Global Vibration Sensor Market Size, Share, Growth Analysis By Product Type (Accelerometers, Velocity Sensor, Displacement Sensor, Others), By Technology (Piezoresistive, Strain Gauge, Variable Capacitance, Hand Probe, Optical Sensor, Tri-Axial Sensors, Others), By Material (Doped Silicon, Piezoelectric Ceramics, Quartz), By End Use Industry (Automotive & Transportation, Aerospace, Pulp and Paper, Food and Beverage, Oil and Gas Refining Petrochemicals, Power Generation, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181173

- Number of Pages: 218

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

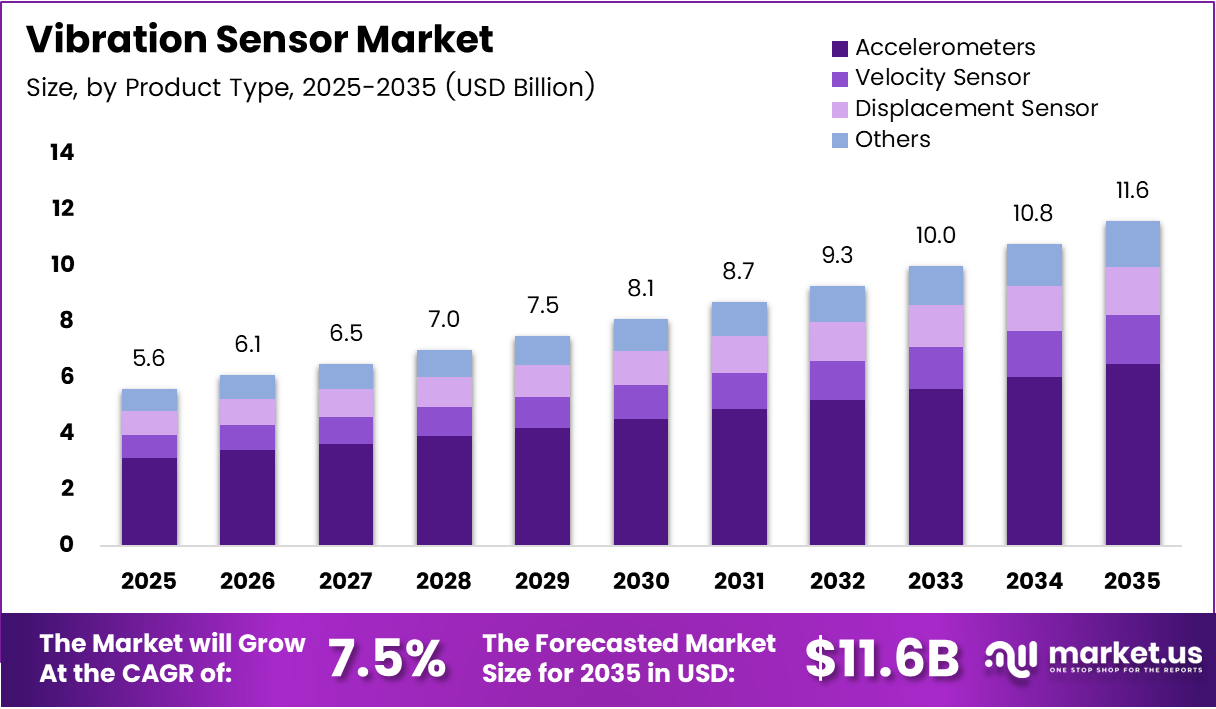

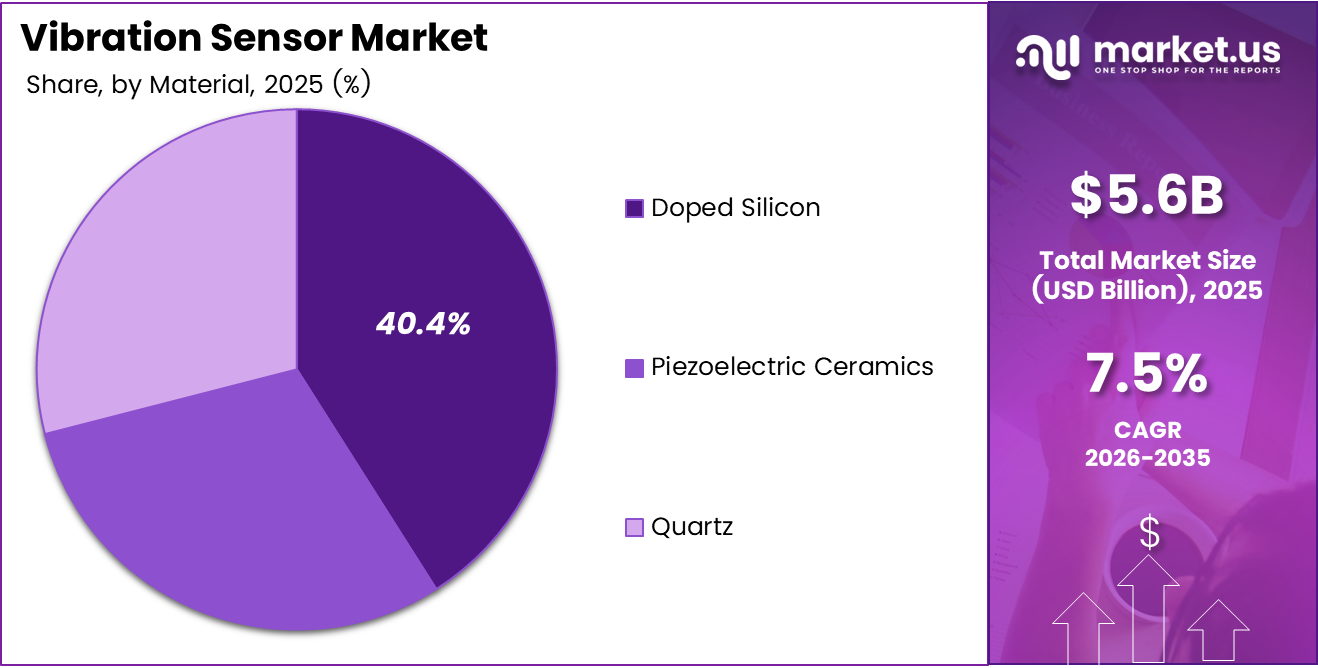

Global Vibration Sensor Market size is expected to be worth around USD 11.6 Billion by 2035 from USD 5.6 Billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035.

Vibration sensors detect mechanical oscillations in rotating and stationary equipment, converting physical motion into measurable electrical signals. These devices serve as the diagnostic backbone for industrial condition monitoring, enabling facilities to track equipment health without halting operations. Their application spans motors, turbines, compressors, and structural assets across heavy industry.

The market’s expansion reflects a structural shift in how industrial operators manage asset performance. Manufacturers, energy producers, and transportation operators now treat vibration data as a core operational input — not an optional diagnostic tool. This shift moves procurement decisions up the value chain, from maintenance teams to operations and engineering leadership.

Automotive and transportation end users represent 30.2% of total demand, reflecting how vehicle safety systems and powertrain diagnostics have embedded vibration monitoring at the hardware level. This concentration signals that automotive OEMs now treat sensor integration as a standard design requirement, not an aftermarket option.

Accelerometers command 55.4% of the product type segment, driven by their precision-to-cost ratio in high-frequency monitoring applications. This dominance locks in a clear technology preference among industrial buyers, narrowing the competitive window for alternative sensor types.

Doped silicon leads material selection at 40.4%, while piezoresistive technology holds 31.2% of the technology segment. These figures confirm that established material science and manufacturing scale continue to set the baseline for mass-market vibration sensor deployment.

Strategic consolidation is accelerating. In September 2024, Spectris plc announced the acquisition of Piezocryst Advanced Sensorics GmbH for €133.5 million, directly targeting piezoelectric vibration and pressure sensor capabilities. This signals that specialized sensing IP is now a premium acquisition target across the industrial technology sector.

According to AssetWatch, vibration analysis improved Mean Time Between Failures from 500 to 2,500 hours — a 5x increase — by eliminating unplanned bearing failures. This outcome quantifies the direct ROI of vibration monitoring for asset-intensive operators, making budget justification substantially easier for new deployments.

According to AssetWatch, vibration analysis saved $1.6 million annually by preventing unplanned bearing failures at a single facility. This figure reframes the sensor as a financial instrument, not just a technical tool — and strengthens the case for enterprise-wide rollouts in manufacturing and power generation environments.

Key Takeaways

- The Global Vibration Sensor Market was valued at USD 5.6 Billion in 2025 and is forecast to reach USD 11.6 Billion by 2035.

- The market advances at a CAGR of 7.5% from 2026 to 2035.

- By Product Type, Accelerometers dominate with a 55.4% share due to their precision and cost efficiency in high-frequency monitoring.

- By Technology, Piezoresistive sensors lead with 31.2% share, driven by their reliability in industrial and automotive applications.

- By Material, Doped Silicon holds the largest share at 40.4%, supported by established semiconductor manufacturing scale.

- By End Use Industry, Automotive and Transportation leads with 30.2% share, reflecting embedded sensor requirements in vehicle safety systems.

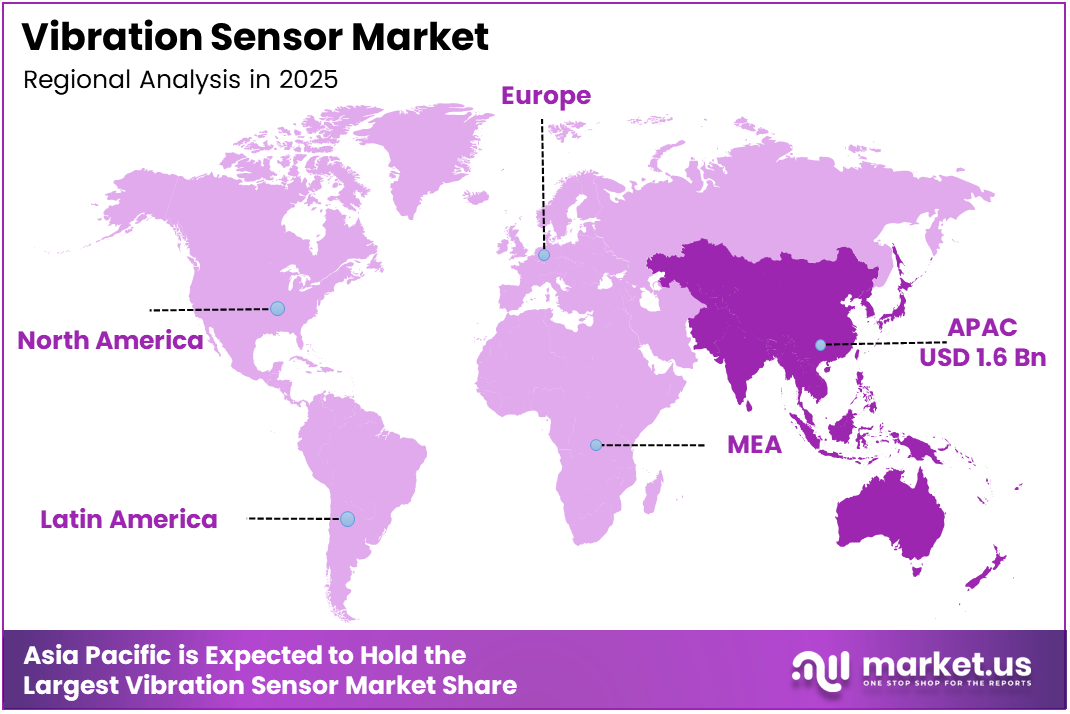

- Asia Pacific dominates the regional landscape with a 28.9% share, valued at USD 1.6 Billion.

Product Type Analysis

Accelerometers dominate with 55.4% due to precision-to-cost ratio in high-frequency applications.

In 2025, Accelerometers held a dominant market position in the By Product Type segment of the Vibration Sensor Market, with a 55.4% share. Their ability to measure high-frequency vibrations across multiple axes makes them the preferred choice for rotating machinery diagnostics in manufacturing, power generation, and aerospace. This concentration reflects a well-established buyer preference that competing sensor formats must overcome with clear differentiation.

Velocity Sensors serve as the primary tool for mid-frequency vibration measurement in industrial machinery, particularly where displacement amplitude matters alongside frequency. They fill a measurement gap between accelerometers and displacement sensors, making them a supporting rather than a competing technology in complex monitoring configurations.

Displacement Sensors carry the highest precision requirement within the product type segment, targeting slow-speed rotating machinery such as large turbines and shaft monitoring systems. Their use cases demand tighter installation tolerances, which limits broad deployment but creates high-value specification opportunities in power generation and heavy industry.

Others in the product type category include specialized formats such as proximity probes and tachometers used in niche industrial configurations. These products serve legacy equipment and custom OEM applications where standard accelerometer or velocity sensor formats do not meet mechanical constraints.

Technology Analysis

Piezoresistive sensors dominate with 31.2% due to proven reliability in harsh industrial environments.

In 2025, Piezoresistive sensors held a dominant market position in the By Technology segment of the Vibration Sensor Market, with a 31.2% share. Their resistance-based signal generation performs consistently across wide temperature and pressure ranges, which explains their sustained preference in automotive, oil and gas, and power generation end markets. This structural advantage limits the near-term displacement potential of newer sensing technologies.

Strain Gauge technology differentiates through its ability to measure both static and dynamic forces simultaneously, making it valuable in structural health monitoring and aerospace applications where load and vibration data must be captured together. However, its higher sensitivity to environmental drift means calibration requirements add operational cost.

Variable Capacitance sensors operate effectively at low frequencies and in high-precision positioning applications, where piezoresistive alternatives lose resolution. Their MEMS-compatible design structure positions them well for next-generation miniaturized sensor platforms targeting consumer electronics and smart devices.

Hand Probe devices serve portable, non-continuous monitoring applications where permanently installed sensors are not justified by equipment criticality or cost. Maintenance technicians rely on these for periodic route-based condition checks across large equipment fleets.

Optical Sensors differentiate through their immunity to electromagnetic interference, positioning them for specialist applications in high-voltage environments such as power generation switchgear and electrical substations where conventional sensors produce unreliable readings.

Tri-Axial Sensors capture vibration data across X, Y, and Z axes in a single installation, reducing sensor count per monitoring point. This efficiency advantage drives their adoption in smart factory automation where installation cost and data density per mounting point directly affect system economics.

Others in the technology segment include emerging formats such as MEMS-based capacitive and resonant frequency sensors being developed for ultra-low-power IoT node applications. These represent an early-stage technology pipeline rather than a current volume driver.

Material Analysis

Doped Silicon dominates with 40.4% due to semiconductor manufacturing scale and MEMS compatibility.

In 2025, Doped Silicon held a dominant market position in the By Material segment of the Vibration Sensor Market, with a 40.4% share. Its compatibility with MEMS fabrication processes allows manufacturers to achieve high-volume, low-cost production with tight dimensional tolerances. This manufacturing advantage compounds over time, creating a cost floor that alternative materials currently cannot match at scale.

Piezoelectric Ceramics deliver the highest energy output per vibration event within the material segment, making them the preferred substrate for high-sensitivity industrial accelerometers and energy harvesting applications. Their established position in condition monitoring for heavy rotating machinery creates a stable and recurring demand base.

Quartz differentiates through its exceptional temperature stability and repeatability, earning specification preference in aerospace, defense, and precision metrology applications. However, its higher material and machining cost relative to doped silicon limits its use to high-specification segments where performance requirements justify the price premium.

End Use Industry Analysis

Automotive and Transportation dominates with 30.2% due to mandatory sensor integration in safety systems.

In 2025, Automotive and Transportation held a dominant market position in the By End Use Industry segment of the Vibration Sensor Market, with a 30.2% share. OEM-level integration of vibration sensors into powertrain diagnostics, active suspension, and ADAS systems embeds demand at the vehicle design stage — making automotive the most structurally reliable end market for sensor volumes over the forecast period.

Aerospace represents the highest per-unit value application within the end use segment, where structural fatigue monitoring on airframes and propulsion vibration analysis demand sensors certified to extreme reliability standards. Lower unit volumes are offset by premium pricing and long contract lifecycles.

Pulp and Paper facilities rely on continuous vibration monitoring of high-speed rollers, dryers, and pump systems to prevent costly production interruptions. Their asset base runs at near-constant throughput, creating persistent demand for ruggedized sensors that perform in high-moisture, chemically aggressive environments.

Food and Beverage plants deploy vibration monitoring to maintain hygiene compliance and prevent contaminant risk from mechanical degradation. Regulatory requirements around food safety add a compliance dimension to condition monitoring investment, reinforcing sensor adoption beyond pure cost justification.

Oil and Gas, Refining, and Petrochemicals operate some of the most asset-intensive and hazard-exposed equipment in any industry, where unmonitored mechanical failure carries both financial and safety consequences. Vibration sensors here face the strictest installation and certification requirements, raising barriers for new market entrants.

Power Generation facilities use vibration monitoring across turbines, generators, and cooling systems where even brief unplanned outages create substantial revenue loss. The shift toward renewable energy sources — particularly wind — extends this market into new installation categories with different sensor requirement profiles.

Others include defense, construction, semiconductor fabrication, and marine applications where vibration monitoring addresses specialized structural or equipment health requirements. These segments individually represent smaller volumes but collectively sustain demand for custom and application-specific sensor configurations.

Key Market Segments

By Product Type

- Accelerometers

- Velocity Sensor

- Displacement Sensor

- Others

By Technology

- Piezoresistive

- Strain Gauge

- Variable Capacitance

- Hand Probe

- Optical Sensor

- Tri-Axial Sensors

- Others

By Material

- Doped Silicon

- Piezoelectric Ceramics

- Quartz

By End Use Industry

- Automotive & Transportation

- Aerospace

- Pulp and Paper

- Food and Beverage

- Oil and Gas, Refining, Petrochemicals

- Power Generation

- Others

Drivers

Predictive Maintenance Adoption and Industrial Automation Integration Drive Vibration Sensor Deployment Across Asset-Intensive Industries

Manufacturing plants, oil and gas facilities, and power generation operators have shifted from scheduled maintenance cycles toward condition-based strategies that depend on real-time vibration data. This transition creates a direct, recurring hardware requirement for vibration sensors at every critical asset monitoring point — converting a one-time capital purchase into a repeating deployment cycle. According to Dr. Shruti Bhat, IoT sensors monitoring real-time health metrics including vibration reduced equipment downtime by 25% at a machinery manufacturer. That outcome directly quantifies the operational ROI that now drives procurement decisions at plant and operations director level.

Smart factory infrastructure and industrial automation systems treat vibration monitoring as a baseline capability rather than an optional upgrade. As automation density increases — more motors, conveyors, robotics, and pumps per square meter — the number of monitoring points multiplies. Consequently, every new automated line added to a facility represents a new sensor demand cluster, compounding market volumes without requiring entirely new customers.

Rotating machinery including motors, turbines, pumps, and compressors generates the highest concentration of sensor demand within industrial facilities. In December 2024, Wilcoxon Sensing Technologies announced a strategic partnership with KCF Technologies to integrate vibration sensor data directly into predictive maintenance platforms — a move that shortens the data-to-decision chain and lowers the expertise barrier for plant operators running condition monitoring programs. This integration trend accelerates deployment timelines for new sensor installations.

Restraints

High System Costs and Technical Complexity Limit Vibration Monitoring Adoption Among Mid-Market and Smaller Industrial Operators

Advanced industrial vibration monitoring systems require specialized installation, precise calibration, and ongoing signal interpretation — each step adding cost beyond the sensor hardware itself. For smaller manufacturers and mid-tier industrial operators, the total system investment frequently exceeds budget thresholds for maintenance capital expenditure. This cost barrier concentrates adoption among large enterprises with dedicated reliability engineering teams, slowing overall addressable market penetration.

Interpreting vibration data for accurate fault diagnosis demands technical expertise that many plant operators do not have in-house. Without skilled analysts, raw vibration signals produce limited actionable output — reducing the perceived ROI of the system and increasing reliance on third-party service providers. This dependency adds recurring cost and creates hesitation at the point of initial investment decision.

According to Dr. Shruti Bhat, maintenance costs decreased by 15% in a case study using vibration-monitoring IoT sensors — a meaningful saving, but one that requires months of data collection before the benefit materializes. For operators with short capital payback requirements, deferred savings profiles reduce the financial attractiveness of full-system deployments, particularly when upfront installation and calibration costs are front-loaded against uncertain timelines.

Growth Factors

Wireless IoT Sensors, Renewable Energy Deployment, and MEMS Miniaturization Open New Revenue Channels Across Industrial and Consumer Markets

Industrial IoT-enabled wireless vibration sensors remove the wiring and infrastructure costs that historically limited broad sensor deployment across large facilities. Remote monitoring capability allows operators to cover geographically dispersed equipment — pipelines, offshore platforms, wind farms — without permanent instrumentation runs. In January 2025, TE Connectivity launched its IoT Wireless Vibration Sensors featuring piezoelectric accelerometers, embedded FFT analysis, and up to 10-year battery life, directly addressing the operational cost objection that previously blocked wireless adoption at scale.

Renewable energy infrastructure, particularly wind turbines and hydropower plants, represents a structurally new installation base for vibration monitoring. Wind turbine drivetrains operate under variable load conditions that accelerate mechanical fatigue, making continuous vibration analysis essential for asset life management. According to Path of Science, piezoelectric harvesters on wind turbine blades generated 100 μW to power vibration sensors in an offshore wind farm case study — demonstrating that energy-autonomous sensor operation is achievable in remote renewable installations, eliminating grid power dependency.

Compact MEMS-based vibration sensors are creating demand in consumer electronics, wearables, and smart infrastructure — markets previously outside the industrial sensor addressable base. Structural health monitoring on bridges, railways, and smart city infrastructure adds a new category of long-life, low-power deployment that fits MEMS technical capabilities precisely. This diversification reduces the market’s historical concentration in heavy industry and extends the total addressable sensor population.

Emerging Trends

AI-Integrated Analysis, Wireless Platforms, and Cloud-Connected Monitoring Redefine How Vibration Data Translates Into Operational Decisions

AI-integrated vibration analysis platforms now process sensor signals in real time, moving fault detection from a manual review task to an automated alert system. According to IJRASET, a CNN model using continuous wavelet transform scalograms from vibration signals achieved 99.13% fault classification accuracy — outperforming traditional FFT-based models at 93.8%. This accuracy gap is large enough to materially change maintenance decision quality, and it signals that AI-augmented platforms will progressively replace manual signal interpretation across industrial condition monitoring programs.

The market shift toward wireless and battery-powered vibration monitoring devices reflects a fundamental change in deployment economics. Eliminating hardwired infrastructure cuts installation time and cost, enabling sensor networks to scale across facilities without proportional capital expenditure. In April 2025, Wilcoxon Sensing Technologies released the 883M digital triaxial accelerometer with Modbus protocol support for direct PLC and SCADA integration, confirming that digital-native connectivity has become a standard product specification requirement.

Cloud-based analytics platforms connected to industrial vibration monitoring solutions extend the value of sensor data beyond the plant floor, enabling enterprise-level benchmarking, cross-facility trend analysis, and remote diagnostics. Advancements in MEMS technology continue driving higher sensitivity into smaller form factors, making dense sensor networks more economically viable. Together, these developments compress the timeline from sensor installation to actionable operational insight.

Regional Analysis

Asia Pacific Dominates the Vibration Sensor Market with a Market Share of 28.9%, Valued at USD 1.6 Billion

Asia Pacific holds the largest regional share at 28.9%, valued at USD 1.6 Billion, driven by the concentration of manufacturing output, automotive production, and industrial automation investment across China, Japan, South Korea, and India. The region’s high density of process industries and expanding smart factory programs sustains vibration sensor demand across multiple end-use verticals simultaneously, creating a broad and structurally stable revenue base.

North America Vibration Sensor Market Trends

North America maintains a strong position in the global vibration sensor market, underpinned by mature oil and gas infrastructure, large aerospace manufacturing capacity, and well-developed industrial IoT adoption. The region’s early deployment of condition monitoring programs in power generation and refining has produced an installed base that now generates recurring upgrade and replacement demand alongside new system deployments.

Europe Vibration Sensor Market Trends

Europe’s vibration sensor demand centers on precision manufacturing, aerospace, and energy transition infrastructure including offshore wind farms and grid modernization projects. Germany’s industrial machinery sector and the region’s strong automotive OEM base provide consistent sensor procurement volumes, while regulatory pressure on industrial energy efficiency accelerates condition monitoring adoption across manufacturing facilities.

Latin America Vibration Sensor Market Trends

Latin America represents an earlier-stage but expanding market for vibration sensors, where mining, oil and gas, and agricultural processing industries drive the primary demand base. Brazil and Mexico lead regional deployment, supported by infrastructure investment and increasing technology adoption among industrial operators seeking to reduce unplanned downtime in remote and challenging operating environments.

Middle East and Africa Vibration Sensor Market Trends

The Middle East and Africa market centers on oil and gas refining, petrochemical processing, and power generation — all sectors where equipment failure carries significant financial and safety consequences. GCC countries, particularly Saudi Arabia and the UAE, lead regional investment in asset integrity programs that incorporate vibration monitoring as a core component of facility reliability management.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Baumer positions itself at the intersection of precision sensor engineering and application-specific customization, serving automotive, food processing, and industrial automation markets with a portfolio that spans mechanical, optical, and inductive sensing. Their competitive advantage lies in deep application engineering support — a capability that reduces customer switching risk and maintains long-term supply relationships with OEM accounts across Europe and Asia.

Bosch Sensortec GmbH leverages its parent company’s semiconductor manufacturing infrastructure and automotive-grade quality standards to deliver MEMS-based vibration sensing solutions at consumer electronics and automotive scale. This manufacturing depth enables Bosch Sensortec to compete on cost-per-unit economics that pure-play sensor companies cannot replicate, positioning it as the default supplier for high-volume, cost-sensitive vibration monitoring applications.

TE Connectivity brings a broad connectivity and sensor portfolio that allows it to bundle vibration sensing within larger industrial monitoring system solutions, reducing customer procurement complexity. Their January 2025 launch of the IoT Wireless Vibration Sensor series — featuring embedded FFT analysis and up to 10-year battery life — demonstrates a deliberate shift toward integrated wireless solutions that extend their addressable market beyond traditional wired sensor replacement.

Honeywell International Inc. applies its industrial process control expertise and global service infrastructure to deliver vibration monitoring within broader asset management and safety system platforms. Their strategic positioning targets large enterprise accounts in oil and gas, aerospace, and power generation where integration with existing Honeywell control and analytics platforms reduces implementation risk and creates multi-product account stickiness.

Key Players

- Baumer

- Bosch Sensortec GmbH

- TE Connectivity

- NATIONAL INSTRUMENTS CORP

- Honeywell International Inc.

- SAFRAN

- Hansford Sensors

- DYTRAN INSTRUMENTS INCORPORATED

- Analog Devices, Inc.

- ASC GmbH

- Other Key Players

Recent Developments

- August 2024 – AES Engineering completed the acquisition of Condition Monitoring Services (CMS), a leading provider of vibration monitoring and reliability services across the southwestern United States, expanding its geographic service footprint in industrial condition monitoring.

- December 2024 – Spectris plc completed the acquisition of Piezocryst Advanced Sensorics GmbH, integrating the piezoelectric sensor specialist into its HBK business unit to strengthen its vibration and pressure sensor portfolio.

- December 2024 – Tractian secured $120 million in Series C funding led by Sapphire Ventures to scale its AI-powered vibration sensor analysis and industrial condition monitoring solutions, signaling strong investor confidence in AI-integrated sensing platforms.

- 2024 – Broadsens released the SVT-L series long-range wireless vibration and temperature sensors capable of 1 km transmission range in open space, along with OTA firmware upgrades and auto-acceleration range adjustment on its SVT-V series.

Report Scope

Report Features Description Market Value (2025) USD 5.6 Billion Forecast Revenue (2035) USD 11.6 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Accelerometers, Velocity Sensor, Displacement Sensor, Others), By Technology (Piezoresistive, Strain Gauge, Variable Capacitance, Hand Probe, Optical Sensor, Tri-Axial Sensors, Others), By Material (Doped Silicon, Piezoelectric Ceramics, Quartz), By End Use Industry (Automotive & Transportation, Aerospace, Pulp and Paper, Food and Beverage, Oil and Gas Refining Petrochemicals, Power Generation, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Baumer, Bosch Sensortec GmbH, TE Connectivity, NATIONAL INSTRUMENTS CORP, Honeywell International Inc., SAFRAN, Hansford Sensors, DYTRAN INSTRUMENTS INCORPORATED, Analog Devices Inc., ASC GmbH, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Baumer

- Bosch Sensortec GmbH

- TE Connectivity

- NATIONAL INSTRUMENTS CORP

- Honeywell International Inc.

- SAFRAN

- Hansford Sensors

- DYTRAN INSTRUMENTS INCORPORATED

- Analog Devices, Inc.

- ASC GmbH

- Other Key Players

Our Clients

- 181173

- Mar 2026