisfy international quality and safety requirements for pharmaceutical-grade outputs.

Rising prevalence of hospital-acquired infections drives adoption of advanced air and water filtration systems across healthcare facilities. Activated carbon plays a central role in HVAC filtration, water treatment, and surface decontamination in clinical environments. Haycarb PLC’s group revenue from coconut-shell-based activated carbon reached Rs 43.18 billion, supporting pharmaceutical and medical purification end markets and confirming sustained commercial demand from healthcare supply chains.

Restraints

Raw Material Volatility and High Certification Costs Constrain Market Expansion

Persistent volatility in coconut shell and coal raw material prices creates significant supply chain challenges for pharmaceutical-grade activated carbon producers. Raw material costs account for a substantial portion of production expenses, and price fluctuations directly compress manufacturer margins. Consequently, suppliers struggle to maintain stable pricing for pharmaceutical customers who require consistent quality carbon under long-term supply agreements and procurement contracts.

High certification and quality assurance costs present a meaningful barrier for producers seeking to supply pharmaceutical-grade activated carbon. Obtaining and maintaining approvals from regulatory bodies such as the FDA, EMA, and USP requires significant investment in testing, documentation, and process validation. Moreover, smaller manufacturers face disproportionate compliance burdens, limiting the pool of qualified suppliers available to pharmaceutical companies with rigorous vendor qualification requirements.

Supply chain disruptions affecting coconut shell-producing regions amplify raw material availability risks for activated carbon manufacturers. Climate-related impacts and agricultural cycles in key sourcing countries like Sri Lanka, India, and the Philippines affect feedstock supply consistency. Therefore, manufacturers dependent on natural biomass-derived precursors face periodic production constraints that limit their ability to scale output in response to growing pharmaceutical sector demand.

Growth Factors

Medical Applications, Sustainable Technologies, and Strategic Partnerships Drive Long-Term Expansion

Medical-grade activated carbon finds expanding applications in overdose treatment, gastrointestinal disorder therapies, and blood purification systems. Hemoperfusion cartridges and critical care devices increasingly integrate specialized carbon grades for toxin removal and organ support functions. Furthermore, according to WITS trade data, India’s exports of activated carbon to the United States alone reached USD 38,854.91 thousand, reflecting strong North American demand for pharmaceutical and medical-grade carbon products from Asian suppliers.

Sustainable reactivation technologies for spent carbon in pharmaceutical wastewater streams represent a significant growth opportunity. Companies invest in reactivation infrastructure that extends carbon service life and reduces disposal costs. Consequently, circular economy models gain traction among pharmaceutical manufacturers seeking to lower total purification costs while meeting environmental compliance obligations tied to wastewater management and sustainability reporting programs.

Strategic supplier collaborations with leading biotech firms create customized filtration solution opportunities for activated carbon producers. Biotech companies developing novel therapeutics require highly specific carbon grades tailored to their unique purification challenges. Additionally, Ingevity Corporation’s Performance Materials segment, which includes activated carbon for purification markets, delivered net sales of USD 609.6 million in 2024, up from USD 608.2 million in 2023, confirming sustained commercial momentum in this segment.

Regional Analysis

Asia Pacific Dominates the Activated Carbon for Pharma and Healthcare Market with a Market Share of 52.7%, Valued at USD 262.3 Billion

Asia Pacific holds a commanding 52.7% market share, valued at USD 262.3 billion, driven by large-scale generic drug manufacturing in India, China, and South Korea. Regional governments actively support pharmaceutical production expansion through policy incentives.

North America maintains a strong demand for pharmaceutical-grade activated carbon, supported by the presence of major drug manufacturers and strict FDA regulatory requirements. The United States serves as both a leading consumer and exporter of activated carbon. Reflecting competitive pricing pressure that North American and European buyers monitor closely when sourcing purification materials.

Europe represents a mature and quality-sensitive market for activated carbon in pharmaceutical and healthcare applications. EMA compliance requirements drive consistent demand for validated, high-purity carbon products across drug manufacturing facilities in Germany, France, the UK, and Italy. Additionally, European pharmaceutical companies pursue sustainable sourcing strategies, favoring bio-based and certified carbon suppliers aligned with EU Green Deal manufacturing principles.

