Quick Navigation

Report Overview

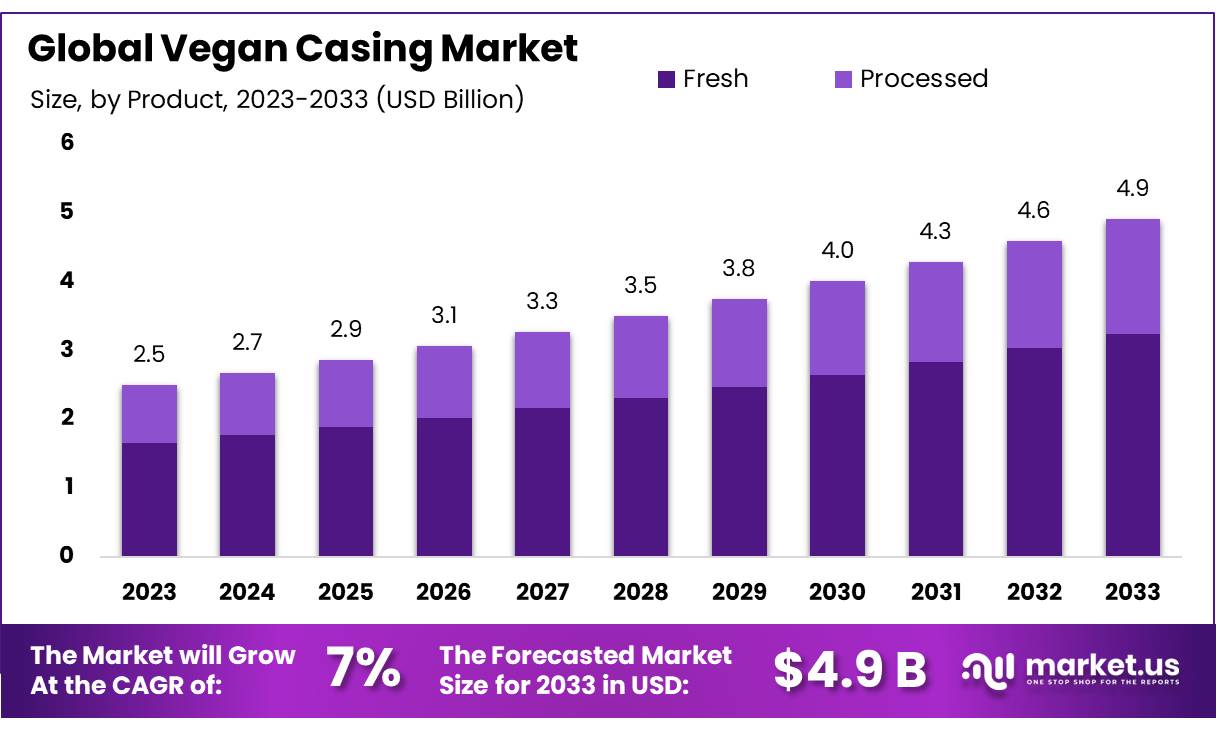

The Global Vegan Casing Market size is expected to be worth around USD 4.9 Bn by 2033, from USD 2.5 Bn in 2023, growing at a CAGR of 7.0% during the forecast period from 2024 to 2033.

Vegan casing refers to a type of food packaging or casing material made from plant-based ingredients, designed as an alternative to traditional animal-derived casings, such as those made from collagen (often sourced from animal intestines).

Vegan casings are commonly used in the production of plant-based sausages, deli meats, and other plant-based protein products, offering a sustainable and ethical option for the growing demand for vegan and vegetarian food. These casings are typically made from a variety of plant-based materials, such as seaweed, cellulose, or soy, and are designed to mimic the texture and appearance of traditional casings while being fully vegan-friendly.

The demand for vegan casings is heavily driven by the growing popularity of plant-based food, particularly in meat alternatives. According to the Plant Based Foods Association, the plant-based food market in the U.S. reached $7.4 billion in 2022, with plant-based meat alternatives accounting for $1.9 billion of that.

On the import-export side, the global trade in vegan food products has been expanding. According to UN Comtrade, the global export of vegan food products grew by 6.2% in 2022, with North America and Europe being the primary exporters. Vegan casings, often sourced from specialized suppliers in Europe and North America, are exported globally to meet the increasing demand in regions like Asia-Pacific and Latin America.

