Global Vitamin And Mineral Premixes Market Size, Share, And Industry Analysis Report By Form (Powder/Dry, Liquid), By Product Mode (Vitamin Premixes, Mineral Premixes, Vitamin and Mineral Blends), By Application (Animal Feed, Food and Beverage, Pharmaceutical, Personal Care and Cosmetics), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182246

- Number of Pages: 257

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

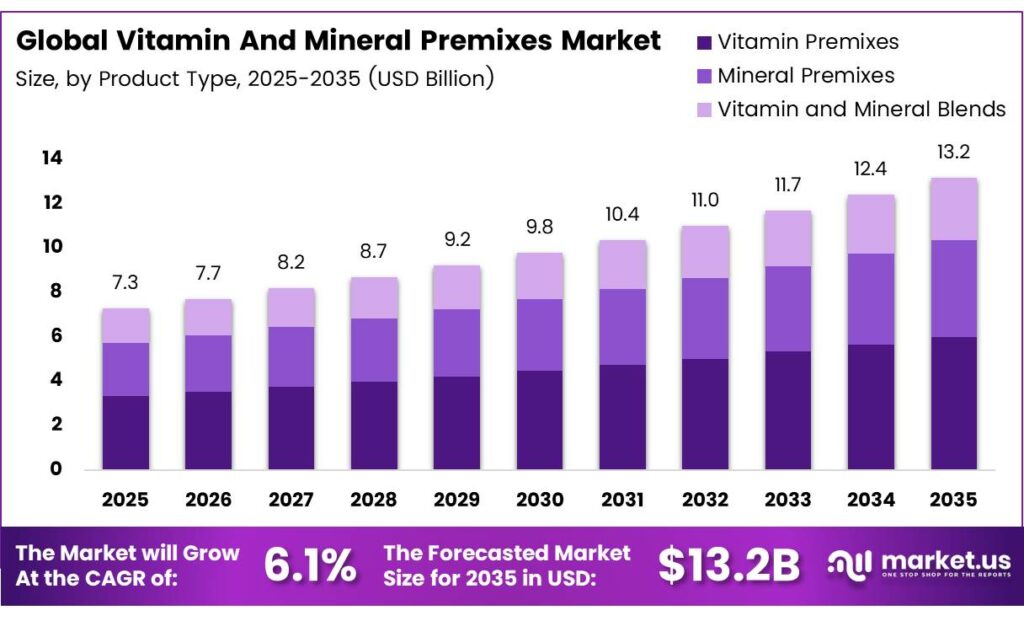

The Global Vitamin and Mineral Premixes Market size is expected to be worth around USD 13.2 billion by 2035 from USD 7.3 billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

The vitamin and mineral premixes market covers customized blends of essential micronutrients used across animal feed, food and beverage, pharmaceutical, and personal care industries. Manufacturers formulate these premixes to meet precise nutritional requirements. They help producers fortify end products efficiently and consistently.

Premixes play a critical role in addressing nutritional deficiencies at scale. Food producers, feed manufacturers, and pharmaceutical companies rely on these solutions to deliver consistent nutrient profiles. Consequently, demand for precision-formulated blends continues to rise across multiple application sectors globally.

ADM’s Animal Nutrition revenue reached $3,405 million in 2024, reflecting the scale of integrated nutrition operations serving premix-dependent sectors. This figure underscores how large-scale nutrition companies anchor the demand chain for vitamin and mineral premix inputs.

Glanbia Group’s revenue reached $3.9 billion in 2025, with Health and Nutrition LFL revenue growth of +6.8%, driven by strong volume growth across premix and flavour solutions businesses. This performance confirms sustained commercial momentum within the global premix industry.

Consumer interest in clean-label nutrition, functional foods, and personalized health products further expands market potential. Producers increasingly seek natural, non-GMO, and organic premix ingredients to align with evolving label standards. Moreover, pharmaceutical-grade premix applications in nutraceuticals and clinical nutrition add another high-value growth dimension.

