Quick Navigation

Overview

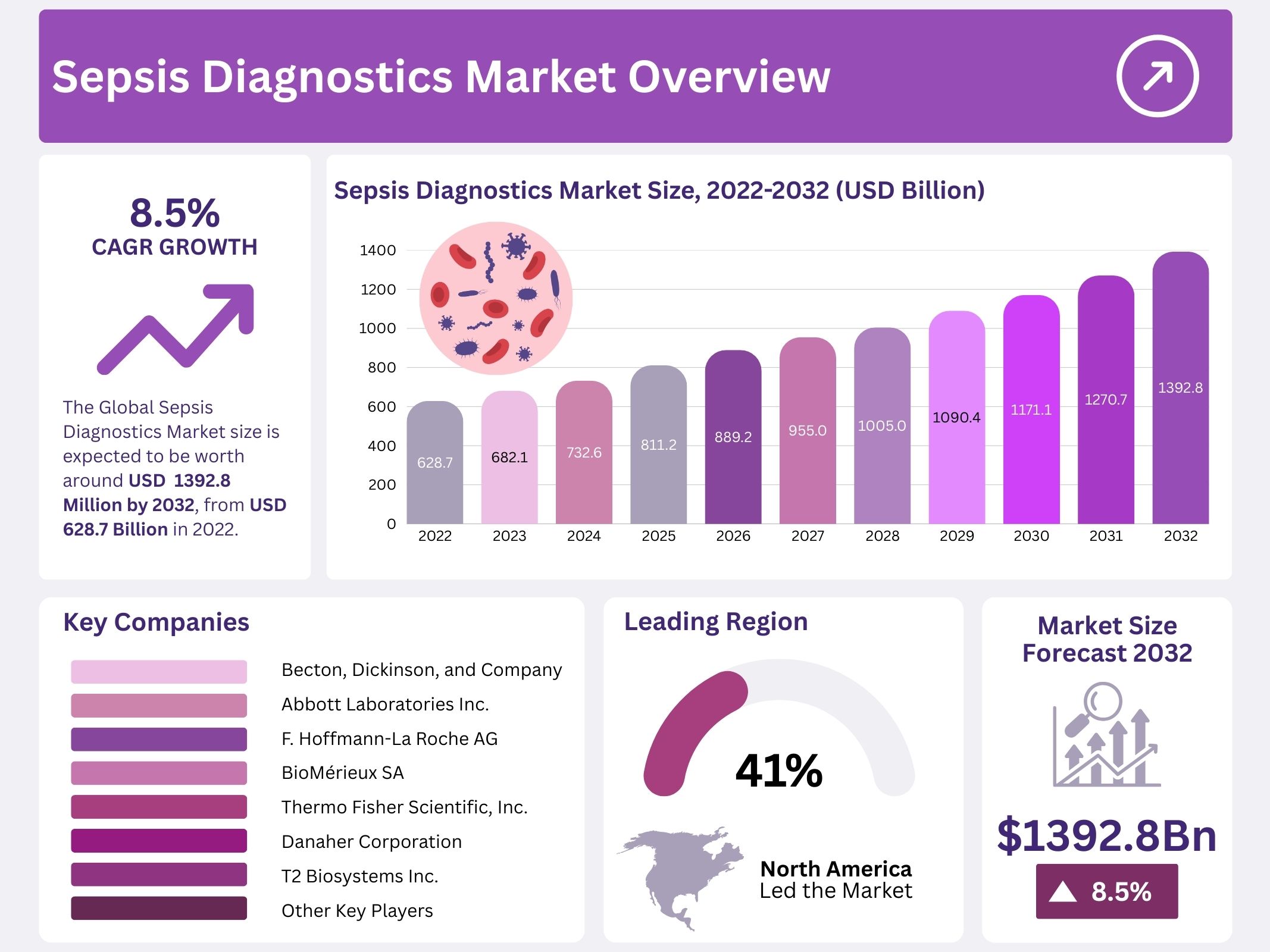

The Global Sepsis Diagnostics Market is projected to reach USD 1,392.8 million by 2032, up from USD 628.7 million in 2022, with a compound annual growth rate (CAGR) of 8.5% from 2023 to 2032. Sepsis is a life-threatening condition caused by a dysregulated immune response to infection. If left untreated, it can lead to multiple organ failure and death. Early detection is therefore critical. Sepsis diagnostics include clinical assessment, laboratory tests, imaging methods, and pathogen identification. The demand for faster and more accurate diagnostic solutions is fueling market expansion during the forecast period.

The increasing prevalence of sepsis remains a primary growth driver. According to the Centers for Disease Control and Prevention (CDC), over 1.7 million adults in the United States develop sepsis annually. It contributes to one-third of hospital fatalities and accounts for nearly 35% of hospital deaths. Furthermore, 19% of patients are readmitted within 30 days, while 40% face readmission within 90 days. Notably, 87% of sepsis cases begin outside hospital settings. Each hour of delayed treatment raises mortality risk by up to 9%, highlighting the urgent need for rapid diagnostic methods.

Growing awareness and investment in healthcare research are further strengthening market growth. Governments worldwide are increasing funding for infectious disease diagnostics. For instance, the National Institute of Allergy and Infectious Diseases (NIAID) allocated USD 17 million in 2020 to support the Centers for Research in Emerging Infectious Diseases. Over five years, the program will receive approximately USD 82 million, aimed at studying how infections spread from wildlife to humans. Such large-scale investments are expected to encourage the development of advanced sepsis diagnostic technologies.

Technological innovation plays a crucial role in advancing diagnostic accuracy. Molecular diagnostic techniques, point-of-care testing, and next-generation sequencing are being integrated into sepsis detection. These solutions allow clinicians to identify pathogens more quickly and assess antibiotic resistance. Imaging methods, including CT scans and ultrasounds, remain vital in locating the source of infection. In addition, increasing cases of hospital-acquired infections and pneumonia are stimulating demand for advanced diagnostic systems across hospitals and laboratories.

Overall, the market outlook for sepsis diagnostics is positive. Rising sepsis prevalence, aging populations, and increasing healthcare investments are expected to drive sustained growth. Rapid diagnostic solutions will be essential in reducing mortality and healthcare costs linked to sepsis. With ongoing research initiatives and government funding, the industry is set to experience strong adoption of innovative technologies. The combination of awareness campaigns, improved clinical practices, and advanced diagnostic tools is likely to ensure consistent market expansion through 2032.

Key Takeaways

- The global sepsis diagnostics market is projected to reach USD 1,392.8 million by 2032, expanding at a compound annual growth rate of 8.5%.

- Sepsis diagnostics focus on identifying a life-threatening infection-related condition using clinical evaluations, laboratory testing, and imaging tools such as CT scans and X-rays.

- Market growth is driven by increasing sepsis prevalence, aging population, hospital-acquired infections, pneumonia incidence, and adoption of advanced diagnostic technologies worldwide.

- In the United States, 1.7 million adult sepsis cases occur annually, accounting for nearly one-third of hospitalizations ending in patient fatalities.

- Blood culture media holds a 39% share, while diagnostic instruments are anticipated to experience the fastest growth in sepsis detection technologies.

- Bacterial sepsis dominates with 75% market share, while fungal sepsis diagnosis is gaining significant traction due to higher detection demand.

- Conventional diagnostic methods currently lead with 54% share, though automated diagnostic technologies are expected to expand rapidly in the coming years.

- Microbiology-based diagnostics dominate with 45% share, while molecular diagnostic methods show strong growth momentum due to faster and more accurate sepsis detection.

- Hospitals and clinics account for 71% of total demand, whereas pathology and reference laboratories are expected to witness accelerated adoption.

- North America leads with a 41% market share, while the Asia Pacific region is forecasted to experience the highest growth rate.

Regional Analysis

The sepsis diagnostics market in North America accounted for the largest share of 41%, with revenue of USD 257.7 million in 2022. Growth in the region is supported by rising cases of sepsis and other infectious diseases. Increasing research and development investments in advanced diagnostic solutions are also driving market expansion. According to the CDC, over 1.7 million adults in the U.S. are affected by sepsis annually, with nearly 270,000 deaths. This burden highlights the urgent need for efficient and rapid diagnostic tools across the healthcare system.

The increasing prevalence of hospital-related deaths linked to sepsis is a significant growth driver. The CDC noted that one in three hospital deaths is caused by sepsis. The availability of advanced healthcare infrastructure and favorable reimbursement policies strengthens market opportunities in North America. The presence of key players offering innovative diagnostic solutions further supports regional dominance. Strategic partnerships, product launches, and technological advancements are expected to sustain the growth momentum throughout the forecast period.

The Asia Pacific region is projected to register strong growth in the coming years. Rising hospital-acquired infections (HAIs) are creating substantial demand for sepsis diagnostics. The growing burden of infectious diseases, rising investments in healthcare facilities, and supportive government initiatives are additional growth factors. Increased awareness about sepsis diagnosis and monitoring is improving adoption rates. Expanding healthcare access in countries such as China and India is expected to accelerate demand. As a result, Asia Pacific is likely to emerge as a high-growth market for sepsis diagnostics during the forecast period.

Segmentation Analysis

The blood culture media segment is expected to dominate the sepsis diagnostics market, holding a share of around 39%. The rising burden of sepsis, a severe and life-threatening condition, continues to drive demand for accurate diagnostic tools. Blood culture media play a critical role in detecting pathogens causing bloodstream infections, thereby guiding the selection of appropriate antibiotic treatment. The ability of this method to track treatment efficacy further strengthens its adoption. Consequently, the segment is likely to maintain its strong market position during the forecast period.

The instruments segment is projected to grow at a rapid pace in the coming years. Instruments are essential for collecting, processing, and analyzing clinical samples, enabling healthcare professionals to achieve timely and accurate diagnoses. The increasing emphasis on early detection of sepsis and the growing need for efficient workflows in diagnostic laboratories are key growth drivers. Rising investment in advanced diagnostic technologies is also likely to contribute to the expansion of this segment across both developed and emerging healthcare markets globally.

Bacterial sepsis accounted for nearly 75% of market share in 2022 and is expected to remain dominant. The condition is a major cause of hospitalization, linked with high mortality and significant healthcare costs. Early and precise diagnostic methods are crucial in identifying patients needing urgent intervention. This facilitates better resource allocation in intensive care settings. At the same time, fungal sepsis is emerging as a notable segment, supported by growing awareness among clinicians and an increasing focus on rapid detection tools dedicated to fungal infections.

Conventional diagnostic methods continue to lead the sepsis diagnostics market, with a revenue share of 54% in 2022. Their affordability, accessibility, and broad adoption in diverse healthcare settings are central to this dominance. These methods are widely used in facilities with limited resources, ensuring broad applicability. However, automated diagnostics are projected to witness the fastest growth. The rising prevalence of sepsis and the need for faster and more accurate results are driving demand for automation, which improves efficiency and accuracy in laboratory operations worldwide.

Hospitals and clinics remain the largest end-users, representing 71% of the sepsis diagnostics market. The demand is influenced by the urgent need for timely diagnosis and its critical role in reducing mortality. Hospitals prioritize investments in diagnostic solutions to meet regulatory requirements and improve patient outcomes. In contrast, pathology and reference laboratories are expected to grow significantly. Their role in providing specialized testing, high-volume diagnostic capacity, and research-driven solutions is increasing. This makes them important stakeholders in advancing accurate and efficient sepsis diagnosis globally.

Key Players Analysis

The global sepsis diagnostics market is highly fragmented due to the increasing number of companies offering diagnostic solutions. The rising prevalence of infectious diseases has created a strong demand for accurate and timely testing options. This demand is boosting competition, as key players focus on expanding their product portfolios. Companies are striving to enhance diagnostic accuracy and reduce turnaround time. These factors are shaping the market landscape and ensuring constant innovation across different segments of sepsis diagnostics.

In addition, the adoption of strategic initiatives is significantly influencing market growth. Mergers, acquisitions, collaborations, and partnerships are being prioritized by leading players to strengthen their market presence. The launch of new and efficient diagnostic tools is further accelerating competition. Market participants are investing heavily in research and development to address the unmet clinical needs. As a result, the global sepsis diagnostics market is expected to witness strong growth during the projected period.

Market Key Players

- Becton Dickinson and Company

- Abbott Laboratories Inc.

- F. Hoffmann-La Roche AG

- BioMérieux SA

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- T2 Biosystems Inc.

- Luminex Corp.

- Immunexpress Inc.

- Bruker Corporation

- Axis-Shield Diagnostics Ltd

- Other Key Players

Conclusion

The sepsis diagnostics market is set for steady growth, driven by rising cases of infection-related illnesses and the urgent need for faster and more reliable testing. Growing awareness among healthcare providers, along with strong government and research support, is encouraging the adoption of advanced diagnostic solutions. Hospitals and laboratories are prioritizing early detection to reduce risks and improve patient outcomes. With innovations in molecular diagnostics, automation, and imaging tools, the market is expected to see continuous technological progress. Overall, the combination of better clinical practices, wider healthcare access, and ongoing investments will ensure that sepsis diagnostics remain a vital part of global healthcare improvement.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Blood Culture Test Market || Point-of-Care Molecular Diagnostics Market || PCR Molecular Diagnostics Market || Core Clinical Molecular Diagnostics Market || Biomarkers Market || Digital Biomarkers Market