The market for vegan casings has attracted significant investments from both private and government sources. In 2023, Oatly, a leader in plant-based food, received a $200 million investment from BlackRock and Temasek Holdings to expand its production of plant-based products, including vegan casings. Additionally, in 2022, the German government announced a $50 million initiative to fund innovations in plant-based food production, which is expected to increase demand for vegan casings in the region.

Several companies have been innovating in the vegan casing space, with some notable acquisitions and partnerships. For instance, in 2023, Vegan Food Co. acquired Green Casing Solutions for $25 million, expanding its product portfolio in vegan casing technology.

Additionally, The Plant-Based Foods Association reported a 32% increase in the number of plant-based product innovations in 2023 alone, including new vegan casing formulations that offer better texture and durability.

Governments worldwide have been supporting the growth of plant-based and vegan products, including vegan casings, through various regulations and initiatives. The European Union has set ambitious targets to reduce meat consumption by promoting plant-based alternatives under its Farm to Fork Strategy. The U.S. has also seen favorable policies, such as the 2023 Farm Bill, which includes provisions for plant-based protein research and development.

Key Takeaways

- Vegan Casing Market size is expected to be worth around USD 4.9 Bn by 2033, from USD 2.5 Bn in 2023, growing at a CAGR of 7.0%.

- Fresh vegan casings held a dominant market position, capturing more than a 66.1% share.

- natural vegan casings held a dominant market position, capturing more than a 57.1% share.

- 20-26mm caliber segment held a dominant market position, capturing more than a 38.2% share.

- plant-based vegan casings held a dominant market position, capturing more than a 58.4% share.

- sausage held a dominant market position in the vegan casing market, capturing more than a 47.1% share.

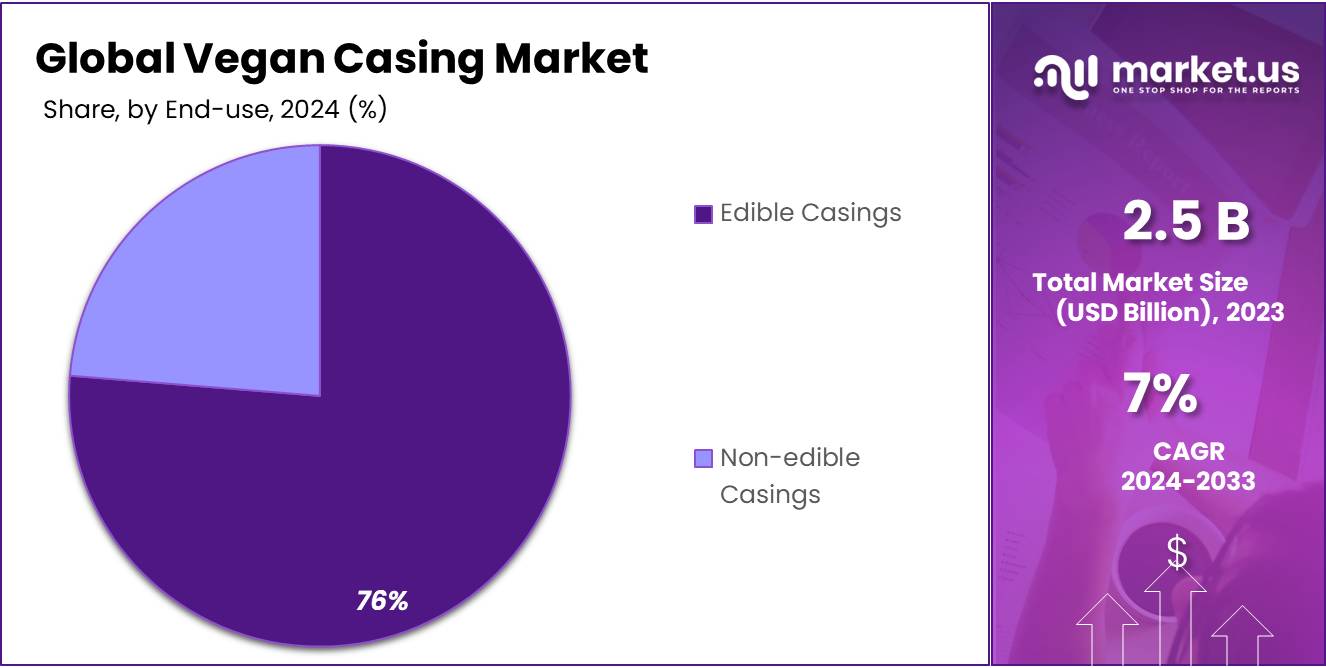

- edible casings held a dominant market position in the vegan casing market, capturing more than a 74.4% share.