Key Takeaways

- The Global Vitamin and Mineral Premixes Market is valued at USD 7.3 billion in 2025 and is projected to reach USD 13.2 billion by 2035 at a CAGR of 6.1% during the forecast period 2026 to 2035.

- Powder/Dry dominates with a 76.3% market share in 2025.

- Vitamin Premixes lead with a 34.6% share in 2025.

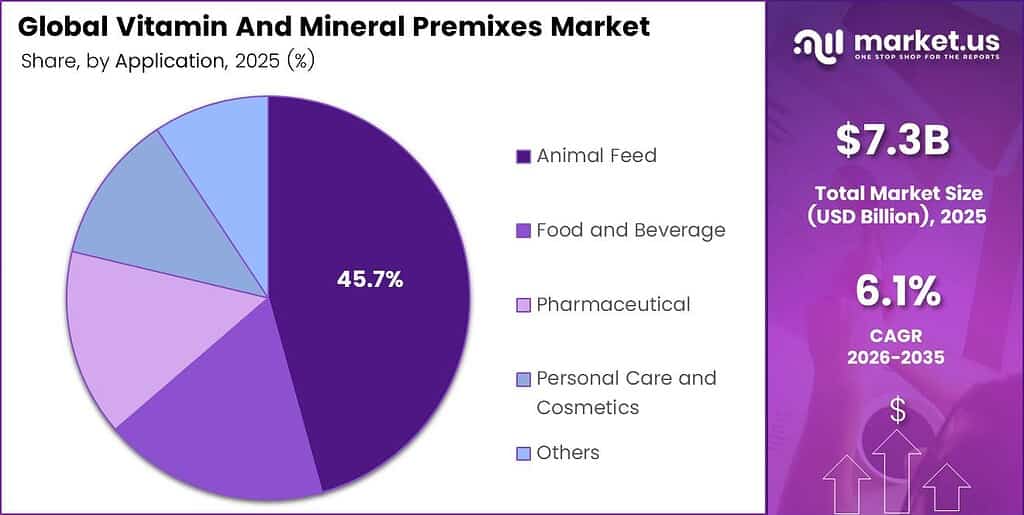

- Animal Feed holds the largest share at 45.7% in 2025.

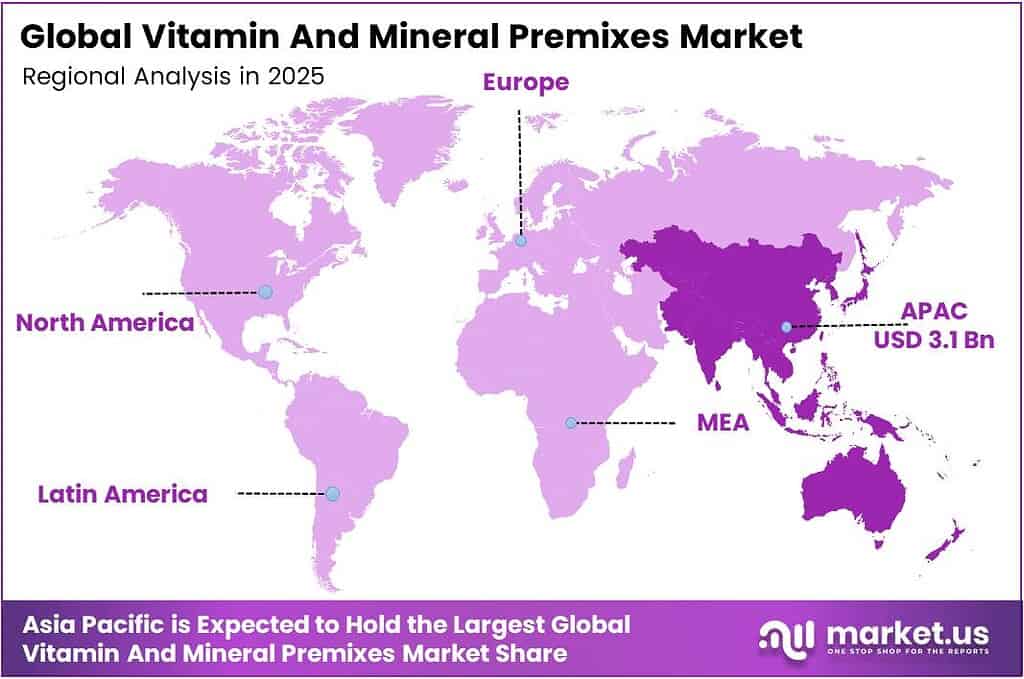

- Asia Pacific dominates the regional landscape with a 42.5% market share, valued at USD 3.1 billion.

By Form Analysis

Powder/Dry dominates with 76.3% due to stability, ease of handling, and widespread compatibility across feed and food applications.

In 2025, Powder/Dry held a dominant market position in the By Form segment of the Vitamin and Mineral Premixes Market, with a 76.3% share. Dry premix formulations offer superior shelf life and nutrient stability under standard storage conditions. Additionally, their ease of blending with solid feed matrices makes them the preferred choice for large-scale animal feed and food fortification operations.

Liquid premixes represent the remaining share of the By Form segment. Liquid formulations gain traction in applications requiring fast solubility and uniform dispersion in water-based systems. However, challenges related to stability, shorter shelf life, and specialized storage requirements moderate their adoption compared to dry alternatives in conventional manufacturing environments.

By Product Mode Analysis

Vitamin Premixes lead with 34.6% due to high demand for essential vitamin blends across animal nutrition and food fortification applications.

In 2025, Vitamin Premixes held a dominant market position in the By Product Mode segment of the Vitamin and Mineral Premixes Market, with a 34.6% share. These formulations deliver concentrated blends of fat-soluble and water-soluble vitamins critical to livestock health and human food enrichment programs. Moreover, regulatory mandates for vitamin fortification in staple foods globally reinforce consistent demand.

Mineral Premixes serve as targeted solutions delivering essential macro and trace minerals to feed and food products. Producers use mineral blends to address specific soil-related nutrient deficiencies in livestock herds. Consequently, demand remains stable across cattle, poultry, and swine production systems worldwide.

Vitamin and Mineral Blends combine both nutrient categories into single, comprehensive formulations. These blended premixes simplify procurement and manufacturing by reducing the number of separate additives required. Therefore, integrated blend formats appeal strongly to mid-size food and feed producers seeking cost and operational efficiency without compromising nutritional completeness.

By Application Analysis

Animal Feed dominates with 45.7% due to large-scale livestock production requirements and mandatory micronutrient supplementation across global feed manufacturing.

In 2025, Animal Feed held a dominant market position in the By Application segment of the Vitamin and Mineral Premixes Market, with a 45.7% share. Livestock producers depend on micronutrient premixes to support animal growth, reproduction, and immune function. Additionally, expanding aquaculture operations worldwide creates incremental demand for species-specific nutrient formulations in this segment.

Food and Beverage applications represent a major growth channel for vitamin and mineral premix producers. Manufacturers incorporate premixes into fortified cereals, dairy products, infant formula, and beverages. Moreover, rising consumer awareness of nutritional health and government food fortification mandates accelerate adoption in processed food categories across both developed and emerging markets.

Pharmaceutical applications utilize high-purity, tightly controlled premix formulations for nutraceuticals and clinical nutrition products. Producers in this segment demand pharmaceutical-grade micronutrient standards for regulatory compliance. Therefore, specialized premix manufacturers invest in advanced quality control systems to serve pharmaceutical clients with consistent, documentation-ready ingredients.

Key Market Segments

By Form

- Powder/Dry

- Liquid

By Product Mode

- Vitamin Premixes

- Mineral Premixes

- Vitamin and Mineral Blends

By Application

- Animal Feed

- Food and Beverage

- Pharmaceutical

- Personal Care and Cosmetics

- Others

Emerging Trends

Blockchain and Digital Tools Reshape Premix Supply Chain Transparency

Premix producers increasingly adopt blockchain technology to track ingredient origins and verify nutrient compliance across complex supply chains. This shift responds to buyer demand for traceability and regulatory accountability. Vilomix reported a turnover of EUR 590 million and total tonnage growth of 13%, reflecting how operationally advanced producers gain competitive scale through technology-driven efficiency.

Liquid Formulations and Botanical Ingredients Gain Market Momentum

Manufacturers accelerate the development of water-soluble and liquid premix formats to address ease-of-application demands in aquaculture and liquid feed systems. Additionally, formulators integrate phytonutrients and botanical extracts to meet clean-label consumer expectations. Artificial intelligence tools further enable precision formulation, allowing producers to optimize nutrient dosages with greater accuracy and reduced raw material waste.

Drivers

Animal Feed Fortification and Food Regulatory Mandates Fuel Demand Growth

Livestock producers require consistent micronutrient supplementation to sustain productivity, reduce mortality, and improve feed conversion ratios. India has approximately 232 active premix manufacturers with an annual production capacity of around 75 LMT per annum as of June 2024, illustrating how policy-driven fortification programs build industrial-scale premix infrastructure in emerging economies.

Aquaculture Expansion and Clean-Label Nutrition Preferences Broaden Market Scope

Global aquaculture output growth drives rising demand for specialized nutrient blends designed for fish and shrimp species. Glanbia Health and Nutrition LFL revenue grew +6.8% in 2025, supported by strong volume performance in premix businesses. Moreover, consumer preference for natural and non-GMO nutritional additives pushes producers to develop cleaner, traceable premix ingredient systems.

Restraints

Raw Material Price Volatility Pressures Premix Production Economics

Vitamin and mineral premix producers face persistent margin pressure from fluctuating raw material costs. Key vitamin inputs such as vitamin A, E, and B-complex compounds experience significant price swings tied to energy costs and upstream synthesis capacity. Consequently, manufacturers find it difficult to maintain stable pricing for customers under long-term supply contracts without absorbing cost increases.

Mixing Uniformity and Nutrient Stability Challenges Limit Product Consistency

Achieving uniform dispersion of micronutrients across large batches remains a technical challenge for premix manufacturers. Heat-sensitive vitamins and hygroscopic minerals degrade during processing if temperature and moisture controls are inadequate. Therefore, producers must invest in advanced blending equipment and controlled storage infrastructure, raising capital requirements and operational complexity for smaller market participants.

Growth Factors

Personalized Nutrition and Encapsulation Technologies Open Premium Market Segments

EU compound feed production — which incorporates vitamin and mineral premixes — is forecast at 147.5 million tonnes in 2025, a 0.4% increase from 2024. This stable volume base creates consistent premix demand across European feed markets. Additionally, encapsulation technologies that protect sensitive nutrients from degradation unlock premium pricing opportunities in both human and animal nutrition segments.

Emerging Economy Expansion and Organic Product Lines Drive Long-Term Revenue

Premix producers strategically expand operations into underserved agricultural markets across Southeast Asia, Africa, and Latin America to capture early-mover advantages. These regions show rising livestock productivity ambitions and growing food processing sectors. Furthermore, the launch of certified organic and non-GMO premix product lines serves health-conscious consumer markets willing to pay premium prices for clean nutritional solutions.

Regional Analysis

Asia Pacific Dominates the Vitamin and Mineral Premixes Market with a Market Share of 42.5%, Valued at USD 3.1 Billion

Asia Pacific leads the global vitamin and mineral premixes market, holding a 42.5% share valued at USD 3.1 billion in 2025. China, India, and Southeast Asian nations drive this dominance through large-scale animal feed production, growing food fortification mandates, and rapidly expanding aquaculture sectors. Moreover, government nutrition programs across the region sustain robust institutional demand for premix ingredients year-round.

North America represents a mature and high-value market for vitamin and mineral premix solutions. The United States drives demand through advanced livestock operations, fortified food manufacturing, and pharmaceutical-grade nutraceutical production. Additionally, clean-label and functional food trends push domestic premix producers to develop specialized, differentiated formulations targeting premium consumer segments.

Europe maintains strong premix demand driven by regulatory-compliant animal feed manufacturing and food fortification standards across member states. EU feed production volumes sustain consistent premix procurement across poultry, pig, and cattle sectors. However, stricter environmental and ingredient transparency regulations require producers to continually invest in compliant, traceable sourcing systems throughout the supply chain.

Latin America presents growing market potential as Brazil and Mexico expand their livestock, poultry, and aquaculture industries. Rising domestic protein consumption and export-oriented meat production accelerate demand for performance-enhancing feed premixes. Consequently, international premix manufacturers actively target the region through local partnerships, distribution agreements, and tailored product formulations suited to regional feed standards.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

NAGASE and CO., LTD. operates as a diversified specialty chemicals and life sciences group with a strong presence in nutritional ingredients and premix distribution. The company’s Prinova Group subsidiary plays a central role in delivering vitamin and mineral premix solutions across global markets. NAGASE leverages its integrated trading and manufacturing capabilities to serve the food, feed, and pharmaceutical nutrition sectors with reliable supply consistency.

Archer Daniels Midland Company (ADM) ranks among the world’s largest integrated nutrition and agricultural processing companies. ADM’s nutrition segment spans human and animal nutrition, operating extensive processing capacity across North America, Asia-Pacific, Europe, and South America. The company’s scale and vertical integration position it as a key supplier of custom premix solutions for feed manufacturers, food producers, and specialty nutrition customers globally.

Nutreco operates as a global leader in animal nutrition and aquafeed, providing science-based premix solutions for livestock and aquaculture producers worldwide. The company focuses on improving feed efficiency, animal health, and sustainability outcomes through precision nutrition research. Nutreco’s strong research and development capabilities enable continuous formulation innovation tailored to the evolving productivity requirements of modern livestock and fish farming systems.

DSM-Firmenich combines deep expertise in vitamins, carotenoids, and nutritional science with a broad portfolio of premix solutions for animal and human nutrition. The company supplies customized micronutrient blends to food manufacturers, feed producers, and pharmaceutical companies across more than 50 countries. DSM-Firmenich’s investment in encapsulation technology and bioavailability science strengthens its differentiation within the premium premix ingredient segment.

Top Key Players in the Market

- NAGASE and CO., LTD.

- Archer Daniels Midland Company (ADM)

- Nutreco

- dsm-firmenich

- Glanbia PLC

- Corbion

- SternVitamin GmbH and Co. KG

- Barentz

- FENCHEM

- AMINO GmbH

Recent Developments

- In 2025, NAGASE maintains active capabilities in nutrient premixes through its Life & Healthcare Products Department, including processing, OEM, and ODM manufacturing of nutritional products (with vitamins and related ingredients) across facilities in the U.S., U.K., and China. It positions itself as one of the world’s largest distributors of nutritional ingredients, including vitamins and amino acids.

- In September 2025, ADM announced a joint venture with Alltech to create a North American animal feed business. The JV will combine expertise in specialty ingredients, premix, and supplements; ADM’s U.S. premix and additive businesses will supply the new entity, while certain Canadian operations remain with ADM.

Report Scope

Report Features Description Market Value (2025) USD 7.3 Billion Forecast Revenue (2035) USD 13.2 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Powder/Dry, Liquid), By Product Mode (Vitamin Premixes, Mineral Premixes, Vitamin and Mineral Blends), By Application (Animal Feed, Food and Beverage, Pharmaceutical, Personal Care and Cosmetics, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape NAGASE and CO., LTD., Archer Daniels Midland Company (ADM), Nutreco, dsm-firmenich, Glanbia PLC, Corbion, SternVitamin GmbH and Co. KG, Barentz, FENCHEM, AMINO GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Vitamin and Mineral Premixes MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Vitamin and Mineral Premixes MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- NAGASE and CO., LTD.

- Archer Daniels Midland Company (ADM)

- Nutreco

- dsm-firmenich

- Glanbia PLC

- Corbion

- SternVitamin GmbH and Co. KG

- Barentz

- FENCHEM

- AMINO GmbH

Our Clients

- 182246

- March 2026