Global 3D Printing Photopolymers Market By Technology (Stereolithography (SLA), Digital Light Processing (DLP), Continuous Digital Light Processing (cDLP), PolyJet Printing and Others), By Application (Dental, Medical and Healthcare, Audiology, Jewellery, Automotive, Prototyping, Industrial and Engineering, Electronics and Others), By Performance Type (Low Performance, Mid Performance and High Performance), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181087

- Number of Pages: 284

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

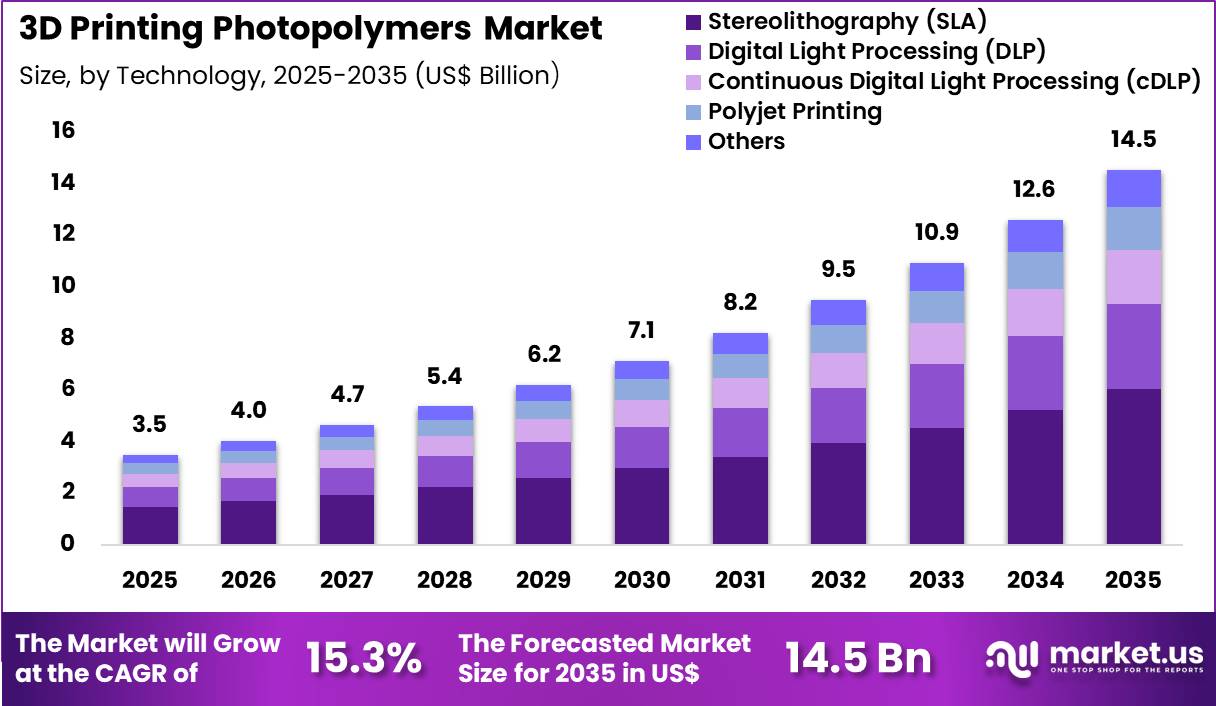

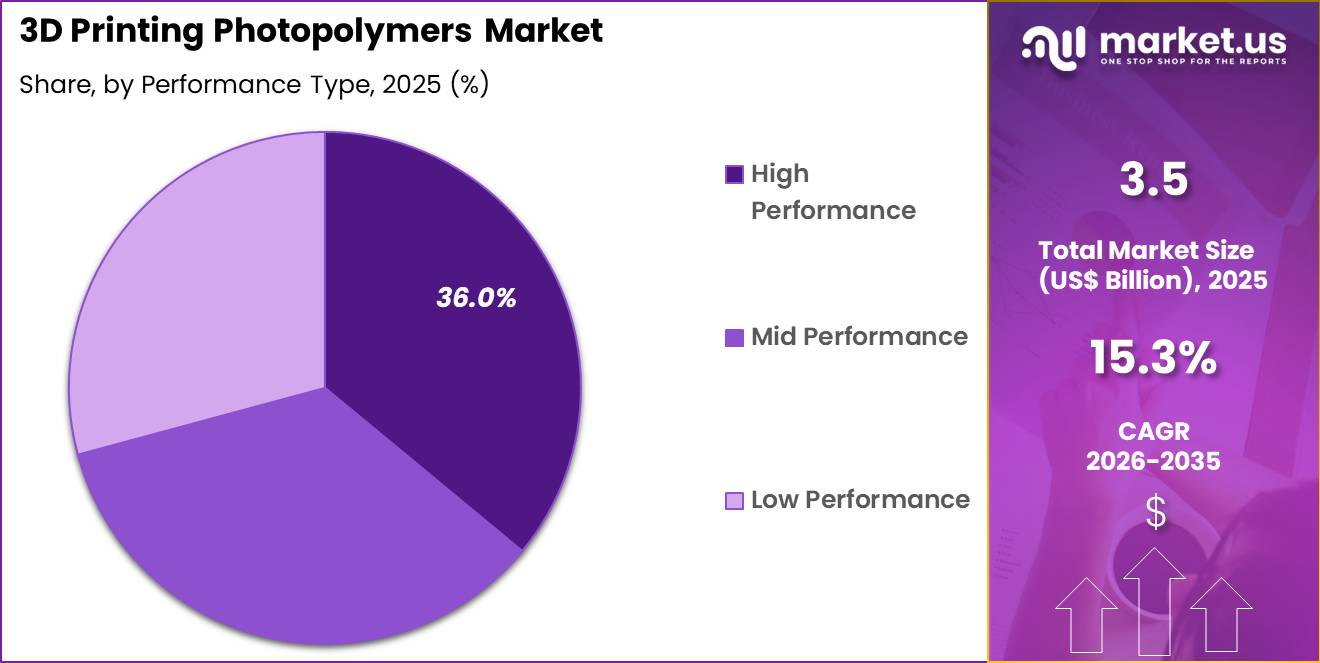

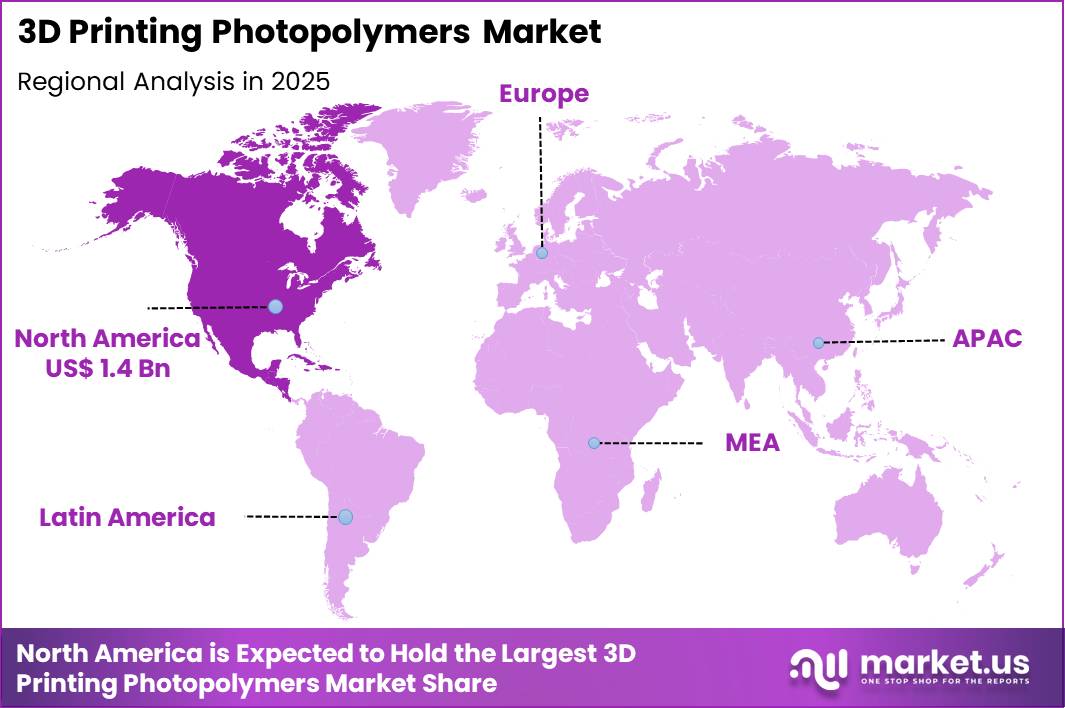

The Global 3D Printing Photopolymers Market size is expected to be worth around US$ 14.5 Billion by 2035 from US$ 3.5 Billion in 2025, growing at a CAGR of 15.3% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.4% share with a revenue of US$ 1.4 Billion.

Increasing demand for high-precision additive manufacturing accelerates the 3D printing photopolymers market as industries require resins that deliver superior resolution, mechanical performance, and functional properties for complex applications.

Manufacturers increasingly utilize photopolymer resins in stereolithography and digital light processing to produce detailed prototypes and end-use parts in consumer electronics, where transparent or translucent housings and intricate internal geometries demand excellent surface finish and dimensional accuracy. These materials support dental applications by enabling the fabrication of custom aligners, surgical guides, and temporary crowns with biocompatible formulations that ensure patient safety and fit precision.

