Quick Navigation

Overview

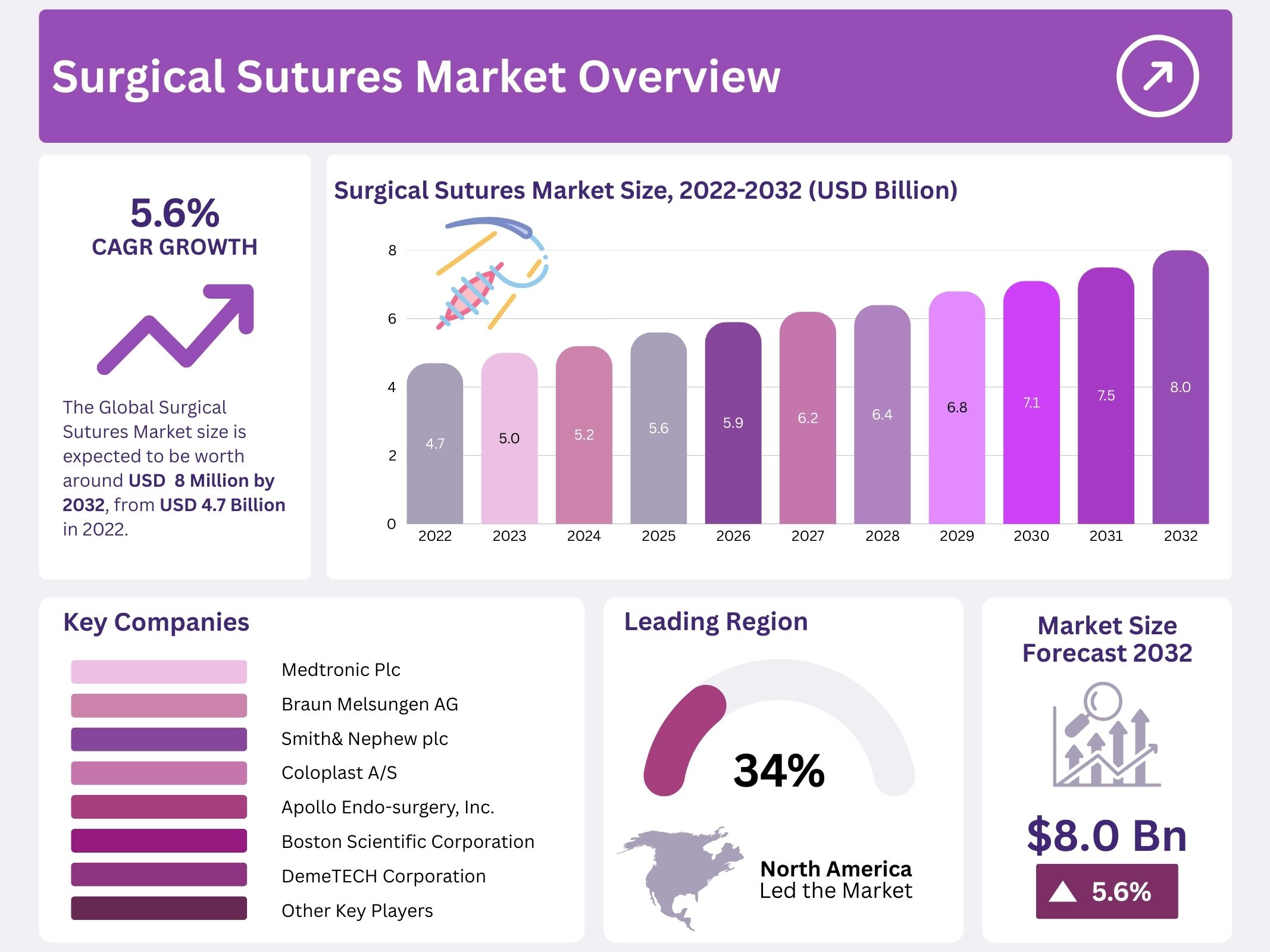

The Global Surgical Sutures Market was valued at USD 4.7 billion in 2022. It is projected to reach nearly USD 8 billion by 2032, expanding at a CAGR of 5.6% during 2023–2032. Growth is being driven by the rising prevalence of chronic diseases and the increasing volume of surgical procedures. Surgical sutures remain a vital component in cardiovascular, orthopedic, and cosmetic surgeries. The market is experiencing higher demand due to technological advancements, including the development of novel absorbable and non-absorbable sutures that improve patient outcomes.

Regulatory Landscape

The market is strongly influenced by stringent regulatory frameworks. In the United States, the Food and Drug Administration (FDA) classifies surgical sutures as Class II devices. These regulations require manufacturers to demonstrate tensile strength, knot security, and biocompatibility before approval. Such oversight ensures that sutures meet safety and efficacy standards for surgical use. Similar guidelines are also adopted by regulatory bodies in Europe and Asia, reinforcing patient safety and product reliability across global markets.

Market Drivers

Absorbable sutures dominate the market due to their convenience and reduced need for post-operative removal. Innovations in suture materials, such as synthetic fibers, are minimizing hypersensitivity risks and enhancing patient recovery times. Antibacterial absorbable sutures are gaining attention as they help reduce surgical site infections, leading to lower healthcare costs. The increasing burden of cardiovascular diseases, affecting over half a billion people globally according to the World Health Federation (2023), further accelerates market growth.

Industry Dynamics

Economic indicators, including GDP growth and employment rates, indirectly impact healthcare spending, which in turn influences demand for surgical sutures. Trade regulations and international agreements also play a role in shaping import and export trends. Investment in healthcare infrastructure by both governments and private entities supports the expansion of surgical facilities and access to advanced technologies. These developments collectively create favorable conditions for sustained market growth.

Outlook

The surgical sutures market is expected to maintain steady expansion during the forecast period. Rising surgical volumes, combined with material innovations and strict regulatory compliance, are key growth enablers. With continuous investments in healthcare systems worldwide, the demand for high-performance surgical sutures will continue to increase, ensuring their critical role in modern surgical practices.

Key Takeaways

- The global surgical sutures market is projected to attain USD 8.0 billion by 2032, fueled by rising surgeries and an expanding aging population.

- North America currently dominates the market, securing nearly 34% revenue share, largely supported by advanced healthcare systems and significant surgical procedure volumes.

- Asia-Pacific is forecasted as the fastest-growing region, supported by increasing disease prevalence, expanding surgeries, and investments in healthcare infrastructure development.

- Technological innovations in surgical sutures, including automated and advanced products, are contributing significantly to ongoing market expansion worldwide.

- Market constraints stem from alternatives such as surgical staplers and risks associated with surgical complications, limiting wider adoption of sutures in certain cases.

- Low and middle-income countries represent significant opportunities, benefiting from supportive regulations, improving medical infrastructure, and expanding access to healthcare services.

- Improved healthcare facilities, along with the expansion of health insurance coverage, are driving higher adoption of surgical sutures across global healthcare systems.

- Key trends shaping the market include development of elastic sutures, knotless technologies, and emerging innovations such as electronic sutures.

- Absorbable sutures account for 55% of global market share, reflecting strong demand due to convenience, reduced removal needs, and compatibility with biological healing.

- Multifilament sutures are emerging as the fastest-growing segment, attributed to superior flexibility, handling ease, and better knot security during surgical procedures.

Regional Analysis

North America dominates the surgical sutures market, accounting for 34% of the revenue share. The growth of this region is strongly influenced by the rising number of surgical procedures. This increase is largely driven by the expanding geriatric population, which requires more surgical interventions. Advanced healthcare infrastructure, along with the availability of modern medical facilities and equipment, further supports this dominance. As a result, North America continues to lead the global market and maintains its position as the largest contributor to surgical sutures adoption.

Europe is projected to experience steady growth during the forecast period. The region benefits from a highly developed healthcare system, which drives both demand and approval for surgical sutures. A growing number of surgeries across European countries strengthens the market outlook. Additionally, regulatory frameworks and supportive healthcare policies enhance adoption of advanced surgical products. This environment fosters significant growth potential in the coming years. Hence, Europe is expected to expand its role as an important regional market in surgical sutures globally.

Asia-Pacific is anticipated to record the highest CAGR during the forecast period. This expansion is driven by increasing cases of cardiovascular and gynecological diseases, leading to more surgical procedures. Rising awareness of advanced surgical devices, along with strong focus by global manufacturers on developing economies, supports market growth. Moreover, improvements in healthcare infrastructure and rising healthcare expenditure contribute positively. In contrast, Latin America and the Middle East & Africa are forecasted to grow moderately due to workforce shortages and limited healthcare access. However, gradual improvements may support moderate long-term growth.

Segmentation Analysis

Product Type Outlook: Absorbable vs. Non-Absorbable Sutures

The global surgical sutures market is divided into absorbable and non-absorbable sutures. Absorbable sutures lead the market with a 55% revenue share due to their wide use in delicate and deep wound management. Their strong tensile strength enables effective wound support and faster healing. Growing preference for absorbable sutures is driven by their natural degradation, eliminating the need for removal and improving patient recovery. This advantage continues to fuel demand, making them the dominant product type during the forecast period.

Filament Preferences: Multifilament Leading Over Monofilament

Sutures are also categorized into monofilament and multifilament types. Multifilament sutures dominate in terms of revenue and are expected to grow fastest due to their flexibility, strength, and ease of use. Surgeons prefer them because they provide superior handling during operations. Monofilament sutures, although offering lower infection risks, are less favored due to handling difficulties. Their stiffness and risk of knot failure limit adoption. Materials such as nylon and polydioxanone are commonly used. Despite advantages, operational challenges reduce their preference compared to multifilament sutures.

Form Segmentation: Synthetic Sutures Driving Market Growth

By form, synthetic sutures dominate the global market. They hold the largest share due to reduced hypersensitivity reactions and greater effectiveness in wound closure. Their reliable performance and lower risk profile have strengthened adoption across healthcare facilities. Natural sutures, while functional, show slower growth because of potential tissue interactions that can complicate healing. The industry’s preference for synthetic sutures aligns with rising demand for advanced, safe, and efficient wound care solutions. Ongoing innovations continue to reinforce synthetic sutures as the preferred option globally.

Application Landscape: Orthopedics and Cardiology at the Forefront

In terms of application, the orthopedics segment holds the largest share at 43%, driven by the rising aging population and high surgical frequency. Gynecology also contributes significantly, supported by technological advances in the field. Cardiology is forecast to grow most rapidly due to the rising incidence of heart disorders and related surgeries. General surgery is expanding due to increasing accidents and procedures. Other applications contribute moderately. Each segment highlights distinct medical needs, with orthopedics and cardiology emerging as strong growth drivers in this evolving market.

End-User Insights: Hospitals, ASCs, and Emerging Specialty Clinics

End-users are primarily hospitals and ambulatory surgical centers (ASCs), both dominating due to the high volume of procedures and favorable reimbursement policies. These facilities have skilled professionals and advanced technologies for complex surgeries, ensuring their leadership position. Specialty clinics, however, are projected to grow at a strong rate due to personalized care and shorter wait times, particularly in developing regions. The rising prominence of clinics alongside established hospital systems underscores dynamic growth patterns. Collectively, end-user demand continues to expand as surgical needs and healthcare infrastructure evolve.

Key Players Analysis

The global surgical sutures market is led by major players such as Medtronic and B. Braun Melsungen AG. These companies focus heavily on innovation and the development of new technologies. Their strategies are centered on strengthening manufacturing capabilities to meet increasing surgical demands. Through continuous improvements, they maintain strong competitive positions in the market. This leadership has been sustained by investments in research, development, and capacity expansion, ensuring long-term market dominance and consistent growth across key regions worldwide.

Other significant companies in the market include Coloplast A/S, Boston Scientific Corporation, DemeTECH Corporation, and Endo-Surgery, Inc. These firms leverage advanced technologies to support complex surgical procedures. Their efforts are directed toward improving the safety, efficiency, and precision of suturing techniques. By expanding their product portfolios, they address the growing demand from both developed and emerging healthcare markets. The strategic focus on innovation enables them to remain relevant in a highly competitive environment, thereby enhancing their overall market share.

The competitive strategies of these players revolve around technological advancements and manufacturing expansion. Investment in production efficiency and advanced R&D allows them to meet rising global healthcare needs. Emphasis is placed on developing sutures suitable for a wide range of surgical applications. This includes the adoption of novel materials and automated production systems. Their ability to combine product innovation with enhanced manufacturing capacity positions them strongly in the global surgical sutures industry, ensuring resilience against market challenges and sustaining profitability over the long term.

Top Leading Surgical Sutures Market Key Players Are

- Medtronic Plc

- Braun Melsungen AG

- Smith& Nephew plc

- Coloplast A/S

- Apollo Endo-surgery, Inc.

- Boston Scientific Corporation

- DemeTECH Corporation

- TEPHA INC.

- Kono Seisakusho Co, Ltd.

- Internacional Framaceutica S.A. de C.V.

- Johnson & Johnson

- Teleflex Incorporated

- Healthium MedTech

- Mellon Medical B.V.

- GPC Medical Ltd.

- Stryker Corporation

- Integra Life Sciences Corporation

- Other Key Players

Conclusion

The global surgical sutures market is set for steady growth, supported by rising surgical procedures, a growing elderly population, and continuous innovations in suture technology. Absorbable and synthetic sutures are gaining preference due to their effectiveness, safety, and patient convenience. North America remains the leading market, while Asia-Pacific is projected to expand at the fastest pace with improving healthcare infrastructure and rising disease prevalence. Despite challenges from alternatives such as staplers, demand is expected to remain strong across diverse surgical fields. With ongoing advancements, increasing healthcare investments, and supportive regulations, surgical sutures will continue to play a vital role in modern medical practices worldwide.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Surgical Navigation Systems Market || Surgical Robotics Market || Surgical Equipment Market || Surgical Lights Market || Surgical Stapling Devices Market || Surgical Microscopes Market || Minimally Invasive Surgical Instruments Market || Surgical Gloves Market || Surgical Sealants and Adhesives Market || Surgical Hat Market