Latin America shows growing adoption of activated carbon in pharmaceutical manufacturing, particularly in Brazil and Mexico, where domestic drug production capacity expands. Regional investments in healthcare infrastructure and generics manufacturing support purification material demand. However, market growth remains tempered by budget constraints and regulatory fragmentation across national pharmaceutical approval systems in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Jacobi Group operates as one of the world’s largest producers of activated carbon, supplying the pharmaceutical and healthcare markets across multiple continents. The company maintains a diversified product portfolio covering powdered, granular, and impregnated carbon grades suited for drug manufacturing purification. Its global manufacturing footprint and technical support capabilities position it as a preferred supplier for pharmaceutical companies seeking reliable, high-purity activated carbon solutions.

Chemviron serves the pharmaceutical and healthcare sector with a range of activated carbon products engineered for stringent purification applications. The company focuses on delivering consistent product quality and technical expertise to support customers navigating complex regulatory compliance requirements. Moreover, Chemviron’s established relationships with European pharmaceutical manufacturers and its quality-certified production processes strengthen its competitive position in the high-specification pharma carbon segment.

Haycarb PLC specializes in coconut shell-based activated carbon, positioning itself as a sustainable supplier to pharmaceutical and healthcare markets globally. The company’s operations in Sri Lanka and international distribution network support a reliable supply to purification-focused customers. Cilicant is a manufacturer of pharmaceutical desiccants and activated carbon sachets for healthcare packaging.

Boyce Carbon provides activated carbon solutions targeting pharmaceutical manufacturing and water purification applications. The company focuses on delivering technically validated carbon products that meet pharmaceutical purity standards for API and finished drug production. Additionally, Boyce Carbon works closely with procurement teams at drug manufacturers to customize product specifications and ensure consistent supply performance that meets quality management system requirements across customer facilities.

Top Key Players in the Market

- Jacobi Group

- Chemviron

- Haycarb PLC

- Boyce Carbon

- Southern Carbon Pvt. Ltd.

- Suneeta Carbons

- Calgon Carbon Corporation

- Karbonous Inc.

- Norit

- Donau Carbon GmbH

Recent Developments

- In 2025, Chemviron (European operations of Calgon Carbon Corporation, a Kuraray subsidiary) provides specialised high-purity powdered and granular activated carbons tailored for pharmaceutical purification and decolourisation. Key offerings include acid-washed grades (CPG LF coal-based and Acticarbone wood-based from renewable marine pine) with low acid-soluble ash/iron, minimal fines/dust, and compliance with USP monograph/Food Chemical Codex standards.

- In 2025, Haycarb PLC (Sri Lanka-based, global producer of coconut-shell activated carbon) offers ultra-pure pharmaceutical-grade activated carbon in powdered, granular, and extruded forms for medical/pharmaceutical/cosmetic use. Applications include toxin/poison adsorption, purification of APIs/excipients/compounds, solvent recovery, dialysis filtration, and high-efficiency polishing in drug manufacturing.

Report Scope

Report Features Description Market Value (2025) USD 497.7 Billion Forecast Revenue (2035) USD 939.2 Billion CAGR (2026-2035) 6.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Powdered, Granular, Bead Carbon, Impregnated Carbon, Activated Fiber, Others), By Application (API Production, Finished Drug Production, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Jacobi Group, Chemviron, Haycarb PLC, Boyce Carbon, Southern Carbon Pvt. Ltd., Suneeta Carbons, Calgon Carbon Corporation, Karbonous Inc., Norit, Donau Carbon GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Activated Carbon For Pharma And Healthcare MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Activated Carbon For Pharma And Healthcare MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Jacobi Group

- Chemviron

- Haycarb PLC

- Boyce Carbon

- Southern Carbon Pvt. Ltd.

- Suneeta Carbons

- Calgon Carbon Corporation

- Karbonous Inc.

- Norit

- Donau Carbon GmbH

Our Clients

- 179453

- February 2026