Global Veterinary Antiparasitics Market By Product Type (Ectoparasiticides, Endoparasiticides, Endectocides and Others), By Animal Type (Companion Animals and Livestock Animals), By Route of Administration (Oral, Injectable and Topical), By End-User (Veterinary Hospitals and Clinics, Animal Farms and Home Care Settings), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181355

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

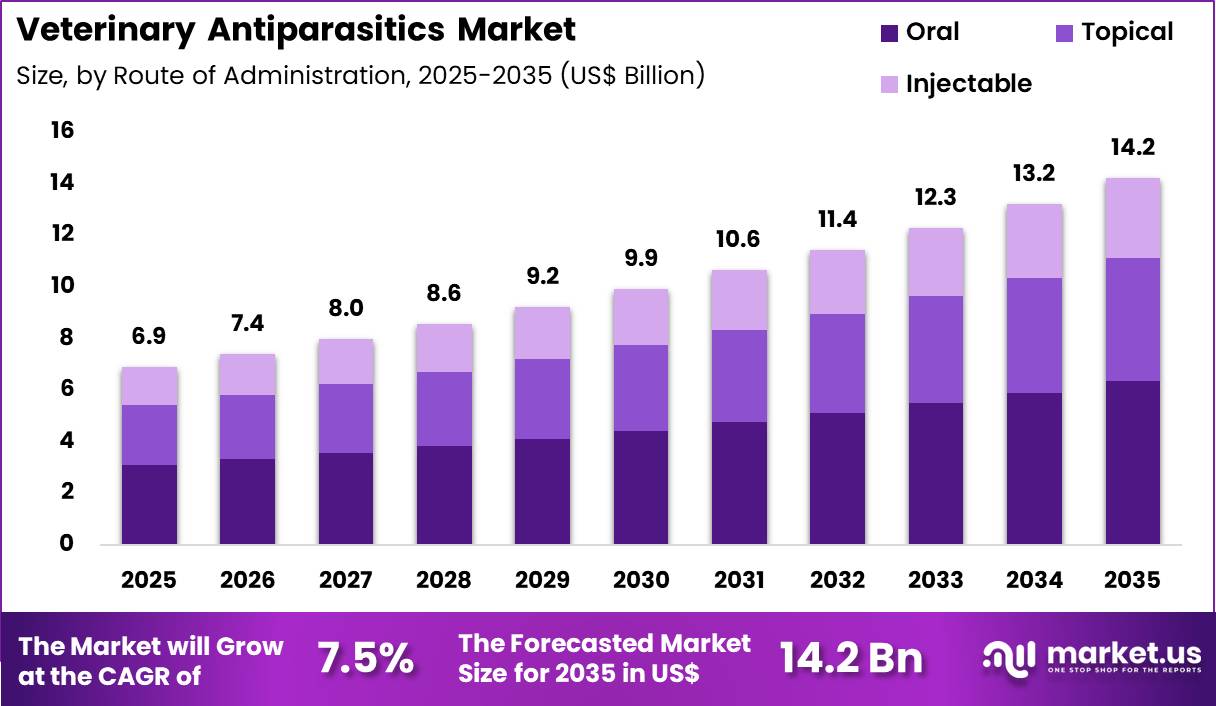

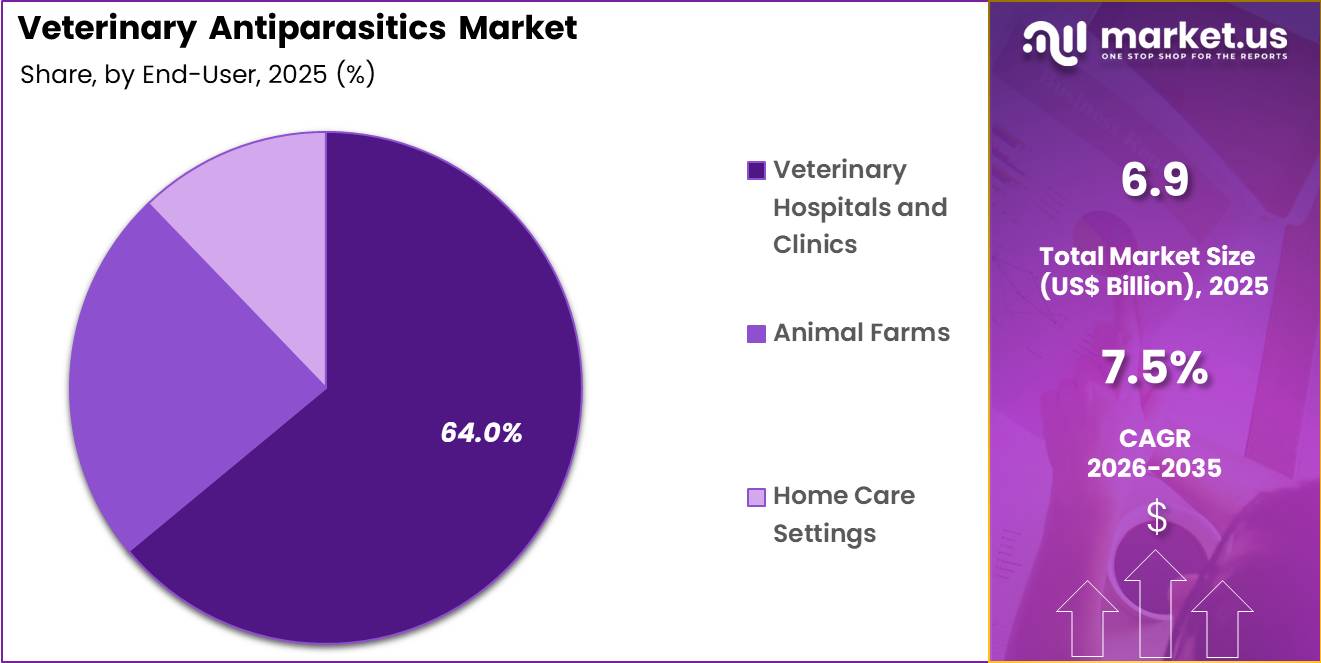

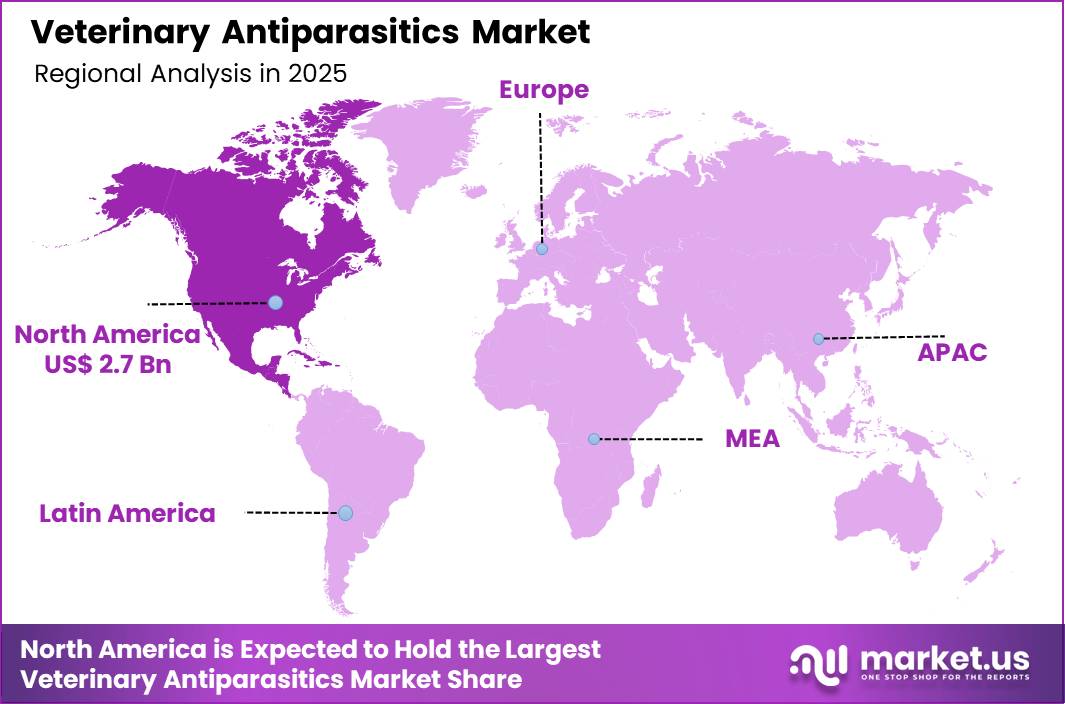

The Global Veterinary Antiparasitics Market size is expected to be worth around US$ 14.2 Billion by 2035 from US$ 6.9 Billion in 2025, growing at a Veterinary Antiparasitics Market during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.6% share with a revenue of US$ 2.7 Billion.

Rising incidence of parasitic infections in companion animals and livestock is strengthening the demand for veterinary antiparasitic therapies across global animal healthcare systems. Parasites such as fleas, ticks, mites, gastrointestinal worms, and heartworms continue to affect the health, productivity, and survival of animals used for companionship, agriculture, and breeding programs.

Veterinary antiparasitic products support prevention and treatment across several applications including dermatological parasite control, gastrointestinal infection management, vector borne disease prevention, and livestock productivity protection. Veterinarians rely on antiparasitic drugs to control infestations that reduce milk yield, meat production, and reproductive efficiency in cattle, sheep, and swine.

Pet owners increasingly seek preventive medications that protect animals from parasites that also threaten human health through zoonotic transmission. Clinics and veterinary hospitals now incorporate routine parasite screening and preventive treatment protocols as part of standard wellness programs Pharmaceutical companies continue to introduce combination therapies that simplify treatment schedules and improve owner compliance.

In January 2025, Zoetis Inc. received expanded label approval from the US FDA for Simparica Trio containing sarolaner, moxidectin, and pyrantel to include the prevention of Borrelia burgdorferi infections. The approval positioned the product as the first oral chewable treatment clinically proven to prevent Lyme disease by killing the vector ticks before transmission occurs. Such innovations strengthen the role of antiparasitic medications as a core component of modern veterinary preventive care.

Growing investment in animal health technologies and preventive veterinary medicine continues to create new opportunities in the veterinary antiparasitics market. Livestock producers increasingly depend on parasite control programs to protect herd health and maintain consistent production levels. Parasite infestations reduce feed efficiency, weaken immune responses, and create costly production losses in commercial farming operations.

Veterinary antiparasitic treatments therefore support disease management strategies that improve livestock productivity and animal welfare outcomes. Companion animal healthcare also demonstrates a shift toward year round parasite prevention supported by veterinary guidance and pet insurance coverage.

Pharmaceutical developers focus on long acting formulations, combination drugs, and convenient delivery formats such as oral chewables, spot on solutions, and extended release injections. Digital veterinary health platforms now encourage preventive care reminders, improving adherence to parasite control regimens.

Veterinary professionals also integrate parasite surveillance with diagnostic screening to detect emerging vector borne diseases at early stages. Increasing awareness of zoonotic disease transmission encourages pet owners and livestock managers to adopt consistent parasite prevention practices. These developments strengthen the commercial and clinical relevance of veterinary antiparasitic products across diverse animal healthcare applications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 6.9 Billion, with a CAGR of 7.5%, and is expected to reach US$ 14.2 Billion by the year 2035.

- The product type segment is divided into ectoparasiticides, endoparasiticides, endectocides and others, with ectoparasiticides taking the lead with a market share of 42.6%.

- Considering animal type, the market is divided into companion animals and livestock animals. Among these, companion animals held a significant share of 64.8%.

- Furthermore, concerning the route of administration segment, the market is segregated into oral, injectable and topical. The oral sector stands out as the dominant player, holding the largest revenue share of 44.6% in the market.

- The end-user segment is segregated into veterinary hospitals and clinics, animal farms and home care settings, with the veterinary hospitals and clinics segment leading the market, holding a revenue share of 64.0%.

- North America led the market by securing a market share of 38.6%.

Product Type Analysis

Ectoparasiticides accounted for 42.6% of growth within product type and dominate the veterinary antiparasitics market due to the widespread prevalence of fleas, ticks, mites, and lice among domestic animals. Veterinary professionals increasingly prioritize ectoparasite prevention because these parasites transmit serious diseases such as Lyme disease and ehrlichiosis.

Companion animals frequently encounter parasite exposure through outdoor activities and interactions with other animals. Veterinary health guidelines therefore emphasize regular parasite prevention programs. According to the Centers for Disease Control and Prevention, tick-borne diseases reported in the United States increased significantly during the past decade, highlighting the growing risk of parasite-related infections.

Veterinary practitioners increasingly prescribe long-acting antiparasitic formulations that improve compliance among pet owners. The segment is expected to strengthen as pharmaceutical companies introduce advanced formulations that provide extended parasite protection and improved safety profiles.

Animal Type Analysis

Companion animals accounted for 64.8% of growth within animal type and dominate the veterinary antiparasitics market due to the rapidly expanding global pet population and rising spending on veterinary healthcare. Dogs and cats frequently require routine parasite prevention as part of preventive veterinary care programs.

Pet owners increasingly invest in parasite control to protect animals from skin disorders, gastrointestinal infections, and vector-borne diseases. The American Pet Products Association reported that pet industry spending exceeded $136 billion in the United States in recent years, demonstrating the growing willingness of owners to invest in animal health.

Veterinarians routinely recommend year-round parasite prevention strategies for companion animals. The segment is projected to grow as urban pet ownership increases and awareness regarding parasite-borne diseases continues to rise across veterinary healthcare systems.

Route of Administration Analysis

Oral administration accounted for 44.6% of growth within route of administration and dominate the veterinary antiparasitics market due to the convenience and accuracy associated with oral dosage formulations. Veterinarians frequently prescribe chewable tablets and flavored oral medications because these products simplify dosing and improve treatment adherence.

Many modern antiparasitic drugs provide broad-spectrum protection against multiple parasites through a single oral dose. Pharmaceutical innovation also improves palatability, which encourages consistent use among pet owners.

Veterinary clinics increasingly recommend oral products that deliver extended parasite protection for several weeks or months. The segment is anticipated to expand as manufacturers develop new systemic antiparasitic medications that provide faster absorption and improved parasite elimination. Growing preference for convenient preventive treatments further strengthens adoption of oral formulations.

End-User Analysis

Veterinary hospitals and clinics accounted for 64.0% of growth within end users and dominate the veterinary antiparasitics market due to their role as primary providers of animal healthcare services. Veterinarians diagnose parasitic infections and prescribe targeted treatment protocols during routine examinations and preventive care visits.

Hospitals and clinics also conduct diagnostic testing to confirm parasite infestations and evaluate treatment effectiveness. These facilities educate pet owners regarding parasite prevention schedules and appropriate medication use.

According to veterinary care statistics reported by professional veterinary organizations, millions of pets visit veterinary clinics annually for preventive healthcare services. This steady patient flow supports consistent demand for antiparasitic products. The segment is expected to expand as veterinary clinics adopt preventive healthcare models that emphasize regular parasite control and disease prevention programs.

Key Market Segments

By Product Type

- Ectoparasiticides

- Endoparasiticides

- Endectocides

- Others

By Animal Type

- Companion Animals

- Livestock Animals

By Route of Administration

- Oral

- Injectable

- Topical

By End-User

- Veterinary Hospitals and Clinics

- Animal Farms

- Home Care Settings

Drivers

Rising companion animal parasiticides sales are driving the market.

Zoetis Inc. reported strong performance in its companion animal parasiticides portfolio during the fourth quarter of 2025. The Simparica franchise and ProHeart product lines demonstrated continued growth momentum. International companion animal parasiticides achieved a 4% operational increase in the fourth quarter of 2025 compared to the corresponding period in 2024.

The Simparica Trio product expanded through additional label indications and market approvals, including Brazil. Companion animal parasiticides benefited from sustained demand for comprehensive protection against fleas, ticks, heartworms, and intestinal parasites. The portfolio includes established brands such as Revolution alongside newer combination formulations addressing multiple parasite classes.

Veterinary recommendations increasingly emphasize year-round preventive protocols to mitigate zoonotic transmission risks. The revenue contribution from these products supports ongoing lifecycle management and promotional activities. The driver reflects heightened owner awareness of parasite-related health threats. This factor maintains consistent forward momentum in the companion animal segment.

Restraints

Emergence of resistance in key parasite populations is restraining the market.

Resistance patterns in heartworm, flea, and tick populations have reduced the perceived efficacy of certain antiparasitic classes in specific geographic regions. Veterinary practitioners report increasing treatment failures with previously effective macrocyclic lactones against heartworm in certain endemic areas. The restraint necessitates more frequent rotation of active ingredients and combination therapies.

Manufacturers face challenges in demonstrating long-term product effectiveness under field conditions. The factor contributes to cautious prescribing practices and reduced prophylactic compliance among pet owners. Diagnostic testing for resistance markers remains limited in routine veterinary practice.

The dynamic moderates growth expectations for single-class parasiticides. Supply chain participants encounter pressure to develop novel chemical entities. This element constrains overall market expansion in mature segments during recent years. The limitation persists in influencing therapeutic decision-making across endemic zones.

Opportunities

Development of novel combination parasiticides with extended duration is creating growth opportunities.

Recent product advancements focus on formulations combining multiple active ingredients to address broader parasite spectra with prolonged efficacy intervals. These developments target improved owner compliance through reduced administration frequency. Opportunities arise for differentiation in competitive markets through superior duration of protection.

The approach supports expanded indications covering emerging parasite challenges. Veterinary practices gain options for integrated preventive protocols in multi-pet households. The framework facilitates value-based pricing emphasizing long-term cost-effectiveness. Manufacturers can pursue additional regulatory approvals for combination claims.

Such innovations enable penetration into segments previously limited by frequent dosing requirements. The opportunity fosters partnerships with diagnostic laboratories for resistance monitoring. This advancement strengthens portfolio resilience and therapeutic relevance.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the veterinary antiparasitics market through livestock profitability, pet care spending, and veterinary clinic purchasing decisions. Inflation raises costs for active ingredients, formulation chemicals, packaging materials, and distribution logistics, which increases production expenses for manufacturers.

Higher interest rates limit investment by animal health companies and reduce discretionary spending by farmers and pet owners. Geopolitical tensions disrupt global supply chains for pharmaceutical intermediates and veterinary drug ingredients, creating sourcing uncertainty for producers.

Current US tariffs on imported chemical compounds and pharmaceutical inputs increase procurement costs and compress supplier margins. These pressures can slow product expansion and limit price flexibility in cost-sensitive livestock markets.

At the same time, manufacturers strengthen domestic sourcing strategies and expand regional production capacity to ensure supply stability. Rising awareness of parasite control, animal productivity, and preventive veterinary care continues to support steady and confident market growth.

Latest Trends

Regulatory approval of new-generation heartworm preventives is driving the market.

The U.S. Food and Drug Administration granted approval to a novel monthly injectable heartworm preventive in late 2025 for dogs. This product provides 12-month protection following a single administration. The approval covers extended efficacy against Dirofilaria immitis larvae.

The development addresses compliance challenges associated with monthly oral or topical alternatives. Veterinary professionals benefit from reliable protection in high-risk geographic areas. The 2025 milestone aligns with ongoing efforts to reduce heartworm incidence through sustained preventive coverage. Facilities report potential improvements in patient adherence metrics.

The innovation supports educational campaigns on long-acting prophylaxis. Early adoption demonstrates consistent efficacy in clinical evaluations. Overall, this regulatory advancement elevates standards for heartworm prevention in companion animal practice.

Regional Analysis

North America is leading the Veterinary Antiparasitics Market

North America accounted for 38.6% of the veterinary antiparasitics market in 2025 as veterinarians and livestock producers increased use of preventive parasite control programs to protect animal health and productivity. Companion animal ownership and intensive livestock farming across the United States and Canada have created strong demand for treatments that control internal and external parasites.

According to the American Veterinary Medical Association, about 66% of U.S. households owned a pet in 2023, reflecting a large population of companion animals that regularly receive parasite prevention treatments. Veterinary clinics increasingly recommend routine deworming and flea or tick control programs to reduce disease transmission and improve animal welfare.

Livestock producers also rely on antiparasitic medicines to protect herd health and maintain production efficiency in cattle, sheep, and poultry farming operations. Veterinary pharmaceutical companies are introducing long-acting formulations and combination products that provide extended parasite protection.

Regulatory oversight and veterinary guidelines have strengthened preventive health practices for companion animals and farm animals. Veterinary hospitals and animal health networks are expanding diagnostic screening programs that detect parasitic infections earlier. These factors collectively supported steady growth of veterinary parasite control treatments across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong expansion during the forecast period as livestock production and companion animal ownership increase across the region. Countries such as China, India, and Australia maintain large populations of cattle, poultry, and small ruminants that require consistent parasite control to protect agricultural productivity.

The Food and Agriculture Organization reports that Asia accounts for a significant share of the world’s livestock population, highlighting the importance of veterinary health programs that manage parasitic diseases affecting food producing animals. Governments across the region are strengthening veterinary disease surveillance programs and expanding vaccination and parasite control campaigns in rural farming communities.

Growing urbanization and rising disposable income are also encouraging pet ownership and preventive veterinary care in major cities. Veterinary hospitals and mobile veterinary services are improving access to parasite control treatments for animals in both urban and rural areas.

Pharmaceutical manufacturers are developing region specific formulations designed to address parasites common in tropical and subtropical climates. Veterinary education institutions are strengthening training programs focused on parasitology and herd health management. These developments are expected to accelerate adoption of parasite prevention therapies throughout Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Veterinary Antiparasitics Market drive growth by developing broad-spectrum parasite control products, expanding preventive care programs, and strengthening collaborations with veterinary clinics and livestock producers. Companies invest in research to create longer-lasting formulations that protect animals against ticks, fleas, worms, and other internal and external parasites.

They also expand distribution through veterinary hospitals, farm supply channels, and digital veterinary pharmacies to improve product accessibility for animal owners. Zoetis Inc. represents a major participant in the Veterinary Antiparasitics Market and operates as a global animal health company headquartered in the United States that develops vaccines, medicines, and diagnostic solutions for livestock and companion animals.

The company maintains a strong portfolio of antiparasitic treatments designed to improve animal health and productivity. Industry competitors continue to pursue product innovation, regulatory approvals, and veterinary partnerships to expand preventive parasite management solutions worldwide.

Top Key Players

- Zoetis Inc.

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc.

- Virbac

- Ceva Santé Animale

- Dechra Pharmaceuticals PLC

- Vetoquinol S.A.

- Norbrook Laboratories Ltd.

- Animalcare Group plc

- Biogénesis Bagó

- Petmedica

Recent Developments

- In July 2025, Boehringer Ingelheim Animal Health launched NexGard Plus, a monthly beef-flavored chewable for dogs. According to the company, the product combines afoxolaner, moxidectin, and pyrantel, providing a streamlined treatment protocol that addresses fleas, ticks, heartworm, roundworms, and hookworms in a single monthly dose.

- In March 2026, Elanco Animal Health announced a global strategic partnership to scale the distribution of Credelio Quattro. As per the development report, this next-generation parasiticide is engineered to protect against 100% of common parasite threats, including tapeworms and whipworms, targeting the rising demand for comprehensive, single-tablet preventative care.

Report Scope

Report Features Description Market Value (2025) US$ 6.9 Billion Forecast Revenue (2035) US$ 14.2 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Ectoparasiticides, Endoparasiticides, Endectocides and Others), By Animal Type (Companion Animals and Livestock Animals), By Route of Administration (Oral, Injectable and Topical), By End-User (Veterinary Hospitals and Clinics, Animal Farms and Home Care Settings) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co., Inc., Virbac, Ceva Santé Animale, Dechra Pharmaceuticals PLC, Vetoquinol S.A., Norbrook Laboratories Ltd., Animalcare Group plc, Biogénesis Bagó, Petmedica. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Veterinary Antiparasitics MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Veterinary Antiparasitics MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Zoetis Inc.

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc.

- Virbac

- Ceva Santé Animale

- Dechra Pharmaceuticals PLC

- Vetoquinol S.A.

- Norbrook Laboratories Ltd.

- Animalcare Group plc

- Biogénesis Bagó

- Petmedica

Our Clients

- 181355

- March 2026