Global Vitamins Market Size, Share, And Industry Analysis Report By Source (Synthetic, Natural), By Type (Vitamin B, Vitamin E, Vitamin D, Vitamin C, Vitamin A, Vitamin K), By Application (Healthcare Products, Food and Beverages, Feed, Personal Care Products), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182902

- Number of Pages: 341

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

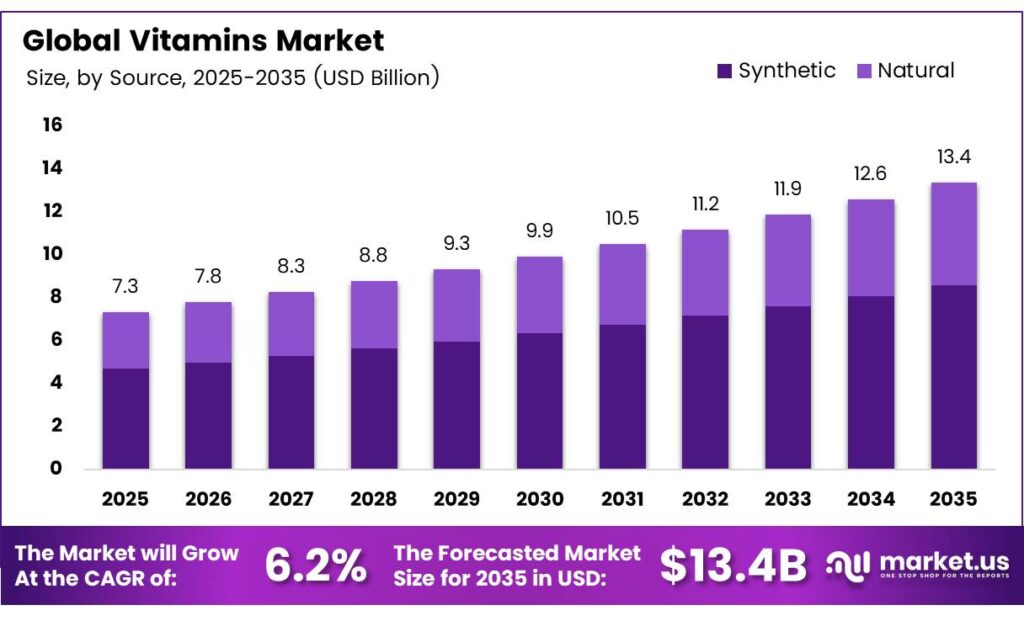

The Global Vitamins Market size is expected to be worth around USD 13.4 billion by 2035 from USD 7.3 billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

The vitamins market covers a wide range of essential micronutrients that support human health, animal nutrition, and food fortification. These include Vitamin C, B complex, A, D, E, and K, available in both synthetic and natural forms. Manufacturers supply these nutrients to healthcare, food and beverage, feed, and personal care industries globally.

Consumer awareness about preventive healthcare drives steady demand for vitamin supplements. Urbanization and rising incomes in developing economies push more households toward daily supplementation routines. Additionally, the growing preference for fortified functional foods and beverages creates new application areas for vitamin producers across multiple end-use sectors.

Global government-reported vitamins trade reached $9.31 billion in 2024, rising 8.29% from $8.60 billion in 2023. This growth reflects accelerating cross-border demand for both pharmaceutical-grade and food-application vitamins, confirming the market’s strong international trade momentum.

Haleon reported an adjusted pre-tax profit of GBP 1.13 billion for H1 2024, with Centrum vitamins delivering double-digit growth inside its vitamins, minerals, and supplements portfolio. This performance signals robust consumer spending on established vitamin brands even amid broader economic pressures.

Personalization technology and genomic-driven supplement design are reshaping product development strategies. Manufacturers increasingly invest in clean-label, plant-derived, and bioavailability-enhanced formulations. Consequently, the vitamins market continues attracting capital from pharmaceutical, food, and wellness sectors, positioning it as one of the fastest-growing segments within the global nutraceuticals industry.

Key Takeaways

- The Global Vitamins Market is valued at USD 7.3 billion in 2025 and is projected to reach USD 13.4 billion by 2035 at a CAGR of 6.2% during the forecast period 2026 to 2035.

- Synthetic vitamins dominate with a 67.2% market share in 2025.

- Vitamin B leads the market with a 34.7% share in 2025.

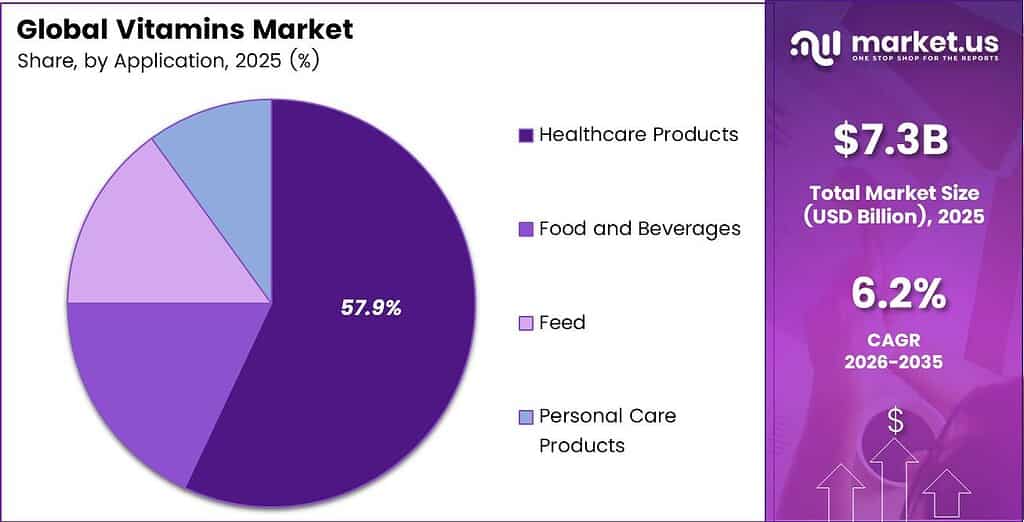

- Healthcare Products holds the largest share at 57.9% in 2025.

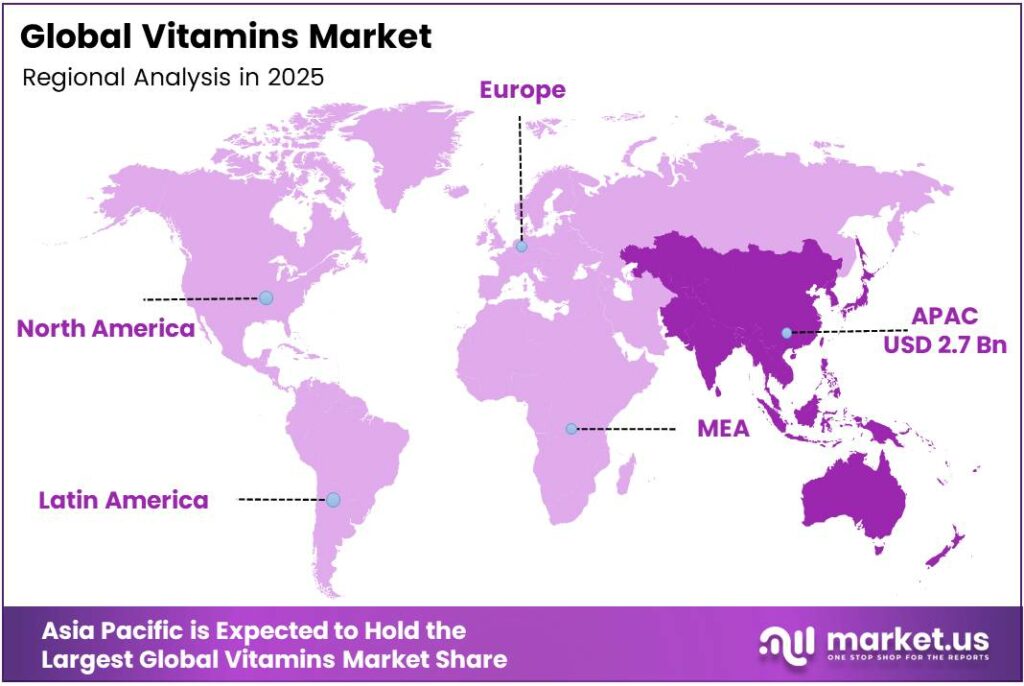

- Asia Pacific dominates the regional landscape with a 37.6% share, valued at USD 2.7 billion.

By Source Analysis

Synthetic dominates with 67.2% due to cost efficiency and large-scale production capability.

In 2025, Synthetic vitamins held a dominant market position in the By Source segment of the Vitamins Market, with a 67.2% share. Synthetic variants offer consistent purity, scalability, and lower production costs compared to natural alternatives. Moreover, their compatibility with pharmaceutical and fortified food manufacturing processes makes them the preferred choice across industrial applications globally.

Natural vitamins represent the growing counterpart, driven by rising consumer preference for clean-label and plant-derived products. Health-conscious buyers increasingly seek supplements free from synthetic additives. However, higher extraction costs and limited raw material availability continue to constrain the natural segment’s ability to challenge synthetic dominance at scale.

By Type Analysis

Vitamin B dominates with 34.7% due to its broad application in energy metabolism and neurological support.

In 2025, Vitamin B held a dominant market position in the By Type segment of the Vitamins Market, with a 34.7% share. The B-complex group supports energy production, red blood cell formation, and cognitive function. Consequently, its wide use across dietary supplements, energy drinks, and fortified foods drives consistent and high-volume demand globally.

Vitamin E maintains strong demand as a powerful antioxidant used in personal care, healthcare, and food preservation applications. Its role in skin health and immune support sustains steady consumer interest. Additionally, Vitamin D has surged in relevance, particularly following pandemic-era awareness of immune and bone health, establishing it as one of the fastest-growing vitamin types in supplement formulations.

Vitamin C remains a market staple, widely used in immunity-support supplements and fortified beverages across all demographic groups. Its affordability and broad consumer familiarity support stable volume demand. Meanwhile, Vitamin A and Vitamin K serve specialized roles in vision health, bone density, and blood coagulation, with growing traction in therapeutic and clinical nutrition segments worldwide.

By Application Analysis

Healthcare Products dominate with 57.9% due to strong supplement adoption for preventive and therapeutic health management.

In 2025, Healthcare Products held a dominant market position in the By Application segment of the Vitamins Market, with a 57.9% share. Dietary supplements, multivitamins, and therapeutic formulations drive this segment. Moreover, rising preventive health awareness and physician-recommended supplementation programs accelerate consumer spending on vitamin-enriched healthcare products globally.

Food and Beverages represent the second-largest application segment, with vitamins integrated across multiple sub-categories. Infant Foods require strict vitamin fortification standards set by global health authorities. Dairy Products, including milk and yogurt, commonly incorporate Vitamins A and D to meet nutritional labeling requirements.

Beverages form a high-growth sub-category, with energy drinks, functional waters, and wellness shots increasingly incorporating Vitamins B, C, and D. Consumer demand for convenient, on-the-go nutrition drives innovation in this space. The Others sub-category captures niche beverage formats and specialty food applications that continue to expand their vitamin content for health-positioned product differentiation.

Key Market Segments

By Source

- Synthetic

- Natural

By Type

- Vitamin B

- Vitamin E

- Vitamin D

- Vitamin C

- Vitamin A

- Vitamin K

By Application

- Healthcare Products

- Food and Beverages

- Infant Foods

- Dairy Products

- Bakery and Confectionery Products

- Beverages

- Others

- Feed

- Personal Care Products

Emerging Trends

Back-to-Basics Wellness Drives Core Vitamin Demand

Consumers increasingly return to foundational vitamins and minerals as core wellness priorities. This back-to-basics movement favors essential nutrients such as Vitamins C, D, and B-complex over complex proprietary blends. Haleon’s H1 2024 power-brand organic revenue increased 5.6%, with Centrum vitamins achieving double-digit growth, confirming mainstream demand for trusted, established vitamin formulations.

Bioavailability Innovation and Personalized Formats Reshape Delivery

Innovative delivery formats, including gummies, liposomal capsules, and effervescent tablets, gain rapid consumer acceptance globally. Manufacturers invest in gut health, immunity, and cellular energy vitamins using advanced absorption technologies. Additionally, biomarker-based personalization and DNA-driven supplement customization enter the mainstream, allowing brands to offer highly tailored vitamin regimens to individual consumers based on genetic and health profile data.

Drivers

Rising Health Consciousness and Aging Populations Accelerate Vitamin Adoption

Global health awareness drives widespread preventive supplementation as consumers seek to address nutrient deficiencies proactively. Simultaneously, rapidly aging populations in North America, Europe, and Asia create strong demand for bone health and age-related wellness vitamins. Vitabiotics’ revenue reached GBP 196.5 million in 2023, reflecting sustained consumer commitment to vitamin supplementation brands.

Urbanization, Rising Incomes, and AI-Powered Personalization Fuel Market Growth

Surging disposable incomes and urbanization in emerging markets accelerate daily vitamin regimen adoption across new consumer demographics. Moreover, breakthrough integration of artificial intelligence, genomics, and wearable devices enables precision-tailored vitamin formulations. These technology-driven tools allow brands to engage consumers with personalized recommendations, strengthening retention and expanding the addressable market across both premium and mass segments.

Restraints

Stringent Regulatory Frameworks Slow Innovation and Market Entry

Global regulatory agencies impose complex compliance requirements on vitamin product development, labeling, and market authorization. These frameworks vary significantly across regions, forcing manufacturers to navigate multiple approval pathways simultaneously. Consequently, product innovation timelines lengthen, and market entry costs rise, particularly for smaller brands seeking to introduce novel formulations or health claims across international markets.

Raw Material Volatility and Supply Chain Disruptions Raise Production Costs

Persistent raw material price volatility creates significant margin pressure for vitamin manufacturers dependent on commodity-priced inputs. Geopolitical tensions and logistics disruptions further compound supply chain instability, raising procurement and operational costs. Therefore, producers struggle to maintain stable pricing for end customers, creating a competitive disadvantage, particularly for companies without vertically integrated supply chain management capabilities.

Growth Factors

Functional Food Integration and E-Commerce Expansion Open New Revenue Channels

Vitamins increasingly integrate into everyday functional foods and beverages, broadening consumer accessibility beyond traditional supplement formats. This fortification trend opens large incremental volume opportunities for ingredient suppliers. China’s government-reported exports of vitamins reached $559.29 million in 2024, with 47.61 million kg shipped, highlighting the enormous scale of global vitamin ingredient supply chains supporting this growth.

Sustainable Formulations and Mental Wellness Vitamins Drive Premium Segment Expansion

Development of sustainable, clean-label, and plant-derived vitamin solutions attracts eco-conscious demographic segments globally. Brands that align with environmental values and transparent sourcing practices command premium pricing and stronger consumer loyalty. Additionally, targeted innovation in mental wellness and cognitive support vitamins addresses high-stress modern lifestyles, creating a fast-growing premium category that commands above-average margins and strong repeat purchase rates.

Regional Analysis

Asia Pacific Dominates the Vitamins Market with a Market Share of 37.6%, Valued at USD 2.7 Billion

Asia Pacific leads the global vitamins market with a 37.6% share valued at USD 2.7 billion in 2025. China dominates regional production and exports, serving as the world’s largest supplier of vitamin ingredients to global markets. Moreover, rising middle-class populations in India, Japan, and Southeast Asia drive accelerating domestic supplement consumption, supporting both import and local production growth across the region.

North America represents a highly mature and innovation-driven vitamins market anchored by strong consumer supplement spending in the United States and Canada. The U.S. remains a leading exporter of pharmaceutical-grade vitamins, with exports to China and Canada among its largest disclosed bilateral trade destinations. Additionally, premium personalized supplement brands and direct-to-consumer e-commerce channels sustain continued revenue expansion across the region.

Europe maintains a significant vitamins market position supported by stringent quality standards and strong regulatory frameworks across member states. Switzerland, the Netherlands, and Germany serve as key manufacturing and re-export hubs for pharmaceutical and specialty-grade vitamin ingredients. Furthermore, growing consumer preference for clean-label, natural-origin supplements drives product reformulation across European food, healthcare, and personal care categories.

The Middle East and Africa region shows increasing vitamin market activity as governments expand public health and nutrition programs targeting micronutrient deficiency. GCC countries lead regional demand, supported by rising health awareness and expanding organized retail channels. However, limited local manufacturing capacity and dependence on imports from Asia and Europe create supply chain vulnerabilities that constrain the market development pace.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Koninklijke DSM NV stands as one of the world’s most recognized vitamin ingredient manufacturers, supplying nutritional solutions across human nutrition, animal feed, and personal care markets. The company invests significantly in sustainable and precision fermentation technologies. Moreover, its broad portfolio spanning Vitamins A, B, C, D, E, and K positions it as a full-spectrum ingredient partner for global food and supplement brands.

Glanbia PLC operates as a leading performance nutrition and ingredient company with a strong vitamins and micronutrient portfolio serving the sports nutrition, healthcare, and functional food sectors. Its vertically integrated business model allows consistent ingredient quality and supply reliability. Additionally, Glanbia leverages its consumer brand capabilities and ingredient science expertise to deliver differentiated vitamin solutions across premium wellness market segments globally.

ADM (Archer-Daniels-Midland) brings deep agricultural sourcing capabilities and global distribution infrastructure to the vitamins ingredient market. The company serves feed, food, and supplement manufacturers across North America, Europe, and the Asia Pacific. Furthermore, ADM’s investments in bioavailability-enhanced and clean-label vitamin solutions align with evolving consumer demands for transparent, science-backed nutritional ingredient sourcing and formulation innovation.

BASF maintains a prominent position as a global vitamins supplier, particularly in the pharmaceutical and food fortification segments. Its manufacturing scale and research capabilities support a comprehensive vitamin product range for both human and animal nutrition markets. Consequently, BASF’s strong regulatory compliance infrastructure and consistent supply chain performance make it a trusted partner for manufacturers requiring high-quality, validated vitamin ingredient supply across international markets.

Top Key Players in the Market

- Koninklijke DSM NV

- Glanbia PLC

- ADM

- BASF

- Lonza Group

- Adisseo

- Vitablend Nederland BV

- Stern Vitamin GmbH

- Farbest-Tallman Foods Corporation

- The Wright Group

- Zhejiang Garden Biochemical High-Tech Co., Ltd

- NewGen Pharma

- Rabar Pty Ltd.

- Resonac

- BTSA BIOTECNOLOGÍAS APLICADAS SL

Recent Developments

- In 2025, DSM-Firmenich opened its NextGen Tonganoxie facility in Kansas (USA), a next-generation, fully automated, pet-only premix plant with 100% automated micro-ingredient additions and full batch traceability. Premixes incorporate vitamins and other functional ingredients for pet nutrition.

- In 2025, Glanbia highlighted innovations in its Health & Nutrition division, emphasizing custom All N premix formulas for immunity, cognition, energy, and other functional applications in supplements and fortified products.

Report Scope

Report Features Description Market Value (2025) USD 7.3 Billion Forecast Revenue (2035) USD 13.4 Billion CAGR (2026-2035) 6.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Synthetic, Natural), By Type (Vitamin B, Vitamin E, Vitamin D, Vitamin C, Vitamin A, Vitamin K), By Application (Healthcare Products, Food and Beverages, Feed, Personal Care Products) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Koninklijke DSM NV, Glanbia PLC, ADM, BASF, Lonza Group, Adisseo, Vitablend Nederland BV, Stern Vitamin GmbH, Farbest-Tallman Foods Corporation, The Wright Group, Zhejiang Garden Biochemical High-Tech Co. Ltd, NewGen Pharma, Rabar Pty Ltd., Resonac, BTSA BIOTECNOLOGÍAS APLICADAS SL Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Koninklijke DSM NV

- Glanbia PLC

- ADM

- BASF

- Lonza Group

- Adisseo

- Vitablend Nederland BV

- Stern Vitamin GmbH

- Farbest-Tallman Foods Corporation

- The Wright Group

- Zhejiang Garden Biochemical High-Tech Co., Ltd

- NewGen Pharma

- Rabar Pty Ltd.

- Resonac

- BTSA BIOTECNOLOGÍAS APLICADAS SL

Our Clients

- 182902

- March 2026