In the medical sector, photopolymers facilitate production of hearing aid shells and anatomical models, offering smooth finishes and durability suitable for prolonged skin contact. Automotive engineers apply high-performance resins to create lightweight functional components such as connectors and housings that withstand thermal and mechanical stresses.

Aerospace designers employ toughened photopolymers for jigs, fixtures, and low-volume production parts requiring resistance to vibration and impact. In April 2024, Formlabs obtained FDA clearance for its Dental LT Clear V2 resin. The approval allows the material to be used for dental applications and broadens the company’s portfolio of medical-grade materials for dental 3D printing.

Manufacturers pursue opportunities to develop specialized photopolymers with enhanced thermal stability and chemical resistance, expanding applications in demanding industrial environments where components face elevated temperatures or aggressive fluids.

Developers advance castable and sinterable resins that enable direct metal casting and ceramic production, broadening utility in jewelry manufacturing and high-precision tooling. These innovations facilitate multi-material printing that combines rigid and flexible photopolymers in a single build, supporting functional prototypes with integrated gaskets or hinges.

Opportunities emerge in sustainable formulations using bio-based monomers that reduce environmental impact while maintaining print quality. Companies invest in low-shrinkage resins with improved post-cure stability, addressing challenges in large-format and high-resolution prints.

In March 2024, BASF expanded its additive manufacturing materials portfolio with the introduction of Ultracur3D HT, a high-temperature photopolymer resin. The material is designed for demanding industrial applications, particularly in automotive and aerospace components that require improved heat resistance and mechanical stability.

Recent trends emphasize engineering-grade resins with tunable properties and hybrid printing techniques, positioning the market for growth in production-scale additive manufacturing across medical, industrial, and consumer sectors.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.5 Billion, with a CAGR of 15.3%, and is expected to reach US$ 14.5 billion by the year 2035.

- The technology segment is divided into stereolithography (SLA), digital light processing (DLP), continuous digital light processing (cDLP), polyjet printing and others, with stereolithography (sla)taking the lead with a market share of 41.6%.

- Considering application, the market is divided into dental, medical and healthcare, audiology, jewellery, automotive, prototyping, industrial and engineering, electronics and others. Among these, dental held a significant share of 28.4%.

- Furthermore, concerning the performance type segment, the market is segregated into low performance, mid performance and high performance. The high performance sector stands out as the dominant player, holding the largest revenue share of 36.0% in the market.

- North America led the market by securing a market share of 39.4%.

Technology Analysis

Stereolithography accounted for 41.6% of growth within technology and dominate the 3D printing photopolymers market due to its high precision and strong compatibility with liquid photopolymer materials. SLA systems cure resin layer by layer using ultraviolet lasers, which allows manufacturers to produce detailed and smooth surface components.

Industries including dentistry, medical devices, and electronics rely on SLA printers to fabricate intricate prototypes and customized components. The dental sector increasingly uses SLA-based photopolymers for aligner molds and surgical guides as digital dentistry expands globally.

Research and development activities in additive manufacturing continue to improve resin curing speed and print resolution. The segment is expected to strengthen as manufacturers seek accurate and repeatable printing technologies for high-detail parts. Continuous improvements in resin chemistry and laser control systems are projected to enhance production efficiency and broaden industrial adoption.

Application Analysis

Dental applications accounted for 28.4% of growth within application and dominate the 3D printing photopolymers market because digital dentistry increasingly relies on resin-based additive manufacturing. Dental laboratories and orthodontic clinics produce aligner molds, dental models, surgical guides, and temporary restorations using photopolymer resins.

According to the American Association of Orthodontists, millions of orthodontic procedures occur annually worldwide, which significantly increases demand for custom dental appliances. Photopolymers allow technicians to create highly accurate dental structures that match patient-specific digital scans.

The segment is expected to expand as dental practices adopt fully digital workflows that combine intraoral scanning, design software, and 3D printing technologies. Growing demand for cosmetic dentistry and orthodontic treatments further supports the production of resin-based dental components. Continuous innovation in biocompatible dental photopolymers strengthens the adoption of this application segment.

Performance Type Analysis

High performance photopolymers accounted for 36.0% of growth within performance type and dominate the market due to their enhanced mechanical strength, chemical resistance, and thermal stability. Manufacturers increasingly adopt advanced resin formulations to produce functional prototypes and end-use components that require strong material performance.

Industries such as automotive, electronics, and medical device manufacturing rely on high performance photopolymers to test product designs before large-scale production. These materials support complex geometries while maintaining structural durability during mechanical stress.

The segment is anticipated to grow as additive manufacturing transitions from prototyping to functional production applications. Companies continue to invest in research programs that improve resin durability and heat resistance. Expanding industrial adoption of additive manufacturing technologies is expected to increase demand for high performance photopolymer materials across engineering and manufacturing sectors.

Key Market Segments

By Technology

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Continuous Digital Light Processing (cDLP)

- PolyJet Printing

- Others

By Application

- Dental

- Medical and Healthcare

- Audiology

- Jewellery

- Automotive

- Prototyping

- Industrial and Engineering

- Electronics

- Others

By Performance Type

- Low Performance

- Mid Performance

- High Performance

Drivers

Rising demand for high-precision photopolymer resins in dental applications is driving the market.

Stratasys Ltd. reported recurring consumables revenue growth of 6.3% in the second quarter of 2024 compared to the corresponding period in 2023. This category includes photopolymer resins formulated for high-accuracy applications such as dental models, surgical guides, and orthodontic appliances.

The increase indicates greater utilization of installed PolyJet systems within dental laboratories and clinical settings. Enhanced material properties enable the production of intricate geometries with superior surface finish and dimensional stability. Dental professionals integrate these resins into fully digital workflows beginning with intraoral scanning and culminating in final restorations.

The growth facilitates expanded training initiatives for technicians working with photopolymer-based processes. Reliable supply chains ensure consistent availability of specialized formulations tailored to dental requirements. The upward trend corresponds with increasing adoption of biocompatible resins for long-term intraoral use. This driver reinforces the critical role of photopolymers in advancing precision dentistry.

Restraints

Declining total revenue across additive manufacturing providers is restraining the market.

Stratasys Ltd. generated total revenue of $627.6 million in fiscal year 2023. Revenue decreased to $572.5 million in fiscal year 2024, reflecting an 8.8% reduction. The contraction continued in fiscal year 2025 with revenue reaching $551.1 million, a further 3.7% decline.

These successive reductions constrain capital allocation toward advancing photopolymer resin formulations. End-users postpone investments in new printer installations that rely on photopolymer consumables. The pattern introduces uncertainty in projecting material consumption volumes.

Suppliers adjust production schedules to align with lower utilization rates. The restraint diminishes enthusiasm for large-scale implementation of photopolymer technologies in production environments. Laboratories prioritize maintenance of current systems over exploratory trials with new resin variants. This factor limits the pace of market expansion for photopolymer materials during the 2023-2025 period.

Opportunities

Strategic partnerships for advanced photopolymer applications are creating growth opportunities.

A collaboration established in 2025 between a resin developer and a manufacturing partner enables mass production of shape memory polymer aligners utilizing specialized photopolymer formulations. The partnership combines material expertise with scalable production capabilities to deliver thermo-responsive orthodontic devices.

Opportunities arise for aligners that adapt dynamically to patient compliance and accelerate tooth movement. The alliance facilitates development of proprietary resin compositions optimized for aligner clarity, durability, and clinical performance. Dental laboratories gain access to advanced materials supporting customized treatment protocols.

The initiative supports regulatory advancement for innovative orthodontic appliances. Expanded manufacturing capacity enables penetration into high-growth regional markets. Such collaborations promote integration of responsive materials within digital orthodontic workflows.

The partnership fosters ongoing innovation in biocompatible photopolymer compositions for extended intraoral applications. This opportunity enhances treatment efficacy and strengthens differentiation in the orthodontic segment.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the 3D printing photopolymers market through manufacturing investment, research spending, and capital allocation across industrial and healthcare sectors. Inflation raises costs for chemical feedstocks, resin formulation, energy, and specialized packaging, which increases production expenses for photopolymer suppliers.

Higher interest rates reduce capital spending on additive manufacturing equipment and slow adoption in small and mid-sized enterprises. Geopolitical tensions disrupt global trade in specialty chemicals, pigments, and photoinitiators used in resin development, creating sourcing uncertainty.

Current US tariffs on imported chemical inputs and printing materials increase procurement costs and compress margins for manufacturers serving the US market. These pressures can delay product launches and limit experimentation with new resin formulations.

At the same time, companies expand domestic chemical sourcing and invest in regional production facilities to reduce external dependencies. Growing demand for high-precision manufacturing and customized production continues to support steady and confident market growth.

Latest Trends

Introduction of specialized photopolymer resins for industrial prototyping is driving the market.

A leading materials provider launched a new series of resin-based photopolymer formulations on December 3, 2025. The portfolio targets industrial applications requiring high-temperature resistance and accurate simulation of injection molding processes. These resins deliver improved mechanical properties suitable for functional prototyping and limited end-use components.

The launch addresses requirements for low-viscosity materials compatible with stereolithography and digital light processing systems. Users achieve reduced post-processing efforts and superior surface quality in complex geometries. The formulations integrate seamlessly into existing SLA and DLP printer platforms.

The development demonstrates continued commitment to broadening photopolymer versatility across manufacturing sectors. Early adopters confirm reliable performance in tooling and fixture validation tasks. The introduction accelerates deployment of advanced photopolymers in precision additive manufacturing workflows. Overall, this 2025 launch strengthens the position of specialized resins in demanding production environments.

Regional Analysis

North America is leading the 3D Printing Photopolymers Market

North America accounted for 39.4% of the 3D printing photopolymers market in 2025 as manufacturers, research laboratories, and healthcare innovators expanded adoption of resin based additive manufacturing technologies for high precision production.

Industries such as dental manufacturing, medical device prototyping, aerospace component development, and consumer electronics increasingly rely on photopolymer materials because these resins enable fine resolution printing and smooth surface finishes. The United States continues to lead global innovation in additive manufacturing, supported by strong research investment and advanced industrial infrastructure.

According to the National Science Foundation, the United States recorded about USD 886 billion in research and development spending in 2022, creating a strong foundation for continued development of advanced materials and additive manufacturing technologies.

Aerospace and defense companies across the region increasingly employ resin based printing systems to create complex prototypes and lightweight components during product development cycles. Medical device manufacturers also use advanced photopolymer materials to produce surgical guides, hearing aids, and dental appliances with highly detailed geometries.

Universities and technology institutes across the United States and Canada are expanding laboratory programs dedicated to advanced materials science and additive manufacturing research. Manufacturers are introducing improved photopolymer formulations that offer higher heat resistance, flexibility, and biocompatibility for specialized applications. These factors collectively supported the expansion of resin based additive manufacturing technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to record strong growth during the forecast period as industrial manufacturing, electronics production, and biomedical research expand across the region. Countries such as China, Japan, South Korea, and Singapore are investing heavily in advanced manufacturing technologies that integrate additive manufacturing into product design and prototyping workflows.

China’s National Bureau of Statistics reported that national research and development spending reached about 3.09 trillion yuan in 2022, reflecting substantial investment in high technology industries including advanced materials and additive manufacturing technologies.

Electronics manufacturers in the region increasingly rely on precision printing systems that use specialized resin materials to produce detailed prototypes and micro components for testing and design validation. Dental laboratories and healthcare device companies are also adopting resin based additive manufacturing to produce customized medical components.

Universities and technical institutes across Asia are expanding engineering programs focused on advanced manufacturing and materials science. Governments are supporting innovation through manufacturing technology parks and national industrial modernization programs.

Local materials companies are developing new resin formulations that match regional industrial requirements and cost structures. These developments are expected to accelerate adoption of advanced additive manufacturing materials across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Leading companies in the 3D Printing Photopolymers market expand their business by developing high-performance resin materials, strengthening collaborations with printer manufacturers, and introducing specialized formulations for industrial, dental, and medical applications.

Firms prioritize research in light-curable polymers that deliver improved mechanical strength, heat resistance, and surface accuracy for advanced additive manufacturing processes. Many suppliers also invest in ecosystem partnerships and workflow optimization programs that help customers adopt resin-based printing technologies across manufacturing sectors. Photopolymer materials enable the production of high-resolution components and prototypes used in industries such as healthcare, automotive, and electronics.

Henkel AG & Co. KGaA represents a notable participant in the 3D Printing Photopolymers market and operates as a global chemical and materials company headquartered in Düsseldorf, Germany. The company develops LOCTITE additive manufacturing resins engineered for functional parts and industrial applications, drawing on decades of expertise in adhesives and material science.

Competitors including BASF, Formlabs, and 3D Systems continue to introduce engineering-grade resins and collaborate with equipment manufacturers to broaden adoption of photopolymer technologies. These initiatives strengthen innovation capacity, expand industrial use cases, and accelerate commercialization across the 3D Printing Photopolymers market.

Top Key Players

- Stratasys Ltd.

- 3D Systems Corporation

- Formlabs Inc.

- Henkel AG & Co. KGaA

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- Carbon, Inc.

- Keystone Industries

- Shenzhen Esun Industrial Co., Ltd.

- Liqcreate

- Photocentric Ltd.

Recent Developments

- In the first quarter of 2024, Henkel acquired Mirage Resins, a company specializing in flexible photopolymer materials. The acquisition strengthens Henkel’s Loctite 3D Printing business by expanding its capabilities in advanced resin development for additive manufacturing.

- In February 2024, Carbon formed a partnership with BMW to collaborate on the development of advanced materials using Digital Light Synthesis technology. The partnership focuses on producing next-generation interior components for vehicles through additive manufacturing.

Report Scope

Report Features Description Market Value (2025) US$ 3.5 Billion Forecast Revenue (2035) US$ 14.5 Billion CAGR (2026-2035) 15.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Stereolithography (SLA), Digital Light Processing (DLP), Continuous Digital Light Processing (cDLP), PolyJet Printing and Others), By Application (Dental, Medical and Healthcare, Audiology, Jewellery, Automotive, Prototyping, Industrial and Engineering, Electronics and Others), By Performance Type (Low Performance, Mid Performance and High Performance) Regional Analysis North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Stratasys Ltd., 3D Systems Corporation, Formlabs Inc., Henkel AG & Co. KGaA, BASF SE, Arkema S.A., Evonik Industries AG, Carbon, Inc., Keystone Industries, Shenzhen Esun Industrial Co., Ltd., Liqcreate, Photocentric Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  3D Printing Photopolymers MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

3D Printing Photopolymers MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Stratasys Ltd.

- 3D Systems Corporation

- Formlabs Inc.

- Henkel AG & Co. KGaA

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- Carbon, Inc.

- Keystone Industries

- Shenzhen Esun Industrial Co., Ltd.

- Liqcreate

- Photocentric Ltd.

Our Clients

- 181087

- March 2026