Global Viscosity Index Improvers Market Size, Share, And Industry Analysis Report By Product (Polymethacrylate (PMA), Ethylene Propylene Copolymer (OCP), Hydrogenated Styrene Diene Copolymer (HSD), Polyisobutylene (PIB), Others), By Application (Engine Oils, Transmission Fluids, Hydraulic Fluids, Gear Oils, Electric Vehicle (EV) Fluids, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179475

- Number of Pages: 209

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

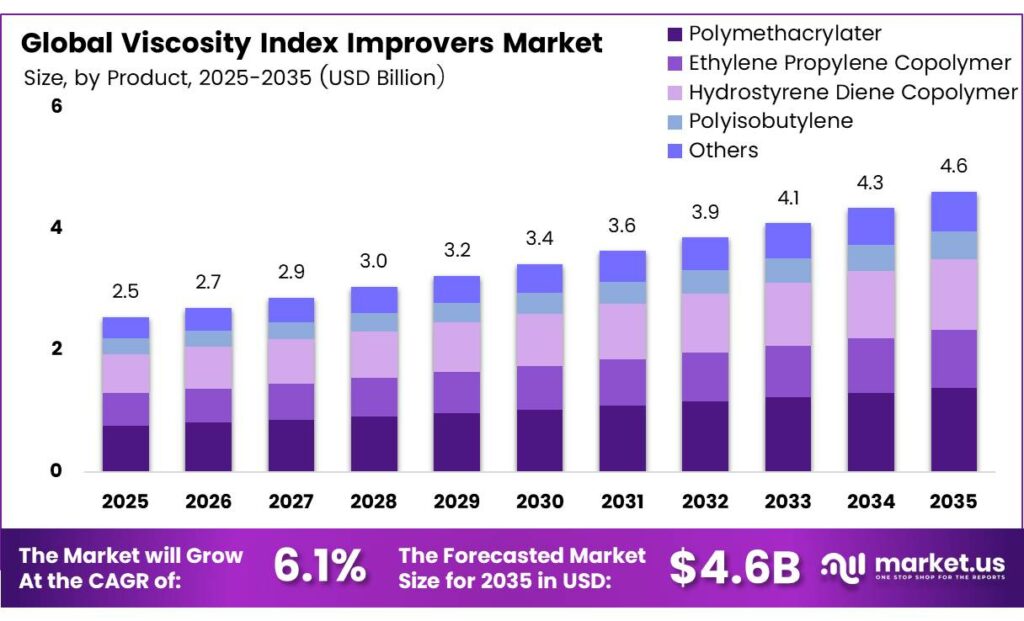

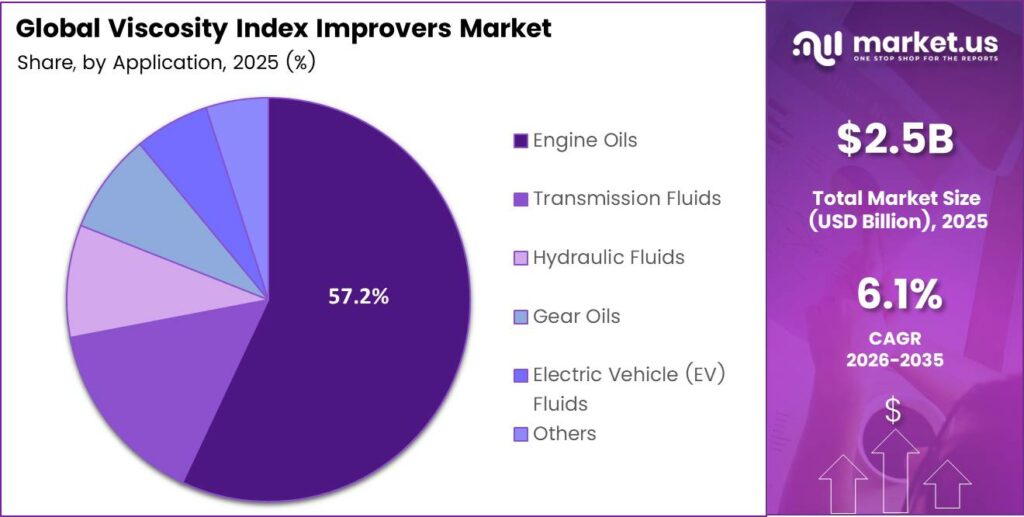

The Global Viscosity Index Improvers Market size is expected to be worth around USD 4.6 billion by 2035 from USD 2.5 billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

Viscosity index improvers (VII) are polymer-based chemical additives that help lubricants maintain consistent viscosity across temperature ranges. These additives prevent oils from becoming too thin at high temperatures or too thick in cold conditions. They serve a critical role in modern engine oils, transmission fluids, and hydraulic systems.

The market covers several polymer chemistries, including polymethacrylates, ethylene propylene copolymers, and polyisobutylene. Formulators add these materials in small concentrations to achieve thermally stable lubricant performance. Consequently, demand spans automotive, industrial, and commercial fleet applications globally.

- Lubrizol India Private Ltd reported revenue of 1,719 crore Indian rupees in FY2023–24 from its lubricant additive and viscosity index improver operations. This figure reflects India’s importance as both a blending base and a production hub for global viscosity modifier supply chains. The year-on-year growth of 10.8% from 1,552 crore rupees underscores rising domestic and export demand.

- Evonik Industries’ specialty Additives division generated sales of 3,578 million euros in 2024 with adjusted EBITDA of 744 million euros. This division houses the oil additives business, including polymeric viscosity index improvers serving lubricants, transportation fluids, and industrial oils. Such scale confirms strong corporate investment in this specialty chemical segment.

Industrial machinery operators also push demand for thermally stable lubrication solutions. Manufacturing plants, construction equipment, and power generation units require lubricants that perform reliably under variable load and temperature conditions. Moreover, growth in emerging markets accelerates fleet expansion and industrial investment, further boosting consumption.

Key Takeaways

- The Global Viscosity Index Improvers Market is valued at USD 2.5 billion in 2025 and is projected to reach USD 4.6 billion by 2035, at a CAGR of 6.1% during the forecast period 2026–2035.

- Polymethacrylate (PMA) dominates with a 37.1% market share in 2025.

- Engine Oils lead with a 57.2% share, reflecting high demand in automotive lubrication.

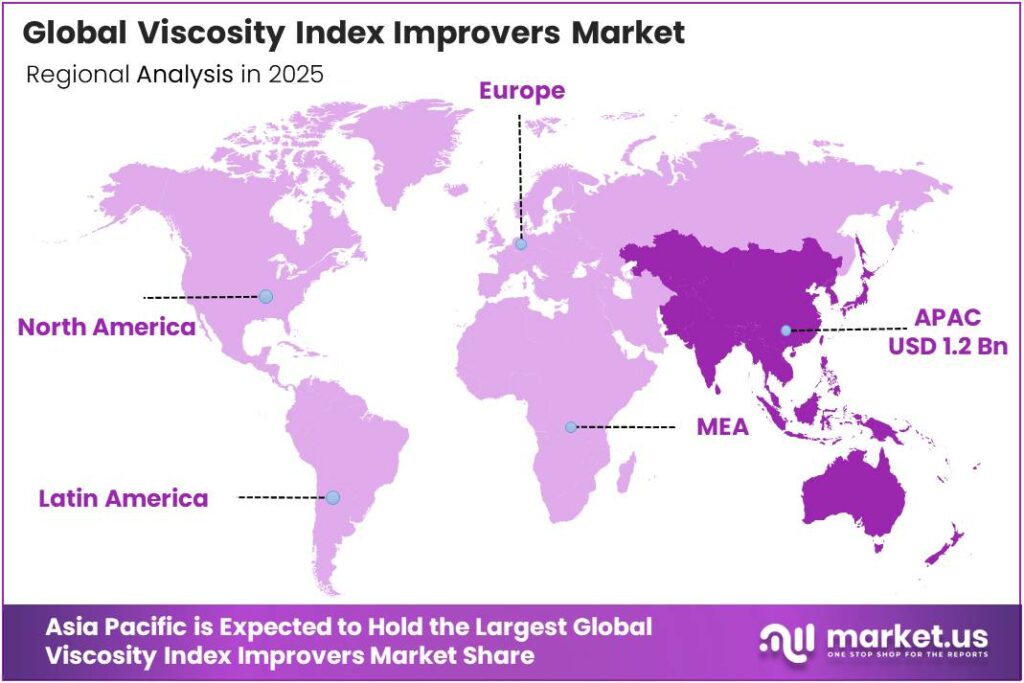

- Asia Pacific dominates the regional landscape with a 46.7% share, valued at USD 1.2 billion.

By Product Analysis

Polymethacrylate (PMA) dominates with 37.1% due to superior thermal stability and versatility across lubricant applications.

In 2025, Polymethacrylate (PMA) held a dominant market position in the By Product segment of the Viscosity Index Improvers Market, with a 37.1% share. PMA offers excellent shear stability and low-temperature performance. Consequently, lubricant blenders widely prefer PMA for premium engine oils and transmission fluids across passenger and commercial vehicles.

Ethylene Propylene Copolymer (OCP) represents the second-largest product segment and delivers strong shear stability at a competitive cost. OCP finds extensive use in high-viscosity lubricants for heavy-duty engines and industrial gear oils. Moreover, its compatibility with both mineral and synthetic base oils makes it a preferred choice among large-volume formulators.

Hydrogenated Styrene Diene Copolymer (HSD) serves niche but growing applications requiring high shear-stable performance. HSD products offer excellent low-temperature fluidity combined with robust thermal resistance. Additionally, their compact molecular architecture supports next-generation long-drain-interval lubricant formulations increasingly demanded by automotive OEMs.

Polyisobutylene (PIB) and Others collectively address specialty applications, including two-stroke engine oils, marine lubricants, and certain hydraulic fluid grades. PIB delivers film-forming properties that reduce wear in gear and hydraulic systems. Therefore, these segments maintain stable demand within industrial and specialized transportation lubrication markets.

By Application Analysis

Engine oils dominate with 57.2% due to widespread automotive demand and strict OEM viscosity grade requirements.

In 2025, Engine Oils held a dominant market position in the By Application segment of the Viscosity Index Improvers Market, with a 57.2% share. Automotive engines require precise viscosity control across temperature extremes. Therefore, engine oil formulators consistently add high concentrations of viscosity modifiers to meet ILSAC, ACEA, and API performance standards.

Transmission Fluids form the second-largest application segment and demand highly shear-stable viscosity improvers. Modern automatic and dual-clutch transmissions operate under extreme pressure and thermal stress. Consequently, transmission fluid formulators specify polymers that maintain film strength and prevent viscosity breakdown throughout extended drain intervals.

Hydraulic Fluids require viscosity modifiers that perform consistently across wide operating temperature ranges. Industrial and mobile hydraulic systems rely on thermally stable fluids to protect pumps and valves. Additionally, manufacturers prioritize additives with low tendency to thicken in cold startup conditions to ensure reliable equipment operation.

Gear Oils, Electric Vehicle (EV) Fluids, and Others represent the fastest-evolving application categories. EV thermal management fluids demand low-viscosity, low-friction solutions compatible with electric drivetrains. Moreover, this segment drives innovation in polymer chemistry as automakers transition to electrified powertrains requiring purpose-built lubrication chemistries.

Key Market Segments

By Product

- Polymethacrylate (PMA)

- Ethylene Propylene Copolymer (OCP)

- Hydrogenated Styrene Diene Copolymer (HSD)

- Polyisobutylene (PIB)

- Others

By Application

- Engine Oils

- Transmission Fluids

- Hydraulic Fluids

- Gear Oils

- Electric Vehicle (EV) Fluids

- Others

Emerging Trends

Multifunctional and Technology-Driven Innovation Reshapes the Viscosity Index Improvers Market

Lubricant formulators increasingly shift toward multifunctional viscosity modifiers that combine shear stability with additional performance attributes. These advanced polymers reduce the need for separate additive packages, lowering formulation costs. Moreover, according to BASF, the company generated 65.3 billion euros of sales in 2024, underscoring the scale of investment global chemical leaders commit to specialty additives, including viscosity modifier technologies.

Olefin copolymers gain traction in premium-grade lubricant blending due to their strong compatibility with synthetic base stocks. Formulators use these materials to meet tightening OEM viscosity grade requirements. Additionally, nanotechnology integration enhances viscosity retention performance, with nano-additives demonstrating improved film strength at elevated temperatures and extended shear stability under high mechanical stress conditions.

Long-drain-interval engine oils drive rapid adoption of innovative additive technologies across passenger and commercial vehicle segments. Automakers demand lubricant solutions that maintain viscosity-grade compliance for 15,000 to 20,000 kilometers between changes. Consequently, additive developers invest heavily in polymer architectures that resist degradation and deliver consistent performance throughout extended service life periods.

Drivers

Increasing Demand for High-Performance Lubricants and Fleet Growth Drive Viscosity Index Improvers Market Expansion

Modern automotive engines operate at higher pressures and temperatures than previous generations, demanding thermally stable lubrication. Automakers specify low-viscosity multigrade oils to meet fuel efficiency and emissions targets. France exported additives for lubricating oils under HS 381121 worth 2,232,991 thousand US dollars in 2024, reflecting the massive global trade volume these performance additives command.

Industrial machinery sectors also accelerate demand for viscosity-enhancing additives. Manufacturing plants, mining operations, and construction equipment fleets require lubricants that sustain performance under variable load and temperature conditions. Moreover, the rapid expansion of commercial transportation fleets in developing economies increases the consumption of engine oils and transmission fluids formulated with high-performance viscosity improvers.

Rising adoption of synthetic and semi-synthetic lubricants across automotive and industrial sectors further boosts market growth. Synthetic base oils require carefully matched polymer additives to achieve target viscosity-temperature profiles. Therefore, lubricant blenders increase procurement of specialized viscosity index improvers that deliver consistent performance in both mineral and fully synthetic oil formulations.

Restraints

Raw Material Price Volatility and Environmental Regulations Challenge Viscosity Index Improvers Market Growth

Petroleum-based raw materials form the primary feedstock for most viscosity index improver polymers. Fluctuating crude oil and petrochemical prices directly impact production economics and profit margins across the supply chain. Consequently, manufacturers find it difficult to maintain stable pricing during commodity price cycles, creating uncertainty for both suppliers and lubricant blenders who plan annual procurement budgets.

Stringent environmental regulations in Europe, North America, and parts of the Asia Pacific limit the use of certain polymer-based additives in lubricant formulations. Regulatory bodies impose restrictions on specific chemical structures associated with environmental persistence or aquatic toxicity. Therefore, producers must invest in reformulation and compliance testing, adding cost and delaying product commercialization timelines for next-generation viscosity modifier packages.

Small and mid-sized lubricant blenders face particular challenges in adapting to regulatory changes, given limited R&D budgets. Compliance requires both technical reformulation and regulatory documentation across multiple jurisdictions. Moreover, divergent regional standards create complexity for global suppliers who must maintain multiple product variants to serve different markets without compromising on performance specifications required by automotive and industrial end users.

Growth Factors

Polymer Chemistry Advancements and Electric Vehicle Penetration Accelerate Viscosity Index Improvers Market Opportunities

Advances in polymer chemistry enable next-generation viscosity index improver formulations with superior performance profiles. Researchers develop star-polymer and comb-polymer architectures that deliver enhanced shear stability and improved low-temperature flow. Mitsui Chemicals’ mobility Solutions business generated 555.1 billion yen of 1,809.2 billion yen total sales in FY2024, confirming substantial corporate investment in mobility-related polymer materials, including viscosity modifier intermediates.

Electric vehicle adoption creates new demand for purpose-built low-viscosity fluids designed for electric drivetrains and thermal management systems. EV manufacturers require lubricants that minimize parasitic energy losses while protecting gearboxes and power electronics from heat. Consequently, additive developers pursue new polymer chemistries compatible with e-fluids, opening a fast-growing application segment distinct from conventional combustion engine lubricants.

Bio-based lubricant additive development supports sustainability goals and addresses tightening environmental regulations. Renewable feedstock-derived viscosity improvers offer reduced carbon footprint and improved biodegradability. Additionally, increasing fuel efficiency requirements in high-mobility emerging markets such as India, Southeast Asia, and Latin America drive broader adoption of premium lubricant grades that rely on advanced viscosity-enhancing additive technologies.

Regional Analysis

Asia Pacific Dominates the Viscosity Index Improvers Market with a Market Share of 46.7%, Valued at USD 1.2 Billion

Asia Pacific leads the global Viscosity Index Improvers Market with a 46.7% share, valued at USD 1.2 billion in 2025. China, India, Japan, and South Korea drive regional demand through large automotive production volumes and expanding industrial machinery sectors. Moreover, rapid fleet growth and rising synthetic lubricant adoption across Southeast Asian markets continue to strengthen the region’s dominant position through the forecast period.

North America represents a mature but innovation-driven market for viscosity index improvers. The United States leads regional demand, supported by large commercial vehicle fleets and stringent API and ILSAC lubricant performance standards. Additionally, domestic chemical producers maintain strong export positions, with the US shipping of lubricant additives under HS 381121 in 2024, ranking it among the world’s top exporters.

Europe sustains a strong demand for advanced viscosity modifiers driven by high automotive engineering standards and strict ACEA specifications. Germany, France, and Italy anchor the regional market as major lubricant additive producers and consumers. France ranked as the world’s largest exporter of HS 381121 lubricant additives in 2024, reflecting a deep European production base that serves both intra-regional and global markets.

Latin America presents growing opportunities for viscosity index improver suppliers as automotive fleet expansion continues in Brazil and Mexico. Rising industrial activity and growing demand for passenger vehicles drive lubricant consumption across the region. However, economic volatility and import dependency for specialty chemicals create supply chain risks that suppliers must manage through regional distribution partnerships and strategic inventory positioning.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE operates as one of the world’s largest chemical suppliers and plays a central role in the viscosity index improvers market through its lubricant additive intermediates portfolio. Petrochemical feedstocks that feed into polymeric viscosity modifier production. BASF’s scale and R&D investment position it as a leading supplier to global lubricant formulators.

Chevron Oronite Company LLC specializes in developing and manufacturing lubricants and fuel additives, including viscosity index improvers for automotive and industrial applications. The company leverages deep formulation expertise and a global supply network to serve major lubricant blenders across North America, Europe, and the Asia Pacific. Its product portfolio addresses engine oils, transmission fluids, and gear oils where thermally stable viscosity performance is critical.

Evonik Industries AG maintains a strong position in the viscosity index improvers segment through its Specialty Additives division. The division supplies polymeric viscosity modifiers under established brand platforms serving automotive and industrial lubricant markets worldwide. Evonik’s continued investment in polymer chemistry research supports the development of next-generation shear-stable and multifunctional viscosity modifier products.

Afton Chemical Corporation delivers a comprehensive range of lubricant additive packages, including viscosity index improvers, designed to meet evolving OEM and industry performance standards. The company invests in application development centers that help formulators optimize additive treat rates and achieve compliance with ILSAC, API, and ACEA specifications. Afton’s technical collaboration model with lubricant blenders strengthens long-term customer relationships across multiple end-use markets.

Top Key Players in the Market

- BASF SE

- Chevron Oronite Company LLC

- Evonik Industries AG

- Afton Chemical Corporation

- The Lubrizol Corporation

- Sanyo Chemical Industries

- Mitsui Chemicals, Inc.

- Petronas

- Sika AG

Recent Developments

- In 2025, BASF introduced IRGAFLO 1050 V, a new shear-stable polyalkyl methacrylate (PMA)-based VII for automotive and heavy-duty gear oils, transmission fluids, and electric drivetrain fluids. It offers excellent low-temperature flow, superior shear stability, high flash point, oxidative and thermal stability, and thermal conductivity.

- In 2025, Chevron Oronite announced the final investment decision to expand its lubricant additive manufacturing facility in Ningbo, China (Ningbo Economic & Technical Development Zone). Construction began in July 2024 with completion targeted for late 2026. The expansion enhances supply flexibility and security for select additive products (including PARATONE VIIs) for China, Asia, and global markets, leveraging proximity to customers and raw materials.

Report Scope

Report Features Description Market Value (2025) USD 2.5 Billion Forecast Revenue (2035) USD 4.6 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Polymethacrylate (PMA), Ethylene Propylene Copolymer (OCP), Hydrogenated Styrene Diene Copolymer (HSD), Polyisobutylene (PIB), Others), By Application (Engine Oils, Transmission Fluids, Hydraulic Fluids, Gear Oils, Electric Vehicle (EV) Fluids, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, Chevron Oronite Company LLC, Evonik Industries AG, Afton Chemical Corporation, The Lubrizol Corporation, Sanyo Chemical Industries, Mitsui Chemicals Inc., Petronas, Sika AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Viscosity Index Improvers MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Viscosity Index Improvers MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Chevron Oronite Company LLC

- Evonik Industries AG

- Afton Chemical Corporation

- The Lubrizol Corporation

- Sanyo Chemical Industries

- Mitsui Chemicals, Inc.

- Petronas

- Sika AG

Our Clients

- 179475

- February 2026