Quick Navigation

Report Overview

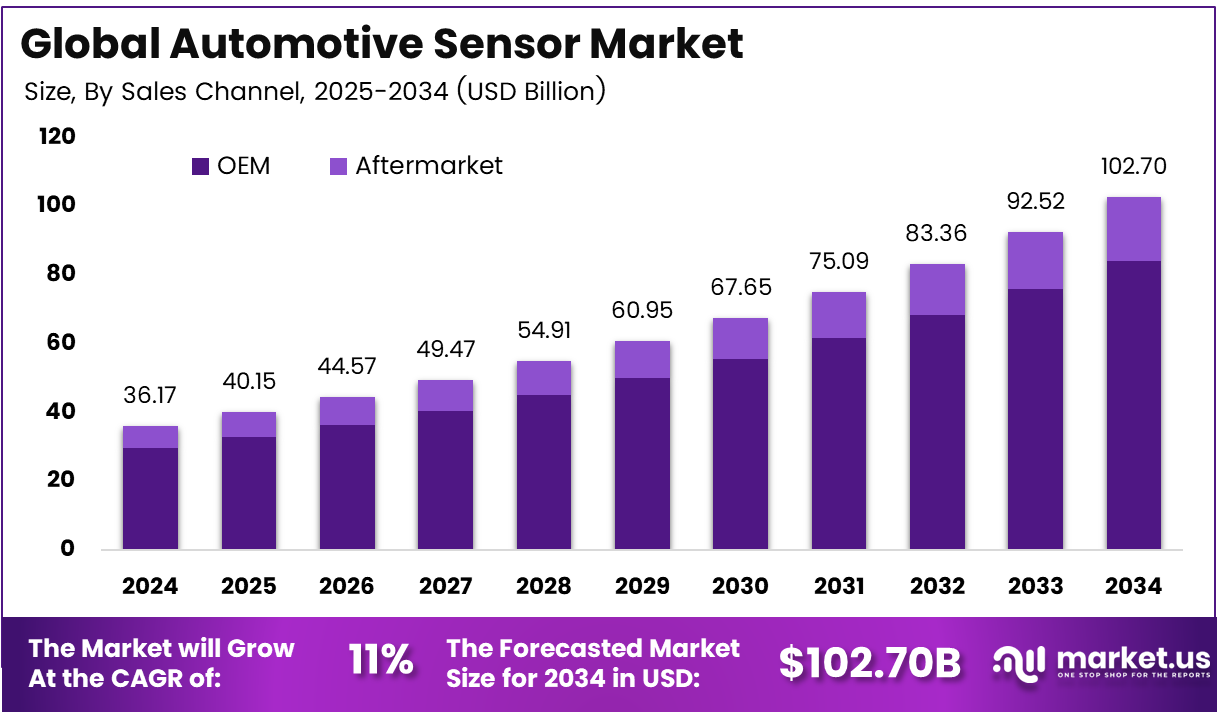

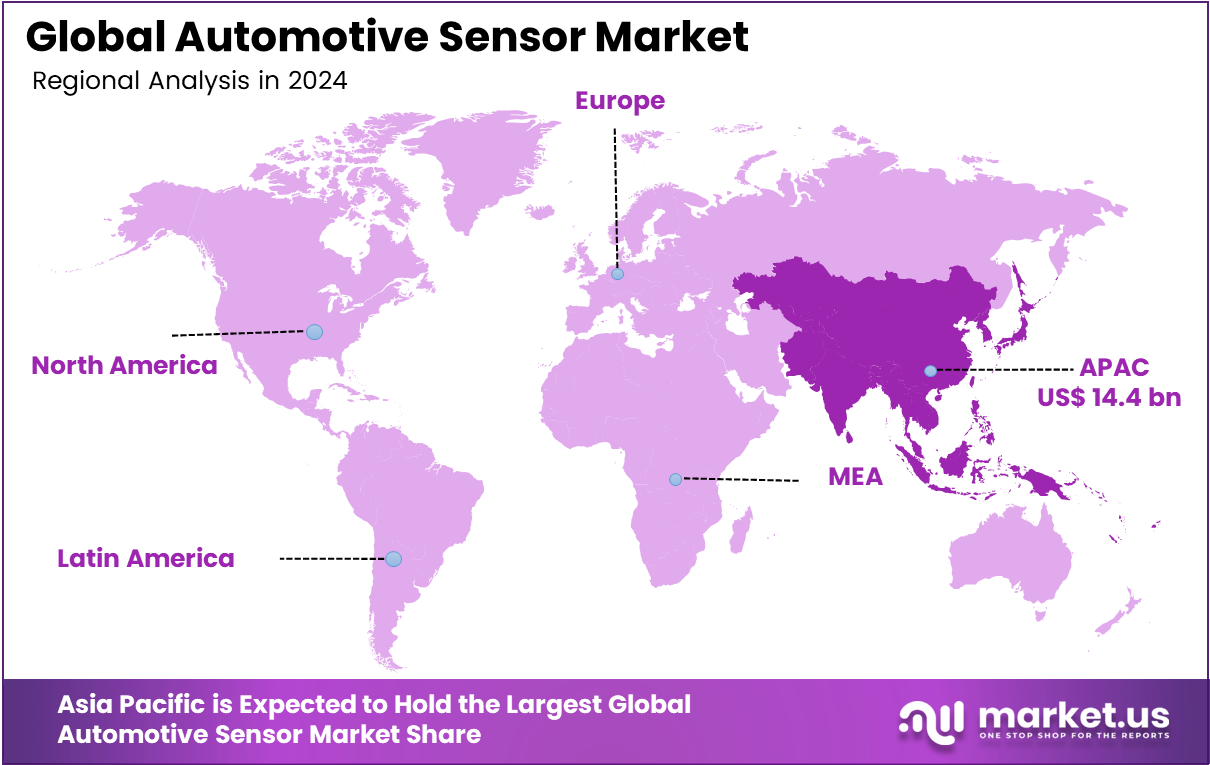

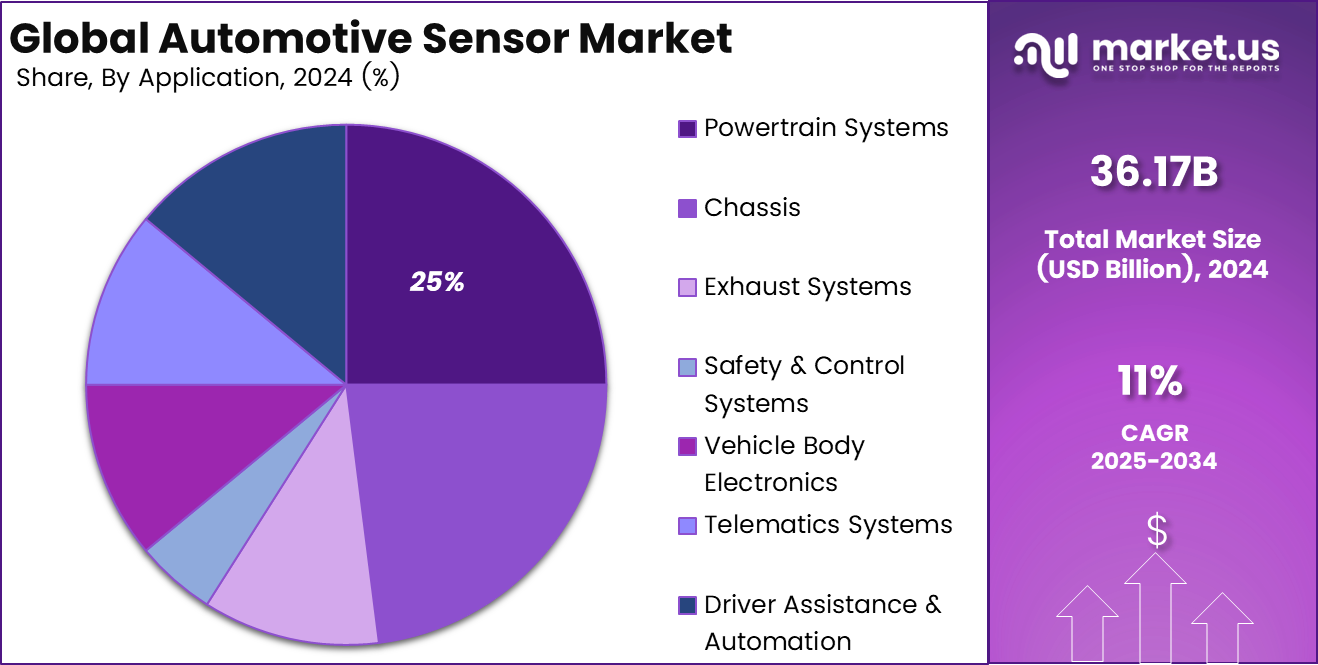

The Global Automotive Sensor Market size is expected to be worth around USD 102.70 billion by 2034, from USD 36.17 billion in 2024, growing at a CAGR of 11% during the forecast period from 2025 to 2034. Asia Pacific held a dominant market position, capturing more than a 40% share, holding USD 14.4 billion in revenue.