- hypermarkets/supermarkets held a dominant market position in the vegan casing market, capturing more than a 44.4% share.

By Product Type

In 2023, Fresh vegan casings held a dominant market position, capturing more than a 66.1% share. This segment is highly preferred for its ability to deliver a clean and natural taste, which is essential for fresh sausages and other similar products.

The demand is particularly strong among consumers seeking healthier, plant-based alternatives that do not compromise on texture or flavor. Fresh vegan casings are favored in both retail and food service applications, where the freshness and quality of ingredients are prioritized.

On the other hand, processed vegan casings also play a crucial role in the market. These casings are designed to withstand various cooking processes and have a longer shelf life, making them suitable for a wide range of culinary applications.

The processed segment caters to the needs of fast-paced food service providers and busy consumers looking for convenient, ready-to-cook options. While this segment holds a smaller share of the market, its importance is growing as food manufacturers continue to innovate and expand their range of vegan products.

By Source

In 2023, natural vegan casings held a dominant market position, capturing more than a 57.1% share. These casings are derived from plant-based materials such as seaweed, rice paper, and vegetable extracts, making them highly favored for their clean label and eco-friendly qualities.

Natural casings are particularly popular among consumers looking for authentic, wholesome food experiences and manufacturers aiming to meet the rising demand for sustainable packaging solutions. The appeal of natural vegan casings extends across various food sectors, especially in premium products where the quality and origin of ingredients are crucial.

Synthetic vegan casings, although holding a smaller market share, are significant in the industry due to their consistency, strength, and versatility. These casings are engineered from food-grade polymers, offering advantages such as uniformity in size and thickness, which are essential for large-scale production.

Synthetic casings are ideal for creating a wide variety of textures and flavors, catering to the diverse preferences of consumers in the vegan market. As technology advances, the functionality and aesthetic appeal of synthetic casings continue to improve, driving their adoption in more specialized and high-volume applications.

By Product

In 2023, the 20-26mm caliber segment held a dominant market position, capturing more than a 38.2% share of the vegan casing market. This range is widely preferred for producing standard-sized vegan sausages and other similar products, offering an ideal balance of texture, strength, and flexibility. The 20-26mm caliber is commonly used in both retail and food service applications due to its versatility and ability to meet the demands of mass production.

The below 20mm caliber segment also plays a significant role, catering to products like snack-sized sausages and plant-based hot dogs. Although it holds a smaller share compared to the 20-26mm segment, the demand for smaller calibers is growing as consumers seek more portable, convenient vegan options for on-the-go consumption.

The 26-32mm caliber is favored for larger vegan sausage products, often used in premium and gourmet offerings. This segment appeals to the growing trend of plant-based alternatives in the high-end food market, where size and presentation are key factors. While it holds a smaller portion of the overall market, it continues to expand as innovation in plant-based foods evolves.

The above 32mm caliber segment, while representing the smallest share of the market, is emerging as a niche offering for specialty products, such as large vegan roasts or premium plant-based sausages. This segment is expected to grow as demand for diverse plant-based food products increases in both retail and food service channels.

By Type

In 2023, plant-based vegan casings held a dominant market position, capturing more than a 58.4% share of the market. These casings are derived from a variety of plant materials such as soy, pea protein, and potato starch, making them the most widely used option in the industry.

The plant-based segment is particularly popular due to its clean label appeal and alignment with consumer preferences for natural, wholesome ingredients. This segment is especially favored in the production of sausages, hot dogs, and other plant-based meat alternatives, driven by the increasing demand for vegan and vegetarian products.

Algae-based casings are gaining traction due to their sustainability and unique properties. Derived from seaweed and other algae, these casings offer excellent moisture retention and a natural, biodegradable alternative to traditional casing materials.

While algae-based casings hold a smaller market share compared to plant-based options, their popularity is growing as consumers and manufacturers alike seek more environmentally friendly and innovative packaging solutions.

Cellulose-based casings, though holding a smaller share in the market, are valued for their versatility and durability. These casings, made from plant fibers, are commonly used in both the vegan and non-vegan sausage industries.

They provide strength and a uniform texture, making them ideal for high-volume production. As the demand for plant-based products increases, cellulose-based casings are expected to grow, particularly in specialty products that require added functionality and structure.

By Application

In 2023, sausage held a dominant market position in the vegan casing market, capturing more than a 47.1% share. This segment is the largest driver of demand for vegan casings, as plant-based sausages continue to gain popularity worldwide.

Vegan sausages are commonly produced using various plant-based proteins, and the use of vegan casings ensures that these products meet the growing consumer demand for sustainable, animal-free options. The versatility of vegan sausages, available in a wide range of flavors and styles, further contributes to the dominance of this segment.

The hot dog segment also plays a significant role, although it holds a smaller share compared to sausages. Vegan hot dogs are becoming increasingly popular due to their convenience and the growing trend of plant-based diets. As more consumers look for meat-free alternatives, vegan hot dogs made with sustainable casings are gaining a solid market presence, particularly in North America and Europe.

The salami and chorizo segments, while smaller, are emerging as key growth areas in the vegan casing market. As the demand for vegan versions of traditional meats rises, manufacturers are developing plant-based alternatives that replicate the texture and flavor of classic salami and chorizo. The ability to create these products with innovative vegan casings is crucial for meeting consumer expectations for authentic taste and appearance.

By End Use

In 2023, edible casings held a dominant market position in the vegan casing market, capturing more than a 74.4% share. These casings are designed to be consumed along with the product, making them a key choice for plant-based sausages, hot dogs, and other vegan meat alternatives.

Edible casings are highly valued for their ability to enhance the texture, appearance, and overall eating experience of plant-based foods. As consumer demand for sustainable and clean-label products grows, edible vegan casings offer a convenient, environmentally friendly solution for manufacturers in the food industry.

Non-edible casings, while holding a smaller share, also serve a crucial role, particularly in applications where the casing is removed before consumption. These casings are often used for larger vegan products like vegan roasts or deli slices.

Non-edible casings provide structural support and are essential for maintaining the shape and integrity of the product during production and distribution. As the market for vegan and plant-based foods expands, the use of non-edible casings is expected to grow, particularly in the processing of specialized products that require a more durable casing material.

By Sales Channel

In 2023, hypermarkets/supermarkets held a dominant market position in the vegan casing market, capturing more than a 44.4% share. These large retail chains are the primary shopping destination for consumers looking for plant-based food products, including vegan casings.

The convenience, variety, and wide availability of vegan products in these stores make them the top choice for consumers. Hypermarkets and supermarkets have embraced the growing demand for plant-based options, offering vegan casings in different formats to cater to a broad customer base.

Convenience stores also play an important role in the market, though with a smaller share compared to hypermarkets. These stores attract busy consumers who are looking for quick and easy access to vegan products, including vegan sausages and hot dogs with plant-based casings. As plant-based diets continue to grow in popularity, convenience stores are increasingly stocking vegan alternatives to meet the needs of time-pressed shoppers.

Food specialty stores cater to a niche but growing segment of consumers who are focused on healthy, organic, or gourmet food choices. These stores often offer a more curated selection of vegan products, including premium vegan casings for specialty applications like artisanal sausages. While their market share is smaller, food specialty stores continue to see strong demand from consumers seeking high-quality, plant-based food options.

Online retail is another significant sales channel, offering the convenience of home delivery and a wider range of vegan products. As e-commerce grows, more consumers are turning to online platforms for their vegan food needs, including vegan casings. This channel is expected to continue expanding as consumers prioritize convenience and access to a broader selection of products.

Key Market Segments

By Product Type

- Fresh

- Processed

By Source

- Natural

- Synthetic

By Product

- Below 20mm Caliber

- 20-26mm Caliber

- 26-32mm Caliber

- Above 32mm Caliber

By Type

- Plant-Based

- Algae-Based

- Cellulose-Based

By Application

- Sausage

- Hot Dog

- Salami

- Chorizo

- Others

By End Use

- Edible Casings

- Non-edible Casings

By Sales Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Food Specialty Stores

- Online Retail

- Others

Drivers

Health Consciousness and Dietary Shifts

A primary factor behind the growing popularity of vegan casings is the increasing shift in consumer dietary preferences towards plant-based, gluten-free, and lower-fat options. According to a 2023 report by the Plant-Based Foods Association, the plant-based food sector in the U.S. alone was worth approximately $7 billion in 2022, with year-over-year growth of 27%.

This shift has been fueled by rising health concerns related to the consumption of animal-based products, such as increased risks of cardiovascular disease, obesity, and other chronic illnesses. As more consumers opt for healthier alternatives, vegan casings become an attractive option. Vegan casings often carry fewer preservatives and are cholesterol-free, making them a preferable choice for health-conscious individuals.

Additionally, the World Health Organization (WHO) has recognized the negative health effects associated with the consumption of processed meats, which has further accelerated the demand for plant-based alternatives.

This growing demand for health-conscious food options has led manufacturers to invest in the development of innovative vegan casing solutions that offer the same texture and functionality as traditional animal casings.

Environmental Sustainability and Climate Change Concerns

Another major driver behind the adoption of vegan casings is the rising concern over environmental sustainability. The environmental impact of animal agriculture, particularly its role in greenhouse gas emissions, land degradation, and water usage, has come under intense scrutiny.

According to a 2021 report from the United Nations’ Food and Agriculture Organization (FAO), livestock production is responsible for nearly 14.5% of global greenhouse gas emissions. This has prompted consumers and companies alike to reconsider their food choices in favor of plant-based products that have a lower environmental footprint.

Vegan casings, made from renewable plant materials, are considered more sustainable than animal-based casings. For example, the production of seaweed-based casings requires significantly less land and water than animal farming.

A 2022 study published in the journal Science Advances found that plant-based meat alternatives, including vegan casings, have up to 90% lower carbon footprints compared to their animal-based counterparts. With growing concerns about climate change, both consumers and regulatory bodies are pushing for more sustainable food solutions.

This has led food manufacturers to explore plant-based packaging and casing alternatives as part of their corporate sustainability strategies. In fact, major food companies such as Nestlé and Tyson Foods are increasingly incorporating plant-based ingredients into their product lines to align with consumer demands for eco-friendly options.

Ethical Consumerism and Animal Welfare Concerns

Ethical consumerism, particularly regarding animal welfare, is another driving factor behind the increased use of vegan casings. As consumers become more aware of the conditions in which animals are raised for food production, many are turning to plant-based alternatives to avoid supporting industries that exploit animals.

According to a 2022 survey by the European Commission, nearly 60% of EU consumers consider animal welfare when making food purchases, and a similar trend is observed in markets across the U.S. and other regions.

Restraints

Raw Material Sourcing and Cost of Vegan Casings

Vegan casings are typically made from plant-based materials such as cellulose, alginate (from seaweed), or pea protein, all of which require specialized sourcing and processing. For example, the production of cellulose casings, one of the most common vegan alternatives, requires significant energy and labor input to extract and process the cellulose fibers.

A 2022 report from the European Food Safety Authority (EFSA) highlights that the cost of sourcing plant-based materials has been increasing due to growing demand across various industries, including food and bioplastics.

In particular, raw materials like alginate and pea protein are not yet produced in sufficient quantities to meet the rising demand for plant-based products. This supply-demand imbalance drives up costs, which are then passed on to manufacturers and ultimately to consumers.

According to a study by the Food and Agriculture Organization (FAO), the price of alginate increased by approximately 15% between 2020 and 2022 due to the higher demand for sustainable, plant-based alternatives.

Similarly, the cost of cellulose has risen by around 10% over the same period, putting pressure on manufacturers who use these materials in their products. These increased raw material costs make vegan casings more expensive to produce than their traditional counterparts, contributing to higher final product prices and limiting their accessibility in the mass market.

Manufacturing Complexity and Technology Investment

The production of vegan casings is not as straightforward as that of traditional animal-based casings, requiring specialized technology and processes that increase manufacturing costs. For example, the process of creating plant-based casings from cellulose requires a series of chemical and mechanical treatments to ensure they possess the desired texture and functionality.

These treatments are energy-intensive and demand a higher level of technical expertise. As a result, manufacturers need to invest in specialized equipment, which increases the upfront capital costs.

According to the U.S. Department of Agriculture (USDA), the capital expenditure for setting up a plant that produces vegan casings can be as much as 30% higher than that for traditional casing production plants. This includes the costs of advanced machinery for processing plant-based materials and the associated energy consumption.

In fact, some companies in the vegan casing space have reported that initial investment in technology and R&D to create high-quality, marketable products can take several years to break even, which can be a significant deterrent for smaller companies entering the market.

Consumer Price Sensitivity and Market Penetration Challenges

The higher production costs for vegan casings directly translate into higher retail prices for the end consumer. While plant-based products have been growing in popularity, price sensitivity remains a significant hurdle for mass market adoption.

According to data from the UK’s National Farmers’ Union (NFU), 40% of consumers in the UK stated that price was the main factor influencing their decision to purchase plant-based food alternatives. In the case of vegan sausages and other products that use vegan casings, the price premium can be substantial—often 20-30% more expensive than their meat-based counterparts.

This price gap can limit the accessibility of vegan products to the broader population, especially in lower-income segments where price sensitivity is particularly high. As a result, while the demand for vegan products is growing, manufacturers are facing difficulties in scaling up production to lower prices, which could hinder market penetration in the long run.

To address this, some companies are looking for cost-reducing strategies, such as collaborating with ingredient suppliers to secure bulk raw material deals or investing in more efficient production methods. However, overcoming the cost barrier remains a long-term challenge.

Opportunity

Surge in Plant-Based Food Consumption

The increasing adoption of plant-based diets is one of the primary factors driving the growth of vegan casings. According to the Plant-Based Foods Association, the U.S. plant-based food market was valued at approximately $7 billion in 2022, with a growth rate of 27% from the previous year. As more consumers choose plant-based options for health reasons, sustainability concerns, or animal welfare motivations, the demand for plant-based food products, including vegan sausages and meat substitutes, continues to rise.

Vegan casings play a crucial role in the production of these products, as they offer a sustainable and ethical alternative to traditional animal-based casings. With the global vegan and plant-based food market projected to grow at a compound annual growth rate (CAGR) of 11.9%, the growth of the overall market presents a huge opportunity for vegan casing suppliers to expand their product offerings and reach new consumer segments.

This growing acceptance of plant-based food and ingredients, particularly in Western markets, is expected to fuel demand for vegan casings. As more food companies look to meet consumer expectations for cruelty-free, environmentally friendly products, the availability and innovation in vegan casings are expected to increase. Vegan casings can also be marketed as allergen-free and gluten-free alternatives, further broadening their appeal.

Health and Sustainability Trends

The rising consumer demand for healthier and more sustainable food options is another significant driver for the growth of vegan casings. According to a 2022 report by the Food and Agriculture Organization (FAO), approximately 75% of global food-related greenhouse gas emissions come from the livestock sector. This environmental impact has led many consumers to seek plant-based alternatives.

As plant-based diets have grown in popularity due to their perceived health benefits—such as lower risks of heart disease, diabetes, and certain cancers—vegan casings have become an integral part of plant-based product formulations. Vegan casings are perceived as more eco-friendly and sustainable due to their lower carbon footprint and use of renewable plant-based materials.

Moreover, as more companies and governments aim to reduce their environmental impact, they are increasingly investing in plant-based food production. The European Union, for example, has pledged to cut emissions by 55% by 2030 and has encouraged sustainable food systems through various green initiatives.

These shifts in policy further boost the demand for plant-based products and, by extension, vegan casings. As consumers become more attuned to the environmental and health benefits of plant-based products, the market for vegan casings is expected to see rapid growth.

Government Support and Incentives

Governments around the world are increasingly recognizing the environmental and health benefits of plant-based foods, and several are offering incentives to boost the production of plant-based alternatives. In 2023, the U.K. government announced a £10 million fund to support the development of plant-based food production.

Similarly, the U.S. government is providing grants and research funding to support innovations in sustainable agriculture and plant-based food technologies. These initiatives help lower the barriers to entry for manufacturers of vegan casings, encouraging greater investment in this space.

Trends

Increased Use of Algae and Seaweed-Based Casings

One of the leading innovations in vegan casings is the use of algae and seaweed-based materials. Algae-derived products like agar and alginate are increasingly used as alternatives to traditional animal-based casings.

According to a 2023 report from the Food and Agriculture Organization (FAO), global seaweed production is growing rapidly, with an annual increase of over 6%, driven by its potential for use in food, medicine, and bioplastics. This trend is particularly relevant to the vegan casing market, as alginate and other seaweed derivatives provide excellent properties such as flexibility, water retention, and natural preservation.

In addition to their functional properties, these ingredients also align with the increasing demand for sustainable, eco-friendly food solutions. The growing popularity of seaweed-based casings is also supported by the expanding consumer interest in marine-based, clean-label foods.

The FAO has identified seaweed as a sustainable and renewable resource with significant potential for global food production. The shift toward algae and seaweed-based casings is expected to meet the dual demand for plant-based alternatives and environmentally friendly food ingredients, offering manufacturers new opportunities to enhance their product offerings.

Focus on Clean Label and Natural Ingredients

According to a 2022 study by the European Food Safety Authority (EFSA), clean label products are increasingly becoming a consumer preference, particularly in the European and North American markets. The clean label trend has been driven by rising consumer demand for transparency, as well as concerns over food safety and the environmental impact of synthetic additives.

Manufacturers are responding to this demand by developing vegan casings made from minimally processed, naturally derived ingredients such as cellulose, pea protein, and rice starch. These ingredients offer both functional properties (e.g., elasticity and water retention) and meet the increasing consumer desire for products with fewer artificial components.

For instance, cellulose casings, derived from plant fiber, are growing in popularity due to their natural, biodegradable properties, which make them a more sustainable alternative to synthetic casings. As consumer awareness around food labeling continues to increase, the demand for clean label vegan casings is expected to grow, pushing manufacturers to innovate further in this space.

Regional Analysis

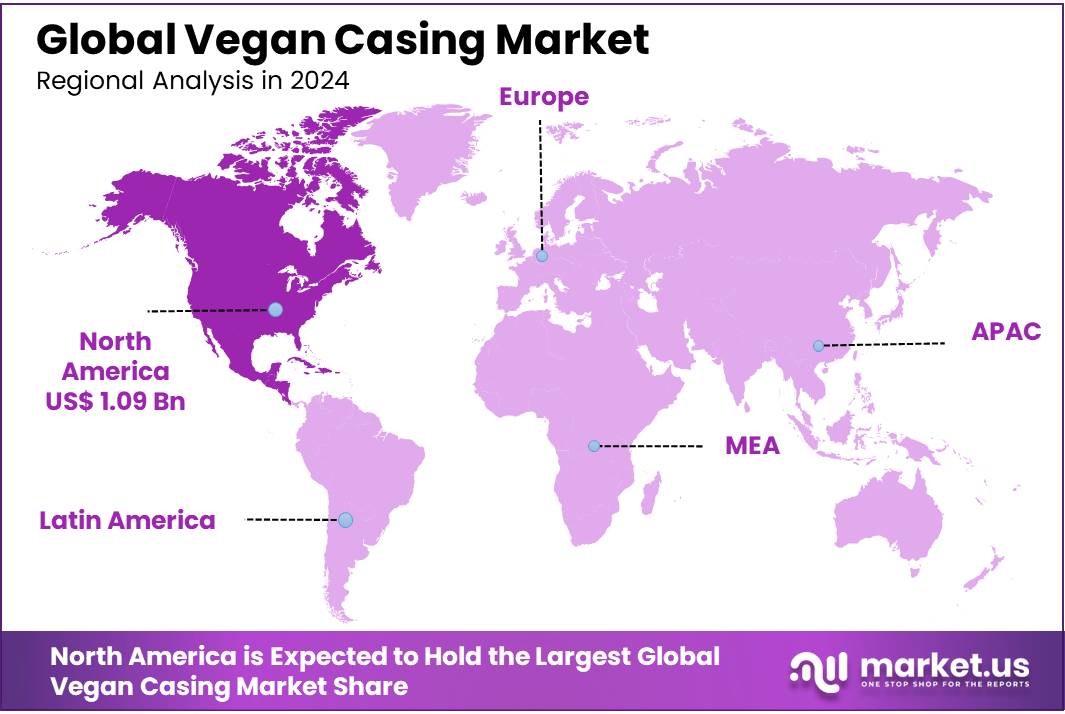

The global vegan casing market is witnessing significant regional growth, driven by shifting consumer preferences towards plant-based alternatives and increasing demand for sustainable food products. Among the key regions, North America holds the dominant share of the vegan casing market, accounting for 42.4% of the total market value, which was approximately USD 1.09 billion in 2023.

This dominance is primarily attributed to the rapidly growing demand for plant-based food products, particularly in the United States and Canada. The plant-based food sector in North America has experienced remarkable growth, with the U.S. market alone reaching a value of over USD 7 billion in 2022, according to the Plant-Based Foods Association. This surge in plant-based consumption is driving the demand for vegan casings, particularly in applications such as plant-based sausages, deli meats, and processed food items.

Europe is another key market for vegan casings, expected to account for a significant share due to increasing consumer awareness about health, sustainability, and ethical food choices. The European vegan food market, valued at approximately USD 6.7 billion in 2022, continues to grow rapidly, fueled by strong demand in countries like Germany, the UK, and France. The shift towards plant-based diets, along with stringent regulations on food labeling and sustainability, is accelerating the adoption of vegan casings in this region.

In the Asia Pacific, the vegan casing market is expanding as countries like China, Japan, and India are increasingly adopting plant-based diets. This region is expected to grow at a CAGR of 8.4% from 2023 to 2030. Meanwhile, Latin America, the Middle East, and Africa are witnessing slower, but steady growth, as these regions gradually embrace plant-based food trends.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The vegan casing market is highly competitive, with several key players driving innovation and product development across different regions. Companies such as ADM, Devro, Viscofan, and Futamura are at the forefront of manufacturing plant-based casings, focusing on sustainable, functional, and cost-effective solutions.

ADM has made significant strides in the food ingredients sector, leveraging its expertise in plant-based products and contributing to the growing market for vegan alternatives. Similarly, Devro, a leading supplier of collagen casings, is expanding its portfolio to include plant-based options, responding to the rising demand for vegan meat alternatives. Viscofan, a global leader in food casings, is also investing in new vegan casing technologies, enhancing its position in the growing plant-based food market.

Other notable players in the vegan casing market include Kalle, Dupont, and Euroduna Food Ingredients GmbH, which are heavily involved in R&D to develop high-quality, biodegradable, and functional vegan casings.

Kalle, known for its expertise in food casings, has been focusing on creating plant-based alternatives that mimic the texture and cooking properties of traditional casings. Dupont and Euroduna are contributing to the market by offering innovative vegan solutions with a strong emphasis on sustainability and cleaner label ingredients.

Regional players such as Chitosen, Envirocore, and Ruitenberg Ingredients B.V. are also carving a niche in the vegan casing market by supplying specialized plant-based ingredients and materials like cellulose, seaweed derivatives, and pea protein.

These companies are increasingly aligning with consumer preferences for eco-friendly and health-conscious alternatives. Smaller but significant players like Smoked and Cured, The Sausage Maker Inc., and Suzy Spoon’s are actively addressing the growing demand for vegan food products in niche markets, contributing to the overall market expansion.

Top Key Players in the Market

- ADM

- Ascona Foods Group

- B. Oliver

- Chitosen

- Devro

- Dunninghams Ltd

- Dupont

- Ennio International

- Envirocore

- Euroduna Food Ingredients GmbH

- Futamura

- High Caliber Products

- Jean Martin Chartier

- Kalle

- Kerry

- Nippi

- Nitta

- Nutra Produkte AG

- PROMAR Sp. z o. o

- Ruitenberg Ingredients B.V.

- Smoked and Cured

- Sonjal Casing (SOREAL)

- Suzy Spoon’s

- The Sausage Maker Inc.

- Viscofan

- Viscofan Group

- Watson Biogenics

- Weschenfelder Direct Ltd

- Wuxi Bio-Technology

Recent Developments

In 2024, ADM’s investment in plant-based solutions is expected to rise by 15-20% year-over-year, demonstrating the company’s commitment to capitalizing on the expanding vegan food market.

In 2024, Ascona Foods is expected to expand its production capacity by 20%, targeting a larger share in the expanding vegan food market, with a projected market value of over USD 500 million in vegan food ingredients by 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.5 Bn |

| Forecast Revenue (2033) | USD 4.9 Bn |

| CAGR (2024-2033) | 7.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Fresh, Processed), By Source (Natural, Synthetic), By Product (Below 20mm Caliber, 20-26mm Caliber, 26-32mm Caliber, Above 32mm Caliber), By Type (Plant-Based, Algae-Based, Cellulose-Based), By Application (Sausage, Hot Dog, Salami, Chorizo, Others), By End Use (Edible Casings, Non-edible Casings), By Sales Channel (Hypermarkets/Supermarkets, Convenience Stores, Food Specialty Stores, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ADM, Ascona Foods Group, B. Oliver, Chitosen, Devro, Dunninghams Ltd, Dupont, Ennio International, Envirocore, Euroduna Food Ingredients GmbH, Futamura, High Caliber Products, Jean Martin Chartier, Kalle, Kerry, Nippi, Nitta, Nutra Produkte AG, PROMAR Sp. z o. o, Ruitenberg Ingredients B.V., Smoked and Cured, Sonjal Casing (SOREAL), Suzy Spoon’s, The Sausage Maker Inc., Viscofan, Viscofan Group, Watson Biogenics, Weschenfelder Direct Ltd, Wuxi Bio-Technology |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |