Global Wax Market Size, Share, And Industry Analysis Report By Wax Type (Mineral Wax, Synthetic Wax, Natural Wax), By Application (Candles, Packaging, Coating and Polishes, Hot-melt Adhesives, Cosmetic and Toiletries, Plastic and Rubber), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 179122

- Number of Pages: 265

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

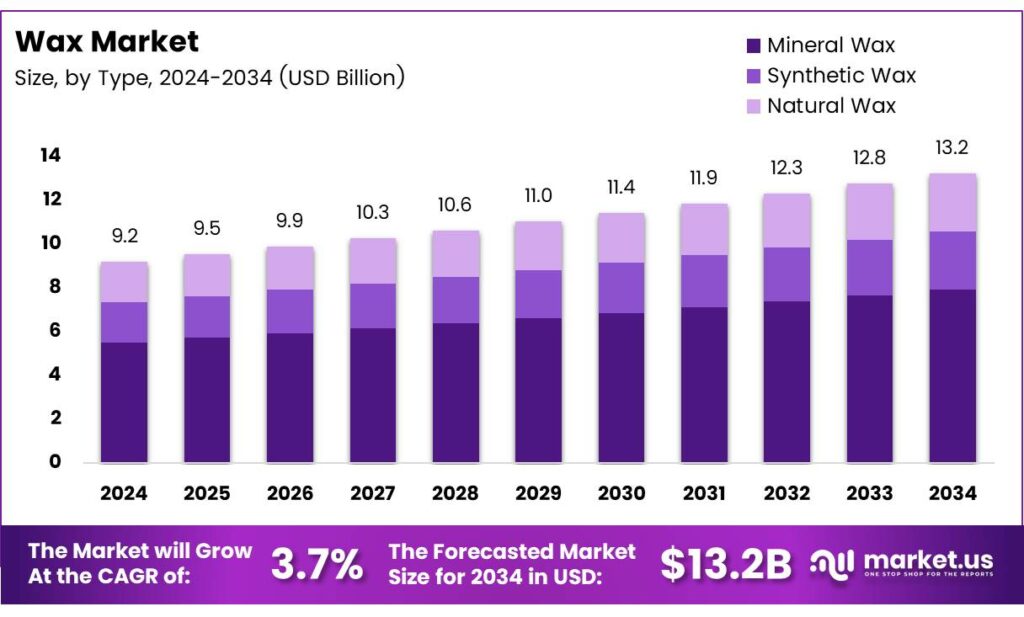

The Global Wax Market size is expected to be worth around USD 13.2 billion by 2034 from USD 9.2 billion in 2024, growing at a CAGR of 3.7% during the forecast period 2025 to 2034.

The wax market covers a broad range of natural, mineral, and synthetic wax products used across industries. These materials serve critical functions in candle manufacturing, packaging, coatings, cosmetics, adhesives, and rubber processing. Their versatility makes them essential inputs across both consumer and industrial supply chains globally.

Mineral waxes, particularly paraffin wax, remain the backbone of global production. However, growing consumer awareness about sustainability is pushing demand toward natural and bio-based alternatives. Manufacturers now balance cost efficiency with eco-friendly innovation to meet shifting buyer expectations across developed and emerging markets.

- The U.S. retail sales of candle products reach approximately $3.14 billion annually, with member companies accounting for about 80% of all candles made domestically. This scale reflects how deeply wax-intensive products are embedded in everyday consumer spending across North America.

- EU-27 candle consumption in 2024 reached approximately 855,000 tons with a wholesale value of €1,948 million. This volume confirms Europe’s position as a major demand center for wax-based products, driven by strong home decoration and wellness trends across the region.

Investment in specialty wax applications is rising steadily. Industries such as electronics, 3D printing, and precision agriculture are creating demand for high-performance wax solutions beyond traditional uses. Moreover, clean beauty and sustainable packaging trends are accelerating innovation pipelines across the specialty and natural wax segments globally.

Key Takeaways

- The Global Wax Market is valued at USD 9.2 billion in 2024 and is projected to reach USD 13.2 billion by 2034, at a CAGR of 3.7% during the forecast period 2025 to 2034.

- Mineral Wax dominates with a 56.2% market share in 2025.

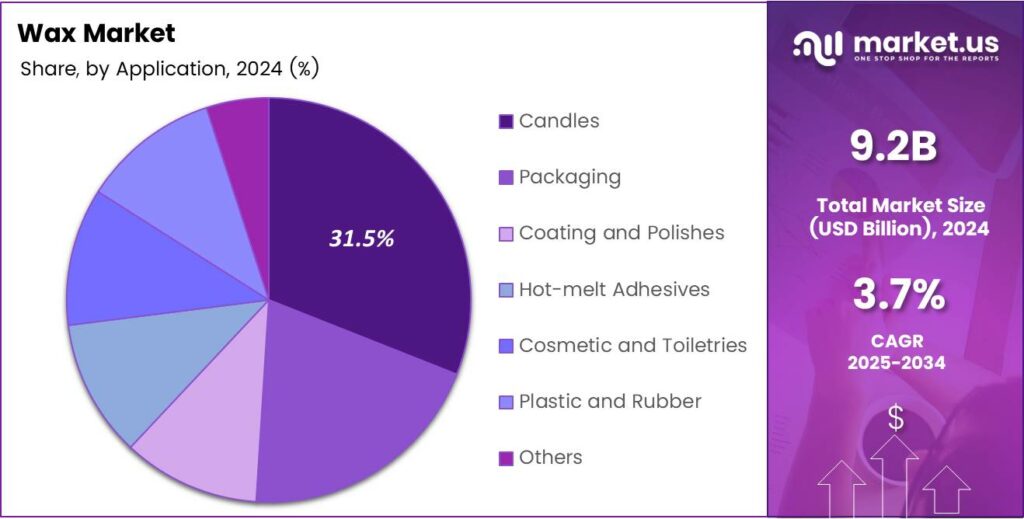

- Candles hold the leading position with a 31.5% share in 2025.

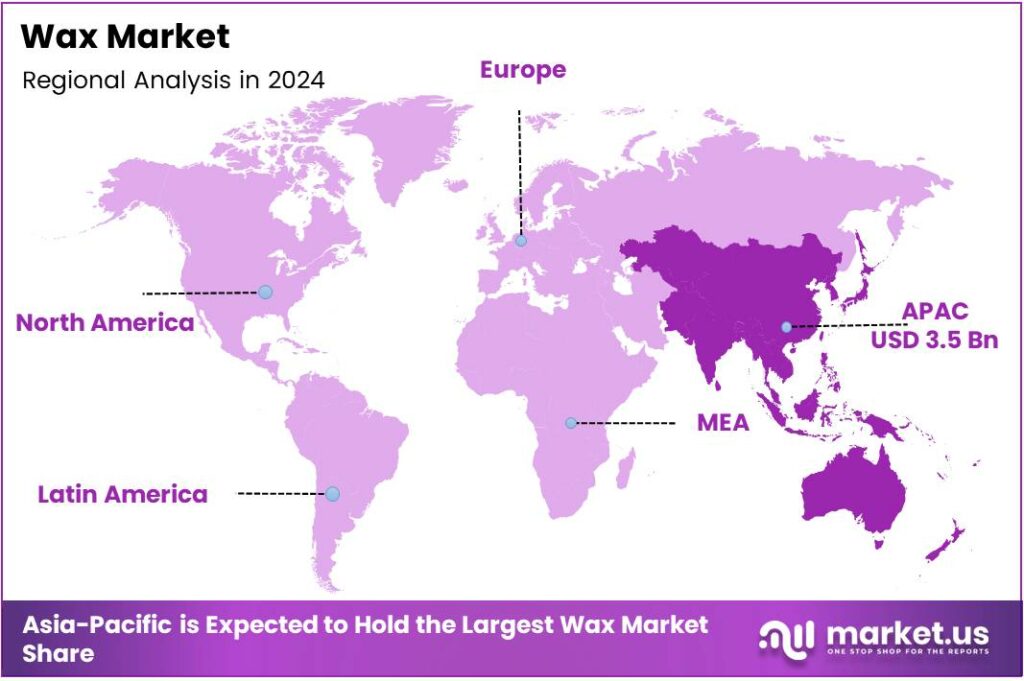

- Asia Pacific leads all regions with a 37.8% market share, valued at USD 3.5 billion.

Wax Type Analysis

Mineral Wax dominates with 56.2% due to its widespread availability, low cost, and broad industrial applicability.

In 2025, Mineral Wax held a dominant market position in the By Wax Type segment of the Wax Market, with a 56.2% share. This category includes Paraffin Wax, Microcrystalline Wax, Ozokerite, Ceresin, Montan Wax, and others. Their affordability and versatility across candles, coatings, and packaging applications continue to drive consistent global demand.

Synthetic Wax represents a growing segment driven by industrial requirements for high-performance materials. Products such as Polyethylene wax, Polypropylene wax, Polyamide, Fatty Acid Amide Waxes, and Fischer-Tropsch Waxes deliver superior durability and thermal stability. Moreover, these solutions gain traction in coatings, adhesives, and polymer processing, where natural waxes fall short.

Natural Wax serves a niche but rapidly expanding consumer base focused on sustainability. Beeswax, Soy Wax, Carnauba Wax, Candelilla Wax, Genuine Rice Bran Wax, and Laurel Wax lead this segment. Additionally, rising demand for clean-label cosmetics and eco-friendly candles pushes natural wax producers to scale up certified supply chains globally.

Application Analysis

Candles dominate with 31.5% due to robust consumer demand for home fragrance, décor, and wellness products.

In 2025, Candles held a dominant market position in the By Application segment of the Wax Market, with a 31.5% share. Rising interest in aromatherapy, home decoration, and wellness rituals fuels consistent demand. Additionally, premiumization trends in gifting and lifestyle products support steady revenue growth for wax-intensive candle manufacturers worldwide.

Packaging applications represent a substantial share driven by demand for moisture-resistant and protective coatings in food and consumer goods. Wax coatings extend shelf life and provide reliable barrier properties. Consequently, expanding food processing sectors and e-commerce packaging requirements continue to generate steady demand for functional wax-based packaging solutions globally.

Coating and Polishes, Hot-melt Adhesives, Cosmetic and Toiletries, Plastic and Rubber, and other end uses collectively diversify market demand across industrial and consumer channels. Cosmetics and personal care applications grow at an accelerated pace due to clean beauty preferences. Moreover, the rubber processing and adhesives sectors create a stable baseline demand for specialty wax formulations.

Key Market Segments

By Wax Type

- Mineral Wax

- Paraffin Wax

- Microcrystalline Wax

- Ozokerite

- Ceresin, Montan Wax

- Others

- Synthetic Wax

- Polyethylene wax

- Polypropylene wax

- Polyamide

- Fatty Acid Amide Waxes

- Fischer-Tropsch Waxes

- Others

- Natural Wax

- Beeswax

- Soy Wax

- Carnauba Wax

- Candelilla Wax

- Genuine Rice Bran Wax

- Laurel Wax

- Others

By Application

- Candles

- Packaging

- Coating and Polishes

- Hot-melt Adhesives

- Cosmetics and Toiletries

- Plastic and Rubber

- Others

Emerging Trends

Natural, Sustainable, and High-Performance Wax Variants Reshape Market Preferences

Aromatherapy and wellness-focused candles drive strong growth across home fragrance categories. Consumers increasingly associate premium scented candles with mental well-being and lifestyle enhancement. Consequently, brands are expanding their wax sourcing strategies to include natural blends that meet both performance requirements and sustainability certifications demanded by health-conscious buyers.

- Consumer preferences are shifting rapidly toward natural and eco-friendly wax variants. Products made from soy, beeswax, and carnauba wax are gaining popularity in candles and cosmetics as buyers prioritize clean-label formulations. Nippon Seiro’s dedicated wax producers, generating net sales of 22,045 million yen confirms the commercial scale behind these evolving product preferences.

High-performance synthetic waxes gain traction in advanced industrial coatings and flexible packaging applications. E-commerce growth and FMCG expansion require durable, moisture-resistant wax solutions for transit and shelf stability. Additionally, integration of specialty wax in flexible packaging driven by digital retail channels positions synthetic wax producers for consistent growth in the coming years.

Drivers

Broad Industrial Demand and Consumer Applications Accelerate Wax Market Growth

The packaging and coatings industries generate sustained demand for moisture-resistant wax solutions. Food manufacturers, pharmaceutical packagers, and consumer goods companies rely on wax coatings to ensure product quality and extend shelf life. Illustrating the commercial weight of home product categories that depend on wax inputs.

- Candle manufacturing drives the largest single application demand for wax globally. According to World Bank WITS trade, the United States imported candles valued at $1,091,317.46 thousand, representing 295,343,000 kg of wax-intensive products. This volume confirms that candle consumption sustains enormous raw material throughput and anchors downstream wax demand across supply chains.

Cosmetics and personal care brands increasingly incorporate wax for texture, stability, and formulation consistency. Rising consumer demand for premium skincare and color cosmetics supports this trend globally. Additionally, growing adoption in rubber processing, adhesives, and polymer manufacturing provides industrial diversification that insulates the overall wax market from single-sector demand fluctuations.

Restraints

Supply Chain Volatility and High Production Costs Challenge Wax Market Stability

Crude oil price volatility directly affects paraffin and mineral wax supply chains since these products derive from petroleum refining. Fluctuating feedstock costs create pricing instability that disrupts procurement budgets for manufacturers. Consequently, downstream buyers in candles, packaging, and coatings face unpredictable input costs that complicate long-term production planning and contract negotiations.

Natural and plant-based wax production faces structural cost pressures that limit widespread commercial adoption. Beeswax, carnauba, and soy wax require land, climate conditions, and harvesting labor that drive up per-unit costs significantly. However, growing eco-conscious demand means producers cannot easily abandon these materials, creating margin pressure that smaller manufacturers find particularly difficult to absorb.

Limited agricultural and biological availability of natural wax feedstocks constrains supply scalability. Unlike petroleum-derived mineral waxes, natural variants depend on crop yields, bee populations, and seasonal harvests. Therefore, supply disruptions from climate events or agricultural challenges create bottlenecks that prevent natural wax producers from meeting surging demand in cosmetics and sustainable consumer product categories.

Growth Factors

Bio-Based Innovation and Specialty Applications Open New Revenue Streams

Bio-based and renewable wax alternatives attract growing investment as brands pursue sustainability targets. Brands in cosmetics, food packaging, and home products accelerate sourcing shifts toward plant-derived wax solutions. Global candle exports totaled approximately $3.41 billion, showing the downstream commercial scale that bio-wax producers can tap with certified sustainable alternatives.

- India’s candle import market illustrates regional growth potential, with imports reaching roughly $8.05 million in 2024, sourced predominantly from China. This pattern reflects rising middle-class consumption of wax-based lifestyle products across Asia. Additionally, clean beauty formulation trends create rising opportunities for sustainably sourced waxes in cosmetics, supporting long-term revenue diversification for global producers.

Specialty wax demand grows in advanced applications, including 3D printing, electronics manufacturing, and precision agriculture. These sectors require customized wax formulations with specific melting points, adhesion properties, and chemical resistance. Moreover, food preservation coatings and post-harvest agricultural applications provide expanding market opportunities for wax producers capable of meeting food-grade safety and regulatory standards.

Regional Analysis

Asia Pacific Dominates the Wax Market with a Market Share of 37.8%, Valued at USD 3.5 Billion

Asia Pacific leads the global wax market, holding a 37.8% share valued at USD 3.5 billion in 2024. The region benefits from large-scale petrochemical refining capacity in China, India, and Japan that supports mineral wax production. Moreover, growing consumer product industries across Southeast Asia fuel demand for candles, cosmetics, and packaging wax solutions at scale.

North America represents a major demand center driven by the large candle, cosmetics, and industrial adhesives sectors. The United States alone accounts for the world’s largest candle import volumes, underlining strong consumer appetite for wax-based home fragrance products. Furthermore, Germany’s candle reflects parallel European demand dynamics that benchmark North American consumption trends.

Europe maintains a significant market presence across both wax production and consumption. Germany, the UK, and the Netherlands are major candle importers. Additionally, European regulatory frameworks around sustainable packaging and cosmetic formulations drive innovation investment across specialty and bio-based wax product lines.

The Middle East and Africa market benefits from proximity to crude oil refining infrastructure that supports affordable mineral wax output. Regional demand centers on industrial applications, including coatings, rubber processing, and packaging. However, limited domestic downstream manufacturing capacity means significant quantities of finished wax products continue to flow in through import channels from Asia and Europe.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Sasol Limited is a South African integrated energy and chemicals company and one of the world’s leading producers of Fischer-Tropsch waxes. The company operates extensive wax production assets serving global industrial and specialty markets. However, Sasol’s broader portfolio faces financial pressure.

Sinopec, formally China Petroleum and Chemical Corporation, operates as one of Asia’s largest petroleum refiners and a dominant supplier of paraffin wax globally. The company produces substantial volumes of wax as a by-product of its massive refining operations across China. Consequently, Sinopec’s scale and distribution network make it a critical price-setting force in the global mineral wax supply chain.

Royal Dutch Shell PLC participates in the wax market through its refining operations that yield paraffin and specialty wax products. Shell’s integrated upstream and downstream capabilities enable competitive feedstock access for wax production. Moreover, the company’s global logistics infrastructure supports efficient distribution of wax-based materials to industrial customers across packaging, coatings, and polymer processing industries worldwide.

Exxon Mobil Corporation produces a range of petroleum-derived waxes, including fully refined and semi-refined paraffin grades for industrial and consumer applications. The company serves candle manufacturers, cosmetic formulators, and packaging companies with consistent quality wax products. Additionally, ExxonMobil’s research capabilities support ongoing development of specialty wax grades tailored to evolving performance requirements in advanced industrial uses.

Top Key Players in the Market

- Sasol Limited

- Sinopec

- Royal Dutch Shell PLC

- Exxon Mobil Corporation

- Petróleo Brasileiro S.A.

- Kerax Limited

- DEUREX AG

- NIPPON SEIRO CO. LTD.

- Numaligarh Refinery Limited

- Strahi and Pitsch, Inc.

Recent Developments

- In 2025, Sasol Chemicals launched SASOLWAX LC Spray 30 G and SASOLWAX LC Spray 30 G-EF (micronised waxes). The waxes are MOSH/MOAH-free, outside ECHA microplastics/polymer definitions, and PFAS-free. They target inks, paints, coatings (architectural, powder, can/coil, wood), and printing inks for surface protection, slip, and rub resistance, and gloss control. PCF calculations follow ISO 14040/14044/14067 standards.

- In 2025, Sinopec Jingmen Company (Hubei) remains the largest lube oil and petroleum wax production base in Central-South China, with crude processing capacity and 43 refining units (including solvent dewaxing for light/heavy feeds). It produces fully-refined paraffin wax and microcrystalline wax (for rubber, cosmetics, and food industries).

Report Scope

Report Features Description Market Value (2024) USD 9.2 Billion Forecast Revenue (2034) USD 13.2 Billion CAGR (2025-2034) 3.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Wax Type (Mineral Wax (Paraffin Wax, Microcrystalline Wax, Ozokerite, Ceresin, Montan Wax, Others), Synthetic Wax (Polyethylene wax, Polypropylene wax, Polyamide, Fatty Acid Amide Waxes, Fischer-Tropsch Waxes, Others), Natural Wax (Beeswax, Soy Wax, Carnauba Wax, Candelilla Wax, Genuine Rice Bran Wax, Laurel Wax, Others)), By Application (Candles, Packaging, Coating and Polishes, Hot-melt Adhesives, Cosmetic and Toiletries, Plastic and Rubber, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Sasol Limited, Sinopec, Royal Dutch Shell PLC, Exxon Mobil Corporation, Petróleo Brasileiro S.A., Kerax Limited, DEUREX AG, NIPPON SEIRO CO. LTD., Numaligarh Refinery Limited, Strahi and Pitsch, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Sasol Limited

- Sinopec

- Royal Dutch Shell PLC

- Exxon Mobil Corporation

- Petróleo Brasileiro S.A.

- Kerax Limited

- DEUREX AG

- NIPPON SEIRO CO. LTD.

- Numaligarh Refinery Limited

- Strahi and Pitsch, Inc.

Our Clients

- 179122

- February 2026