The market for automotive sensors is driven by the rapid adoption of Advanced Driver-Assistance Systems (ADAS), autonomous driving technologies, and the shift toward electric and connected vehicles. Increasing regulatory mandates for safety, emissions control, and vehicle efficiency are accelerating sensor integration across powertrain, chassis, and in-cabin systems.

Additionally, consumer demand for enhanced driving experiences and predictive maintenance is propelling the deployment of smart, IoT-enabled sensors. These trends collectively position sensors as foundational components in next-generation automotive innovation.

For instance, in June 2025, ISRO partnered with key automotive industry stakeholders to advance sensor technology through the adaptation of space-grade innovations for mobility applications. This initiative aims to leverage satellite-based navigation, high-precision imaging, and robust sensor architectures developed for aerospace to enhance vehicle safety, navigation, and autonomy.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 36.17 Bn |

| Forecast Revenue (2034) | USD 102.70 Bn |

| CAGR (2025-2034) | 11% |

| Largest market in 2024 | Asia Pacific [40% market share] |

Key Takeaway

- In 2024, the Pressure Sensors segment held a dominant market position, capturing a 20% share of the Global Automotive Sensor Market.

- In 2024, the OEM segment held a dominant market position, capturing an 82% share of the Global Automotive Sensor Market.

- In 2024, the Passenger Car segment held a dominant market position, capturing an 80% share of the Global Automotive Sensor Market.

- In 2024, the Powertrain Systems segment held a dominant market position, capturing a 25% share of the Global Automotive Sensor Market.

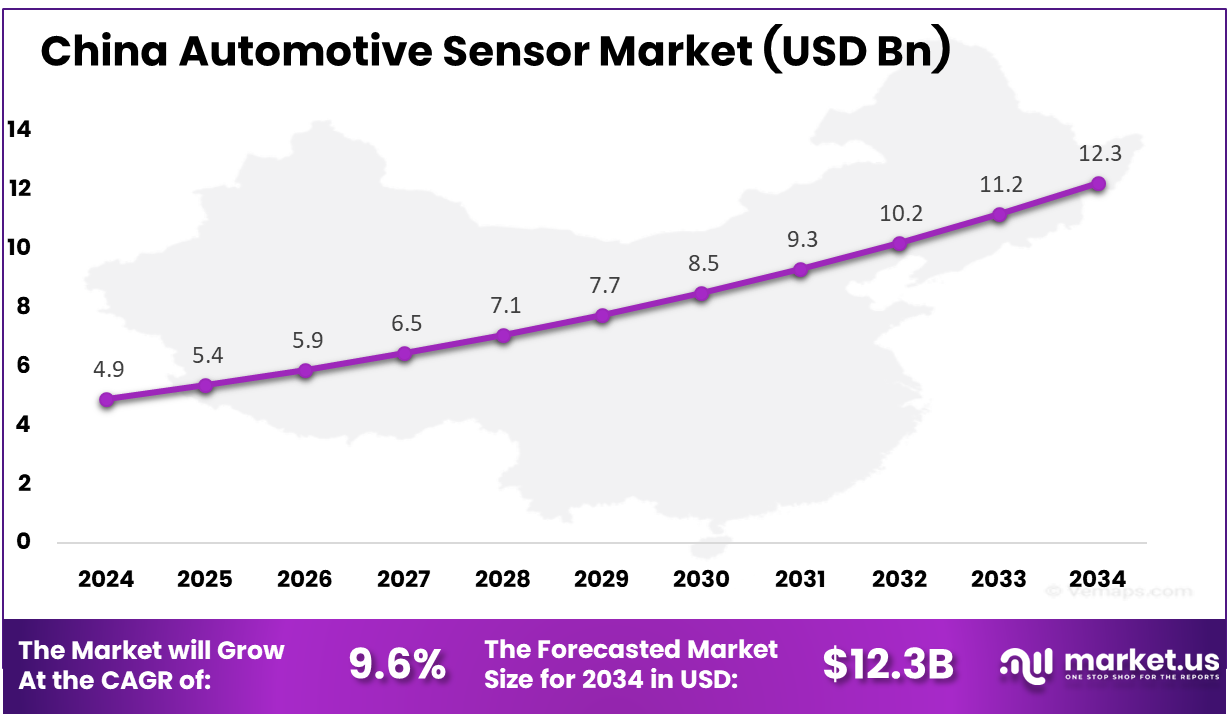

- The China Automotive Sensor Market was valued at USD 4.9 billion in 2024, with a robust CAGR of 9.6%.

- In 2024, the Asia Pacific held a dominant market position in the Global Automotive Sensor Market, capturing more than 40% share.

Regional Analysis

In 2024, the Asia Pacific held a dominant market position in the Global Automotive Sensor Market, capturing more than a 40% share, holding USD 14.4 billion in revenue. This dominance is due to its high vehicle production volumes, rapid adoption of electric and autonomous vehicles, and strong presence of leading OEMs. Government initiatives promoting EV adoption, smart mobility, and safety regulations further accelerated sensor integration. Additionally, countries like China, Japan, and South Korea invested heavily in R&D and semiconductor manufacturing, creating a robust ecosystem that supports continuous innovation and cost-effective sensor deployment at scale.

For instance, in October 2024, Sony Semiconductor unveiled an industry-first image sensor for automotive cameras, reinforcing Asia Pacific’s leadership in sensor innovation. As a regional tech powerhouse, Japan continues to drive high-performance sensor development for ADAS and autonomous systems.

China Automotive Sensor Market Size

The market for Automotive Sensors within China is growing tremendously and is currently valued at USD 4.9 billion; the market has a projected CAGR of 9.6%. The market is growing due to China’s strong focus on electric vehicles, smart mobility, and autonomous technologies. Regulatory mandates on emissions, safety, and intelligent transport systems are accelerating sensor deployment across vehicles. Growing use of ADAS, along with AI and IoT integration, is boosting demand for real-time diagnostics and safety features. Furthermore, substantial investments in R&D, manufacturing, and digital infrastructure are reinforcing this expansion, positioning China as a leading hub for innovation in automotive sensor technologies.

For instance, in August 2025, FORVIA HELLA began series production of a next-generation steering sensor tailored for a leading Chinese carmaker, underscoring China’s growing influence in the global automotive sensor market. This development highlights the country’s strategic focus on advanced driver-assistance technologies and localized innovation.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Sensor Type Analysis

In 2024, the Pressure Sensors segment held a dominant market position, capturing a 20% share of the Global Automotive Sensor Market. Pressure sensors play a vital role in tracking key vehicle systems, including engine efficiency, tire pressure, fuel management, and braking performance. With tightening emission standards and evolving safety regulations, automakers are adopting these sensors to improve diagnostics, compliance, and overall vehicle efficiency. Their importance has grown further with the rise of electric vehicles and ADAS technologies, which depend on precise pressure data for critical functions.

For instance, in September 2025, a new pressure sensor assembly tailored for Honda models such as the Accord, Fit, and HR-V was launched, underscoring the continued demand for high-precision pressure sensing in both combustion and hybrid vehicles. These sensors play a crucial role in fuel efficiency, emissions control, and safety system performance.

Sales Channel Analysis

In 2024, the OEM segment held a dominant market position, capturing an 82% share of the Global Automotive Sensor Market. This dominance is due to the rising sensor integration in new vehicles to meet safety, efficiency, and regulatory standards. Automakers are embedding advanced sensors across ADAS, powertrain, and in-cabin systems to support electrification, autonomy, and connectivity. The growing production of EVs and smart vehicles has further increased OEM reliance on high-performance, factory-installed sensors, positioning OEMs as the primary channel for large-scale sensor deployment and innovation.

For instance, in March 2025, Aeva announced it had secured an OEM deal to supply its next-generation LiDAR technology for an advanced vehicle platform, underscoring the critical role of OEMs in driving sensor adoption. This partnership reflects the increasing demand from automakers for integrated, high-performance sensor solutions to support autonomous capabilities.

Vehicle Type Analysis

In 2024, the Passenger Car segment held a dominant market position, capturing an 80% share of the Global Automotive Sensor Market. This dominance is due to the rising consumer demand for safety, comfort, and connectivity features. The widespread integration of ADAS, infotainment systems, and emission control technologies in passenger vehicles has significantly increased sensor usage. Additionally, the rapid growth of electric and hybrid passenger cars, coupled with regulatory mandates for safety and emissions, has further propelled sensor deployment, making this segment the largest consumer of automotive sensor technologies.

For instance, in May 2021, HELLA introduced 77GHz radar sensors into series production for passenger vehicles, marking a pivotal advancement in driver assistance technologies. These compact, high-resolution sensors enable features like blind spot detection, lane change assist, and rear cross-traffic alerts.

Application Analysis

In 2024, the Powertrain Systems segment held a dominant market position, capturing a 25% share of the Global Automotive Sensor Market. This dominance is due to the critical role sensors play in optimizing engine performance, fuel efficiency, and emissions control. Pressure, temperature, position, and speed sensors are integral to ensuring real-time monitoring and precise control of combustion, transmission, and hybrid systems. As global emission norms tightened and electrification advanced, automakers increasingly relied on sensor-driven powertrain technologies to enhance vehicle performance, regulatory compliance, and operational reliability.

For instance, in September 2025, ZF Group secured strategic orders in India, expanding into the powertrain and tyre testing segments with multi-million euro projects. This move underscores the growing demand for advanced sensor technologies to monitor and optimize vehicle powertrain systems.

Key Market Segments

By Sensor Type

- Temperature Sensors

- Pressure Sensors

- Oxygen Sensors

- Speed Sensors

- Position Sensors

- Radar Sensors

- Image Sensors

- Lidar Sensors

- Other Sensor Types

By Sales Channel

- OEM

- Aftermarket

By Vehicle Type

- Passenger Car

- Commercial Vehicle

By Application

- Powertrain Systems

- Chassis

- Exhaust Systems

- Safety & Control Systems

- Vehicle Body Electronics

- Telematics Systems

- Driver Assistance & Automation

- Other Applications

Market Dynamics

Drivers - ADAS & Autonomous Vehicles

The rapid evolution of Advanced Driver-Assistance Systems (ADAS) and autonomous vehicle (AV) platforms is significantly accelerating demand for high-performance sensors. Radar, LiDAR, ultrasonic, and vision-based camera modules are essential enablers of functions such as adaptive cruise control, lane-keeping, automated braking, and full autonomy. As automakers race toward higher SAE levels of automation, sensor integration becomes foundational, not optional. This trend underscores sensors’ critical role in enhancing vehicle safety, driving intelligence, and regulatory compliance across global markets.

For instance, in August 2025, Honda entered a multi-year partnership with Helm.ai to accelerate the development of next-generation autonomous driving technologies. This collaboration focuses on leveraging Helm.ai’s advanced neural network software for real-time perception and sensor fusion, critical for Level 3+ automation.

Restraint - High Development and Production Costs

Despite increasing demand, the automotive sensor market faces cost-related headwinds. Advanced sensors, particularly LiDAR, radar, and integrated vision modules, require high R&D investment, specialized materials, and complex manufacturing processes. These factors drive up production costs, limiting affordability and broader adoption, especially in mid- and entry-level vehicle segments. Moreover, pricing pressures from OEMs and tier-1 suppliers compress margins for sensor manufacturers, necessitating innovation in cost engineering, economies of scale, and vertical integration to sustain profitability and competitiveness.

For instance, in March 2025, EE Times highlighted efforts to address sensor design cost pressures through the adoption of single-chip LIN-based 8-bit microcontrollers (MCUs). These compact, integrated solutions reduce bill-of-materials (BOM) costs and design complexity in vehicle sensor modules by consolidating communication, processing, and control functions.

Opportunities - Smart & IoT-Enabled Sensors

The emergence of smart, IoT-enabled sensors represents a transformative opportunity in automotive innovation. These sensors offer advanced features such as real-time diagnostics, edge processing, wireless communication, and adaptive calibration. Their integration supports predictive maintenance, autonomous navigation, and seamless vehicle-to-everything (V2X) connectivity. By enhancing system intelligence and reducing data latency, smart sensors align with the growing demand for connected, autonomous, and software-defined vehicles. This evolution positions sensor technology as a strategic enabler of next-generation mobility ecosystems.

For instance, in March 2025, Mercedes-Benz revealed its decision to integrate Hesai’s advanced LiDAR sensors into its global smart car lineup, signaling a pivotal shift toward intelligent, data-rich vehicle platforms. These smart sensors, equipped with real-time perception and digital connectivity features, enhance object detection, environmental mapping, and system redundancy.

Challenges - Complexity & Integration Difficulty

Integrating multiple sensor types within increasingly complex vehicle architectures poses a major engineering challenge. Compatibility across ECUs, data fusion requirements, thermal management, and compliance with safety standards make design and validation highly resource-intensive. Additionally, ensuring seamless interoperability between radar, LiDAR, cameras, and ultrasonic sensors, while managing latency and power consumption, requires sophisticated development environments and multidisciplinary collaboration. These technical complexities can delay product cycles and elevate costs, creating barriers for OEMs and suppliers aiming for rapid innovation.

For instance, in February 2025, a report from SemiEngineering highlighted how ADAS advancements are intensifying the complexity of automotive sensor fusion. As systems integrate radar, LiDAR, ultrasonic, and camera modules, synchronizing diverse data streams in real time becomes a formidable engineering challenge.

Latest Trends

The convergence of electric vehicle (EV) architectures and autonomous driving technologies is reshaping the automotive sensor landscape. As vehicles shift toward software-defined, electrified platforms, demand grows for sensors that monitor battery health, motor performance, thermal systems, and driver monitoring. Concurrently, AV functionality expands sensor roles in navigation, perception, and situational awareness. This ecosystem evolution is prompting OEMs and suppliers to develop multi-functional, ruggedized, and interoperable sensor solutions tailored to modular EV and AV platforms.

For instance, in August 2025, HCLTech announced a strategic collaboration with Astemo and Cypremos to accelerate innovation in the autonomous vehicle ecosystem. This partnership underscores a broader industry shift toward integrating cloud-native platforms, AI-driven control systems, and real-time sensor intelligence across EV and AV architectures.

Key Players Analysis

One of the leading players in May 2025, DENSO Corporation, announced a strategic collaboration with ROHM Co., Ltd. to co-develop advanced analog ICs for automotive systems. This alliance focuses on enhancing performance and reliability in applications supporting electrification and autonomous driving, such as battery management, power control, and sensor interface systems. By strengthening semiconductor integration at the component level, the partnership addresses growing demand for compact, efficient, and robust electronics critical to next-generation mobility platforms.

Top Key Players in the Market

- DENSO Corporation

- Infineon Technologies AG

- Robert Bosch GmbH

- Texas Instruments Inc.

- Sensata Technologies Holding PLC

- Aptiv PLC (Delphi Automotive)

- CTS Corporation

- Maxim Integrated Products Inc.

- NXP Semiconductors NV

- Analog Devices Inc.

- Continental AG

- Littelfuse Inc.

- Hitachi Automotive Systems Americas Inc.

- Other Key Players

Recent Developments

- In March 2025, Bosch introduced a new radar sensor built on RF CMOS technology, which integrates high-frequency and digital circuitry on a single chip, bolstering imaging performance and enabling scalable ADAS and autonomous applications.

- In November 2024, Continental forged a strategic partnership with NOVOSENSE Microelectronics to co-develop automotive-grade sensor ICs tailored for safety-critical powertrain systems, such as battery monitoring and airbag deployment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 36.17 Billion |

| Forecast Revenue (2034) | USD 102.70 Billion |

| CAGR (2025-2034) | 11% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Sensor Type (Temperature Sensors, Pressure Sensors, Oxygen Sensors, Speed Sensors, Position Sensors, Radar Sensors, Image Sensors, Lidar Sensors, Other Sensor Types), By Sales Channel (OEM, Aftermarket), By Vehicle Type (Passenger Car, Commercial Vehicle), By Application (Powertrain Systems, Chassis, Exhaust Systems, Safety & Control Systems, Vehicle Body Electronics, Telematics Systems, Driver Assistance & Automation, Other Applications) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | DENSO Corporation, Infineon Technologies AG, Robert Bosch GmbH, Texas Instruments Inc., Sensata Technologies Holding PLC, Aptiv PLC (Delphi Automotive), CTS Corporation, Maxim Integrated Products Inc., NXP Semiconductors NV, Analog Devices Inc., Continental AG, Littelfuse Inc., Hitachi Automotive Systems Americas Inc., Other Key Players |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |